APRA’s revised mortgage guidance released yesterday, on the surface may look benign but if you look at the detail there are a number of changes which together do change the game in terms of risk analysis during underwriting, and through the life of the mortgage. We think this will slow credit growth through 2017 and beyond.

We suggest this is imposing significant micro-management on the portfolio, which will force some lenders to change their current practices.

We suggest this is imposing significant micro-management on the portfolio, which will force some lenders to change their current practices.

Investment Property Underwriting Tightened.

APRA says a minimum haircut of 20% on expected rental income, and larger discounts on properties where there is a higher risk of non-occupancy should be applied. They also need to taking into account a borrower’s investment property-related fees and expenses. Also, APRA highlights that an ADI should ideally “place no reliance on a borrower’s potential ability to access future tax benefits from operating a rental property at a loss”, but if an ADI chooses to do so, it “would be prudent to assess it at the current interest rate rather than one with a buffer applied”.

Serviceability Tests Strengthened

APRA reaffirmed the interest rate buffer of at least 2% and minimum lending floor rate of at least 7% for mortgages. But now APRA says ADIs should apply these buffers a borrower’s new and existing debt commitments. To do this, banks will need to have more detailed knowledge of a borrower’s existing debt commitments and history of delinquency.

Expenses Assessment Tightened

APRA wants ADIs to use the greater of a borrower’s declared living expenses or an appropriately income scaled version of the Household Expenditure Measure (HEM) or Henderson Poverty Index (HPI). They cannot rely fully on HEM or HPI to assess living expenses. They suggest expenses should be more correlated to income.

Income Assessment Tightened

APRA says banks should apply discounts of at least 20% (instead of being calculated at the ADIs’ discretion) to be applied to most types of non-salary income (rental income on investment properties, bonuses, child benefits etc.). A larger discount should sometimes be used where income is more variable over time – “an ADI may choose to use the lowest documented value of such income over the last several years, or apply a 20 per cent discount to the average amount received over a similar period”.

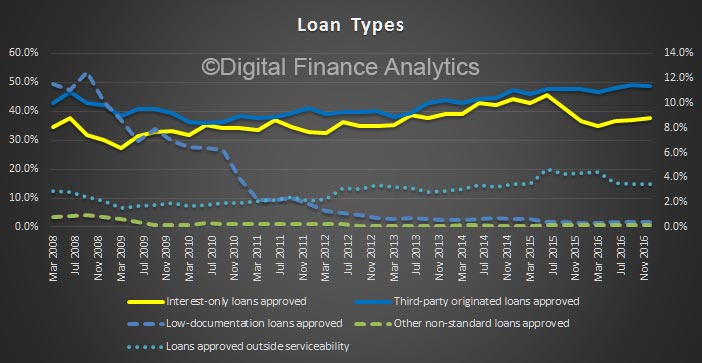

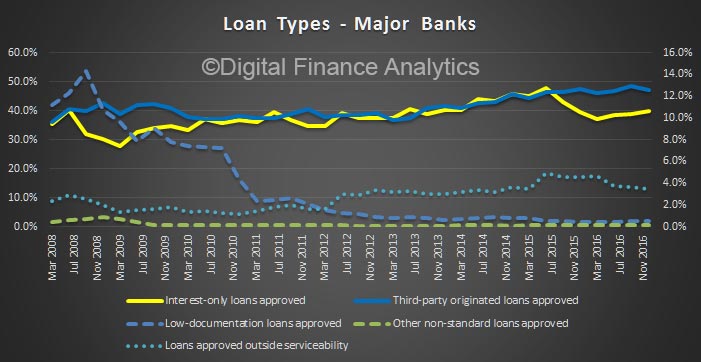

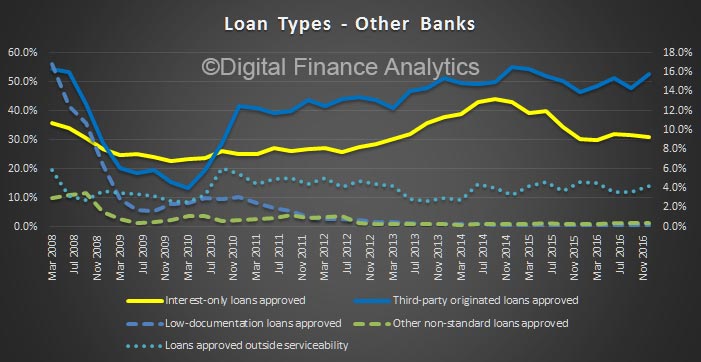

Interest Only Loans More Restricted

APRA expects interest-only periods offered on residential mortgage loans to be of limited duration, particularly for owner-occupiers. Interest-only loans may carry higher credit risk in some cases, and may not be appropriate for all borrowers. This should be reflected in the ADI’s risk management framework, including its risk appetite statement, and also in the ADI’s responsible lending compliance program. APRA expects that an ADI would only approve interest-only loans for owner-occupiers where there is a sound and documented economic basis for such an arrangement and not based on inability to service a loan on a principal and interest basis.

