The new AHURI report highlight the fact that more Australians are taking mortgage debt into retirement, will have to us superannuation to repay the debt, and so put more pressure on Government in terms of future support.

High debt into retirement is also leading to more stress.

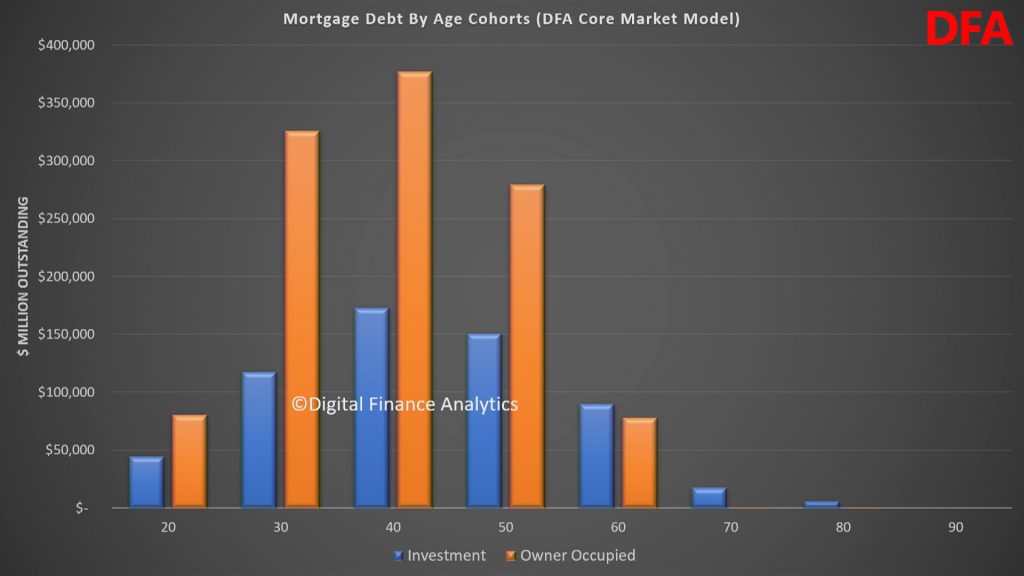

Our surveys show the relative debt by age cohorts. The trends are “moving to the right” as people buy later, get larger loans, and hold them into retirement. Overall debt has never been higher.

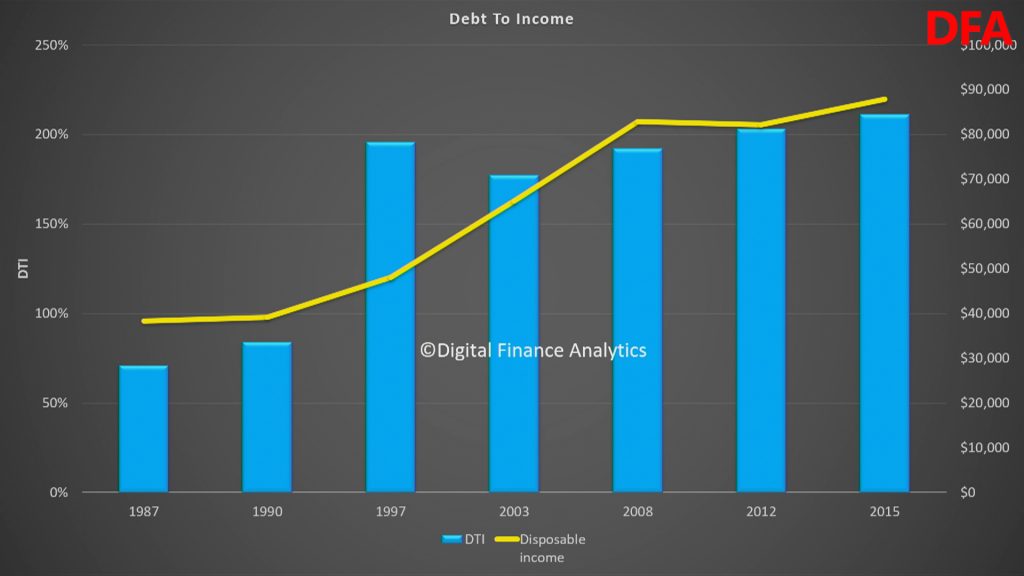

As a result the debt to income ratio of those over 55 years has deteriorated significantly.

The final point to make is households as they enter retirement will be more reliant on fixed incomes, at a time when savings rates on deposits are at a record low. So servicing this debt into retirement will be a major issue.

