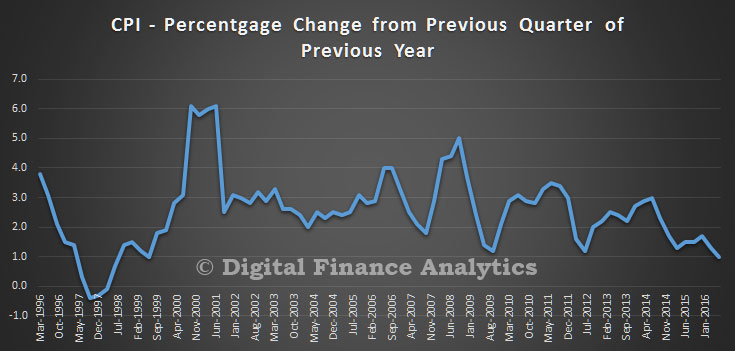

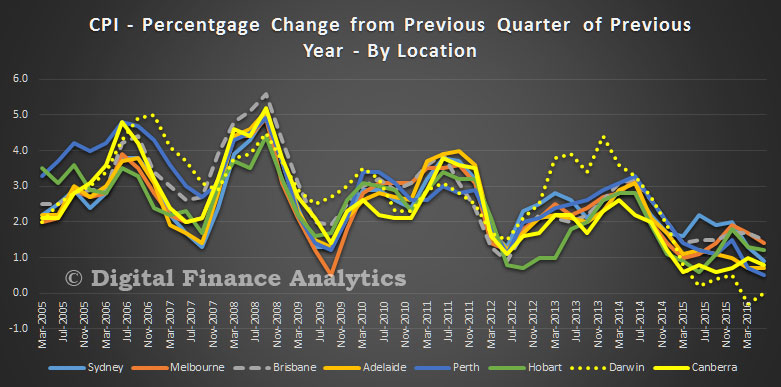

Monthly trend employment in Australia increased in July 2016, according to figures released by the Australian Bureau of Statistics (ABS) today. However, there are significant state variations as well as movements between full-time and part-time work. Younger Australians and females are more likely to be unemployed. Beware the national averages!

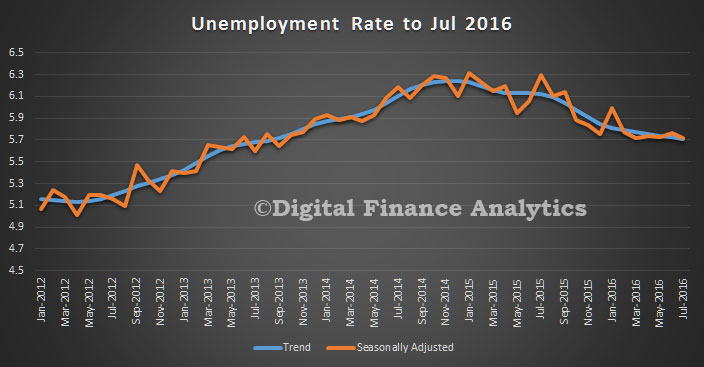

The trend unemployment rate remained steady at 5.7 per cent. The participation rate also remained steady at 64.8 per cent. These figures have been constant since May 2016.

In July 2016, trend employment increased by 11,800 persons to 11,955,100 persons – a monthly growth rate of 0.1 per cent. Trend part-time employment growth continued, with an increase of 10,600 persons, while full-time employment increased by 1,200 persons.

In July 2016, trend employment increased by 11,800 persons to 11,955,100 persons – a monthly growth rate of 0.1 per cent. Trend part-time employment growth continued, with an increase of 10,600 persons, while full-time employment increased by 1,200 persons.

“The latest Labour Force release shows continued strength in part-time employment growth. Over the past six months there has been an increase of 82,600 people working part-time, compared with a 21,600 decrease in those working full-time,” said the Program Manager of ABS’ Labour and Income Branch, Jacqui Jones.

The trend monthly hours worked in all jobs increased by 0.9 million hours (0.06 per cent), although it remained slightly below the high in December 2015.

Trend series smooth the more volatile seasonally adjusted estimates and provide the best measure of the underlying behaviour of the labour market.

The seasonally adjusted number of persons employed increased by 26,200 in July 2016. The seasonally adjusted unemployment rate for July 2016 decreased by 0.1 percentage points to 5.7 per cent and the seasonally adjusted labour force participation rate remained unchanged at 64.9 per cent.