SMSF Property Loans Require More Examination

The nature of loans to SMSFs gives rise to unique operational, legal and reputational risks that differ from those of a traditional mortgage loan. Legal recourse in the event of default may differ from a standard mortgage, even with guarantees in place from other parties. Customer objectives and suitability may be more difficult to determine. In performing a serviceability assessment, ADIs would need to consider what regular income, subject to haircuts as discussed above, is available to service the loan and what expenses should be reflected in addition to the loan servicing. APRA expects that a prudent ADI would identify the additional risks relevant to this type of lending and implement loan application assessment processes and criteria that adequately reflect these risks.

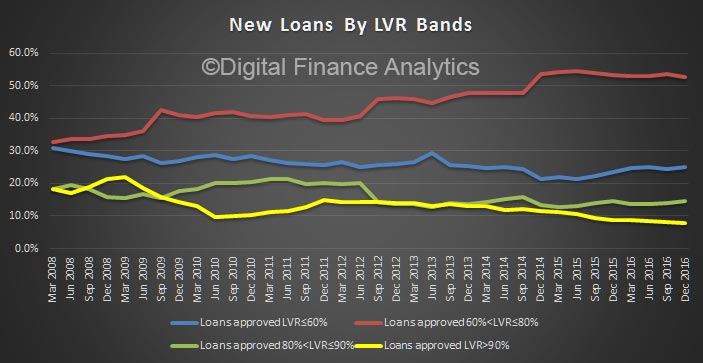

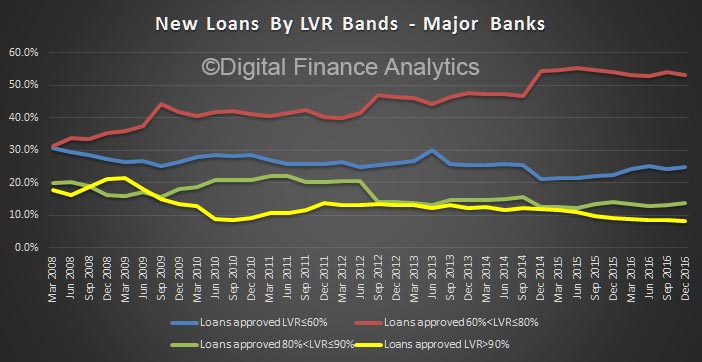

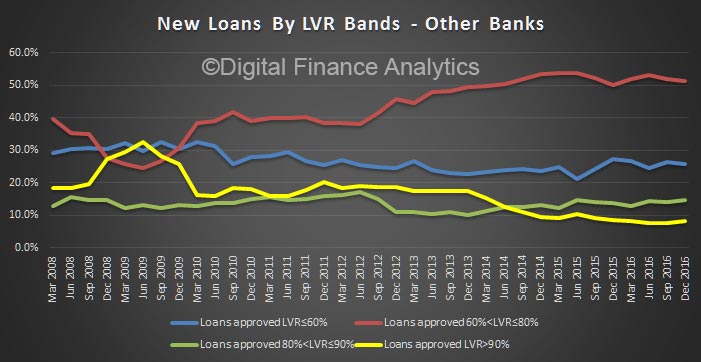

LVR Is Not A Good Risk Indicator

Although mortgage lending risk cannot be fully mitigated through conservative LVRs, prudent LVR limits help to minimise the risk that the property serving as collateral will be insufficient to cover any repayment shortfall. Consequently, prudent LVR limits serve as an important element of portfolio risk management. APRA emphasises, however, that loan origination policies would not be expected to be solely reliant on LVR as a risk-mitigating mechanism.

Genuine Savings To Be Tested

ADIs typically require a borrower to provide an initial deposit primarily drawn from the borrower’s own funds. Imposing a minimum ‘genuine savings’ requirement as part of this initial deposit is considered an important means of reducing default risk. A prudent ADI would have limited appetite for taking into account non-genuine savings, such as gifts from a family member. In such cases, it would be prudent for an ADI to take all reasonable steps to determine whether non-genuine savings are to be repaid by the borrower and, if so, to incorporate these repayments in the serviceability assessment.

Granular and Ongoing Portfolio Management Required

Where residential mortgage lending forms a material proportion of an ADI’s lending portfolio and therefore represents a risk that may have a material impact on the ADI, the accepted level of credit risk would be expected to specifically address the risk in the residential mortgage portfolio. Further, in order to assist senior management and lending staff to operate within the accepted level of credit risk, quantifiable risk limits would be set for various aspects of the residential mortgage portfolio.

