The ACCC has established a Financial Services Competition Branch, which it says will provide support for the Commonwealth Director of Public Prosecutions’ prosecution of ANZ, Citigroup, Deutsche Bank and six senior officers, via InvestorDaily.

The unit, enabled by an allocation from the government’s mid-year

budget, falls under the ACCC’s new Compliance and Enforcement Policy and

includes a permanent competition investigation team.

The competition regulator expects its team to complete a number of investigations that could result in court proceedings.

The announcement made by ACCC chair Rod Sims during his address to

the Committee for Economic Development Australia comes on the back of

AMP executives facing potential criminal charges, in a case against ASIC

over charging fees for no service.

“In commenting on regulators, the final report of the financial

services royal commission focused on issues that were of primary concern

to ASIC and APRA,” Mr Sims said.

“However, an underlying theme of the royal commission final report

was that competition is not vigorous among the major banks or in some

parts of the financial sector.”

The watchdog is also writing rules for the Consumer Data Right

system, known as ‘open banking’, which will determine how banks must

operate under the scheme.

The ACCC’s work will also focus on foreign exchange fees remaining high, Mr Sims added.

The ACCC said the finance competition investigation team will

complement a market studies unit that focuses on the financial sector,

which has been in place for a year.

The opaque, discretionary pricing of residential mortgages by banks makes it difficult and time consuming for borrowers to shop around and stifles price competition, a report by the ACCC has found.

The ACCC’s Residential Mortgage Price Inquiry monitored the prices

charged by the five banks affected by the government’s Major Bank Levy

between 9 May 2017 and 30 June 2018.

The ACCC’s final report

found the unnecessarily high search costs or effort required by

borrowers to find better prices reduces their willingness to shop

around, but that many borrowers who negotiate with their bank can get a

much better price.

“Pricing for mortgages is opaque and the big four banks have a lot of

discretion. The banks profit from this and it is against their

interests to make pricing transparent,” ACCC Chair Rod Sims said.

“Borrowers may not be aware they can negotiate with their lender on

price, both before and, particularly, after they have established their

mortgage.”

As at 30 June 2018, an existing borrower with an average-sized

mortgage could initially save up to $850 a year in interest if they

negotiated to pay the same interest rate as the average new borrower at

the five banks under review. For many borrowers the gain will be much

larger.

It appears that media attention on banks from the Banking Royal

Commission, the Productivity Commission’s Inquiry into competition in

the Australian financial system and the ACCC’s inquiry prompted some

borrowers to approach their lender for a better rate.

The ACCC reports that about 11 per cent of borrowers with variable

rate mortgages had the price of their current residential mortgage

reduced by one of the five banks under review in the year to 30 June

2018.

“I encourage more people to ask their lender whether they are getting

the lowest possible interest rates for their residential mortgage and,

as they do so, be ready to threaten to switch to another lender,” Mr

Sims said.

“I am afraid that the threat of switching banks will often be necessary to achieve a competitive mortgage rate.”

When directing the ACCC to conduct this inquiry, the Treasurer

requested the ACCC to report whether it found any evidence of the five

banks passing on the costs associated with the Major Bank Levy to

residential mortgage borrowers.

“The ACCC found no evidence that the five banks changed prices

specifically to recover the cost of the Major Bank Levy, whether in part

or in full, during the price monitoring period,” Mr Sims said.

The ACCC did find that measures announced by APRA in March 2017 to

limit new interest-only residential mortgage lending created an

opportunity for banks to synchronise increases to headline variable

interest rates for interest-only mortgages.

“We were not surprised banks seized the opportunity to increase

prices for interest-only loans. These price rises were enabled by the

oligopoly market structure in which the big four banks collectively have

a market share of about 80 per cent,” Mr Sims said.

ANZ was the first bank to announce increases to these interest-only

rates in June 2017. It did so safe in the knowledge that its move would

put the other banks at risk of breaching the APRA limits.

The other four banks, therefore, announced similar changes in the

same month. Together, the big four banks estimated revenue gains of over

$1.1 billion for their 2018 financial year, primarily as a result of

these rate increases.