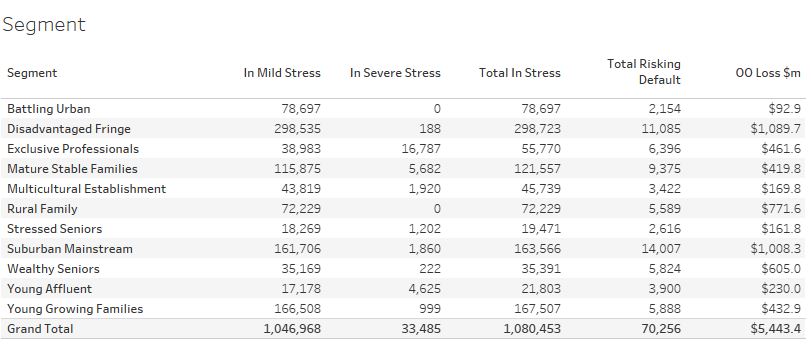

Combined this explains why mortgage stress is lurking among older households, as our July stress data revealed. This includes more than 35,000 “Wealthy Seniors” across the country.

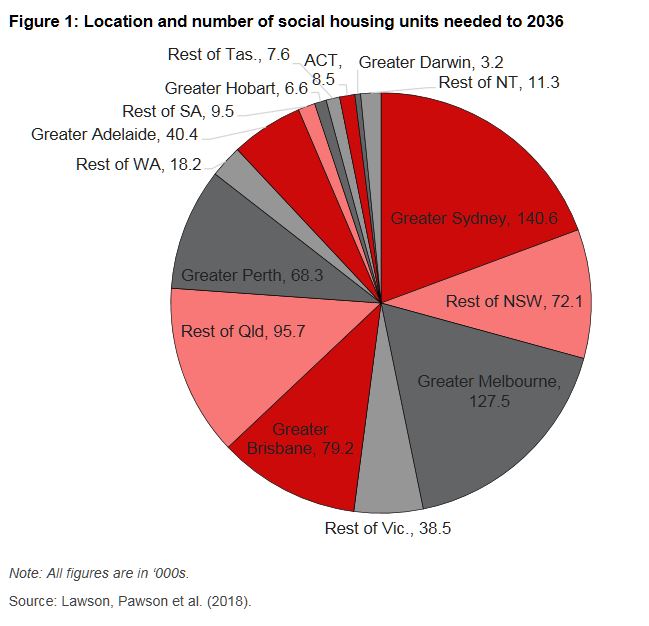

Australia will need another 730,000 social housing dwellings in 20 years if it is to tackle homelessness and housing stress among low-income renters. These are the findings of a new report from the Australian Housing and Urban Research Institute (AHURI), which shows social housing is in urgent need of direct public investment; via The Conversation.

Instead of directly investing in social housing, the federal

government has sought to establish investment opportunities for other

actors, such as pension funds and private corporations.

The federal government has also encouraged states and territories to

focus public resources on supply, land policy reform and the use of planning methods such as inclusionary zoning to deliver affordable and social housing.

These initiatives are worthy, but they won’t generate enough new

social housing supply on their own. Without direct public investment in

the form of a needs-based capital investment program, the government is

unlikely to fill the social housing gap.

Needs-based capital investment is where decisions on what to invest

is not only based on financial return, but also on other factors like

the effects on society (so infrastructure investment is one which is

needs based).

And needs-based capital investment provides the most cost effective

mechanism to influence the scale, location and quality of housing

produced.

Social housing supply is dangerously lagging

The Australian Bureau of Statistics estimated 116,000 people were

homeless in 2016, living in improvised and severely overcrowded homes.

Our further analysis of the 2016 Census

shows 315,000 households rely on very low incomes, paying more than 30%

of their income on rent. This is known as housing stress.

To address homelessness and housing stress right now, we need an

additional 430,000 social housing dwellings. And this will grow over

time.

Between 1951 and 1996, Australian jurisdictions built

8,000 to 14,000 social housing dwellings per year. In those years,

social housing building programs were funded through direct public

investment, with grants and long-term loans.

But without direct investment, social housing construction levels have languished since the mid 1990s.

In fact, the total number of Australian households increased by 30%

from 1996 to 2016, and yet social housing grew by just 4%. This means

there is a substantial backlog in supply, and the need for resources is

now urgent.

Subsidies alone won’t cut it

It’s naive to think social housing systems can be adequately

resourced through demand-side subsidies alone, such as cash support to

tenants. In the UK,

for instance, we’ve seen that while rent assistance budgets have grown,

they haven’t helped to grow an affordable supply of homes, especially

in tight, unregulated private rental markets.