A robust management information system would be able to provide good quality information on residential mortgage lending risks. This would typically include:

a) the composition and quality of the residential mortgage lending portfolio, e.g. by type of customer (first home buyer, owner-occupied, investment etc), product line, distribution channel, loan vintage, geographic concentration, LVR bands at origination, loans on the watch list and impaired;

b) portfolio performance reporting, including trend analysis, peer comparisons where possible, other risk-adjusted profitability and economic capital measures and results from stress tests;

c) compliance against risk limits and trigger levels at which action is required;

d) reports on broker relationships and performance;

e) exception reporting including overrides, key drivers for overrides and delinquency performance for loans approved by override;

f) reports on loan breaches and other issues arising from annual reviews;

g) prepayment rates and mortgage prepayment buffers;

h) serviceability buffers including trends, performance, recent changes to buffers and adjustments and rationale for changes;

i) missed payments, hardship concessions and restructurings, cure rates and 30-, 60- and 90-days arrears levels across, for example, different segments of the portfolio, loan vintage, geographic region, borrower type, distribution channel and product type;

j) changes to valuation methodologies, types and location of collateral held and analysis relating to any current or expected changes in collateral values;

k) findings from valuer reviews or other hindsight reviews undertaken by the ADI;

l) reporting against key metrics to measure collections performance;

m) tracking of loans insured by LMI providers, including claims made and adverse findings by such providers;

n) provisioning trends and write-offs;

o) internal and external audit findings and tracking of unresolved issues and closure;

p) issues of contention with third-parties including service providers, valuation firms, etc; and

q) risk drivers and other components that form part of scorecard or models used for loan origination as well as risk indicators for new lending.

When setting risk limits for the residential mortgage portfolio, a prudent ADI would consider the following areas:

a) loans with differing risk profiles (e.g. interest-only loans, owner-occupied, investment property, reverse mortgages, home equity lines-of-credit (HELOCs), foreign currency loans and loans with non-standard/alternative documentation);

b) loans originated through various channels (e.g. mobile lenders, brokers, branches and online);

c) geographic concentrations;

d) serviceability criteria (e.g. limits on loan size relative to income, (stressed) mortgage repayments to income, net income surplus and other debt servicing measures);

e) loan-to-valuation ratios (LVRs), including limits on high LVR loans for new originations and for the overall portfolio;

f) use of lenders mortgage insurance (LMI) and associated concentration risks;

g) special circumstance loans, such as reliance on guarantors, loans to retired or soon-to–be-retired persons, loans to non-residents, loans with non-typical features such as trusts or self-managed superannuation funds (SMSFs);

h) frequency and types of overrides to lending policies, guidelines and loan origination standards;

i) maximum expected or tolerable portfolio default, arrears and write-off rates; and

j) non-lending losses such as operational breakdowns or adverse reputational events related to consumer lending practices.

Good practice would be for the risk management framework to clearly specify whether particular risk limits are ‘hard’ limits, where any breach is escalated for action as soon as practicable, or ‘soft’ limits, where occasional or temporary breaches are tolerated.

