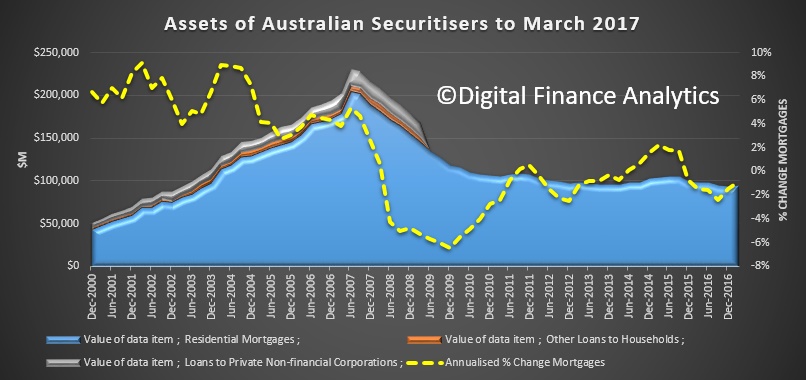

The ABS released their data on Australian securitisers today. At 31 March 2017, total assets of Australian securitisers were $121.6b, up $4.4b (3.8%) on 31 December 2016.

Residential mortgages continue to make up most of the transactions and there was a small overall lift, but in the past year the value of mortgages fell 0.9%. So whilst the securitisation conduits are open, and pricing reasonable (if higher than pre-GFC), overall volumes are still well below their 2007 peaks. This is because other forms of funding are available, including direct investment. Most securitisation instruments are sold to Australian investors.

During the March quarter 2017, the increase in total assets was primarily due to an increase in other loans (up $1.9b, 12.0%), residential mortgage assets (up $1.3b, 1.4%) and cash and deposits (up $1.0b, 27.2%).

At 31 March 2017, total liabilities of Australian securitisers were $121.6b, up $4.4b (3.8%) on 31 December 2016. The increase in total liabilities was due to an increase in long term asset backed securities issued in Australia (up $7.6b, 7.8%). This was partially offset by a decrease in short term asset backed debt securities issued in Australia (down $1.9b, 42.0%) and loans and placements (down $0.6b, 6.4%).

At 31 March 2017, asset backed securities issued in Australia as a proportion of total liabilities increased to 88.6%, up 1.5% on the December quarter 2016 proportion of 87.1%. Asset backed securities issued overseas as a proportion of total liabilities decreased to 3.8%, down 0.3% on the December quarter 2016 proportion of 4.1%.