The latest APRA data on ADI Property Exposures to December 2016 tells an interesting story. Essentially, whilst the proportion of higher LVR loans slides, in recent times lenders – especially the big four – appear to be more willing to make interest only loans (on the back of higher volumes of investment loans) alongside out of normal criteria loans. The APRA guidance has not it seems trimmed risk appetite so far.

ADIs residential term loans to households were $1.49 trillion as at 31 December 2016. This is an increase of $110.0 billion (8.0 per cent) on 31 December 2015. There are 5,728,000 housing loans (up 3.6% a year ago). The average balance is $257,300, up 3.5% from a year ago. $101.0 billion of loans were written in the December quarter.

Total Book

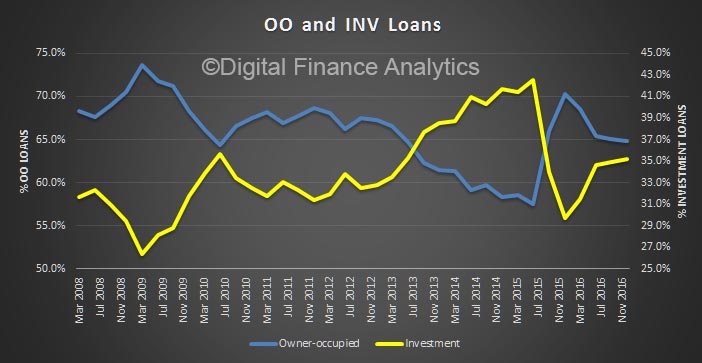

Looking in more detail, first at the aggregate data, we clearly see a rise in the proportion of new investment loans being written to December 2016.

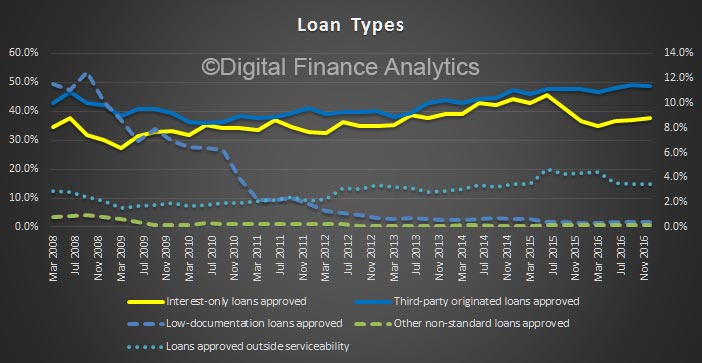

Interest only loans are rising, to 40% and the share via brokers also trended up to 48.8%. We know loans via brokers are higher risk. The proportion of loans approved outside serviceability is also higher.

Interest only loans are rising, to 40% and the share via brokers also trended up to 48.8%. We know loans via brokers are higher risk. The proportion of loans approved outside serviceability is also higher.

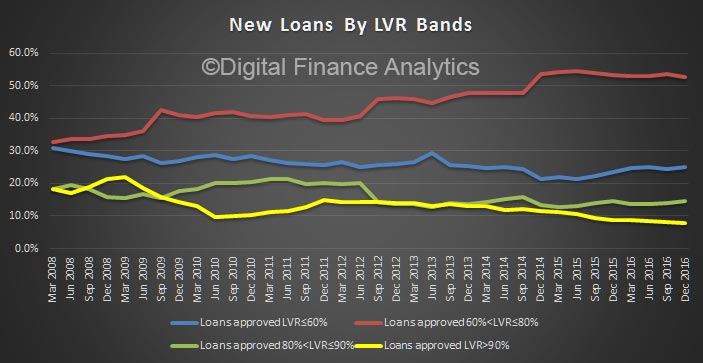

The proportion of higher LVR loans continues to trend down whilst the 60-80% LVR loans are higher, we also see a slight uptick in the 80-90% LVR bands.

The proportion of higher LVR loans continues to trend down whilst the 60-80% LVR loans are higher, we also see a slight uptick in the 80-90% LVR bands.

The Four Majors

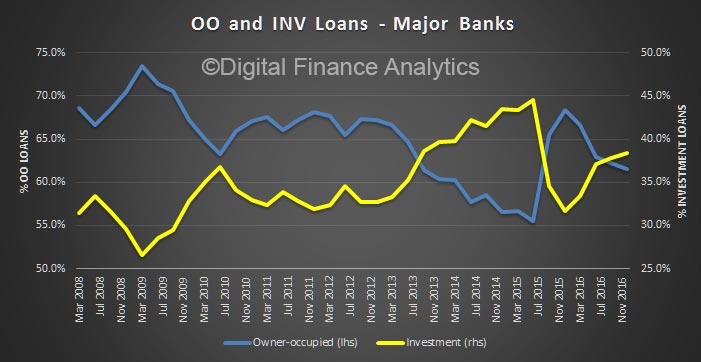

Turning to the aggregate data from the 4 majors, the rise in investment loans is more pronounced, to 38.4%.