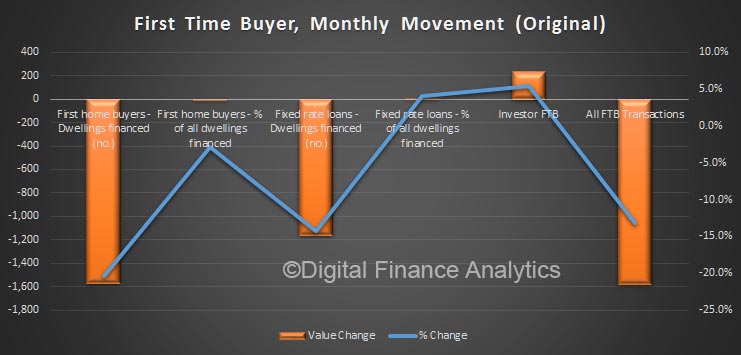

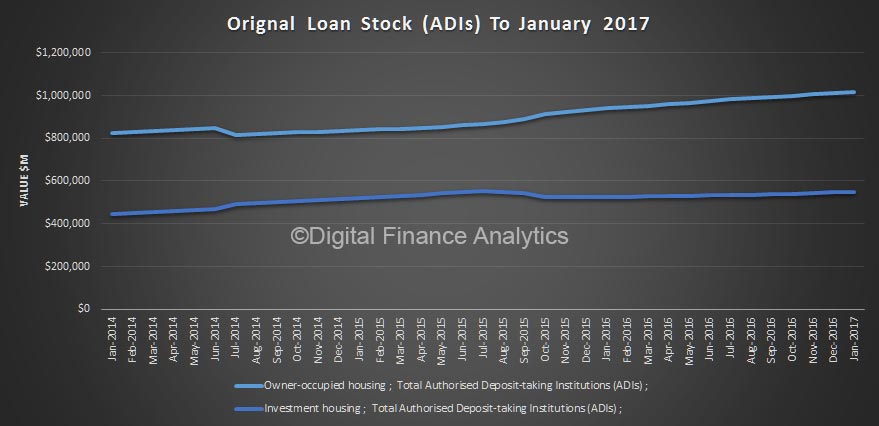

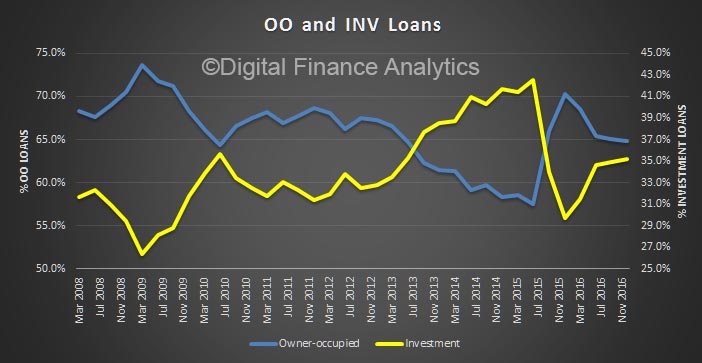

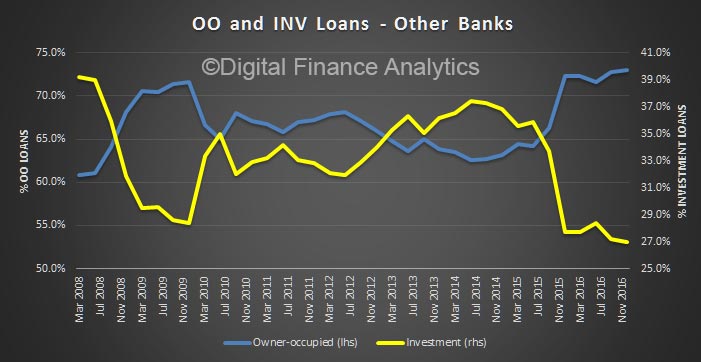

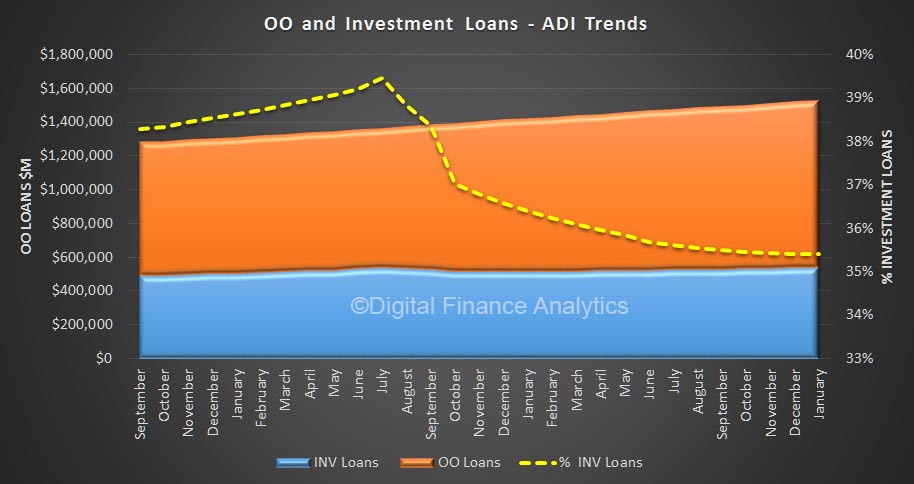

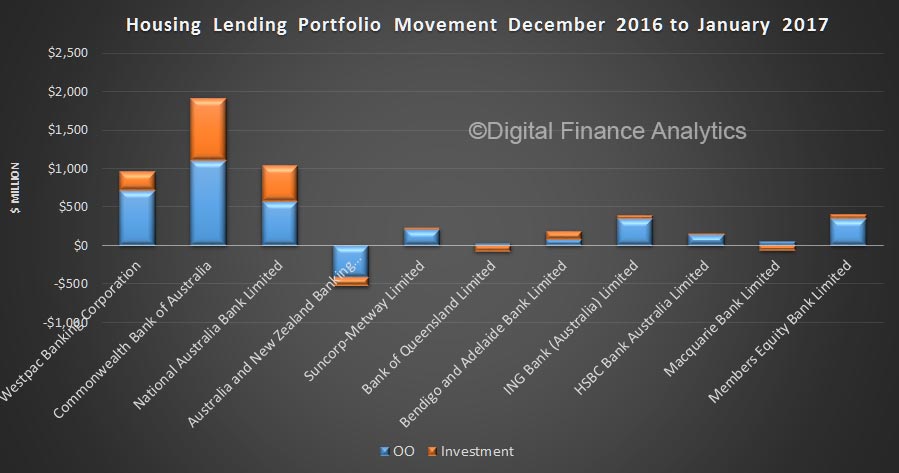

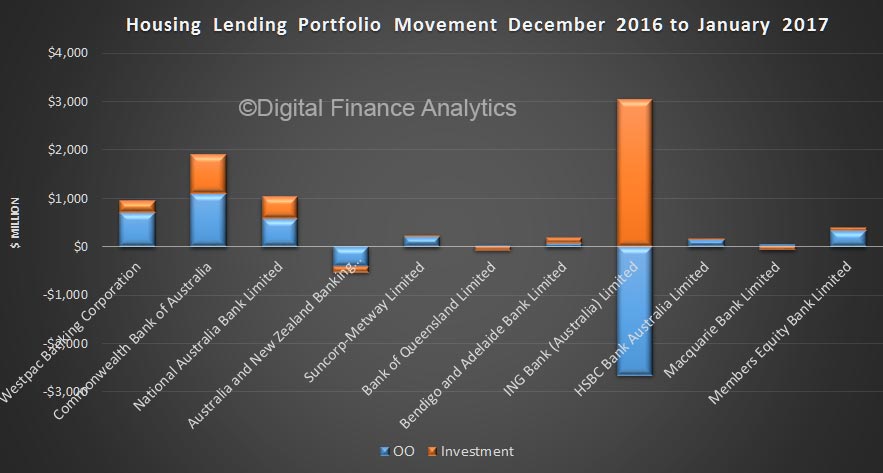

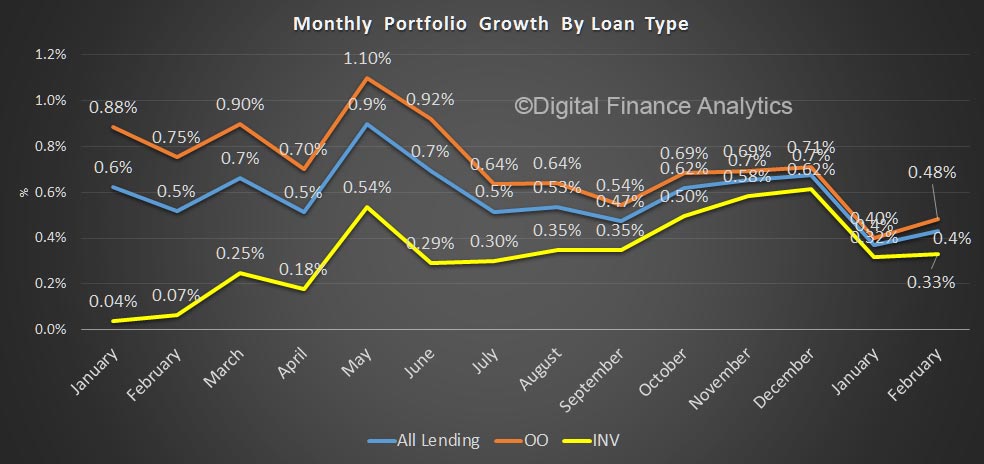

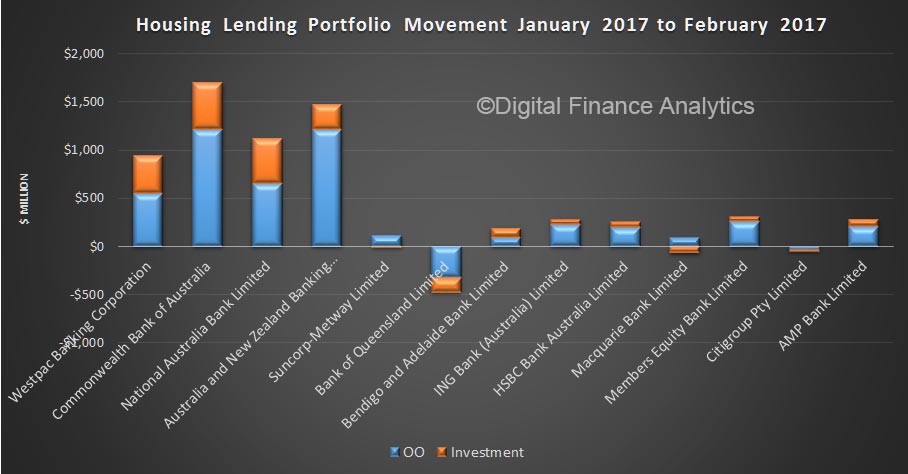

This means the banks total book is now worth $1.54 trillion. Within that owner occupied loans rose 0.48% to $993 billion, whilst investment loans rose 0.33% to $543 billion, or 35.4%. This tells us that more investors are going to the non-banks – which are not regulated by APRA, but by ASIC as commercial companies – and they do not have the same capital requirements as the banks – this is a major regulatory blind-spot.

