The ABS released their Housing Finance data to May 2017 today. Overall, trend housing finance owner occupied housing commitments rose 0.4%, while investment housing commitments fell 1.5%. The trend estimate for the total value of dwelling finance commitments excluding alterations and additions fell 0.3%.

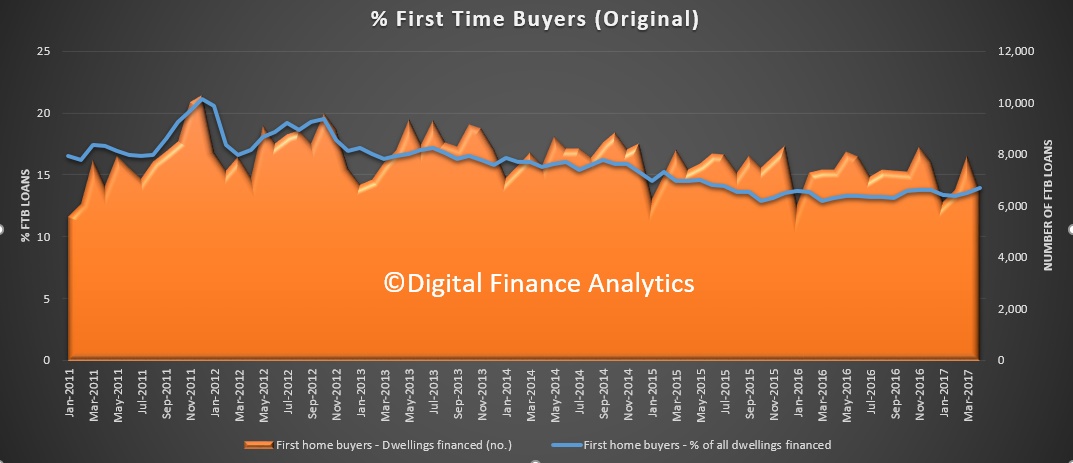

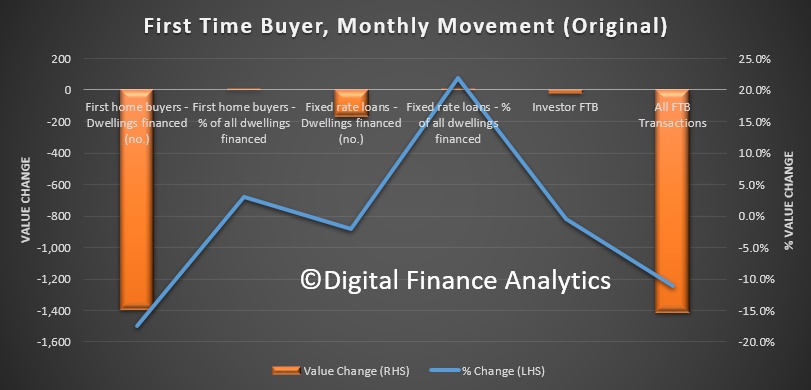

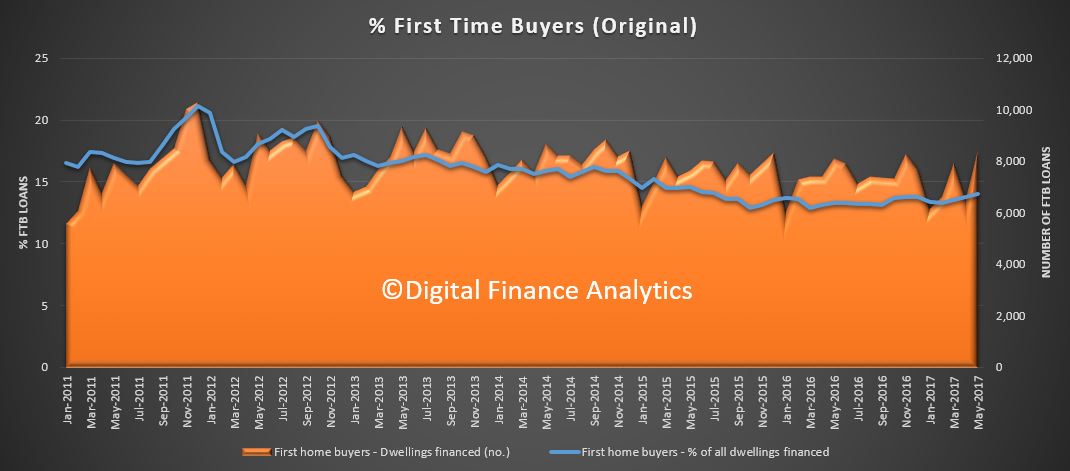

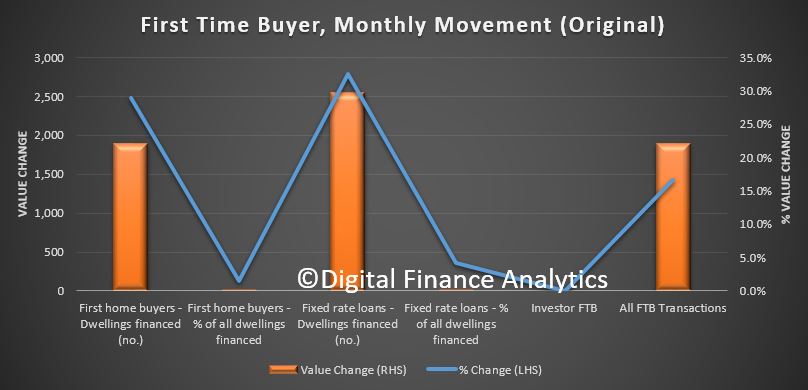

First, there was a rise in the number of first time buyers in May. The original data (no seasonal adjustments) is always volatile but the percentage rose a little to 14.0% from 13.8% in April 2017.

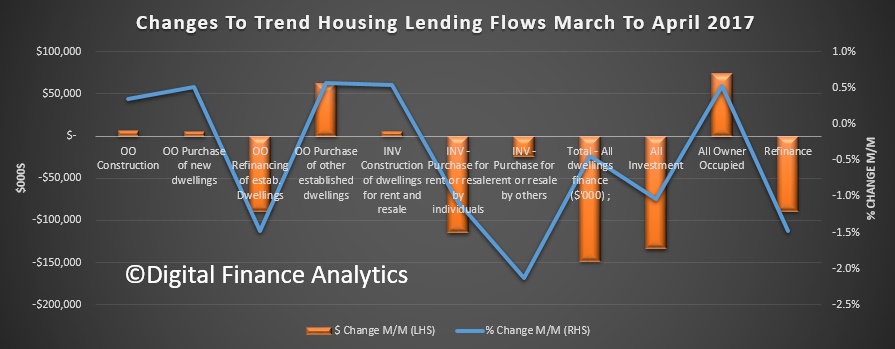

The month on month movements show a rise in the number of loans, up nearly 2,000 and also a rise in the number of refinanced loans.