In Australia, the Productivity Commission found that even after rent

assistance is paid to eligible pensioners, 40.3% of them pay more than

30% of their incomes on rent. This leaves little for life’s other essentials, such as food, medical care and electricity.

What’s more, the spatial distribution of need for social housing is

just as important as the overall volume, as the costs for these

dwellings vary from A$146,000 to A$614,000, depending on local land

values, building types and construction costs in different regions.

So it’s imperative any public investment program is carefully designed and spatially nuanced.

The AHURI report calls for a new National Housing Authority

The AHURI report also assesses the costs of land and construction needed for social housing, which would underpin a capital investment program.

It calls for the creation of a National Housing Authority to inform,

co-ordinate and fund the expansion of new social housing supply through a

needs-based capital investment program, together with the existing

National Housing Finance Investment Corporation (NHFIC).

In the past, social housing relied on external industry bodies, such

as the National Housing Supply Council, to advise on Australia’s future

housing needs.

But a national housing authority would provide more effective,

consistent and authoritative leadership. It would have the

responsibility and resources to plan for and fund more inclusive and

sustainable housing outcomes. And it would co-ordinate this effort with

other key stakeholders including state Housing Authorities, not for

profit community housing providers, the National Disability Insurance

Scheme and Clean Energy Finance Corporation.

A net benefit to society

The way cost-benefit assessments are conducted must be changed so the

social benefits of social housing are properly quantified. This is

necessary not only to capture both productivity and social gains, but

also for making a coherent rationale for social housing investment.

But there is more work to be done to improve methods for cost-benefit analysis for social housing, the report says.

In contrast to conventional infrastructure, the housing sector has

suffered from a long-term lack of investment. This means the methods for

cost-benefit analysis are not yet as advanced.

It’s clear there is no fundamental barrier to government sourced large-scale investment in social housing. An improved cost-benefit analysis method can provide assurance to funding agencies that a long-term social housing construction program is viable and cost effective.

Authors: Julie Lawson, Honorary Associate Professor, Centre for Urban Research, RMIT University; Jago Dodson, Professor of Urban Policy and Director, Centre for Urban Research, RMIT University; Kathleen Flanagan, Research Fellow & Deputy Director, HACRU, University of Tasmania; Keith Jacobs, Professor of Sociology, University of Tasmania; Laurence Troy, Research Fellow, City Futures Research Centre, UNSW; Ryan van den Nouwelant, Lecturer in Urban Management and Planning, Western Sydney University

