We look at the latest from the MPC and the Bank of England. At its meeting ending on 22 September 2021, the Committee judged that the existing stance of monetary policy remained appropriate. The MPC voted unanimously to maintain Bank Rate at 0.1%. The Committee voted unanimously for the Bank of England to maintain the stock of sterling non-financial investment-grade corporate bond purchases, financed by the issuance of central bank reserves, at £20 billion. The Committee voted by a majority of 7-2 for the Bank of England to continue with its existing programme of UK government bond purchases, financed by the issuance of central bank reserves, maintaining the target for the stock of these government bond purchases at £875 billion and so the total target stock of asset purchases at £895 billion.

Go to the Walk The World Universe at https://walktheworld.com.au/

We discuss the House of Lords Report on the Bank of England’s Quantitative Easing Programme. They ask the critical question – just how will it be unwound? Has the Bank of England created greater inequality through the programme – and just how independent is the Bank and its relationship with HM Treasury.

We discuss the House of Lords Report on the Bank of England’s Quantitative Easing Programme. They ask the critical question – just how will it be unwound? Has the Bank of England created greater inequality through the programme – and just how independent is the Bank and its relationship with HM Treasury.

The Bank of England and HM Treasury have today announced the joint creation of a Central Bank Digital Currency (CBDC) Taskforce to coordinate the exploration of a potential UK CBDC. A CBDC would be a new form of digital money issued by the Bank of England and for use by households and businesses. It would exist alongside cash and bank deposits, rather than replacing them.

Go to the Walk The World Universe at https://walktheworld.com.au/

This step is designed to help alleviate frictions observed in money markets in recent weeks, both globally and domestically, as a result of the economic shock caused by the outbreak says the Bank of England.

The CTRF is a flexible liquidity insurance tool that allows participants to borrow central bank reserves (cash) in exchange for other, less liquid assets (collateral).

The Bank’s liquidity insurance facilities support financial market functioning by providing market participants with predictable and reliable sources of liquidity. The Bank’s liquidity insurance facilities support financial stability by reducing the cost of disruption to critical financial services.

Holding additional CTRF operations over the next two weeks complements the Bank’s existing liquidity facilities. The CTRF will run alongside the Bank’s regular sterling market operations – the Indexed Long-Term Repo (CTRF) and Discount Window Facility (DWF). The Bank is also able to lend in all major currencies through its participation in the central bank swapline network.

The CTRF will lend reserves for a period of three months. This will also allow participants to use the CTRF as a way to bridge beyond the point at which drawings can be made from the Term Funding Scheme with additional incentives for SMEs (TFSME) – helping to support lending to the real economy as quickly as possible.

An accompanying Market Notice provides additional detail and the terms of this operation

The Bank of Canada, the Bank of England, the Bank of Japan, the European Central Bank, the Federal Reserve, and the Swiss National Bank are today announcing a coordinated action to further enhance the provision of liquidity via the standing U.S. dollar liquidity swap line arrangements.

To improve the swap lines’ effectiveness in providing U.S. dollar funding, these central banks have agreed to increase the frequency of 7-day maturity operations from weekly to daily. These daily operations will commence on Monday, March 23, 2020 and will continue at least through the end of April. The central banks also will continue to hold weekly 84-day maturity operations.

The swap lines amongst these central banks are available standing facilities and serve as an important liquidity backstop to ease strains in global funding markets, thereby helping to mitigate the effects of such strains on the supply of credit to households and businesses, both domestically and abroad.

The same information appeared on other Central Bank web site too.

The spread of Covid-19 and the measures

being taken to contain the virus will result in an economic shock that

could be sharp and large, but should be temporary. The role of the Bank

of England is to help to meet the needs of UK businesses and households

in dealing with the associated economic disruption.

On 11 March, the Bank of England’s three

policy committees announced a package of measures to support UK

businesses and households through this period. In his Budget on the

same day, the Chancellor of the Exchequer announced a number of fiscal

measures with the same aim. On 17 March, this combined package of

measures was complemented by the announcement by HM Treasury of the

Covid 19 Corporate Financing Facility (CCFF), for which the Bank will

act as HM Treasury’s agent. By purchasing commercial paper, the CCFF

will provide funding to non-financial businesses making a material

contribution to the UK economy to support them in paying salaries, rents

and suppliers while experiencing the likely disruption to cashflows

associated with Covid-19.

