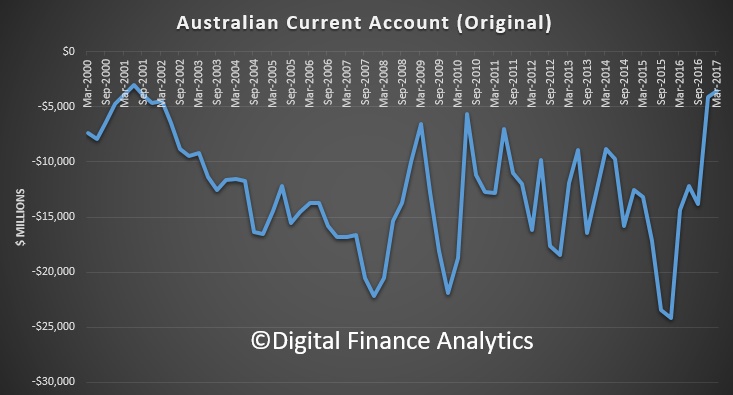

For the third quarter in succession, higher export commodity prices contributed to a narrowing of the current account deficit in the March quarter 2017, according to latest figures from the Australian Bureau of Statistics (ABS).

The seasonally adjusted current account deficit fell $403 million (11 per cent) to $3,108 million in the March quarter 2017. In seasonally adjusted terms, the balance on goods and services surplus in the March quarter 2017 is the highest on record at $9,242 million. Exports of goods and services rose $4,852 million (5 per cent) and imports of goods and services rose $1,723 million (2 per cent). The primary income deficit widened $2,712 million (29 per cent).

The seasonally adjusted current account deficit fell $403 million (11 per cent) to $3,108 million in the March quarter 2017. In seasonally adjusted terms, the balance on goods and services surplus in the March quarter 2017 is the highest on record at $9,242 million. Exports of goods and services rose $4,852 million (5 per cent) and imports of goods and services rose $1,723 million (2 per cent). The primary income deficit widened $2,712 million (29 per cent).

In volume terms, imports grew this quarter while exports went down, and as a result international trade is expected to detract 0.7 percentage points from growth in the March quarter 2017 Gross Domestic Product. In seasonally adjusted chain volume terms, the balance on goods and services surplus decreased $2,966 million (85 per cent) to $543 million.

Australia’s net international investment position was a liability of $1,025.5 billion at 31 March 2017, a decrease of $2.7 billion on the revised 31 December 2016 position of $1,028.2 billion.

Australia’s net foreign debt liability decreased $13.6 billion (1 per cent) to a net liability position of $1,015.0 billion. Australia’s net foreign equity had a turnaround of $10.9 billion from a net asset position of $0.3 billion at 31 December 2016 to a net liability position of $10.6 billion at 31 March 2017.