The month on month movements show a rise in the number of loans, up nearly 2,000 and also a rise in the number of refinanced loans.

Overlaying data from our surveys to capture investor first time buyers, we see the combined trend is rising. We expect a further kick in July when the new FTB incentives kick in.

Overlaying data from our surveys to capture investor first time buyers, we see the combined trend is rising. We expect a further kick in July when the new FTB incentives kick in.

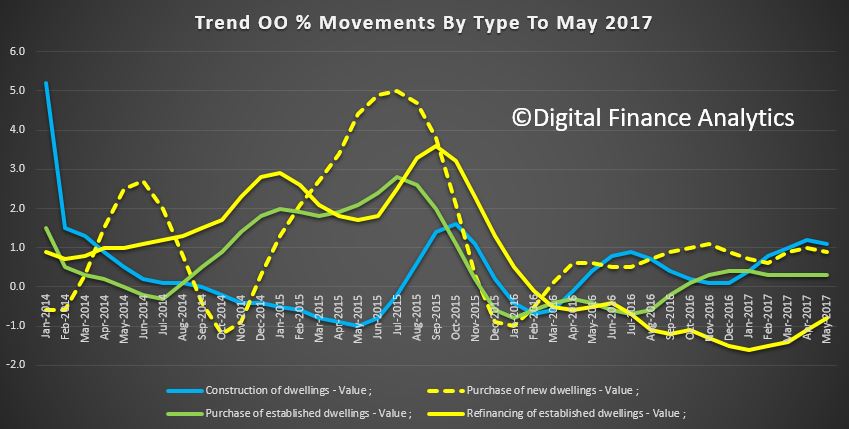

![]() Next we look at the owner occupied changes across the months. We see an inflection in refinanced loans, but still falling, whilst other categories of loans are relatively stable or falling slightly.