“We consider that ANZ increased its rates, clear in its belief that,

given the APRA limits, the other big four banks would follow its lead,

and this expectation proved correct,” Mr Sims said.

The ACCC calculated that the rate increases by the five banks would

have added, in the first year, about $1300 in interest charged to the

average-sized owner-occupier interest-only standard variable mortgage.

“Such is the oligopolistic nature of banking that the banks all took

the opportunity to increase rates on both new and existing interest-only

mortgages, despite APRA’s measures only applying to new lending,” Mr

Sims said.

The ACCC also compared the approach to pricing of a sample of seven

banks that were not subject to the Inquiry. Three of these banks were

particularly focussed on competing on price, and therefore have lower

rates. Some of the banks in our sample rely heavily on brokers and

aggregators to gain market share. The ACCC notes that these banks, and

other lenders in a similar position, are likely to be more vulnerable to

future regulatory changes that affect the use of brokers as a

distribution channel.

In this report the ACCC notes that the new Consumer Data Right will,

among other things make it much easier for consumers to compare

available interest rates.

“The ACCC looks, in particular, to the Consumer Data Right to empower consumers in their dealings with banks,” Mr Sims said.

On 9 May 2017 the Treasurer, the Hon. Scott Morrison MP, issued a

direction to the ACCC to inquire into prices charged or proposed to be

charged by Authorised Deposit-taking Institutions affected by the Major

Bank Levy in relation to the provision of residential mortgage products

in the banking industry in Australia. The Major Bank Levy came into

effect from 1 July 2017.

The five banks affected by the levy are Australia and New Zealand

Banking Group Limited (ANZ), Commonwealth Bank of Australia, Macquarie

Bank Limited, National Australia Bank Limited, and Westpac Banking

Corporation.

The ACCC used its compulsory information gathering powers to obtain

documents and data from the five banks on their pricing of residential

mortgage products. The ACCC supplemented its analysis of the documents

and data supplied by the five banks with data from the Reserve Bank of

Australia (RBA), Australian Prudential Regulation Authority (APRA) and

the Australian Bureau of Statistics (ABS).

This Inquiry was the first task of the ACCC’s Financial Services Unit

(FSU), which was formed as a permanent unit during 2017 following a

commitment of continuing funding by the Australian Government in the

2017-18 Budget. Alongside the ACCC’s role in promoting competition in

financial services through its enforcement, infrastructure regulation,

open banking, and mergers and adjudication work, the FSU will monitor

and promote competition in Australia’s financial services sector by

assessing competition issues, undertaking market studies, and reporting

regularly on emerging issues and trends in the sector.

The FSU is currently examining the pricing of foreign currency

conversion services in Australia to evaluate whether there are

impediments to effective price competition in the sector. An inquiry

report is to be delivered to the Treasurer by 31 May 2019.

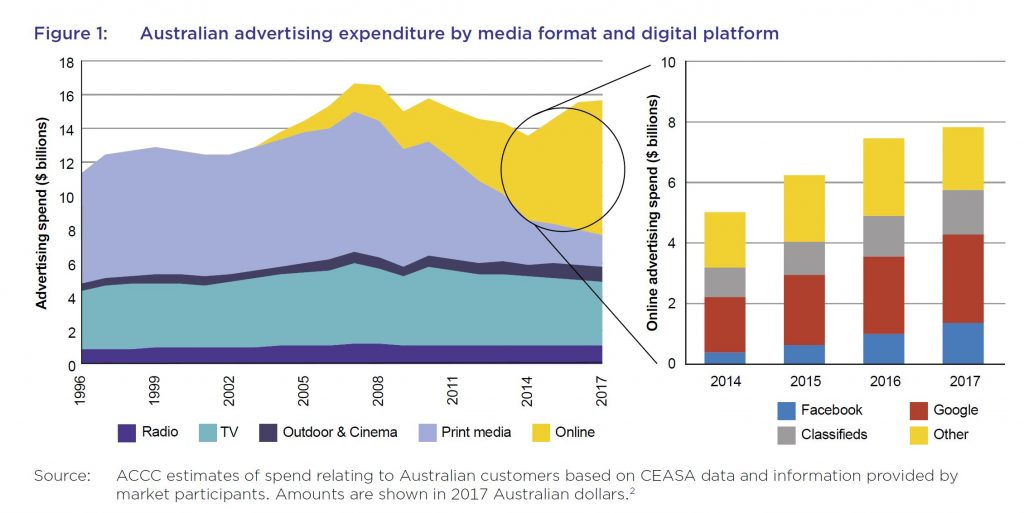

The issues raised are significant and far reaching, and questions the substantial market power players such as Google and Facebook have, the data they capture and monitise and their impact on the media. 94 per cent of online searches in Australia currently performed through Google.

