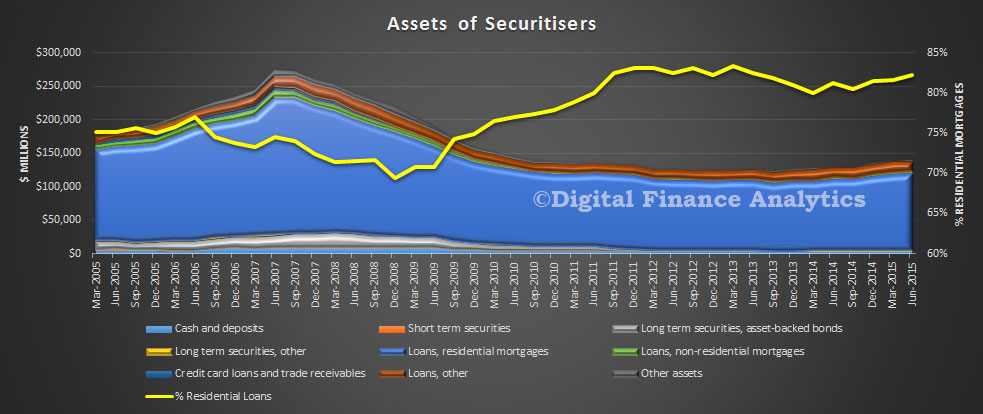

Data from the ABS shows that in the quarter to June 2015, balances with Securitisers grew. At 30 June 2015, total assets of Australian Securitisers were $140.4b, up $0.5b (0.3%) on 31 March 2015. During the June quarter 2015, the rise in total assets was due to an increase in residential mortgage assets (up $1.3b, 1.2%) and cash deposits (up $0.4b, 11.3%). This was partially offset by decreases in other loans (down $1.0b, 5.6%). Residential and non–residential mortgage assets accounted for 83.8% of total assets, were $117.6b at 30 June 2015, an increase of $1.3b (1.1%) during the quarter.

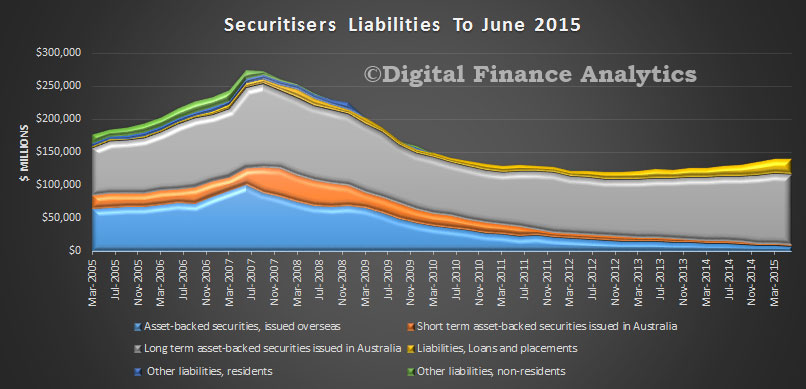

At 30 June 2015, total liabilities of Australian securitisers were $140.4b, up $0.5b (0.3%) on 31 March 2015. The rise in total liabilities was due to the increase in loans and placements (up $2.3b, 11.6%). This was partially offset by a decrease in long term asset backed securities issued in Australia (down $0.9b, 0.9%) and asset backed securities issued overseas (down $0.9b, 9.8%). At 30 June 2015, asset backed securities issued overseas as a proportion of total liabilities decreased to 5.9%, down 0.7% on the March quarter 2015 proportion of 6.6%. Asset backed securities issued in Australia as a proportion of total liabilities decreased to 77.1%, down 1.1% on the March quarter 2015 proportion of 78.2%.

At 30 June 2015, total liabilities of Australian securitisers were $140.4b, up $0.5b (0.3%) on 31 March 2015. The rise in total liabilities was due to the increase in loans and placements (up $2.3b, 11.6%). This was partially offset by a decrease in long term asset backed securities issued in Australia (down $0.9b, 0.9%) and asset backed securities issued overseas (down $0.9b, 9.8%). At 30 June 2015, asset backed securities issued overseas as a proportion of total liabilities decreased to 5.9%, down 0.7% on the March quarter 2015 proportion of 6.6%. Asset backed securities issued in Australia as a proportion of total liabilities decreased to 77.1%, down 1.1% on the March quarter 2015 proportion of 78.2%.

We would expect to see further growth, because non-banks are likely to get more business as the majors dial back their investment lending, and because the securitisation market pricing has normalised from their heights of the GFC. That said, they are of course exposed to the global financial markets and events such as volatility in China are tending to lift rates a little. This may slow growth.

We would expect to see further growth, because non-banks are likely to get more business as the majors dial back their investment lending, and because the securitisation market pricing has normalised from their heights of the GFC. That said, they are of course exposed to the global financial markets and events such as volatility in China are tending to lift rates a little. This may slow growth.