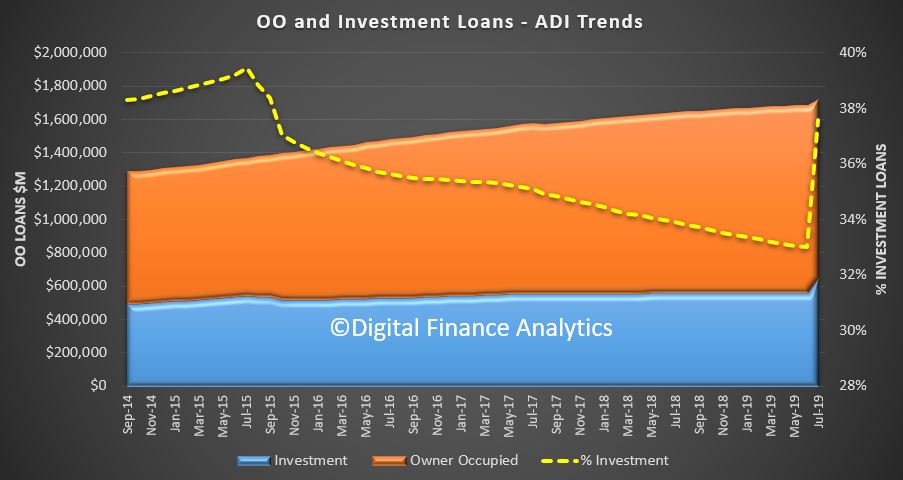

APRA released their monthly statistics to end July 2019. They are rubbish, in terms of trend tracking because thanks to a revised method of data capturing the value of investment lending rose considerably, offset by a fall in owner occupied loans.

The RBA said that there were reclassifications of loans between owner occupied and investment, plus off shore and onshore borrowers.

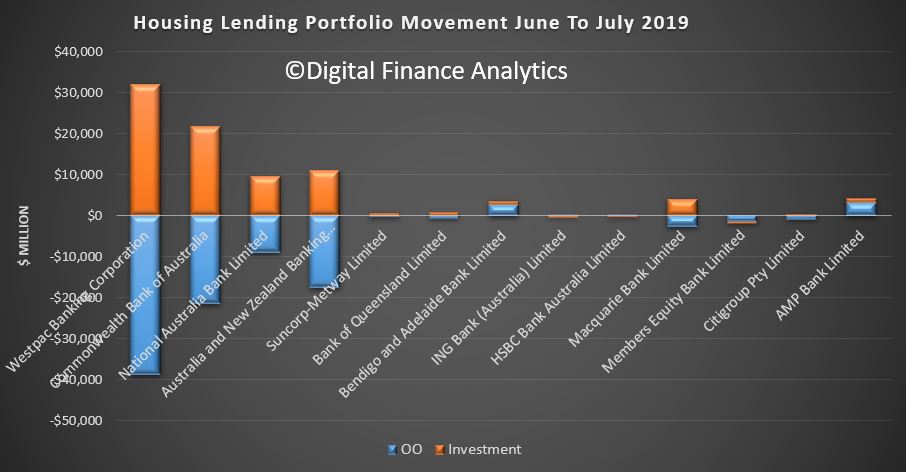

The changes from last month are therefore considerable. Westpac made the largest switch with $40 billion dropping from the owner occupied side of the house.

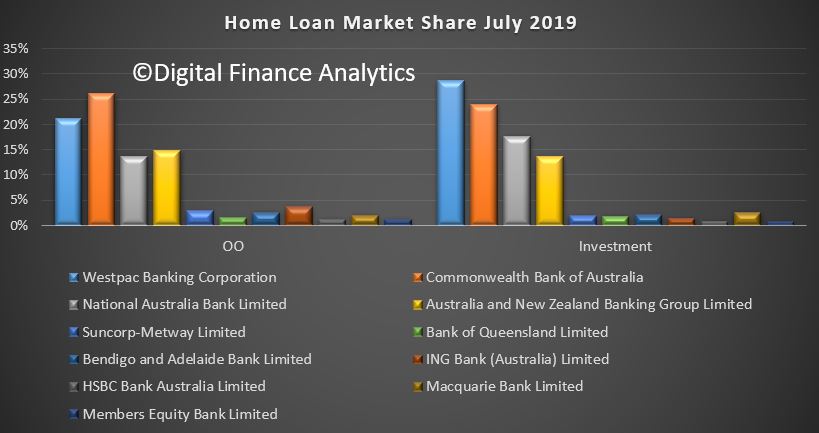

The overall portfolio mix by lender changed less.