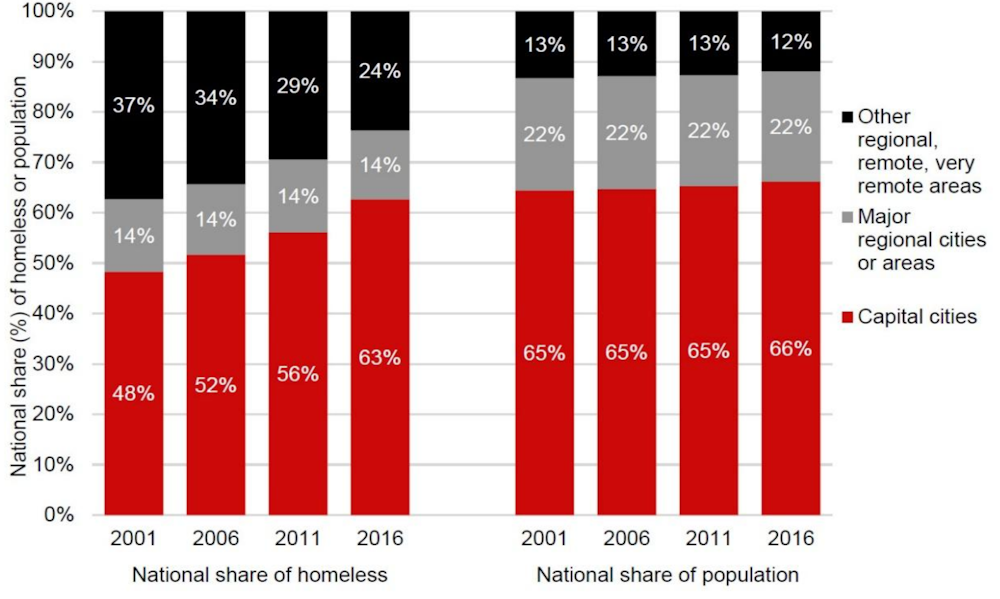

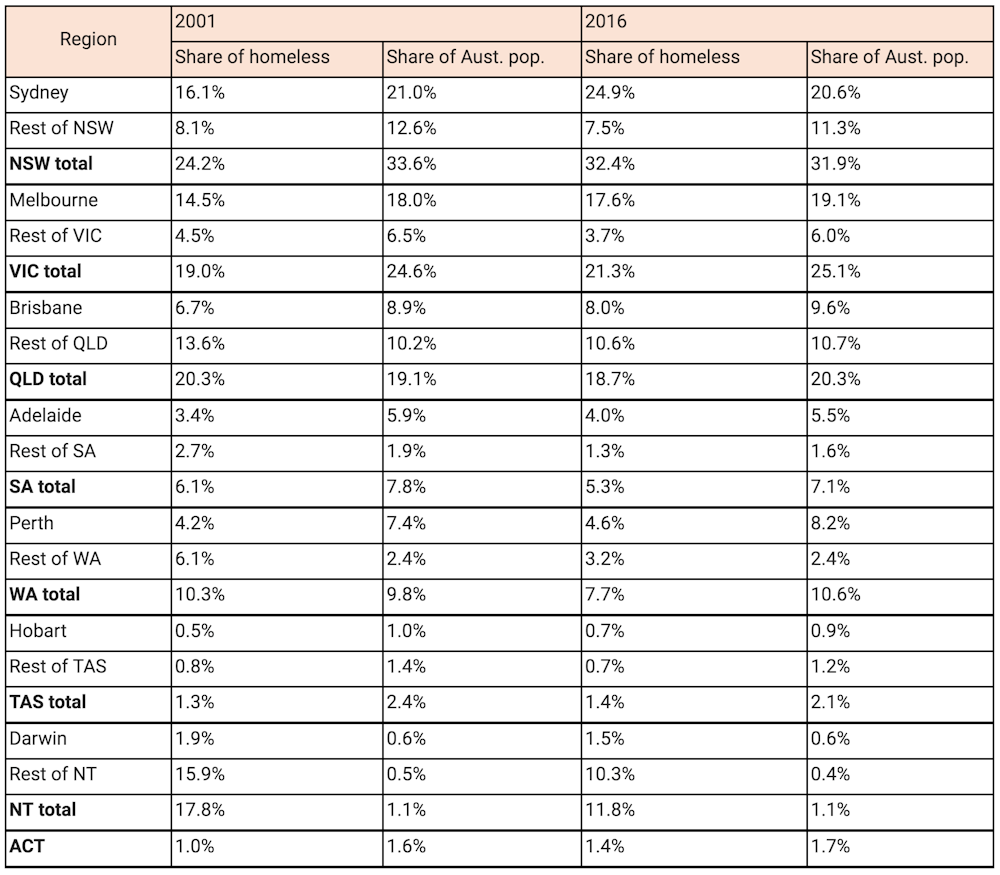

Homelessness has increased greatly in Australian capital cities since 2001. Almost two-thirds of people experiencing homelessness are in these cities, with much of the growth associated with severely crowded dwellings and rough sleeping.

Homelessness in major cities, especially severe crowding, has risen

disproportionately in areas with a shortage of affordable private rental

housing and higher median rents. Severe crowding is also strongly

associated with weak labour markets and poorer areas with a high

proportion of males.

These are some of the key findings of our Australian Housing and Urban Research Institute (AHURI) research released today.

People counted as homeless

on census night live in: improvised dwellings, tents or sleeping out

(rough sleeping); supported accommodation; staying temporarily with

other households (i.e. couch surfing); boarding houses; temporary

lodging; or severely crowded conditions.