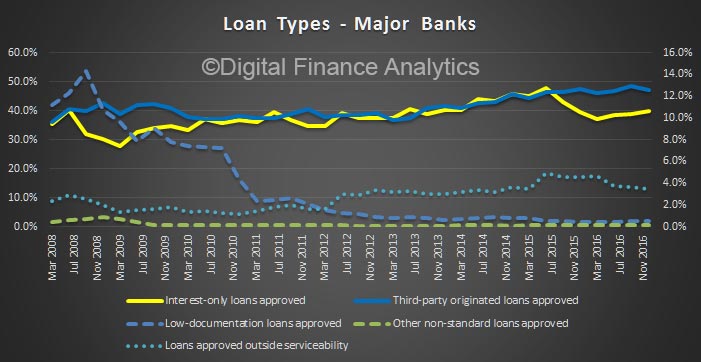

The proportion of interest loan loans has risen, to 40%, from a recent low of 37%. Loans outside serviceability sits at 3.5%.

The proportion of interest loan loans has risen, to 40%, from a recent low of 37%. Loans outside serviceability sits at 3.5%.

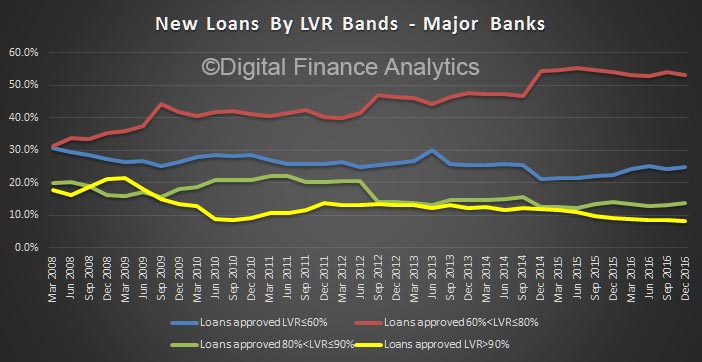

The high LVR loans are lower, more than half of new loans are in the 60-80% LVR band.

The high LVR loans are lower, more than half of new loans are in the 60-80% LVR band.

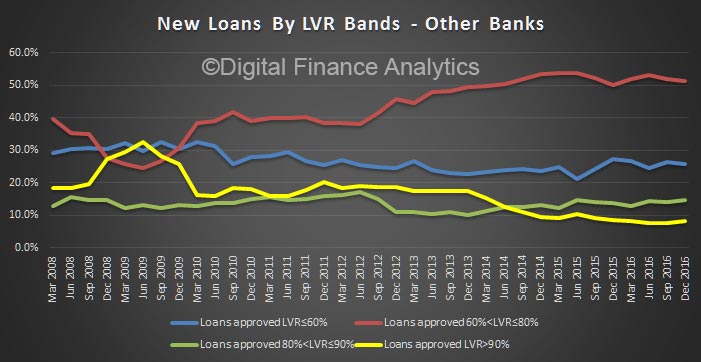

Other Banks (Regionals Etc.)

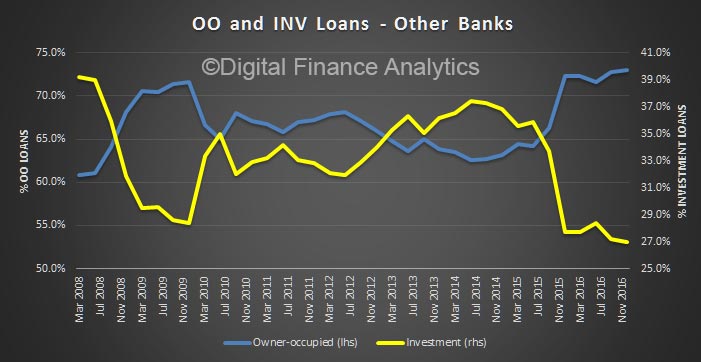

Looking at the other banks (excluding the big 4), the share of investment loans are down to 27%.

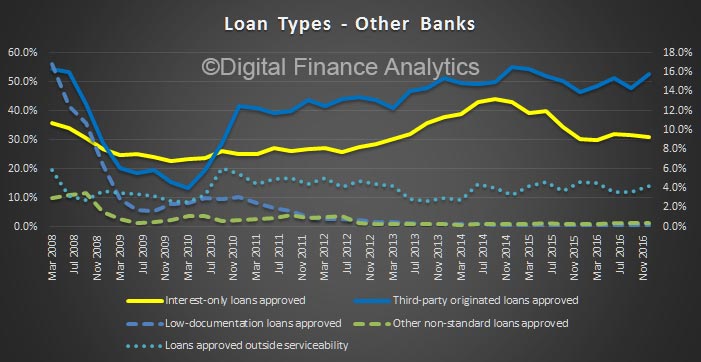

We see a fall in interest only loans, down to 30.7%, whilst the share of broker loans has risen to 52.2%, higher than the majors.

We see a fall in interest only loans, down to 30.7%, whilst the share of broker loans has risen to 52.2%, higher than the majors.

We see a similar trend in a fall in higher LVR loans.

We see a similar trend in a fall in higher LVR loans.

Worth also noting the volumes through credit unions and building societies are no longer being report, thanks to low volumes. So much for the “new force” in banking from the Customer Owned Institutions.

Worth also noting the volumes through credit unions and building societies are no longer being report, thanks to low volumes. So much for the “new force” in banking from the Customer Owned Institutions.