But the proportion of investment loans jumped to 37.6%, compared with 33% the previous month. This means that banks ARE EVEN MORE EXPOSED to investment lending than had been previously reported!

Given the size of the changes, it is impossible to tell what is happening within individual lenders (which is convenient?). So we will have to start from this point as a series break.

For the record, the value of owner occupied loans fell 5% from $1.13 trillion to $1.10 trillion, while investment loans rose by 16% from $557.3 billion to $647.4 billion.

Total lending rose from $1.68 trillion to $1.72 trillion, up more than 2%. But this is meaningless.

Frankly this is a joke, and I feel it is designed to hide, not inform. The investment debt bomb just got bigger!

Interesting speech from Wayne Byers “Reflections on a changing landscape“. He discussed the ” extraordinary intervention” to save our banks a decade ago (in a footnote), significant in my view, for what it said, and for what it missed out. There is no mention that both NAB and Westpac required bailing out by the FED’s TAF after the GFC. An important little fact?

APRA’s activities have expanded significantly over the past five years. This has not been a smooth transition: the regulatory pendulum has swung between periods of significant regulatory change, and times when there have been demands to pare back. But overall there is no doubt that expectations of APRA have grown, and they have pushed us into new fields of endeavour. There is no sign that tide is going to turn soon.

I’m not sure what the issues de jour will be in five years’ time but there’s a very good chance they will not be the issues we think are most important today. The past five years has shown that what might seem unusual or out of scope today, can quickly become a core task tomorrow. Some of the topics that I have talked about tonight were not seen, five years ago, to be at the heart of APRA’s role.

In contrast, later this week we will publish our 4 year Corporate Plan and a number of them will be called out as our core outcomes, ranking alongside maintaining financial safety and resilience.

If there is one lesson from the past five years, it is that – be it regulators or risk managers – being ready and able to respond to the demands of a rapidly changing landscape is probably the most important attribute we all need to possess.

But the footnote was the most interesting in my view. For what it said, and for what it missed out.

It is sometimes said the Australian banking system ‘sailed through’ the financial crisis. While the system did prove relatively resilient, there was extraordinary intervention necessary to keep the system stable and the wheels of the economy turning.

That included (i) an unprecedented fiscal response – one of the largest stimulus packages in the world;

(ii) an unprecedented monetary response – the official cash rate was cut by 425 basis points in a little over six months;

(iii) the RBA substantially expanded its market operations and balance sheet;

(iv) ASIC imposed an 8-month ban on the short selling of financial stocks; and

(v) the Federal Government initiated a guarantee of retail deposits of up to $1 million, and a facility for authorised deposit-taking institutions (ADIs) to purchase guarantees for larger deposits and wholesale funding out to 5 years (indeed, at one point more than one-third of the banking system’s entire liabilities were subject to a Commonwealth Government guarantee).

As I have said previously, if all of the above was needed to keep the system stable and operational, then it is difficult to argue that the system sailed through or that some further strengthening of regulation was not justified.

He failed to mention the massive bail-out of our banking system from the FED and the fact that it was China’s response which supported our economy. The evidence suggests we were much closer to the abyss than was acknowledged at the time. Westpac and NAB both required support from the FED, as revealed in papers from the FED.

The US Dodd-Frank Act requires the US Federal Reserve to reveal which institutions it loaned money to under the various bail out programmes.

“Under the program, the Federal Reserve auctioned 28-day loans, and, beginning in August 2008, 84-day loans, to depository institutions in generally sound financial condition… Of those institutions, primary credit, and thus also the TAF, is available only to institutions that are financially sound.

Now of course the question is what does “financially sound” institutions mean. Well, look at the entire list – its long, but some of the names will be familiar. The FED data shows more than 4,200 separate transactions across more than 400 institutions globally between 2008 and 2010.

UK based Lloyds TSB plc received USD$10.5 billion – and was later partially nationalised by the UK government.

And another UK Bank, the Royal Bank of Scotland (RBS) got US$53.5 billion plus and additionally US$1.5 billion for its exposures via ABN Amro after RBS bought it. That was nationalised too.

In Ireland, Allied Irish Bank needed US$34.7 billion of loans from the Fed between February 2009 and February 2010 . This is the bank bailed out via the Irish taxpayer.

And Deutsche Bank needed a massive US$76.8 billion in loans in total (and that bank continues to struggle today).

