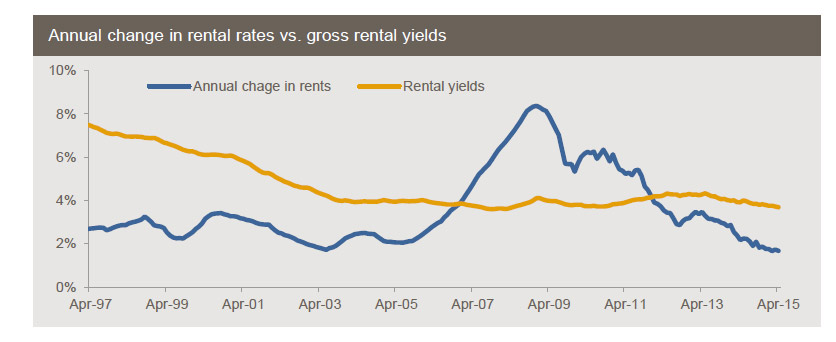

According to analysis from CoreLogic RP Data, rental rates across the combined capital cities increased by 0.1% in April and continue to rise at their slowest annual pace in more than a decade. While rental rates tell part of the story, it is also important to consider rental yields. Rental yields for houses and units are sitting at their lowest level since late 2010. There is a reason for the disconnect between rising house prices and rents. That is simply because rents are more directly linked to average incomes than home values. As we reported recently, income growth is slowing.

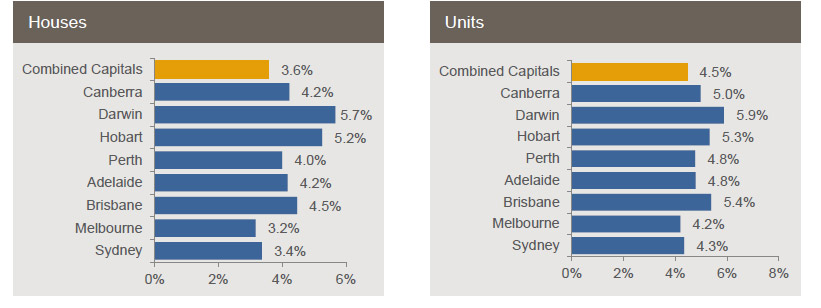

Across the combined capital cities, gross rental yields are recorded at 3.6% for houses and 4.5% for units. At the same time in 2014, gross rental yields were recorded at 3.8% for houses and 4.6% for units. Across the individual capital cities, house rental yields are lowest in Melbourne (3.2%) and Sydney (3.4%) and highest in Darwin (5.7%) and Hobart (5.2%).  Across most cities house rental yields are lower now than they were at the same time last year, the exceptions are Brisbane, Adelaide and Hobart where they are unchanged. At 3.4%, rental yields in Sydney are the lowest they’ve been since May 2005 and at 3.2 per cent Melbourne yields are at their lowest level since November 2010. The unit market shows different trends to the detached housing market with yields higher or unchanged over the year across most cities. Unit yields are lowest in Melbourne (4.2%) and Sydney (4.3%) and highest in Darwin (5.9%) and Brisbane (5.4%). Unit yields in Sydney are at their lowest level since August 2005 while yields in Melbourne have edged higher over the past month.

Across most cities house rental yields are lower now than they were at the same time last year, the exceptions are Brisbane, Adelaide and Hobart where they are unchanged. At 3.4%, rental yields in Sydney are the lowest they’ve been since May 2005 and at 3.2 per cent Melbourne yields are at their lowest level since November 2010. The unit market shows different trends to the detached housing market with yields higher or unchanged over the year across most cities. Unit yields are lowest in Melbourne (4.2%) and Sydney (4.3%) and highest in Darwin (5.9%) and Brisbane (5.4%). Unit yields in Sydney are at their lowest level since August 2005 while yields in Melbourne have edged higher over the past month.

Across the combined capital cities, rental rates are recorded at $487 per week and they have risen by 0.1% over the month, 0.7% over the past three months and by 1.7% over the past 12 months. Although rental rates are still increasing, they are doing so at a moderate rate. In fact, the annual rate of growth has been recorded at 1.7% for four consecutive months and hasn’t previously been this low since June 2003. The slow pace of rental appreciation can likely be attributed to the booming level of dwelling construction coupled with high levels of buying activity from the investment segment which is adding additional rental stock to the market and curtailing rental increases. Looking across the capital cities, over the past year Sydney and Hobart have recorded the greatest increases in weekly rents. Rents have fallen over the past three months in Perth and Darwin; along with Canberra these cities have recorded rental falls over the year, down -4.2%, -4.7% and -2.6% respectively.

Across the combined capital cities, rental rates are recorded at $487 per week and they have risen by 0.1% over the month, 0.7% over the past three months and by 1.7% over the past 12 months. Although rental rates are still increasing, they are doing so at a moderate rate. In fact, the annual rate of growth has been recorded at 1.7% for four consecutive months and hasn’t previously been this low since June 2003. The slow pace of rental appreciation can likely be attributed to the booming level of dwelling construction coupled with high levels of buying activity from the investment segment which is adding additional rental stock to the market and curtailing rental increases. Looking across the capital cities, over the past year Sydney and Hobart have recorded the greatest increases in weekly rents. Rents have fallen over the past three months in Perth and Darwin; along with Canberra these cities have recorded rental falls over the year, down -4.2%, -4.7% and -2.6% respectively.

Looking at the performance of houses as opposed to units there isn’t a great deal of difference in the rates of rental appreciation. House rents were recorded at $492 per week across the combined capital cities in April 2015 compared to $461 per week for units. House rents have recorded stronger growth over the month (0.1%) compared to unit rents which fell by -0.1%. Over the quarter unit rental growth (0.6%) has been lower than houses (0.7%) however, over the past year units have recorded slightly stronger rental growth (1.9%) than houses (1.6%).

Comparing the current rate of rental growth with the 10 year average annual rate of rental appreciation highlights that rental growth is currently sluggish across all cities. In fact, the ten year average annual rate of rental growth is higher than the current growth rate in each capital city. The slower pace of rental growth may be attributed to a number of factors including: a ramp-up in investment purchases resulting in an increase in rental stock, an increase in housing supply which has also added to rental stock and a reduction in net overseas migration decreasing demand for rental stock.

Rental rates are already increasing at their slowest annual rate in more than a decade and the outlook is that a low rate of growth will continue. In fact, with residential construction activity continuing to increase, particularly for inner city units, we would expect that the additional housing supply may result in an even lower rate of rental growth over the coming months. This is likely to be most evident in the markets where new unit supply is surging, being Melbourne and Brisbane and to a lesser extent Sydney.