The results of the 2016 UK Bank stress testing has been released by the Prudential Regulation Authority (PRA). The test did not reveal capital inadequacies for four out of the seven participating banks but the Royal Bank of Scotland Group (RBS), Barclays and Standard Chartered revealed some capital inadequacies and remedial work is required.

However, the PRA concluded that given the results, no system-wide macroprudential actions on bank capital were required in response to the 2016 stress test. Despite a more severe scenario, the aggregate low points for CET1 capital and Tier 1 leverage ratios were higher than in the 2014 and 2015 tests.

Background

In March 2016, the Bank of England launched its third concurrent stress test of the UK banking system. The 2016 stress test covered seven major UK banks and building societies (hereafter referred to as ‘banks’), accounting for around 80% of PRA-regulated banks’ lending to the UK real economy.

The 2016 stress-test scenario was designed under the Bank’s new approach to stress testing. Under this framework, the stress being tested against will generally be severe and broad, in order to assess the resilience of major UK banks to ‘tail risk’ events. Its precise severity will reflect the risk assessment of the FPC and PRA Board.

As such, the 2016 test was more severe than earlier tests. The severity of the stress in the 2016 scenario is based on the risk assessment the FPC and PRA Board made in March 2016 — that overall risks to global activity associated with credit, financial and other asset markets were elevated, and that risks associated with domestic credit were no longer subdued but

As such, the 2016 test was more severe than earlier tests. The severity of the stress in the 2016 scenario is based on the risk assessment the FPC and PRA Board made in March 2016 — that overall risks to global activity associated with credit, financial and other asset markets were elevated, and that risks associated with domestic credit were no longer subdued but

were not yet elevated.

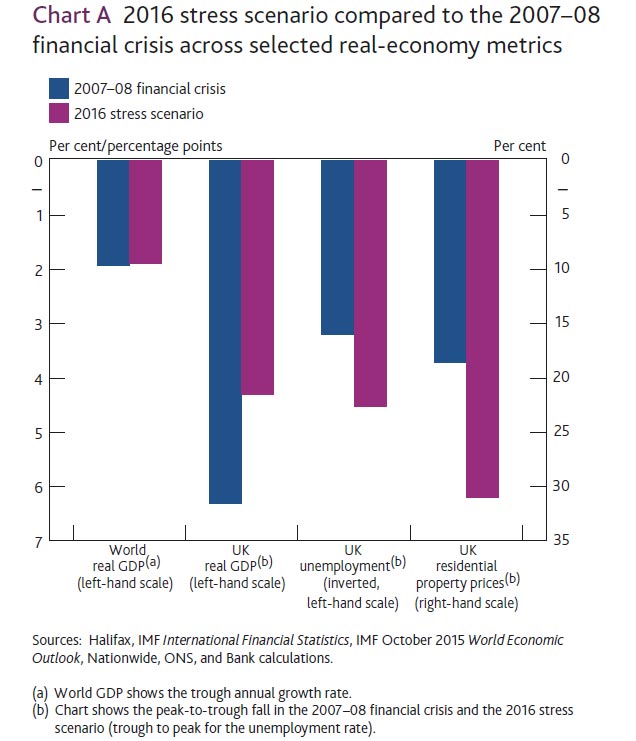

The 2016 annual cyclical scenario incorporates a very severe, synchronised UK and global economic recession, a congruent financial market shock and a separate misconduct cost stress. Annual global GDP growth troughs at -1.9%, as it did during the 2008 global financial crisis. Annual growth in Chinese real GDP is materially weaker than in the financial crisis and troughs at -0.5%. The level of UK GDP falls by 4.3%, accompanied by a 4.5 percentage point rise in the unemployment rate. Overall, the UK stress is roughly equivalent to that experienced during the financial crisis, albeit with a shallower fall in domestic output, and a more severe rise in unemployment and fall in residential property prices.

The stress test also includes a traded risk scenario that is constructed to be congruent with this macroeconomic stress. Having fallen significantly during 2015, the price of oil reaches a low of US$20 per barrel, reflecting the slowdown in world demand. Investors’ risk appetite diminishes more generally and financial market participants attempt to de-risk their portfolios, generating volatility. The VIX index averages 37 during the first year of the stress, which compares to a quarterly average of around 40 between 2008 H2 and 2009 H1.

Interest rates facing some households and businesses increase in the early part of the stress, partly reflecting a rise in term premia on long-term government debt. Credit spreads on corporate bonds rise sharply, with spreads on US investment-grade corporate bonds, for example, rising from around 170 basis points to 500 basis points at the peak of the stress. Meanwhile, policymakers pursue additional monetary stimulus, which starts to reduce long-term interest rates.

Residential property and commercial real estate (CRE) prices also fall. Following rapid recent growth, these falls are particularly pronounced for property markets in China and Hong Kong, with residential property prices falling by around 35% and 50%, respectively. In the United Kingdom, house prices fall by 31% and average CRE prices fall by 42%. These falls are even greater for prime CRE, reflecting the fact that prices of these properties have risen more robustly since the financial crisis.