The list goes on. Bayerische Landesbank required a US$13.4 billion bailout from the state of Bavaria, but also borrowed US$108.19 billion between December 2007 and October 2009.

Where these banks sound?

And our own “financially sound” institutions National Australia Bank and Westpac needed help from the Fed. NAB needed around $7 billion in total (allowing for the exchange rate).

In fact NAB raised $3 billion from shareholders in 2008 to add capital to its business in parallel.

And in January 2008 Westpac said everything was fine with its US exposures, just one month after they got their first bail-out from the FED, worth US$90 million.

In fact, there was a long queue then, as the Fed spreadsheet shows that alongside Westpac, was Citibank, Lloyds TSB Bank, Bayerische Landesbank and Societe Generale, all of whom where bailed out by Governments in their respective countries.

Now, the RBA wrote at the time:

“The Australian financial system has coped better with the recent turmoil than many other financial systems. The banking system is soundly capitalised, it has only limited exposure to sub-prime related assets, and it continues to record strong profitability and has low levels or problem loans. The large Australian banks all have high credit ratings and they have been able to continue to tap both domestic and offshore capital markets on a regular basis.”

So the question is did APRA and the RBA know what was going on?

And my question more generally is how prepared are we for a similar crisis now – given the changed economic and geopolitical forces in play?

As we recently highlighted APRA only looks at loan data not household mortgage data in their analysis. They have now confirmed this again in a piece in their newly released APRA insight 01 2019.

As I have argued before, this myopic view of mortgage land helps to explains the excesses we have seen in the sector, and the lack of effective supervision.

The

Quarterly Authorised Deposit-taking Institution Property Exposures

(QPEX) statistical publication provides bank, credit union and building

society aggregate statistics on commercial property exposures,

residential property exposures and new residential loan approvals. The

QPEX publication is published each quarter on APRA’s website.

In the most recent QPEX publication – March 2019

(issued in June 2019), APRA’s data (as seen in Chart 1) highlighted

negative growth in housing lending over 2018. Between the year ending 31

March 2019 and 31 March 2018, there was a decrease of:

7.2 per cent in owner-occupied new housing loan approvals, and

14.9 per cent in new housing investment loans.

While there has been a decrease in housing loan approvals, the average loan size has continued to grow (as seen in Chart 2).

Since the last QPEX (December 2018) was published, some commentators have misinterpreted APRA’s data in their analysis of the average balance of housing loans. They have assumed that an increase in the number of housing loans (as seen in Chart 2) meant an increase in the number of borrowers with a housing loan. This misinterpretation has resulted in a suggestion that the average balance of housing loans represents the level of indebtedness of Australian households. This conclusion cannot be drawn from the data.

The QPEX publication reports data from the ADI’s perspective (e.g.

the value of loans and number of loan accounts on the ADI’s books)

rather than the borrower’s perspective. The data is a simple average

calculated as the total balance of all housing loans divided by the

total number of housing loans extended by ADIs. In practice, a customer

may have multiple housing loans, which means that the average balance of

housing loans cannot be used to determine the average housing debt of

each borrower. When APRA supervises an ADI, we do not consider the

average loan size to be a reliable indicator of risk; rather the data is

just one of many inputs to identify potential changes to the overall

structure and size of loans.

APRA requires ADIs’ to maintain high lending standards to ensure they

are effectively managing risk when issuing new housing loans to

borrowers. When a borrower applies for a housing loan, APRA requires the

ADI to assess the borrower’s ability to repay the loan, taking into

account the borrower’s other debt commitments and everyday expenses. We

set out our expectations for ADIs on lending standards in Prudential Practice Guide APG 223 Residential Mortgage Lending.

The Australian Prudential Regulation Authority (APRA) has released a strengthened prudential standard aimed at mitigating contagion risk within banking groups. The new rules will come in from 1 January 2021. Until then the 100 or so such operations within a small number of ADIs will remain obscured, with potential higher risks exposure in a down turn.

Such complex group structures could potentially make it difficult for APRA to resolve an ADI quickly and protect depositors’ savings in the unlikely event of a bank failure.

The updated Prudential Standard APS 222 Associations with Related Entities (APS 222) will further reduce the risk of problems in one part of a corporate group having a detrimental impact on an authorised deposit-taking institution (ADI).

Deputy Chair John Lonsdale said APRA began consulting last July on proposed changes to APS 222 to incorporate some of the lessons learned from the global financial crisis.

“Concessions in the existing framework led to some ADIs establishing operations in foreign jurisdictions, which are managed and funded within the domestic bank.