Facebook and Instagram together obtain approximately 46 per cent of Australian display advertising revenue. No other website or application has a market share of more than five per cent.

They say there is a lack of transparency in the operation of Google and Facebook’s key algorithms, and the other factors influencing the display of results on Google’s search engine results page, and the surfacing of content on Facebook’s News feed.

Anti-competitive discrimination by digital platforms in favour of a related business has been found to exist in overseas cases. For example, in the European Commission’s 2017 decision, Google was found to have systematically given prominent placement to its own comparison shopping service (Google Shopping) and to have demoted rival comparison shopping services in its search results.

Monopoly or near monopoly businesses are often subject to specific regulation due to the risks of competitive harm. The risk of competitive harm increases when the monopoly business is vertically integrated. The ACCC considers that Google and Facebook each have substantial market power and each have activities across the digital advertising supply chain. Google in particular occupies a near monopoly position in online search and online search advertising, and has multiple related businesses offering advertising services.

This is their executive summary:

On 4 December 2017, the then Treasurer, the Hon Scott Morrison MP, directed the Australian Competition and Consumer Commission (the ACCC) to hold an inquiry into the impact of online search engines, social media and digital content aggregators (digital platforms) on competition in the media and advertising services markets. The ACCC was directed to look at the implications of these impacts for media content creators, advertisers and consumers and, in particular, to consider the impact on news and journalistic content.

Digital platforms offer innovative and popular services to consumers that have, in many cases, revolutionised the way consumers communicate with each other, access news and information and interact with business. Many of the services offered by digital platforms provide significant benefits to both consumers and business; as demonstrated by their widespread and frequent use by many Australians and many Australian businesses.

The ACCC considers, however, that we are at a critical point in considering the impact of digital platforms on society. While the ACCC recognises their significant benefits to consumers and businesses, there are important questions to be asked about the role the global digital platforms play in the supply of news and journalism in Australia, what responsibility they should hold as gateways to information and business, and the extent to which they should be accountable for their influence. In particular, this report identifies concerns with the ability and incentive of key digital platforms to favour their own business interests, through their market power and presence across multiple markets, the digital platforms’ impact on the ability of content creators to monetise their content, and the lack of transparency in digital platforms’ operations for advertisers, media businesses and consumers.

Consumers’ awareness and understanding of the extensive amount of information about them collected by digital platforms, and their concerns regarding the privacy of their data, are also critical issues. There are also issues with the role of digital platforms in determining what news and information is accessed by Australians, how this information is provided, and its range and reliability.

Digital platforms are having a profound impact on Australian news media and advertising. The impact of digital platforms on the supply of news and journalism is particularly significant. News and journalism generate broad benefits for society through the production and dissemination of knowledge, the exposure of corruption, and holding governments and other decision makers to account.

It is important that governments and the public are aware of, and understand, the implications of the operation of these digital platforms, their business models and their market power.

The ACCC’s research and analysis to date has provided a valuable understanding of the markets that are the subject of this Inquiry, including information that has not previously been available, and has identified a number of issues that could, or should, be addressed. Many of these issues are complex.

The ACCC has decided that the best way to address these issues in the final report, due 3 June 2019, is to identify preliminary recommendations and areas for further analysis, and to engage with stakeholders on these potential proposals. Such engagement may result in considerable change from the ACCC’s current views, as expressed in this report.

The ACCC says many people are either abandoning their private health insurance policies or downgrading to lower-cost, lower-benefit products as premium increases continue to outpace inflation and wage growth.

In its annual report into the private health insurance industry, the ACCC found Australians are increasingly dropping their hospital cover, instead opting for just extras cover. Many people are also choosing policies with higher excess payments in an attempt to keep policy premiums to a minimum.