The 2016 stress test also incorporates stressed projections, generated by Bank staff, for potential misconduct costs, beyond those paid or provided for by the end of 2015. These stressed misconduct cost projections are not a central forecast of such costs. They are a simultaneous, but unrelated, stress alongside the macroeconomic stress and traded risk scenario incorporated in the 2016 test.

Impact of the stress scenario on the banking system

The stress scenario is estimated to lead to system-wide losses of £44 billion over the first two years of the stress, around five times the net losses incurred by the same banks as a group over 2008–09. Based on the Bank’s projections, the 2016 stress scenario would reduce the aggregate CET1 capital ratio across the seven participating banks from 12.6% at the end of 2015 to a low point of 8.8% in 2017, after factoring in the impact of management actions and the conversion of AT1 instruments into CET1 capital (Table 1).(1) The aggregate Tier 1 leverage ratio falls from 4.9% at the end of 2015 to a low point of 3.9% in 2017.

Compared to previous tests, the fall in the aggregate CET1 capital ratio from start to stressed low point was larger in the 2016 stress test, reflecting the greater severity of the stress scenario. Nevertheless, at 8.8% that low point was well above the 7.6% low point reached in 2014 and 2015.

Lloyds Banking Group and Santander UK cut their ordinary dividends to zero by the low point of the stress, in line with their published payout policies.(1) In reaction to losses made during both the first and second years of the stress, HSBC makes a substantial discretionary cut in ordinary dividend payments in 2016 and then pays no ordinary dividend in 2017,

as it makes a loss and becomes subject to CRD IV distribution restrictions. Meanwhile, Barclays and Standard Chartered are loss-making during the first two years of the stress and cut their ordinary dividend payments to zero as they become subject to CRD IV distribution restrictions. The Royal Bank of Scotland Group does not pay an ordinary dividend in any year

of the stress scenario. Nationwide continues to make distributions on its Core Capital Deferred Shares (CCDS).

In general, the stress has the greatest impact on those banks with significant international and corporate exposures. The three banks operating principally in domestic markets — Lloyds Banking Group, Nationwide and Santander UK — remain well above their hurdle rates throughout the stress. This reflects, in part, improvements in the asset quality of banks’ core UK mortgage businesses, through a combination of rising property prices, which have bolstered the value of collateral backing loans, as well as banks adopting more prudent new lending standards.

The PRA Board judged that:

- The test did not reveal capital inadequacies for four out of the seven participating banks, based on their balance sheets at end-2015 (HSBC, Lloyds Banking Group, Nationwide Building Society and Santander UK).

- The Royal Bank of Scotland Group (RBS) did not meet its common equity Tier 1 (CET1) capital or Tier 1 leverage hurdle rates before additional Tier 1 (AT1) conversion in this scenario. After AT1 conversion, it did not meet its CET1 systemic reference point or Tier 1 leverage ratio hurdle rate. Based on RBS’s own assessment of its resilience identified during the stress-testing process, RBS has already updated its capital plan to incorporate further capital strengthening actions and this revised plan has been accepted by the PRA Board. The PRA will continue to monitor RBS’s progress against its revised capital plan.

- Barclays did not meet its CET1 systemic reference point before AT1 conversion in this scenario. In light of the steps that Barclays had

already announced to strengthen its capital position, the PRA Board did not require Barclays to submit a revised capital plan. While these steps are being executed, its AT1 capital provides some additional resilience to very severe shocks. - Standard Chartered met all of its hurdle rates and systemic reference points in this scenario. However, it did not meet its Tier 1 minimum capital requirement (including Pillar 2A). In light of the steps that Standard Chartered is already taking to strengthen its capital position, including the AT1 it has issued during 2016, the PRA Board did not require Standard Chartered to submit a revised capital plan.

- The FPC judged that the system should be capitalised to withstand a test of this severity, given the risks it faced. It therefore welcomed the actions by some banks to improve their capital positions. Despite a more severe scenario, the aggregate low points for CET1 capital and Tier 1 leverage ratios were higher than in the 2014 and 2015 tests. The FPC noted the increased resilience to stress provided by banks’ AT1 capital positions and banks’ stated intention to reduce dividends in stress. It also noted the strong performance of the most domestically focused banks. Given the results, no system-wide macroprudential actions on bank capital were required in response to the 2016 stress test.

- The FPC is maintaining the UK countercyclical capital buffer rate at 0% and reaffirms that it expects, absent any material change in the outlook, to maintain this rate until at least June 2017. This reflects developments since the stress test was launched in March, which suggest greater uncertainty around the UK economic outlook and an increased possibility that material domestic risks could crystallise in the near term. The FPC was concerned that banks could respond to these developments by hoarding capital and restricting lending. That position has not changed.

One thought on “Some UK Banks Fail Latest Stress Tests”