“APRA has only limited visibility of these operations, which also fall outside the purview of foreign regulators. They complicate operating structures and there is no certainty their assets would be available to an ADI if it were to enter resolution. There are currently around 100 such operations within a small number of ADIs.

“Additionally, if an ADI were to fully utilise some of the limits within the existing framework, they would be exposed to excessive levels of contagion risk,” Mr Lonsdale said.

APRA received submissions from 10 stakeholders to its consultation; most supported updating the requirements, however some raised concerns about the complexity of implementing certain proposed changes.

Responding to the consultation, APRA confirmed that APS 222 will be updated to include:

a broader definition of related entities that includes board directors and substantial shareholders;

revised limits on the extent to which ADIs can be exposed to related entities;

minimum requirements for ADIs to assess contagion risk; and

removing the eligibility of ADIs’ overseas subsidiaries to be regulated under APRA’s Extended Licensed Entity framework.

Additionally, APRA will require ADIs to

regularly assess and report on their exposure to step-in risk – the likelihood

that they may need to “step in” to support an entity to which they are not

directly related.

Mr Lonsdale said the stronger APS 222 will enhance the prudential safety of

ADIs and reinforce financial system stability.

“As we saw during the global financial crisis, deficiencies in governance or

internal controls in one part of a corporate group can quickly spread and cause

financial or reputational damage to an ADI. Furthermore, complex group

structures could potentially make it difficult for APRA to resolve an ADI

quickly and protect depositors’ savings in the unlikely event of a bank

failure.

“By updating and strengthening the requirements of APS 222, APRA will ensure

ADIs are better able to monitor, manage and control contagion risk within their

organisations.

“While aspects of the revised standard will have a material impact on some

ADIs, we have adjusted our original proposals in some areas to make the

requirements less burdensome. We are open to considering appropriate transition

arrangements on a case-by-case basis where specific entities request it,” Mr

Lonsdale said.

The new APS 222 will come into effect from 1 January 2021.

The Australian Prudential Regulation Authority (APRA) has served infringement notices on Westpac Banking Corporation (Westpac) and two of its subsidiaries for failing to meet their legal obligations to report data to APRA.

Westpac, along with two of its registered financial corporations (RFCs), St George Finance Holdings Limited and Capital Finance Australia Limited, breached the requirements of the Financial Sector (Collection of Data) Act 2001 (FSCODA) by failing to report data by the required deadlines. Westpac was up to 20 days late in filing its reports for the month ending 31 March 2019 under the Economic and Financial Statistics program, which were due on 1 May. The two RFCs missed the same deadline by up to 37 days.

The RFCs were also up to 28 days late in submitting their reports for the month ending 30 April 2019. Additionally, all three Westpac entities were between 9 and 28 days late in filing their reports for the quarter ending 31 March 2019, which were due on 10 May 2019.

Failure to submit monthly or quarterly returns within the timeframes specified by APRA’s reporting standards is a strict liability offence.

APRA sent show cause notices to the Westpac entities on 22 July seeking their responses to APRA’s intention to serve them with infringement notices over the FSCODA breaches. After assessing Westpac’s responses, APRA has decided to proceed with the issuing of infringement notices.

Under the terms of the infringement notices, APRA requires the Westpac entities to pay a cumulative penalty of $1,501,500. This is the maximum financial penalty APRA can issue for infringement notices under FSCODA.

APRA Deputy Chair John Lonsdale said APRA’s reporting standards were legally binding in the same way as its prudential standards.

“Access to accurate and timely data is critical for APRA to monitor effectively the safety and stability of the banking, insurance and superannuation sectors.”

“By issuing these infringement notices, APRA wants to send a strong message to industry that compliance with our reporting standards is mandatory, and cannot be considered secondary to other business priorities,” Mr Lonsdale said.

The Westpac entities have until 6 September to pay the fines imposed by the infringement notices

We review the latest data from the RBA, APRA and ABS, plus higher mortgage delinquencies and the new bill to clamp down on cash transactions. A lot to talk about!

Full show on the war on cash: https://youtu.be/770M2s6ZD8Y

The Australian Prudential Regulation Authority (APRA) has required several banks to tighten the intra-group funding arrangements for their Australian operations.

Following a review of funding agreements across the authorised deposit-taking (ADI) industry, APRA has notified Macquarie Bank Limited, Rabobank Australia Limited and HSBC Bank Australia Limited that the reporting of their intra-group funding as stable has been in breach of the prudential liquidity standard.