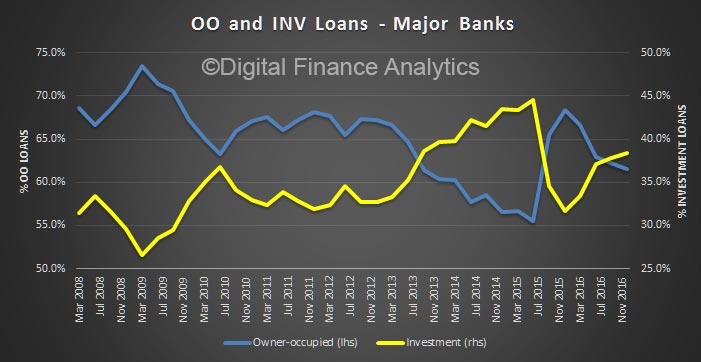

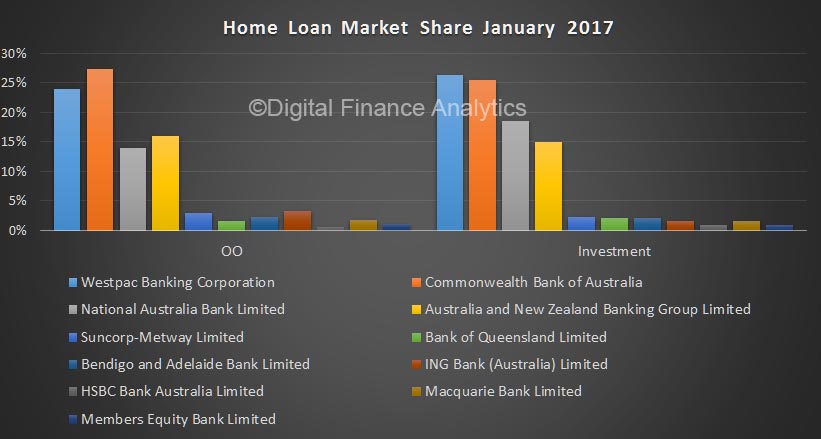

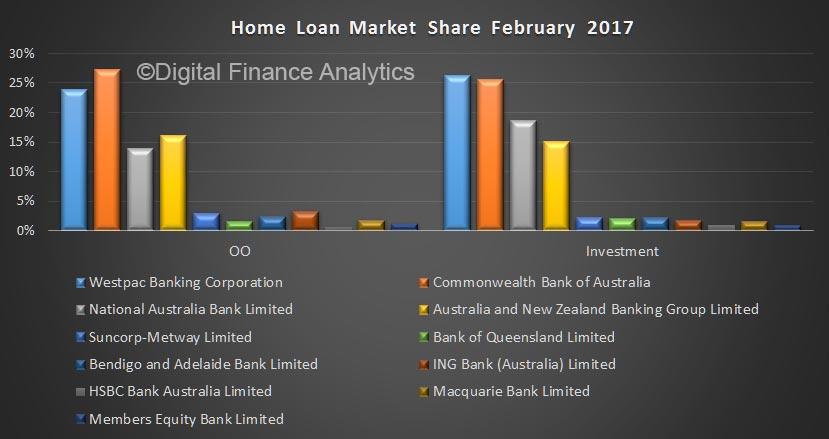

This means the banks total book is now worth $1.54 trillion. Within that owner occupied loans rose 0.48% to $993 billion, whilst investment loans rose 0.33% to $543 billion, or 35.4%. This tells us that more investors are going to the non-banks – which are not regulated by APRA, but by ASIC as commercial companies – and they do not have the same capital requirements as the banks – this is a major regulatory blind-spot. The overall market share of the majors show CBA with the largest share of the OO market, and Westpac still in pole position (just) on investment loans. ANZ has a larger share than NAB of owner occupied loans, whilst in the investment loan sector, the position is reversed.