“People are increasingly feeling the pinch of private health premium increases and growing gap payments. In response, many are shifting to cheaper products with reduced coverage, and some are dropping their cover altogether,” ACCC Deputy Chair Delia Rickard said.

The affordability of private health insurance has been an increasing concern for consumers in recent years.

Many insurers will be updating their policies ahead of the Australian Government’s private health insurance reforms, which aim to make private health insurance simpler and more affordable, and come into effect on 1 April 2019.

The ACCC is warning private health insurers they must provide clear, prominent and timely communication with customers regarding changes.

“Private health funds have clear obligations not to mislead their customers under the Australian Consumer Law. Failing to properly tell customers about cuts to their benefits or policies may be a breach of the law,” Ms Rickard said.

“Ahead of 1 April 2019, we will be monitoring to see how health funds are telling consumers about changes to their policies and benefits. Private health insurers need to be transparent about what is and isn’t included in their policies or risk losing their customers’ trust and ultimately, their business.”

In 2017–18, consumers paid about $23.9 billion in private health insurance premiums, an increase of almost $834 million or 3.6 per cent from 2016–17.

The amount of hospital benefits paid by health insurers was $15.1 billion and the amount of extras treatment benefits paid was $5.2 billion.

In June 2018, 45.1 per cent of the Australian population held hospital-only or combined health insurance cover, a decrease of 0.9 percentage points from June 2017.

The proportion of the population holding extras-only policies increased from 8.9 per cent in June 2017 to 9.2 per cent in June 2018.

About 88 per cent of in-hospital treatments were delivered with no gap payments.

The average out-of-pocket expenses from hospital treatment increased by 3.3 per cent. Extras treatment recorded a decline of 0.7 per cent.

Consumers are also continuing to shift to lower cost policies with exclusions, or excess and co-payments. In June 2018, 44 per cent of hospital policies held had exclusions, compared with 40 per cent in June 2017. There was also an increase in hospital policies with an excess or co-payment from 83 per cent to 84 per cent.

Complaints to the Private Health Insurance Ombudsman (PHIO) have decreased by 21 per cent since June 2017. The PHIO attributes this to improved complaint handling processes of larger insurers and the smaller premium increases in 2018 compared to recent years.

Despite the decrease, the number of complaints received by the PHIO in 2017–18 is the second highest level recorded over the past five years.

Private health funds must provide accurate disclosures about their policies including any changes to the benefits available under their policies. Funds are not exempt from regulation and can face significant penalties if they breach the Australian Consumer Law (ACL).

Private health insurers and other health industry participants have been the subject of a number of recent ACCC enforcement matters for alleged ACL breaches. The ACCC has recently finalised action against Australian Unity. Enforcement matters involving NIB and Ramsay Health Care are ongoing, and the ACCC’s appeal in the Medibank matter is awaiting judgment.

Background

Each year, the ACCC is required by the Senate to produce a report on key competition and consumer developments and trends impacting on people’s health cover. This report covers the 2017–18 period.

This is the ACCC’s 20th report to the Senate under this order.

The ACCC has granted authorisation for arrangements between SA Housing Authority, Renewal SA and land and property developers, which are designed to increase Adelaide’s supply of affordable housing.

This authorisation enables developers to agree to requests from SA Housing Authority or Renewal SA which could otherwise be a breach of competition laws, including agreement to cap prices for some properties, to rent or sell to certain identified tenants or purchasers, or agreement not to compete for the rental or sale of property.

The South Australian government’s stated goal is to make 15 per cent of all new significant developments available as affordable housing for people in the low to moderate income category, such as people employed in the health care, social services and administrative support occupations.

“The arrangements are likely to increase the affordable housing stock in the greater metropolitan region of Adelaide. This is likely to benefit people who are otherwise unable to access the general housing market or social housing in the region,” ACCC Commissioner Mr Roger Featherston said.

On 27 September 2018, the ACCC issued a draft determination proposing to grant authorisation for 10 years. No concerns have been raised about the arrangements.

“Housing affordability criteria are set and published by the South Australia government and developers have a wide range of land and property developments from which to choose,” Mr Featherston said.