APRA’s review found these banks were improperly reporting the stability of the funding they received from other entities within the group. These banks had provisions in their funding agreements that would potentially allow the group funding to be withdrawn in a stress scenario, undermining the stability of the Australian bank.

APRA is requiring these banks to strengthen intra-group agreements to ensure term funding cannot be withdrawn in a financial stress scenario. APRA is also requiring these banks to restate their past funding and liquidity ratios where these had been reported incorrectly, to provide transparency to investors and the broader community. Supervisors are considering a range of further options, including the imposition of higher funding and liquidity requirements on these ADIs.

APRA Deputy Chair John Lonsdale said: “Macquarie Bank, Rabobank Australia and HSBC Australia are financially sound, with strong liquidity and funding positions in the current stable environment. However, to ensure they would be able to withstand a scenario of financial stress, group funding agreements for Australian banks must be watertight, so they can be relied on when they would be most needed.”

To assist ADIs in complying with the prudential regulations, APRA has published a new frequently asked question (question 17), available on the following page: Liquidity – frequently asked questions

17. How should clauses which accelerate the repayment of funds owing

under funding programs or agreements (such as in the event of a

material adverse change) affect the treatment of the funding under APS

210 Attachment A paragraph 45 and APS 210 Attachment C paragraph 8?

APRA expects that a clause which allows a lender (or depositor) to accelerate repayment if the ADI is under financial stress but is still solvent and meeting its financial obligations under the program/agreement will be included in the LCR as funding that has its earliest possible contractual maturity date within the LCR horizon of 30 days. A run-off rate according to the requirements of APS 210 Attachment A paragraph 53 must then be applied. Similarly, APRA expects for NSFR purposes that the ADI will assume a residual maturity of less than six months, being the earliest date at which the funds under the funding agreement containing the relevant acceleration clause may be redeemed, and assign an ASF factor in accordance with the requirements of APS 210 Attachment C paragraph 15. The clauses that were of concern allow the lender (or depositor) to accelerate maturity, making funds owed under the funding agreement immediately due and payable (regardless of the maturity date) upon the borrowing ADI hitting a particular trigger or coming under (or potentially coming under) stress. Such clauses could allow the lender (or depositor) to withdraw funds when they are most needed by the borrowing ADI. Further, the funds might be withdrawn in priority to other creditors, including retail depositors. Examples of such clauses include, but are not limited to:

any material adverse change of the borrowing ADI which could affect the ability of the borrowing ADI to satisfy its obligations;

meeting a specified market-based or similar trigger (for example, hitting a credit default swap spread or equity price), regardless of the likelihood of meeting that trigger;

any representation or warranty made at issuance later becomes untrue or misleading either when made or repeated;

a downgrade in excess of 3 notches in the borrowing ADI’s long-term credit rating; and

any litigation or governmental investigation or proceeding pending or threatened against the borrowing ADI.

APRA appreciates the difficulty of precisely prescribing whether a clause will result in the funding being included within the 30-day horizon of the LCR. APRA expects ADIs to apply a robust process of challenge to such a determination. However, at a high level, a clause that potentially triggers early repayment where the ADI is still meeting its financial obligations under the facility, has not failed and continues to operate as an ADI should warrant careful scrutiny. If the ADI remains in doubt, it should send a query to APRA rather than risk a potential breach of the requirements in APS 210. In addition to consideration of the appropriate LCR and NSFR requirements in APS 210, if an ADI has a term or condition in a funding agreement with a related entity which is not typically contained in its external funding programs and agreements, the ADI should also consider the requirements of APS 222 paragraph 9.

This is in response to the fact that in the financial sector, APRA has observed an over-emphasis on short-term financial performance and a lack of accountability when failures occur, especially among senior management.

In a discussion paper released today for consultation, APRA has proposed creating a new prudential standard to better align remuneration frameworks with the long-term interests of entities and their stakeholders, including customers and shareholders.

Draft prudential standard CPS 511 Remuneration introduces heightened requirements on entities’ remuneration and accountability arrangements in response to evidence that existing arrangements have been a factor driving poor consumer outcomes.

The proposed reforms address recommendations 5.1 to 5.3 from the Final Report of the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry, which were endorsed by the Government in February.

The package of measures is materially more prescriptive than APRA’s existing remuneration requirements and will place Australia in line with better international remuneration practice.