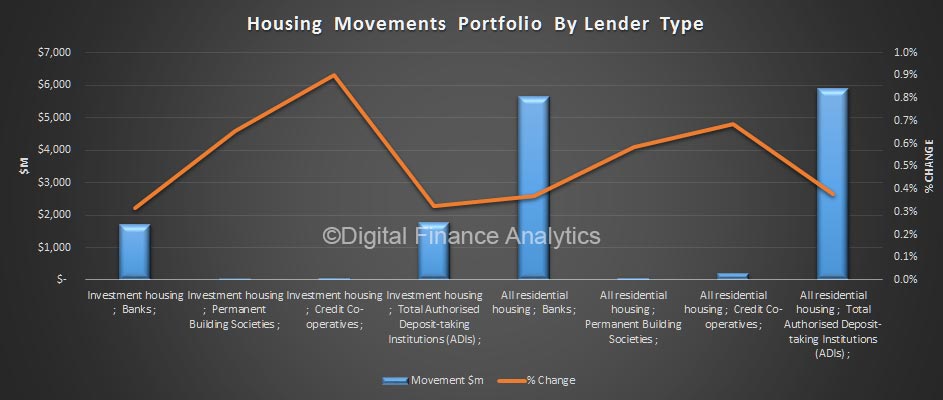

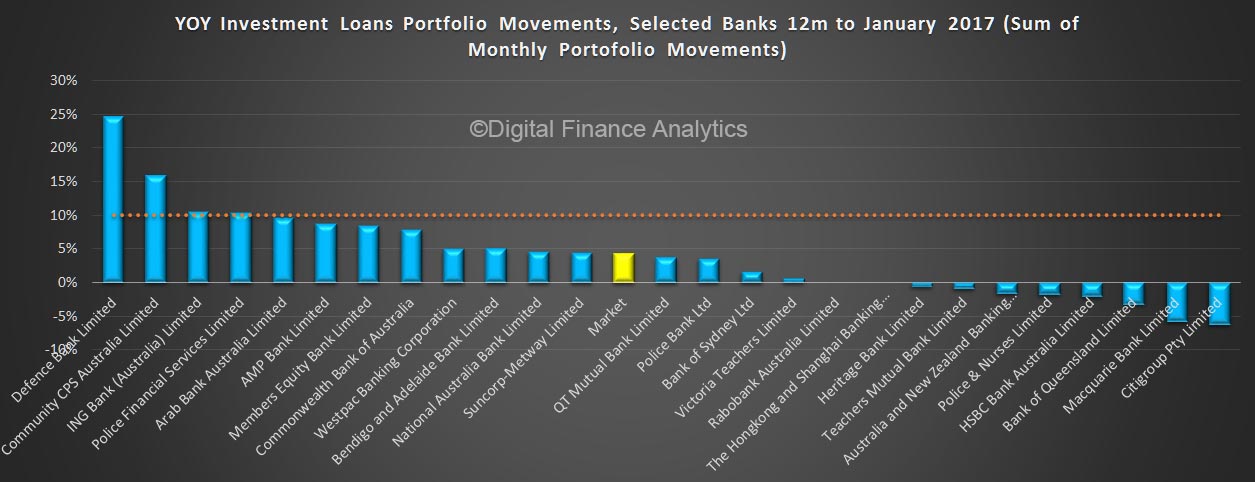

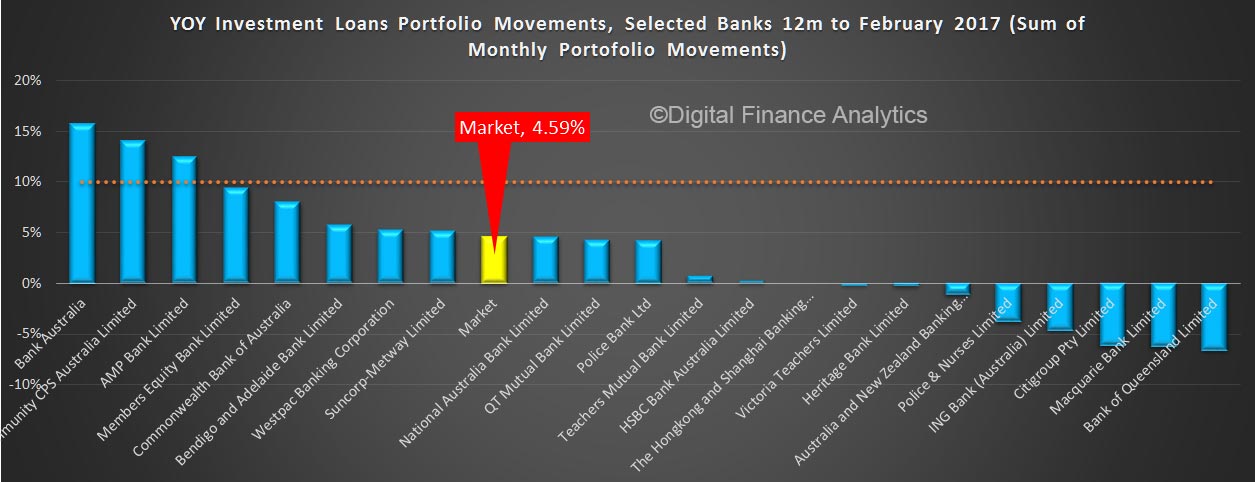

The overall market share of the majors show CBA with the largest share of the OO market, and Westpac still in pole position (just) on investment loans. ANZ has a larger share than NAB of owner occupied loans, whilst in the investment loan sector, the position is reversed. The APRA speed limit of 10% is higher than the annualised growth rate (which we calculate by summing the monthly movements from APRA), and we see that all the major players are “comfortably below” the 10%.