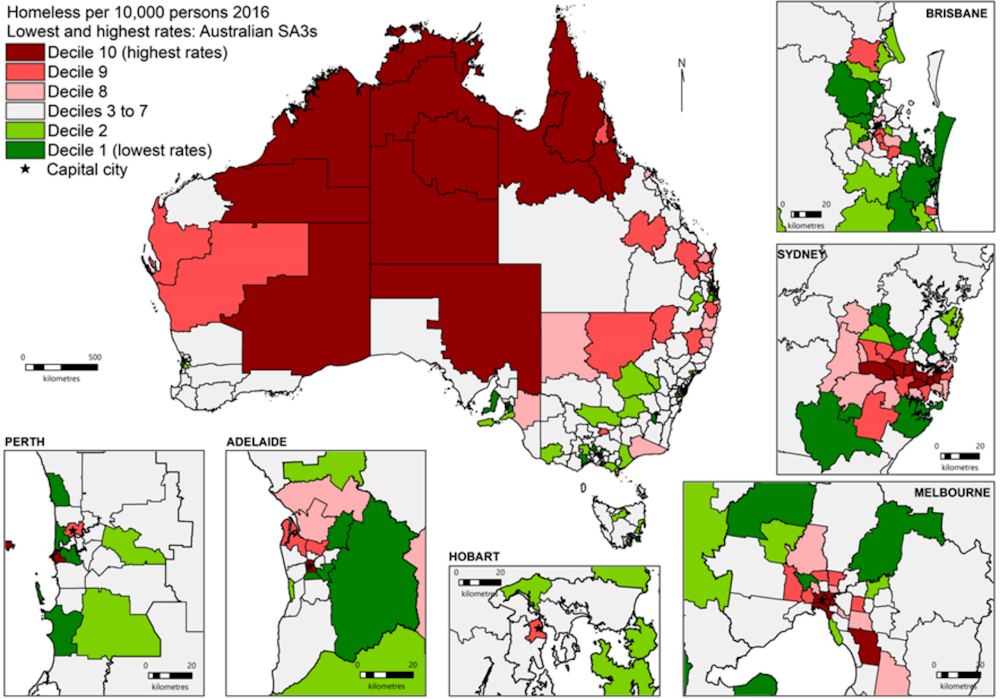

How has the geography of homelessness changed?

Nationally, 63% of all homelessness is found in capital cities. That’s up from 48% in 2001.

Shares (%) of homelessness and population by area type

At the same time, homelessness has been falling in remote and very

remote areas. However, it still remains higher in these areas per head

of population.

Homelessness is also becoming more dispersed across major cities.

In Sydney, a corridor of high homelessness rates stretches from the

inner city westward through suburbs such as Marrickville, Canterbury,

Strathfield, Auburn and Fairfield (more than 30km from the CBD).

In Melbourne, high homelessness rates are found in Dandenong (around

25km southeast of the CBD), Maribyrnong and Brimbank to the west,

Moreland and Darebin to the north and Whitehorse to the east, about 15km

from the CBD.

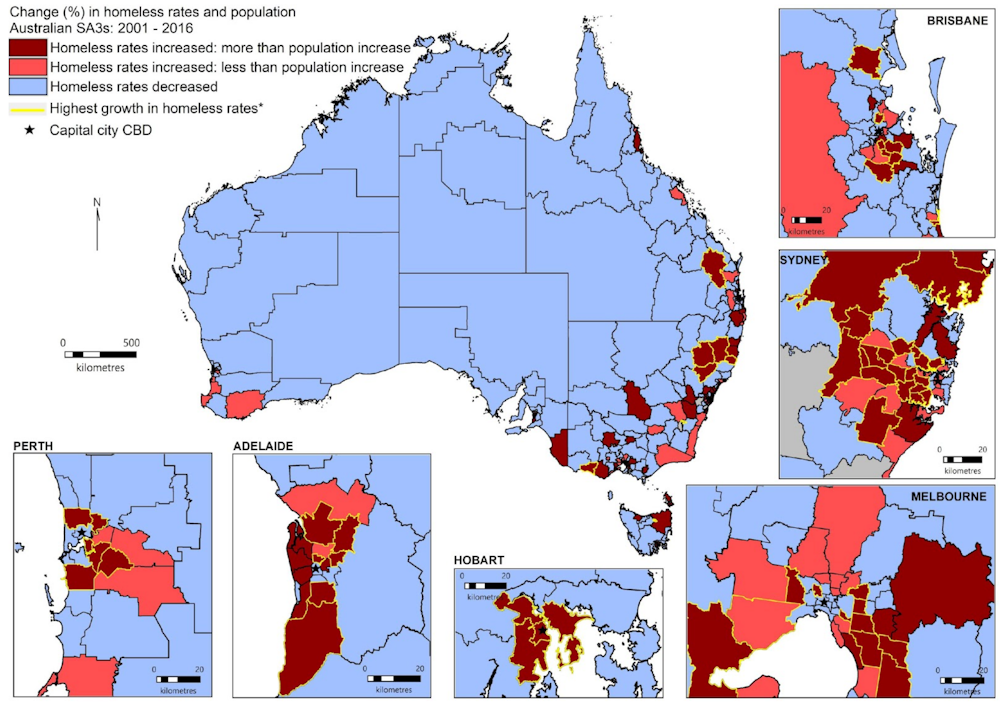

After accounting for population growth, we see a decline in homeless

rates in the CBD and inner areas of Perth, Adelaide, Melbourne and to an

extent Brisbane over the 15 years. At the same time, homeless rates in

outer urban areas have increased. In many regions this increase outpaced

population growth.