In light of actions to tackle the spread of the virus, and evidence relating to the global and domestic economy and financial markets, the Monetary Policy Committee (MPC) held an additional special meeting on 19 March. Over recent days, and in common with a number of other advanced economy bond markets, conditions in the UK gilt market have deteriorated as investors have sought shorter-dated instruments that are closer substitutes for highly liquid central bank reserves. As a consequence, UK and global financial conditions have tightened.

At its special meeting on 19 March, the MPC judged that a further package of measures was warranted to meet its statutory objectives. It therefore voted unanimously to increase the Bank of England’s holdings of UK government bonds and sterling non-financial investment-grade corporate bonds by £200 billion to a total of £645 billion, financed by the issuance of central bank reserves, and to reduce Bank Rate by 15 basis points to 0.1%. The Committee also voted unanimously that the Bank of England should enlarge the TFSME scheme, financed by the issuance of central bank reserves.

The majority of additional asset purchases

will comprise UK government bonds. The purchases announced today will

be completed as soon as is operationally possible, consistent with

improved market functioning. The Bank will issue further guidance to

the market in due course.

The next regularly scheduled MPC meeting

will end on 25 March, with the minutes published on 26 March. The

minutes of today’s special meeting will be released at the same time.

UK Treasury and the Bank are coordinating closely in order to ensure that our initiatives are complementary and that they will, collectively, have maximum impact, consistent with the Bank and HM Treasury’s independent responsibilities.

Although the magnitude of the economic

shock from Covid-19 is highly uncertain, activity is likely to weaken

materially in the United Kingdom over the coming months. Temporary, but

significant, disruptions to supply chains and weaker activity could

challenge cash flows and increase demand for working capital from

companies.

The CCFF will provide funding to

businesses by purchasing commercial paper of up to one-year maturity,

issued by firms making a material contribution to the UK economy. It

will help businesses across a range of sectors to pay wages and

suppliers, even while experiencing severe disruption to cashflows.

The facility will offer financing on terms

comparable to those prevailing in markets in the period before the

Covid-19 economic shock, and will be open to firms that can demonstrate

they were in sound financial health prior to the shock. The facility

will look through temporary impacts on firms’ balance sheets and cash

flows by basing eligibility on firms’ credit ratings prior to the

Covid-19 shock. Businesses do not need to have previously issued

commercial paper in order to participate.

The scheme will operate for at least 12

months and for as long as steps are needed to relieve cash flow

pressures on firms that make a material contribution to the UK economy.

The Bank will publish further details of the operation of the CCFF in a

Market Notice on Wednesday 18 March. The Bank will implement the

facility on behalf of the Treasury and will put it into place as soon as

possible.

By providing an alternative source of

finance for a wide range of companies, the scheme will help to preserve

the capacity of the banking system to lend to other companies, including

small and medium-sized enterprises, which rely on banks. Last week,

the Bank of England boosted this capacity by:

launching a new Term Funding Scheme

with additional incentives for lending to SMEs (TFSME). This will, over

the next 12 months, offer four-year funding to banks of at least 5% of

participants’ stock of real economy lending at interest rates at, or

very close to, Bank Rate. Additional funding will be available for

banks that increase lending, especially to small and medium-sized

enterprises (SMEs).

reducing the UK countercyclical

capital buffer rate to 0% of banks’ exposures to UK borrowers with

immediate effect. This extended banks’ capacity to lend to businesses by

up to £190bn.

Taken together the actions announced by HM

Treasury and the Bank of England will help UK businesses and households

to bridge a temporarily difficult period and thereby to mitigate any

longer-lasting effects of Covid-19 on jobs, growth and the UK economy.

HM Treasury and the Bank will take all

further necessary steps to support the UK economy and financial system,

consistent with its statutory responsibilities.

Overnight the Bank of England cuts the UK cash rate by 0.5% to 0.25%, cut the banks’ liquidity buffer to zero, and announced extra funding for banks to lend to businesses, all in response to the virus. The Prudential Regulation Authority (PRA) said that banks should not increase dividends or other distributions, such as bonuses, in response to these policy actions.

The Bank is coordinating its actions with those of HM Treasury in order to ensure that initiatives are complementary and that they will, collectively, have maximum impact. The Bank continues to co-ordinate closely with international counterparts. We will discuss the budget spend, also announced today in a separate post.