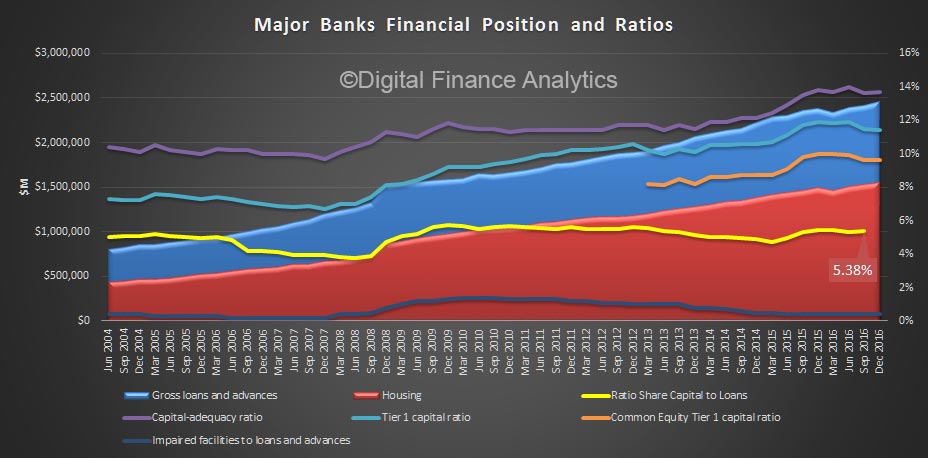

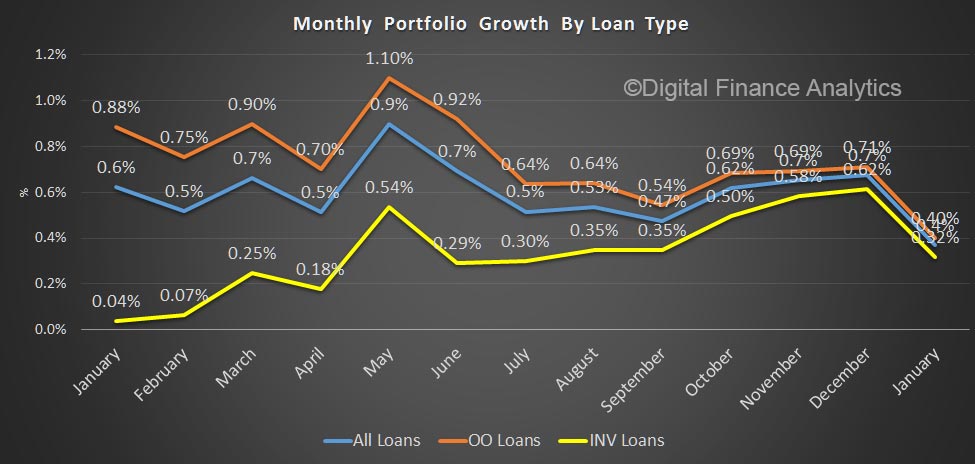

The APRA speed limit of 10% is higher than the annualised growth rate (which we calculate by summing the monthly movements from APRA), and we see that all the major players are “comfortably below” the 10%. All in all then, we think the banks will still be writing more investment loans, and as a result, we expect the investor lending party will continue until such time as the tax breaks are reduced (which just might happen in the budget?). Therefore home prices are set to continue to push higher, as household debt rises higher. In addition, the out of cycle rises on investor loans will bolster bank profits, whilst the additional interest costs will be born by tax payers, as investors who are negatively geared offset the higher borrowing costs. There is nothing here that will fundamentally change the trajectory of the market.

All in all then, we think the banks will still be writing more investment loans, and as a result, we expect the investor lending party will continue until such time as the tax breaks are reduced (which just might happen in the budget?). Therefore home prices are set to continue to push higher, as household debt rises higher. In addition, the out of cycle rises on investor loans will bolster bank profits, whilst the additional interest costs will be born by tax payers, as investors who are negatively geared offset the higher borrowing costs. There is nothing here that will fundamentally change the trajectory of the market.