Next we look at the owner occupied changes across the months. We see an inflection in refinanced loans, but still falling, whilst other categories of loans are relatively stable or falling slightly.

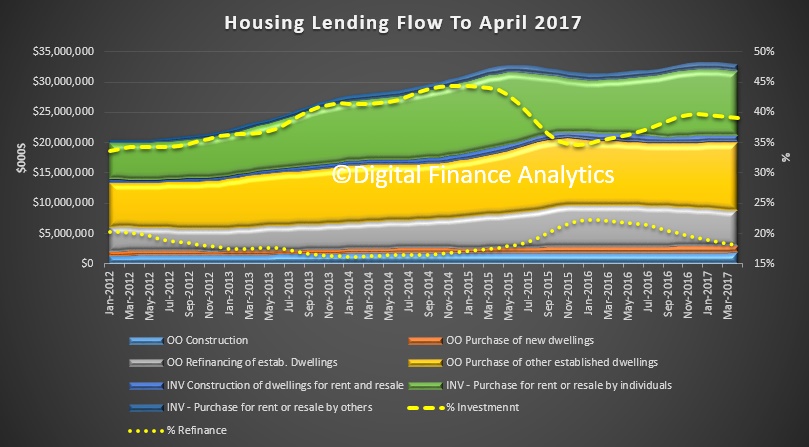

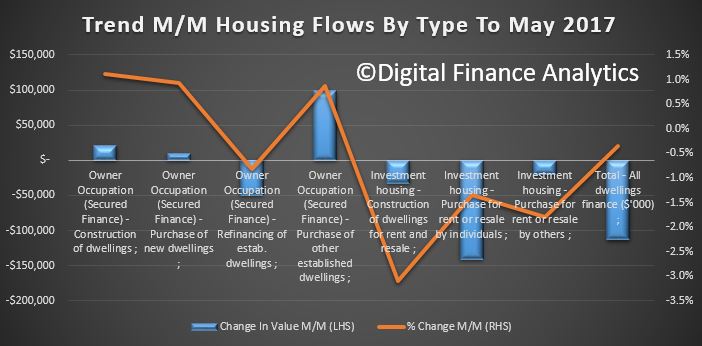

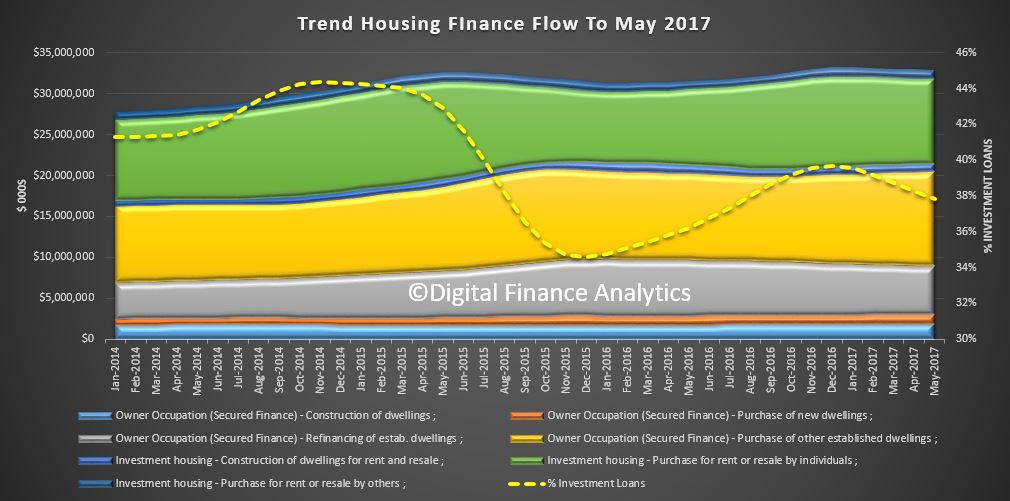

Next we look at flow by category. Owner occupied purchase of established dwellings rose the strongest, with the owner occupied construction and new purchases also up. The value of refinancing fell as did all categories of investor loans. We can conclude the regulatory tightening and lower expectations of investors are having a cooling impact on the market. Hence all the repricing across the market we have seen in recent weeks.

Next we look at flow by category. Owner occupied purchase of established dwellings rose the strongest, with the owner occupied construction and new purchases also up. The