We have updated our Small Amount Credit Contract (SACC) models to include data to end September 2016. SACC is of course the new name for what were pay day loans, before the last round of regulatory changes. In fact we are still waiting on Government for their response to the review which was completed earlier in the year.

We published detailed analysis of the market last year. The report “The Stressed Finance Landscape” is available here. Our model is based on responses from our household surveys, and we also overlay economic growth factors and other data, to estimate potential future growth.

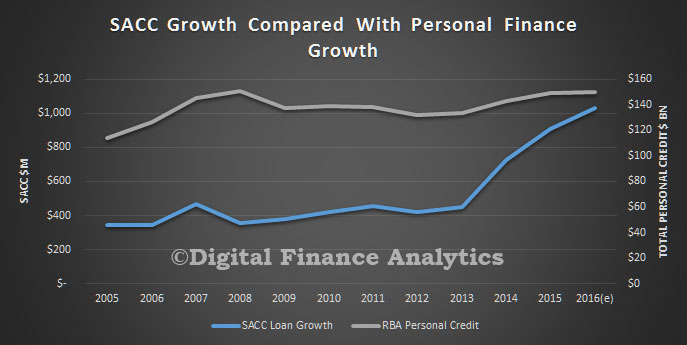

So looking at the new data, our first observation is that growth in SACC loans (under $2,000 and 1 year) is significantly faster than personal credit as reported by the RBA personal credit data. The overall value of these SACC loans is still small, under $1 billion compared with the $145 billion for personal credit (cards and personal loans).

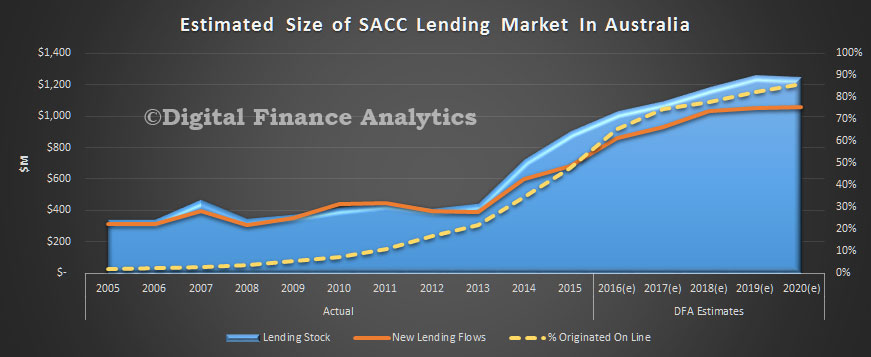

However, the growth in SACC loans appears to be directly linked with the rise on online usage, as more lenders, and borrowers go digital. We think about 70% of new SACC loans were originated via the online channels. We are also expecting the momentum to slow, as market participants tweak their business models and players leave, or enter the market.

However, the growth in SACC loans appears to be directly linked with the rise on online usage, as more lenders, and borrowers go digital. We think about 70% of new SACC loans were originated via the online channels. We are also expecting the momentum to slow, as market participants tweak their business models and players leave, or enter the market.

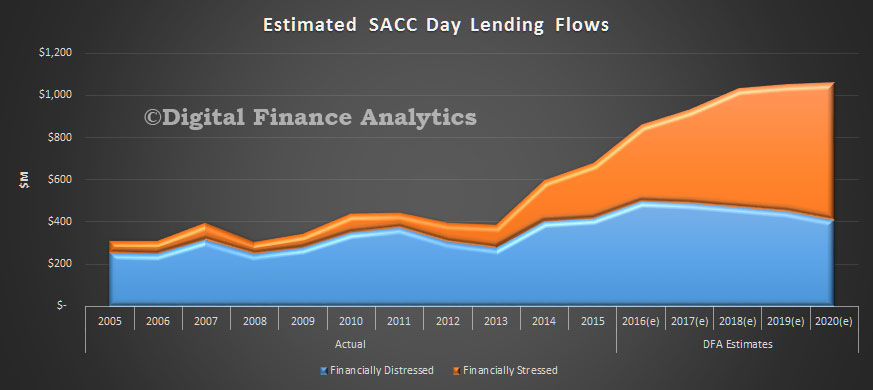

One clue is the mix of households. We identify households who have no choice but to use SACC loans (financially distressed) and those who choose to use these loans for convenience (financially stressed). The mix is changing, with more financially stressed using SACC, whilst distressed households are static, and we think will reduce over time, as lenders change the focus of their business models. In a nutshell, the new focus of the industry is convenient loans to more affluent households, rather than those struggling to make ends meet, and probably on Centrelink payments.

One clue is the mix of households. We identify households who have no choice but to use SACC loans (financially distressed) and those who choose to use these loans for convenience (financially stressed). The mix is changing, with more financially stressed using SACC, whilst distressed households are static, and we think will reduce over time, as lenders change the focus of their business models. In a nutshell, the new focus of the industry is convenient loans to more affluent households, rather than those struggling to make ends meet, and probably on Centrelink payments.

The final clue is that the larger proportion of households with digital capabilities are those stressed, not distressed, so there is strong alignment with online origination. We conclude that it is online which is changing the game. This has profound implications for those seeking to work with households under pressure financially and how digital offerings should be regulated.

The final clue is that the larger proportion of households with digital capabilities are those stressed, not distressed, so there is strong alignment with online origination. We conclude that it is online which is changing the game. This has profound implications for those seeking to work with households under pressure financially and how digital offerings should be regulated.