Sydney house prices have another year or so of rises before the bubble shrinks.

Median housing prices in Sydney are overvalued by 14% and in Melbourne by 8%, but will decline gradually rather than sharply over the next few years, according to analysis by KPMG Economics predicts.

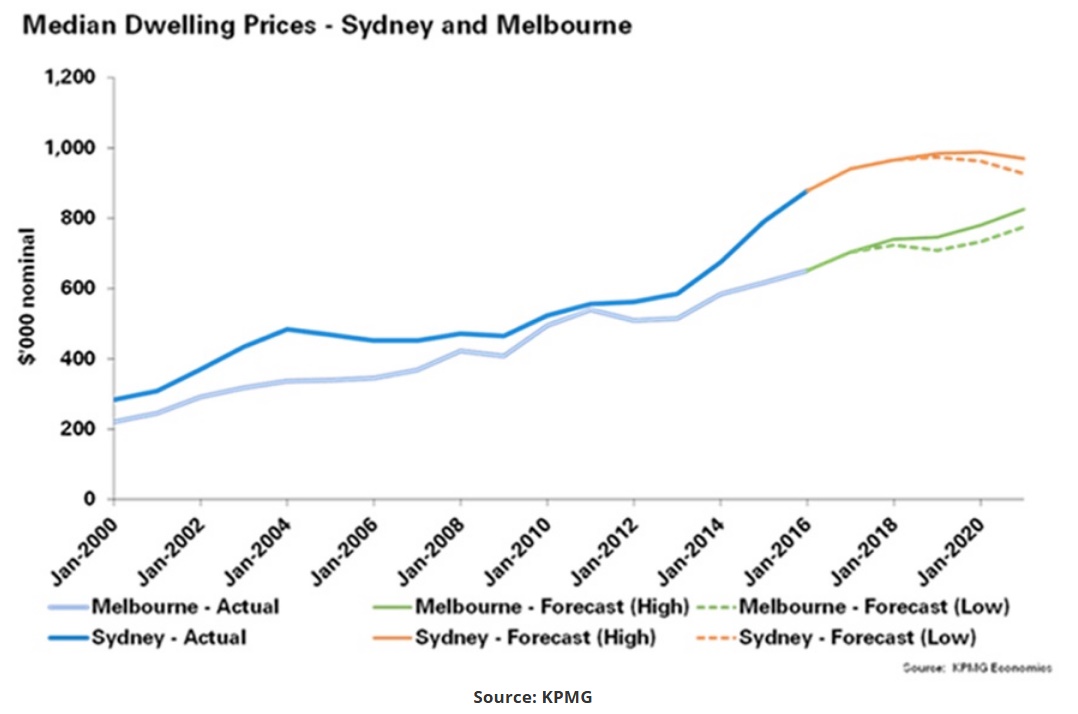

Sydney median prices are forecast to peak at $980,000 in 2019, up from $880,000 from June 2016, and then gradually roll back to between $930,000 and $950,000 by the end of the 2021 financial year.

However, Melbourne prices are expected to peak next year, pause for year or two, and then start to grow again.

The median prices in Melbourne are expected to rise to between $720,000 to $740,000, from about $650,000 in 2016, by the end of 2019. After plateauing, they will then regain momentum to be between $775,000 and $825,000 by the end of 2021.

“Our forecasts show Sydney will experience a greater adjustment than Melbourne in the next few years, but this is likely to be gradual rather than a collapse in the median dwelling price,” says Brendan Rynne, KPMG chief economist.

“Whether or not the current Sydney and Melbourne housing prices constitute a ‘bubble’ is a matter for debate, but we estimate that short-term factors have pushed median dwelling prices above their long-term ‘equilibrium’ prices by about 14% and 8% respectively.

“But it should be remembered that this has happened before in Australia and prices have returned to equilibrium without the sort of crash we have returned to equilibrium without the sort of crash we have seen in other countries after the GFC.

“We expect the same again to happen here now. We anticipate a cooling in price growth, and from next year prices will start to gradually come down. While prices are high now, they are still within known boundaries by historic standards.”

Here’s how KPMG sees Sydney and Melbourne house prices moving:

Source: KPMG

Source: KPMG

KPMG’s report, Housing affordability: What is driving house prices in Sydney and Melbourne?, argues that Sydney house prices have become more volatile since the GFC even though there has not been the same volatility in supply, demand and costs.

It also finds there is a long-term relationship between house prices and variables including working population levels, stock of dwellings, rate of borrowing by property investors, and the adoption of stronger prudential controls by the regulator APRA.

The banks have been winding back their interest only offerings favoured by property investors, increasing rates, while offering better deals on principal and interest mortgages.

Anecdotal evidence suggests demand by Chinese investors for Australian residential property may have softened in recent months due a combination of factors, including the adoption of differential stamp duty in some states, and vacant property taxes for foreign buyers.

“Investors both here and overseas have been the key driver behind the housing price boom and policymakers are now addressing this,” says Rynne.