Authorisation provides statutory protection from court action for conduct that might otherwise raise concerns under the competition provisions of the Competition and Consumer Act 2010. Broadly, the ACCC may grant an authorisation when it is satisfied that the public benefit from the conduct outweighs any public detriment.

Background

In this case, SA Housing Authority and Renewal SA, and land and property developers may be considered competitors for the supply of affordable housing.

Therefore, by arranging to cap prices and not compete for the supply of rentals and the sale of properties, they risk breaching competition laws unless they have ACCC authorisation.

The ACCC says that the Federal Court has imposed record penalties totalling $18 million against We Buy Houses Pty Ltd (We Buy Houses) and its sole director, Rick Otton, for making false or misleading representations about how people could create wealth through buying and selling real estate, following ACCC action.

The penalties of $12 million imposed against We Buy Houses, and $6 million imposed against Mr Otton personally, are the highest ever imposed for contraventions of the Australian Consumer Law by a corporation and an individual, respectively.

The Federal Court also banned Mr Otton from managing corporations for 10 years in Australia and permanently restrained Mr Otton and We Buy Houses from further involvement in the supply or promotion of services or advice concerning real property transactions or investment.

“We Buy Houses and Mr Otton peddled false hope to people simply looking to get a foothold in the housing market or invest money in real estate for their future,” said ACCC Chair, Rod Sims.

“The record penalties imposed against both We Buy Houses and Mr Otton reflect their egregious conduct.”

“They have also effectively been permanently banned from any further involvement in real estate in order to protect consumers,” Mr Sims said.

“These record penalties demonstrate the determination of the ACCC to take strong and effective enforcement action against businesses and individuals who prey on consumers using the false hope of creating financial success. The judgement signals the Court’s condemnation of false and misleading property spruiking and get rich quick schemes.”

“This outcome also reflects a recent trend of higher penalties for Australian Consumer Law breaches. We can expect this to continue following recent law changes to increase maximum financial penalties under consumer law,” Mr Sims said.

We Buy Houses and Mr Otton taught real estate investment strategies via free seminars, and paid ‘boot camps’ and mentoring programs that claimed people could:

buy a house for $1, without needing a deposit, bank loan or real estate experience, or using little or none of their own money

create passive income streams through property and quit their jobs

build a property portfolio without their own money invested, new bank loans or any real estate experience, and

start making profits immediately and create or generate wealth.

“In her judgement on liability, Justice Gleeson said the free seminars were a waste of time, and that the boot camps and the mentoring programs were an expensive waste of time,” Mr Sims said.

The Court also found that Mr Otton had made false or misleading representations that he had successfully implemented the wealth creation strategies he taught. In addition, a book authored by Mr Otton, and websites operated by We Buy Houses and Mr Otton, included testimonials from ‘students’ claiming they were able to buy a house for $1, which the court found were false or misleading.

Background

The ACCC instituted proceedings against We Buy Houses and Mr Otton in March 2015 following a coordinated investigation with New South Wales Fair Trading. On 11 August 2017, the Federal Court delivered judgment on liability, finding that Mr Otton and/or We Buy Houses had engaged in multiple contraventions of sections 18, 29(1)(f), 29(1)(g), 34 and 37 of the Australian Consumer Law.

We Buy Houses had been conducting training programs including free seminars, boot camps and mentoring programs throughout Australia since around 2000. Between 2011 and 2014, We Buy Houses generated the majority of its $20 million revenue from conducting these training programs.

The ACCC has issued a draft determination proposing to authorise SA Housing Authority and Renewal SA to enter into arrangements with land and property developers to increase the supply of affordable housing in the greater metropolitan region of Adelaide.

The government of South Australia has set a goal that 15 per cent of all new significant developments should be available as affordable housing.

Affordable housing is to be made available to people in the low to moderate income category, who are often employed in the health care, social services and administrative support occupations.

Under the proposed arrangements, SA Housing Authority and Renewal SA may ask developers to agree to cap prices for properties in some developments, agree to rent or sell to specified tenants or purchasers and agree not to compete for the rental or sale of property.

