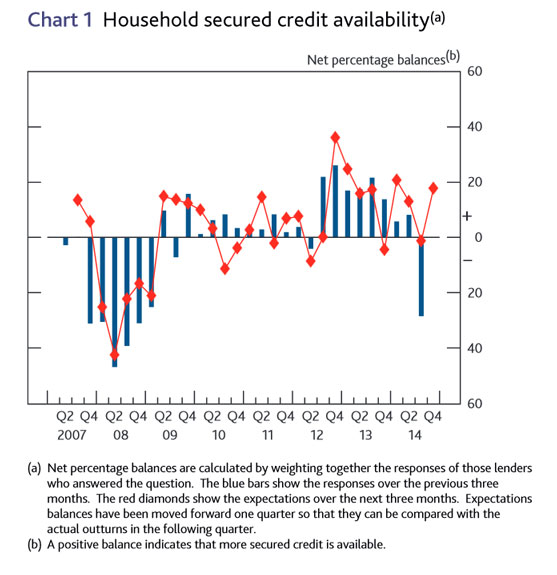

The Bank of England just released their latest Financial Stability report. Within the document there is a section on the implementation of macroprudential measures relating to mortgage lending. This makes an interesting contrast with the Australian Regulatory framework.

Mortgage affordability test – Implemented: When assessing affordability, mortgage lenders should apply an interest rate stress test that assesses whether borrowers could still afford their mortgages if, at any point over the first five years of the loan, Bank Rate were to be 3 percentage

points higher than the prevailing rate at origination.

Loan to income limit – Implemented: The PRA and the FCA should ensure that mortgage lenders do not extend more than 15% of their total number of new residential mortgages at loan to income ratios at or greater than 4.5. This Recommendation applies to all lenders which

extend residential mortgage lending in excess of £100 million per annum.

Powers of Direction over leverage ratio – Action under way: The FPC recommends that HM Treasury exercise its statutory power to enable the FPC to direct, if necessary to protect and enhance financial stability, the PRA to set leverage ratio requirements and buffers for PRA-regulated banks, building societies and investment firms, including:

- a minimum leverage ratio requirement to remove or reduce systemic risks attributable to unsustainable leverage in the financial system;

- a supplementary leverage ratio buffer that will apply to G-SIBs and other major domestic UK banks and building societies, including ring-fenced banks to remove or reduce systemic risks attributable to the distribution of risk within the financial sector;

- a countercyclical leverage ratio buffer to remove or reduce systemic risks attributable to credit booms — periods of unsustainable credit growth in the economy.

The Government intends to lay the final legislation before Parliament in early 2015, alongside publishing a consultation response document and impact assessment. As with the housing instruments, the FPC intends to issue a draft Policy Statement in early 2015 to inform the Parliamentary debate.

HM Treasury intends to consult separately on LTV/interest coverage ratio powers for the buy-to-let sector in 2015, with a view to building further evidence on how the UK buy-to-let housing market may pose risks to financial stability.