Change in homeless rate compared with population growth 2001–2016

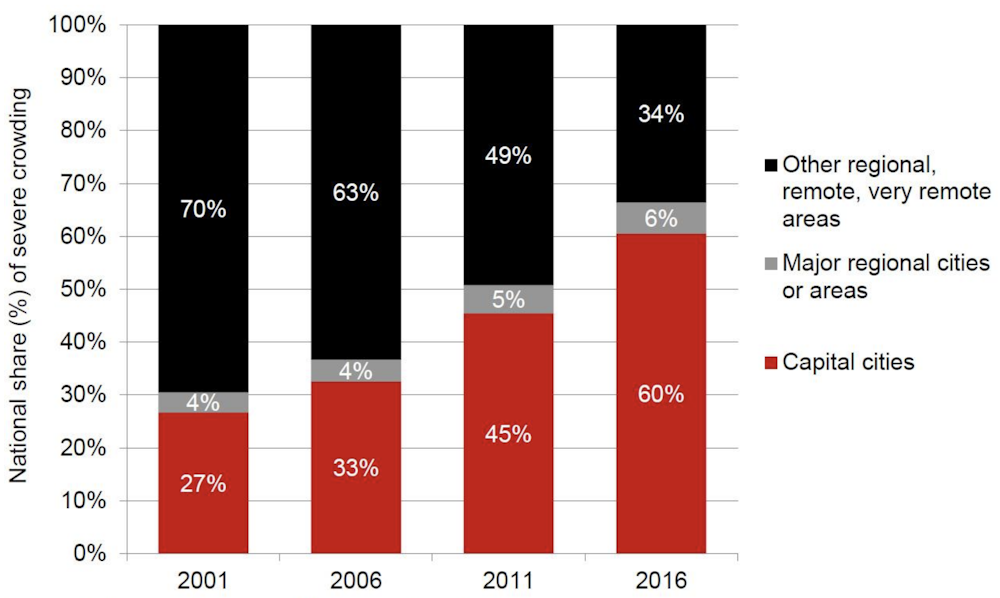

The numbers of households living in severely crowded dwellings in

capital cities have doubled in 15 years, accounting for much of the

growth in homelessness overall. In 2001, this group accounted for 35% of

people experiencing homelessness, with 27% living in cities. By 2016,

severe crowding rates had soared to 44% of all people experiencing

homelessness, with 60% living in capital cities.

Rough sleeping has also transformed into an urban phenomenon — nearly

half of all rough sleepers in Australia are now found in capital

cities.

What is driving these changes?

Homelessness has risen disproportionately in areas with a shortage of

affordable private rental housing and higher median rents. That’s

especially the case in Sydney, Hobart and Melbourne. In capital city

areas with a shortage of affordable private rentals in both 2001 and

2016, severe crowding grew rapidly (by 290.5%) against all homelessness

growth (32.6%).

Changes in share of homeless and population by city and region, 2001-16

The effects of rental affordability on homelessness rates still hold

after controlling for other area characteristics. We also find that

these rates are strongly correlated with higher shares of particular

demographic groups in an area, including males, younger age groups,

young families, those with an Indigenous or ethnic background, and

unmarried persons.

Severe crowding in capital cities is also strongly associated with

weak labour markets and poorer areas with a high proportion of males.

However, these associations do not hold for severe crowding in remote

areas.

Governments must find ways to urgently increase both the supply and

size of affordable rental dwellings for people with the lowest incomes.

We also require better integration of planning, labour, income support

and housing policies targeted to areas of high need.

Rates of severe crowding remain highest in remote areas, and

continued efforts to increase housing supply in remote areas, such as

the National Partnership on Remote Housing (NPRH), are needed. Targeted responses are required to combat its growth in major cities.

It is critical that specialist homelessness services, as a first

response to homelessness, are well located to respond in areas where

demand is highest.

Authors: Sharon Parkinson, Senior Research Fellow, Centre for Urban Transitions, Swinburne University of Technology; Deb Batterham, PhD Candidate, Centre for Urban Transitions, Swinburne University of Technology; Margaret Reynolds, Researcher, Centre for Urban Transitions, Swinburne University of Technology

AHURI is a national independent research network with an expert not-for-profit research management company, AHURI Limited, at its centre. AHURI undertakes evidence-based policy development on a range of priority policy topics that are of interest to our audience groups, including housing and labour markets, urban growth and renewal, planning and infrastructure development, housing supply and affordability, homelessness, economic productivity, and social cohesion and wellbeing.