“The ACCC considers that the arrangements are likely to contribute to an increase in the supply of affordable housing in the greater metropolitan region of Adelaide. People who may otherwise find themselves excluded from both the general housing market and social housing, are likely to benefit from an increase in affordable housing,” ACCC Commissioner Mr Roger Featherston said.

“The arrangements are unlikely to result in public detriment. Housing affordability criteria are set and published by the government of South Australia and developers have a wide range of land and property developments from which to choose.”

The ACCC proposes to grant authorisation for 10 years and expects to make a final determination in November 2018.

Further information about the application for authorisation, including copies of the ACCC’s draft determination and public submissions, is available at SA Housing Authority and Renewal SA.

Authorisation provides statutory protection from court action for conduct that might otherwise raise concerns under the competition provisions of the Competition and Consumer Act 2010. Broadly, the ACCC may grant an authorisation when it is satisfied that the public benefit from the conduct outweighs any public detriment.

Authorisation is sought as the proposed conduct may contain a cartel provision.

Background

SA Housing Authority and Renewal SA, and land and property developers may be considered competitors for the supply of affordable housing.

Therefore, by arranging to cap prices and not compete for the supply of rentals and the sale of properties, they risk breaching competition laws unless they have ACCC authorisation.

The ACCC says that scammers are increasingly catching out people by impersonating well-known businesses or the police so they can get access to computers and steal money or banking information.

The ACCC’s Scamwatch website has recorded a significant spike in these types of scams, known as remote access scams, with more than 8000 reports recorded in 2018 so far and losses totalling $4.4 million.

“The spike in remote access scams is very concerning; losses so far in 2018 have already surpassed those for the whole of 2017, and sadly it is older Australians that are losing the most money,” ACCC Deputy Chair Delia Rickard said.

Scammers will impersonate a well-known company, most commonly Telstra, NBN or Microsoft, or even the police, and spin you a very credible and believable story about why they need to access your computer using software such as TeamViewer.

“The scammers are becoming more sophisticated. The old trick scammers used to use was to call people and say there was a virus on their computer that needed fixing but, in a new twist, scammers are now telling people they need their help to catch hackers,” Ms Rickard said.

The scammers claim they are tracking the ‘scammers’ or ‘hackers’, and tell the consumer that their computer has been compromised and is being used to send scam messages. This is where they say with the victim’s help, they can use the victim’s computer and online banking to trap the (fake) ‘scammer’.

The scammer will then pretend to deposit money into their victim’s account. In reality the scammer just shuffles money between the victim’s accounts (for example, from a person’s credit card account to a savings account), which gives the illusion of money being deposited. The money is then sent out of the victim’s account as part of the con to ‘catch a scammer’, straight to the scammer’s own bank accounts.

“Unfortunately there are many stories from people who give a scammer access to their computer and are then conned into giving access to online banking. Some are also tricked into providing iTunes gift card numbers over the phone to these scammers,” Ms Rickard said.

Once the scammer has a victim on the hook, if they start to doubt the situation, the scammer will become threatening, stating that the victim would jeopardise the investigation if they refuse to help and may even face legal consequences.

These types of scam can be very scary, as scammers can become threatening and aggressive if they sense they are ‘losing’ the victim, or starting to cotton on. This is particularly frightening for older people who may not be as tech savvy.

“It’s vital that people remember they should never, ever, give an unsolicited caller access to your computer, and under no circumstances offer your personal, credit card or online account details over the phone,” Ms Rickard.

“If you receive a phone call out of the blue about your computer and remote access is requested, it’s a scam 100 per cent of the time. Just hang up.”

The ACCC says that the Federal Court has found one of Australia’s largest debt collection firms, ACM Group Ltd, engaged in misleading or deceptive conduct, harassment and coercion, and unconscionable conduct in its dealings with two vulnerable consumers.

ACM’s conduct was found to be in contravention of the Australian Consumer Law.

The ACCC brought the action against ACM in respect of its conduct between 2011 and 2015 in pursuing two vulnerable customers who had defaulted on their phone bills. Their debts had been on-sold by their service provider to ACM for debt recovery.

“The ACCC and ASIC have done extensive work to improve debt collection practices,” ACCC Commissioner Sarah Court said.

