In the world of microprudential, the status of individual households and their finances becomes ever more important from a risk perspective. We have already shown that some investment property holders are near to the edge, financially speaking, and would be troubled by rising interest rates or a forced conversion from interest only to interest and principle repayments.

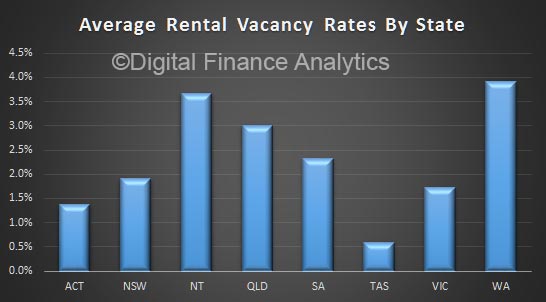

The Basel Committee is pushing towards a requirement for banks’ to hold higher capital where the servicing of the loan is “materially dependent” on regular rental streams. Whilst this might seem arcane when the average vacancy rates are quite low, even now there are significant state variations. Vacancy rates in WA in particular are high.

So using data from our extensive household surveys, we have been looking at the finances of property investors, with the question of servicing the loan in mind should rental streams dry up.

So using data from our extensive household surveys, we have been looking at the finances of property investors, with the question of servicing the loan in mind should rental streams dry up.

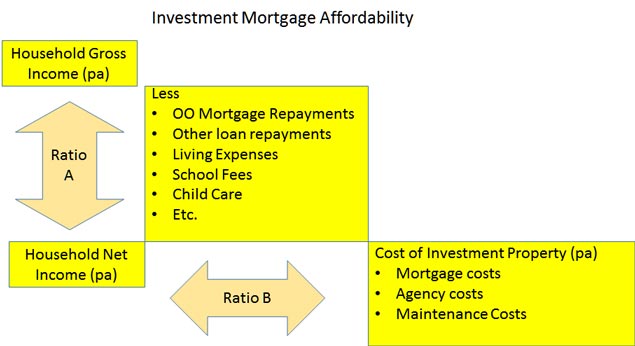

To do this we created a custom data series using the following logic.

We are looking at the available funds, on a cash flow basis after living costs, servicing the OO mortgage (if held) and tax. Next we compared this to the costs of the investment property, again on a cash flow basis.

We are looking at the available funds, on a cash flow basis after living costs, servicing the OO mortgage (if held) and tax. Next we compared this to the costs of the investment property, again on a cash flow basis.

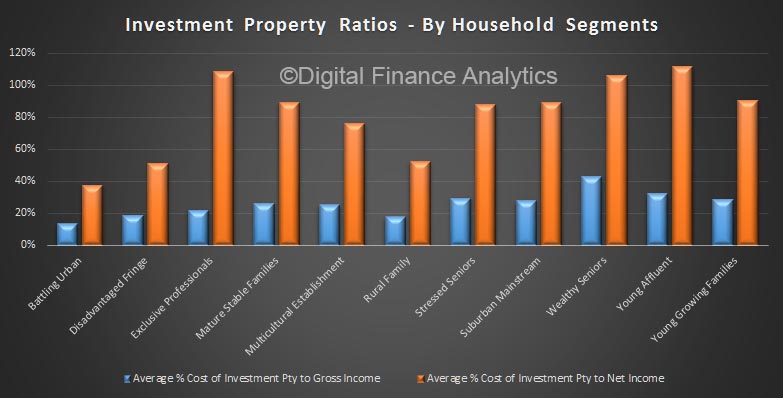

Looking across our household segments, the more affluent households are more likely to find their available funds would not cover the costs of the investment property (all done on an annual basis), whilst those with lower incomes, and who are less affluent are actually better positioned.

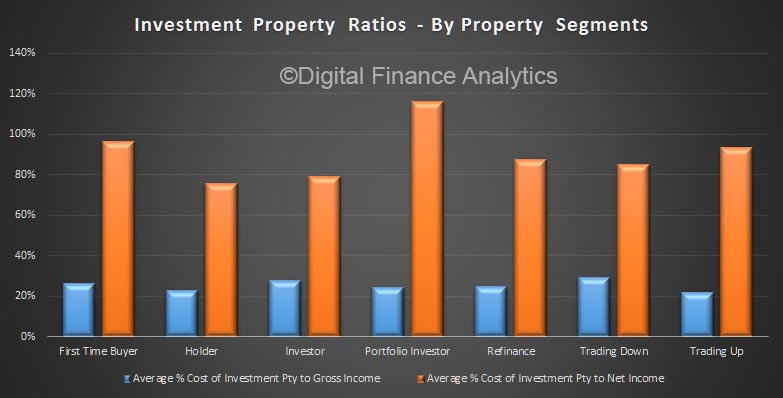

If we cut the data by our property segments, portfolio property investors have the highest exposure, followed by first time buyers.

If we cut the data by our property segments, portfolio property investors have the highest exposure, followed by first time buyers.

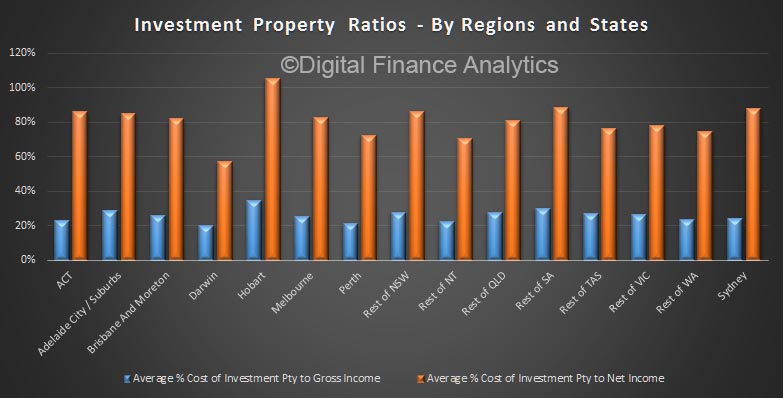

Finally, we can look across the regions, and we find that property investors in Hobart are more exposed (though rental vacancies are lower there) but property investors in NSW also more highly exposed (thanks to larger mortgages compared to income).

Finally, we can look across the regions, and we find that property investors in Hobart are more exposed (though rental vacancies are lower there) but property investors in NSW also more highly exposed (thanks to larger mortgages compared to income).

This alternative way to view the market could become important if differential capital weightings were to be applied. This could move from a theoretical discussion, to one of relative risk-based pricing down the track. Most lenders would not currently differentiate on this basis. Granular data is required to look through this lens.

This alternative way to view the market could become important if differential capital weightings were to be applied. This could move from a theoretical discussion, to one of relative risk-based pricing down the track. Most lenders would not currently differentiate on this basis. Granular data is required to look through this lens.