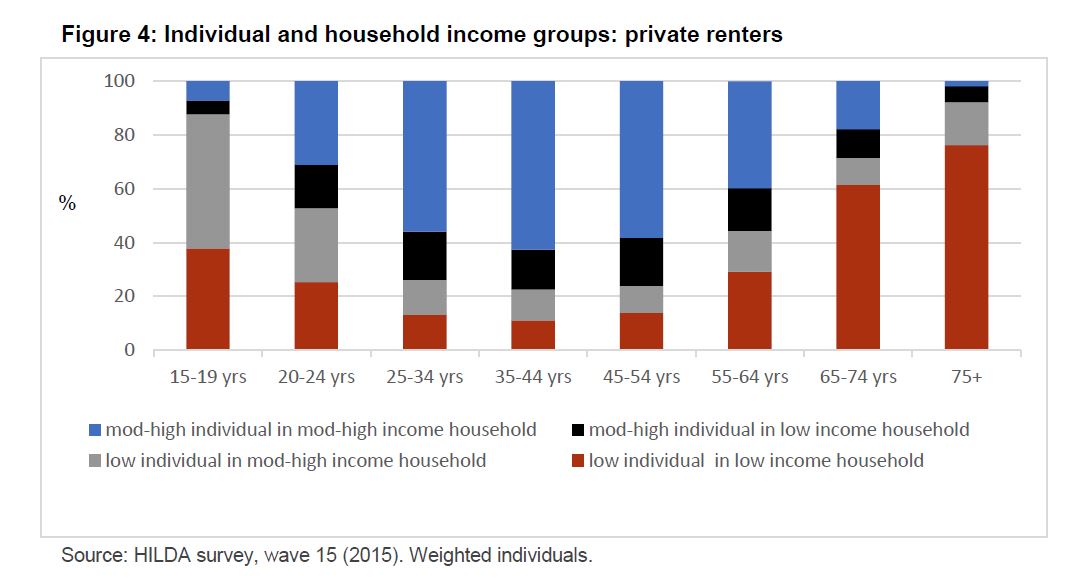

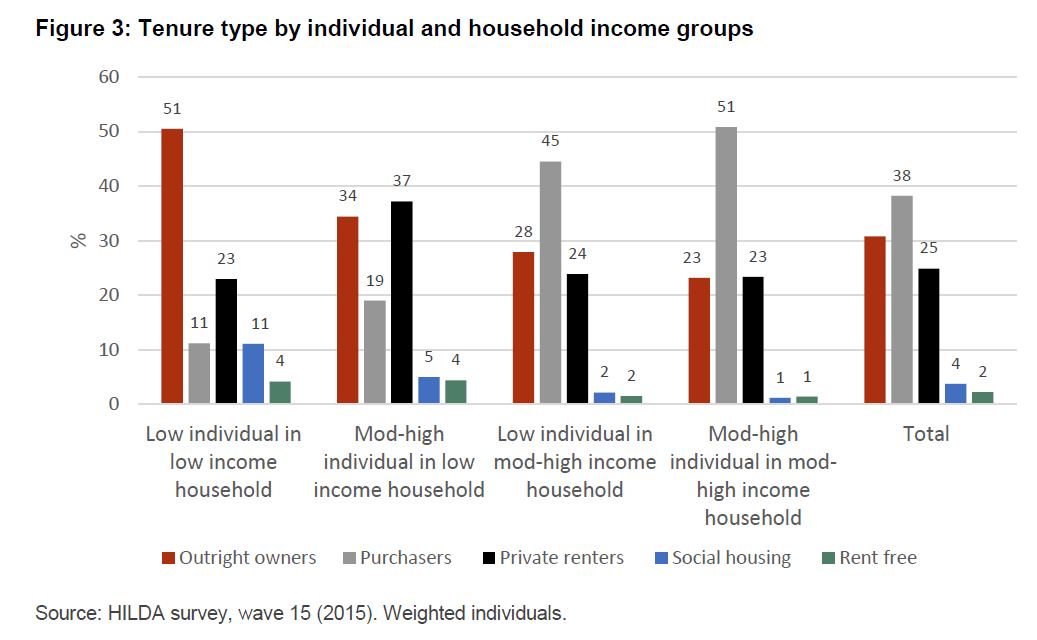

This included HILDA data from 2015, which whilst dated now, highlights the issues in the low-income renter sector.