value of refinancing fell as did all categories of investor loans. We can conclude the regulatory tightening and lower expectations of investors are having a cooling impact on the market. Hence all the repricing across the market we have seen in recent weeks.

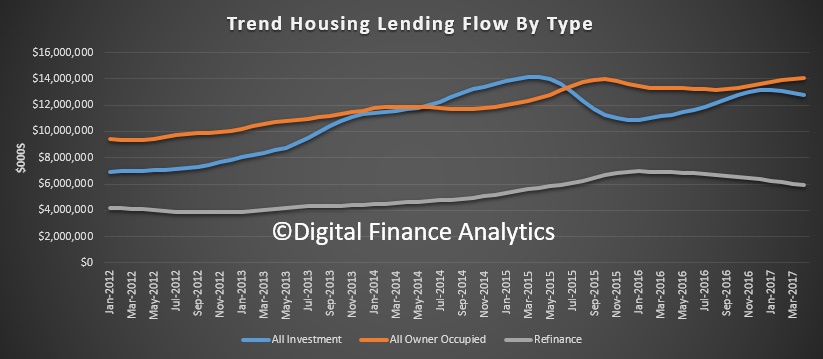

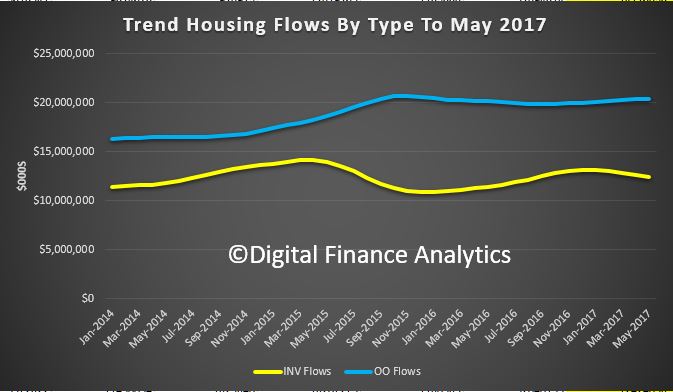

Comparing the flows across new owner occupied and investment loans we see the value of the latter falling, whilst the former is up just a little.

Analysis of the more detailed splits shows the proportion of investor loans fell to below 38% and this falling trend is set to continue. Owner occupied purchase of established dwellings rose. In trend terms, while the number of commitments for the construction of dwellings rose 1.0% and the number of commitments for the purchase of new dwellings rose 0.4%, the number of commitments for the purchase of established dwellings fell 0.6%.