“Lower-income groups suffer greater stress because of debt collection practices and have limited access to legal support, while creditors are using improper ways to escalate disputes.”

“This conduct by ACM was particularly egregious, as it included ongoing harassment of a care facility resident who had difficulty communicating after suffering multiple strokes, as well as a Centrelink recipient who was falsely told their credit would be affected for up to seven years if they failed to pay immediately,” Ms Court said.

“ACM was found to have made empty threats to litigate against both customers despite knowing they had no means, or only limited means, to repay.”

“One of the ACCC’s enduring enforcement priorities is taking action against conduct that impacts disadvantaged or vulnerable consumers,” Ms Court said.

In his judgment, Griffiths J rejected a number of explanations of why ACM had contacted one of the consumers 34 times and found that conduct amounted to undue harassment and coercion.

Griffiths J also found that the multiple telephone calls, coupled with the number and content of its correspondence was calculated to intimidate or demoralise the consumer.

Griffiths J stated that “ACM cannot justify its conduct on the basis that it required verification of information about [the] medical or financial circumstances when ACM itself did not take reasonable steps to contact people who may have been in a position to provide such verification”.

Background

The alleged conduct occurred between 2011–2015 in relation to one consumer, a resident in a care facility, and in September 2014 in relation to the other consumer, a single parent with a limited income. In each case, the debt being pursued had been sold to ACM Group by Telstra.

In 2012, in a case brought by ASIC, the Federal Court found that ACM Group had harassed and coerced consumers and engaged in ‘widespread’ and ‘systemic’ misleading and deceptive conduct when seeking to recover money.

In July 2014, the ACCC and ASIC released updated guidelines for debt collection firms regarding their contact with consumers and compliance with the law. The guidelines encourage debt collectors to be flexible, fair and realistic and to recognise debtors who are vulnerable. The industry association for debt buyers, the Australian Collectors & Debt Buyers Association, required its members to accept these guidelines in March 2016.

Both the ACCC and ASIC are responsible for consumer protection in the debt collection industry. The two agencies work closely and in this case ASIC delegated its powers to the ACCC to pursue this action.