They say that the Private Rental Sector:

… has been expanding and transforming in a number of ways over the past decade as renters and investors/landlords adapt to rising house prices and rents, particularly in Sydney and Melbourne markets. At the low end of the sector, key developments have been the entry and expansion of the role of online platforms and community agency intermediaries in facilitating access to and tenancy management of private rental rooms and dwellings. The profile of renters is becoming more diverse as long-term renting continues to increase across all income groups, generating high competition for the limited dwellings that are affordable on a low income. The profile of investors/landlords and the lease lengths they choose to set for rooms and dwellings is also more varied.

They find that:

The accessibility and affordability of dwellings at the low end of the PRS undoubtedly remains the central issue for vulnerable groups of renters. In seeking to understand how low-income renters navigate changing PRS institutions, we first examine their individual and household income profile, drawing on existing HILDA and Journeys Home data. This background analysis reveals the importance of understanding the connection between individual and household income for low-income renters, beyond existing measures of affordability stress at the household level, which can conceal the difficulties faced by individuals as they navigate access to the PRS. Factors to be considered include the interim solutions individuals may seek when locked out of formal rental pathways (such as more informal or supported pathways into the PRS), and the consequences of persistently low individual and household incomes over time.

Applying an individual–household income typology within the HILDA data we find that:

more than half (55%) of low-income (Q1–Q2) individuals in a low-income (Q1–Q2) household who are renting privately remain in this household group over a five-year period

this group of private renters is most likely to make a transition into social housing and is less likely to move, but when they do move it is typically ‘forced’ (i.e. their property is no longer available to rent)

low-income renters are least able, in terms of personal savings, to afford the upfront and relocation costs of a move.

In examining formal, informal and supported rental arrangements of individuals who have experience of or are at risk of homelessness, drawing on the Journeys Home longitudinal survey, we find the following.

Individuals and households in the lowest 20 per cent of the income distribution (Q1) are least likely to rent in the formal PRS, with over 70 per cent reporting a lack of affordable housing as an obstacle to finding more secure housing. The main type of living arrangements for those with Q1 individual (40%) and Q1 household (31%) incomes was renting from friends and family.

Among Q1 individuals renting in the formal PRS, the main transition between consecutive waves of the HILDA data was to move into an informal arrangement where they rent privately from friends and family (24%).

Transitions in individual income groups showed that 70 per cent of Q1 individuals and 74 per cent of Q2 individuals remained in the same income group over the data collection period (2011–14).

They state:

The formal institutions within the PRS designed to overcome barriers to accessing and managing tenancies for low-income renters have not kept up with the pace of change occurring within informal rental living arrangements. Any reforms to existing formal institutions intended to deliver better outcomes for private renters on a low-income must grapple with an increasingly complex and fragmented PRS. There is a clear need for centralised forms of assistance delivered via the statutory income system of support, but also a need for more devolved initiatives that can target informal and supported pathways through state and local government tenancy regulation and policy intervention. Within this framing, policy reform should take into account the following:

Centralised reforms of rental housing assistance and regulation must seek to redress the growing imbalance in horizontal equity (treating those with similar incomes and wealth the same) and vertical equity (reducing the divide between those at the top and bottom of the income and wealth distribution). This includes reviewing the adequacy of wages, statutory incomes and rental assistance in view of rising costs of living.

There is clear evidence that the informal pathway into the PRS is expanding through the reach of online platforms to exploit and disrupt formal paths to access and management. Regulation of informal rental practices, particularly in the context of online intermediaries and the growth of room rentals, must ensure that supply and access to urgent housing is not impeded, whilst also ensuring that tenants have adequate recourse to live in safe and secure rental housing.

As the community sector expands its focus, there is growing capacity to establish more formal and enduring institutions at the low end of the PRS via a supported pathway delivered through an expanded community housing and welfare sector, in a similar manner to the social rental agencies developed in Belgium (see, for example, Parkinson and Parsell 2018). However, existing policy assumptions surrounding time-limited supported housing in the PRS, including financial subsidies through head-leasing initiatives, are highly problematic for those whose individual and household incomes remain low over time. A

AHURI Final Report No. 302 87

viable supported pathway into the PRS will require appropriate incentives for landlords to set their rents to be comparable with social housing rentals.

The emergence of different types of landlords (offering properties and rooms on a short- through to long-term basis), combined with the expanded reach of online platforms, provides opportunities for policy makers to assume a more direct role in better matching landlords with tenants. This includes targeting of landlord financial and taxation incentives to encourage supply of a mix of leasing options, dwelling types and locations at the low end of the market.

The findings and directions outlined in this report, together with those from an international and national institutional review of sector change and innovation, will inform the broader Inquiry report on The future of the private rental sector to provide a more detailed blueprint for institutional reform.