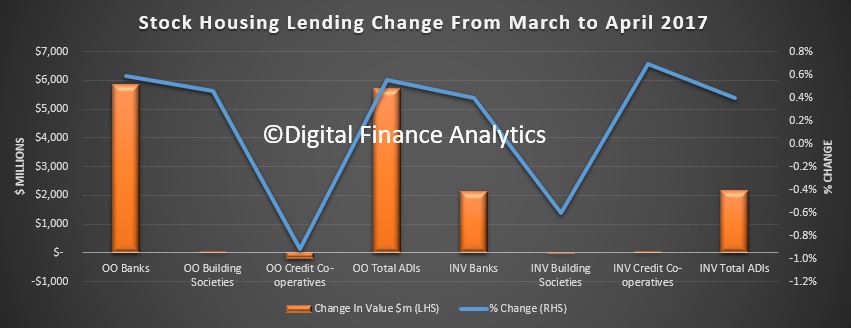

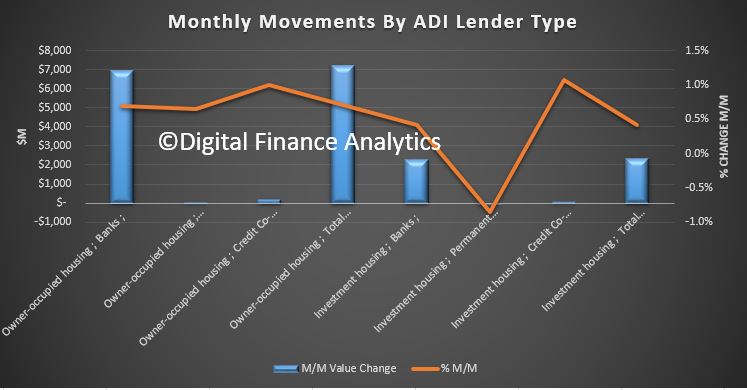

Movements by lender type shows the bulk of lending is being done by the banks, although the mutuals showed a small rise.

Movements by lender type shows the bulk of lending is being done by the banks, although the mutuals showed a small rise.

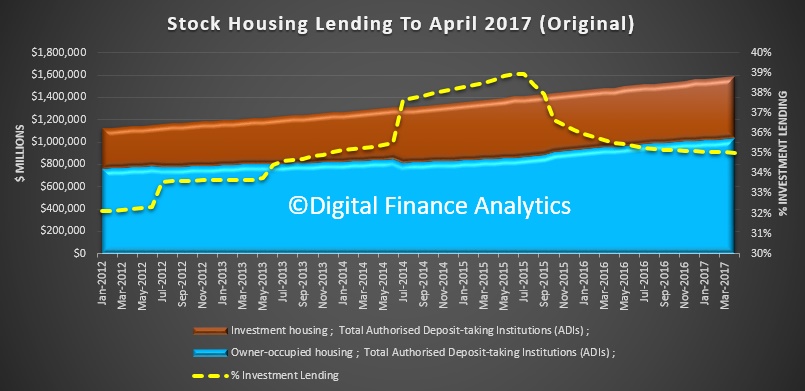

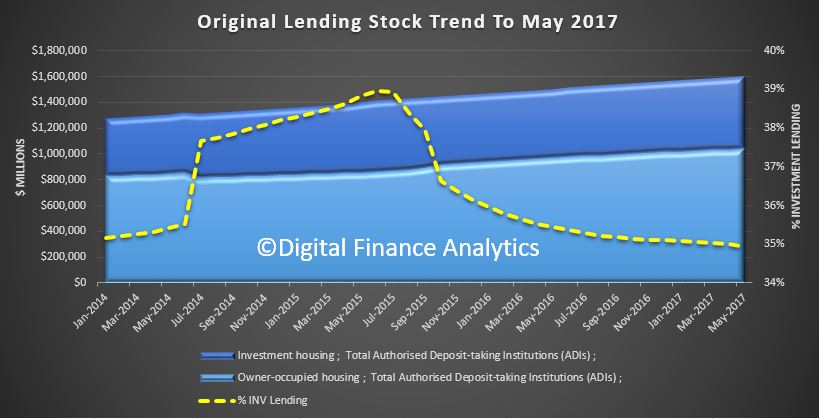

Finally, the trend lending stock to May showed another rise, with the proportion of investor loans slipping to below 35%, the lowest since 2014.

Finally, the trend lending stock to May showed another rise, with the proportion of investor loans slipping to below 35%, the lowest since 2014.

So we can conclude that lending momentum is changing, there is clearly a focus on owner occupied refinance and first time buyers. But given the still firm auction clearance rates reported through June and July, it will be interesting to see just how weak the investment sector goes.

So we can conclude that lending momentum is changing, there is clearly a focus on owner occupied refinance and first time buyers. But given the still firm auction clearance rates reported through June and July, it will be interesting to see just how weak the investment sector goes.