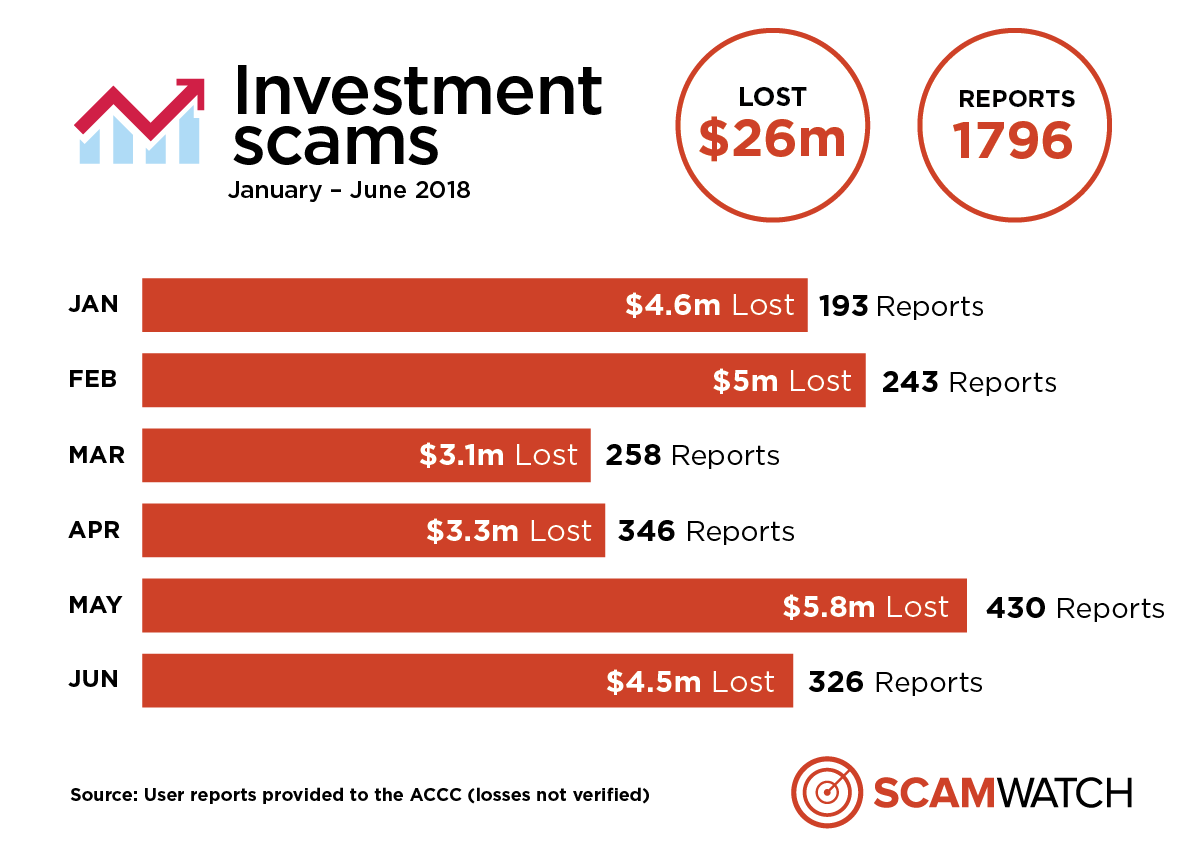

Scamwatch is warning the Australian community to be wary about investment scams, with statistics revealing Australians are collectively losing $4.3 million a month to these scams.

In 2018, more than $26 million has been reported lost to investment scams—already 84 per cent of the total losses recorded in 2017. This represents an average month on month increase in losses of 117 per cent compared to last year.

“The losses to investment scams are horrific. Each week the ACCC receives heartbreaking accounts of people losing hundreds of thousands, and in some cases millions, of dollars,” ACCC Deputy Chair Delia Rickard said.

“Last year, Australians reported they lost $64.6 million to investment scams to Scamwatch and the Australian Cybercrime Online Reporting Network (ACORN). If the current trend continues, combined losses reported to Scamwatch and ACORN in 2018 could be in excess of $100 million.”

“These scams are very sophisticated and the scammers are very convincing. People aged 45–64 are most at risk and make up more than half the reports sent to Scamwatch,” Ms Rickard said.

The vast majority of investment scams are still centred on traditional investment markets like stocks, real estate or commodities. For example, scammers will cold call victims claiming to be a stock broker or investment portfolio manager and offer a ‘hot tip’ or inside information on a stock or asset that is supposedly about to go up significantly in value. They will claim what they are offering is low-risk and will provide quick and high returns.

“Scammers will spend significant time and effort grooming their victims to invest. They will use the right technical language and also offer professional looking websites and documents to convince victims they are legitimate. It’s often only when people try to cash out their investment that they realise their money is gone,” Ms Rickard said.

Two other types of investments where scams are prevalent are cryptocurrency trading and binary options. Cryptocurrency trading scams have grown significantly in the past 12 months and are now the second most common type of investment scam offer pushed on victims.

“The rise in popularity in cryptocurrency trading has not been missed by scammers who are latching onto this new trend to con people. These are similar to any other investment scam: the scammer will claim to have inside knowledge about price movements they will use to make you a fortune. If you invest, your money will quickly disappear,” Ms Rickard said.

“Binary options trading involves scammers pretending they can predict the movements of a commodity, asset or index prices over a short time. They direct you to a website with a login, account details and a trading platform. They appear to put your money into the account and demonstrate a number of successful trades to encourage you to invest greater sums. Then your money begins to disappear and so too does the scammer.”

The clearest warning sign you’re dealing an investment scammer is how they contact you and the promises they make.

“It can be very difficult to tell what is and isn’t legitimate these days. If someone calls, emails or texts you out of the blue with investment advice, don’t engage with them no matter how legitimate they sound. Hang up the phone, or delete the email or text. If you’re searching for new investment opportunities online, don’t always trust what you read. It’s easy for scammers to create professional looking investment websites,” Ms Rickard said.

“Any claims like ‘risk-free investment’, ‘low risk, high return’, ‘be a millionaire in three years’, or ‘get-rich quick’ are also easy tells that you’re dealing with a scammer.”