Among the key reforms, APRA is proposing:

To elevate the importance of managing non-financial risks, financial performance measures must not comprise more than 50 per cent of performance criteria for variable remuneration outcomes;

Minimum deferral periods for variable remuneration of up to seven years will be introduced for senior executives in larger, more complex entities. Boards will also have scope to recover remuneration for up to four years after it has vested; and

Boards must approve and actively oversee remuneration policies for all employees, and regularly confirm they are being applied in practice to ensure individual and collective accountability.

APRA Deputy Chair John Lonsdale said it was clear that existing remuneration arrangements in many entities were not incentivising the right behaviours.

“Remuneration and accountability frameworks play an important role in driving employee behaviour. Where policies are poorly designed, or not followed in practice, companies may incentivise conduct that is contrary to the long-term interests of the company and its customers.

“In the financial sector, APRA has observed an over-emphasis on short-term financial performance and a lack of accountability when failures occur, especially among senior management.

“This has contributed to a series of damaging incidents that have undermined trust in both individual institutions and the financial industry more broadly. Crucially from APRA’s perspective, these incidents have damaged not only institutions’ reputations, but also their financial positions,” Mr Lonsdale said.

Mr Lonsdale said CPS 511 would complement the Banking Executive Accountability Regime to lift industry standards of accountability and reduce the likelihood of misconduct.

“Limiting the influence of financial performance metrics in determining variable remuneration will encourage executives to put greater focus on non-financial risks, such as culture and governance. As our recent response to the industry self-assessments made clear, this remains a weak spot in many financial institutions.

“Introducing the minimum holding periods for variable remuneration ensures executives have ‘skin in the game’ for longer, and allows boards to adjust remuneration downwards if problems emerge over an extended horizon.

“APRA will not be determining how much employees get paid. Rather, we want to empower boards to more effectively incentivise behaviour that supports the long-term interests of their entities. By reducing the risk of misconduct, we hope to see better outcomes for customers and higher returns for shareholders in the long-term.

“We recognise that some aspects of this proposal are far-reaching and will require major changes to industry practices. APRA will listen closely to feedback from impacted stakeholders to determine if our proposed approach is correctly calibrated to achieve its intended outcomes,” he said.

A three month consultation period will close on 22 October. APRA intends to release the final prudential standard before the end of 2019, with a view to it taking effect in 2021 following appropriate transitional arrangements. Copies of the discussion paper and the draft Prudential Standard CPS 511 Remuneration are available on the APRA website at: Consultation on remuneration requirements for all APRA-regulated entities.

I discuss the recent APRA Capability Review with Business Man and Ex ANZ Director John Dahlsen.

We discuss the need to change APRA, and also look at the structure of banking more generally.

The Australian Prudential Regulation Authority (APRA) is applying additional capital requirements to three major banks to reflect higher operational risk identified in their risk governance self-assessments.

APRA has written to ANZ, National Australia Bank (NAB) and Westpac advising of an increase in their minimum capital requirements of $500 million each. The capital add-ons will apply until the banks have completed their planned remediation to strengthen risk management, and closed gaps identified in their self-assessments.

The increase in capital requirements follows APRA’s decision in May last year to apply a $1 billion dollar capital add-on to Commonwealth Bank of Australia (CBA) in response to the findings of the APRA-initiated Prudential Inquiry into CBA.

Following the CBA Inquiry’s Final Report, APRA wrote to the boards of 36 of the country’s largest banks, insurers and superannuation licensees asking them to gauge whether the weaknesses uncovered by the Inquiry also existed in their own companies. Although the self-assessments raised no concerns about financial soundness, they confirmed that many of the issues identified in the Inquiry were not unique to CBA. This included the need to strengthen non-financial risk management, ensure accountabilities are clear, cascaded and enforced, address long-standing weaknesses and enhance risk culture.

APRA Chair Wayne Byres said: “Australia’s major banks are well-capitalised and financially sound, but improvements in the management of non-financial risks are needed. This will require a real focus on the root causes of the issues that have been identified, including complexity, unclear accountabilities, weak incentives and cultures that have been too accepting of long-standing gaps.

“The major banks play a vital role in the stability of the entire financial system, and APRA expects them to hold themselves to the highest standards of risk governance. Their self-assessments reveal that they have fallen short in a number of areas, and APRA is therefore raising their regulatory capital requirements until weaknesses have been fully remediated,” Mr Byres said.

APRA supervisors continue to provide tailored feedback to other banks, insurers and superannuation licensees that provided self-assessments to APRA. Where weaknesses have been identified, the level of supervisory scrutiny is being increased as remediation actions are implemented. Where material weaknesses exist, APRA is also considering the need for the application of an additional operational risk capital requirement.