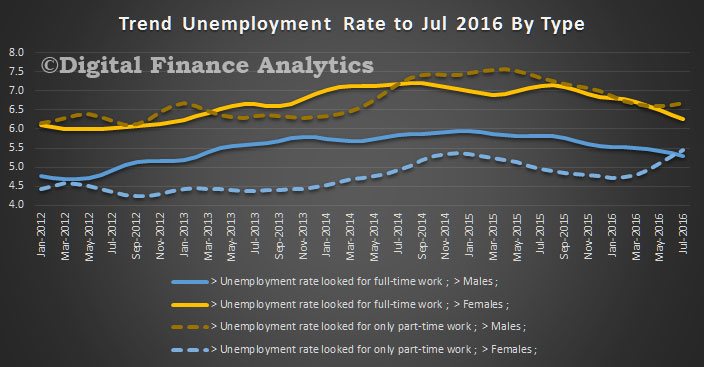

It appears that full-time and part-time unemployment are moving differently, with a rise in both male and female part-time rates.

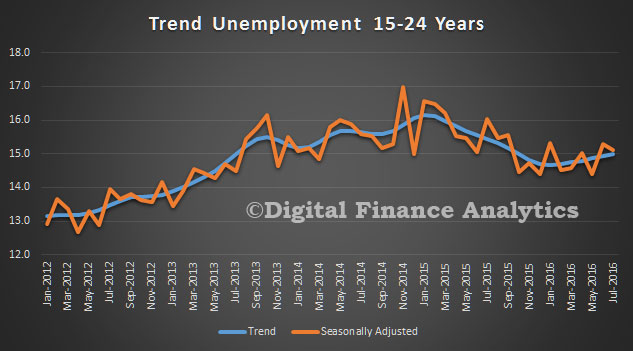

Younger Australians have much higher, and rising unemployment.

Younger Australians have much higher, and rising unemployment.

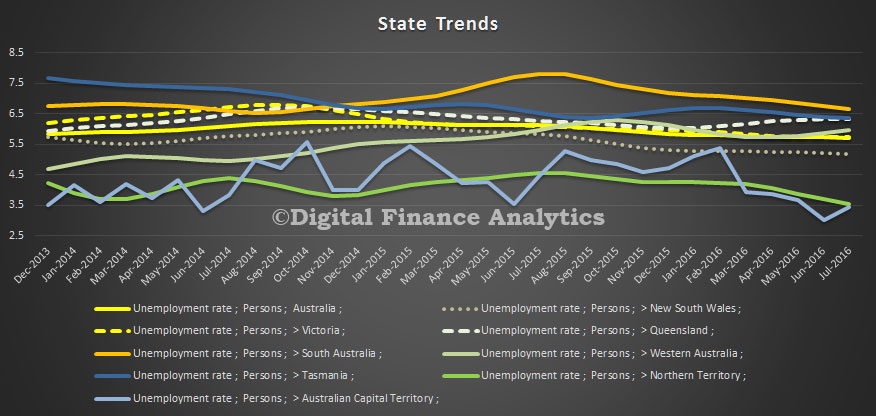

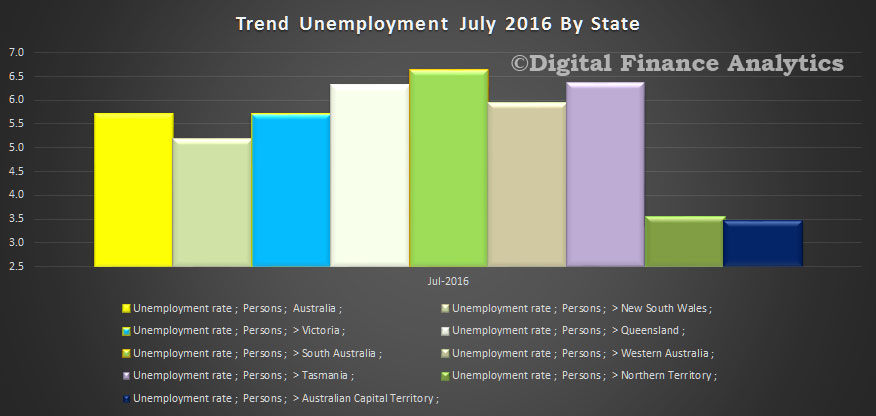

There are significant variations across states, with several, including WA, QLD, TAS and SA above 6%, whilst ACT and NT have much lower rates.

There are significant variations across states, with several, including WA, QLD, TAS and SA above 6%, whilst ACT and NT have much lower rates.

The trends tell the story, with rates falling in NSW and VIC, whilst rising in QLD and WA.

The trends tell the story, with rates falling in NSW and VIC, whilst rising in QLD and WA.