The bank said that although the magnitude of the economic shock from Covid-19 is highly uncertain, activity is likely to weaken materially in the United Kingdom over the coming months. Temporary, but significant, disruptions to supply chains and weaker activity could challenge cash flows and increase demand for short-term credit from households and for working capital from companies. Such issues are likely to be most acute for smaller businesses. This economic shock will affect both demand and supply in the economy.

At its special meeting ending on 10 March

2020, the Monetary Policy Committee (MPC) voted unanimously to reduce

Bank Rate by 50 basis points to 0.25%. The MPC voted unanimously for

the Bank of England to introduce a new Term Funding scheme with

additional incentives for Small and Medium-sized Enterprises (TFSME),

financed by the issuance of central bank reserves. The MPC voted

unanimously to maintain the stock of sterling non-financial

investment-grade corporate bond purchases, financed by the issuance of

central bank reserves, at £10 billion. The Committee also voted

unanimously to maintain the stock of UK government bond purchases,

financed by the issuance of central bank reserves, at £435 billion.

The reduction in Bank Rate will help to

support business and consumer confidence at a difficult time, to bolster

the cash flows of businesses and households, and to reduce the cost,

and to improve the availability, of finance.

When interest rates are low, it is likely

to be difficult for some banks and building societies to reduce deposit

rates much further, which in turn could limit their ability to cut their

lending rates. In order to mitigate these pressures and maximise the

effectiveness of monetary policy, the TFSME will, over the next 12

months, offer four-year funding of at least 5% of participants’ stock of

real economy lending at interest rates at, or very close to, Bank Rate.

Additional funding will be available for banks that increase lending,

especially to small and medium-sized enterprises (SMEs). Experience from

the Term Funding Scheme launched in 2016 suggests that the TFSME could

provide in excess of £100 billion in term funding.

The TFSME will:

help reinforce the transmission of

the reduction in Bank Rate to the real economy to ensure that businesses

and households benefit from the MPC’s actions;

provide participants with a

cost-effective source of funding to support additional lending to the

real economy, providing insurance against adverse conditions in bank

funding markets;

incentivise banks to provide credit to businesses and households to bridge through a period of economic disruption; and

provide additional incentives for

banks to support lending to SMEs that typically bear the brunt of

contractions in the supply of credit during periods of heightened risk

aversion and economic downturns.

To support further the ability of banks to supply the credit needed to bridge a potentially challenging period, the Financial Policy Committee (FPC) has reduced the UK countercyclical capital buffer rate to 0% of banks’ exposures to UK borrowers with immediate effect. The rate had been 1% and had been due to reach 2% by December 2020.

The FPC expects to maintain the 0% rate

for at least 12 months, so that any subsequent increase would not take

effect until March 2022 at the earliest.

Although the disruption arising from Covid-19 could be sharp and large, it should be temporary. Such economic disruption should have less of an impact on the core banking system than recent stress tests run by the Bank have shown the system can withstand. Those stress tests demonstrated that banks would be able to continue to lend to businesses and households even while absorbing the effects of substantial, prolonged economic downturns in both the UK and the global economies, as well as falls in asset prices much larger than experienced in recent weeks.

Given the resilience of the core banking

system, businesses and households should be able to rely on banks to

meet their need for credit to bridge through a period of economic

disruption.

The release of the countercyclical capital buffer will support up to £190 billion of bank lending to businesses. That is equivalent to 13 times banks’ net lending to businesses in 2019. Together with the TFSME, this means that banks should not face obstacles to supplying credit to the UK economy and to meeting the needs of businesses and households through temporary disruption.

The FPC and the Prudential Regulation

Committee (PRC) will monitor closely the response of banks to these

measures as well as the credit conditions faced by UK businesses and

households more generally.

The release of the countercyclical capital

buffer reinforces the expectations of the FPC and the PRC that all

elements of banks’ capital and liquidity buffers can be drawn down as

necessary to support the economy through this temporary shock. In

addition, the Prudential Regulation Authority (PRA) has today set out

its supervisory expectation that banks should not increase dividends or

other distributions, such as bonuses, in response to these policy

actions.

Major UK banks are well able to withstand

severe market disruption. They hold £1 trillion of high-quality liquid

assets, enabling them to meet their maturing obligations for many

months.

In response to the material fall in

government bond yields in recent weeks, the PRC invites requests from

insurance companies to use the flexibility in Solvency II regulations to

recalculate the transitional measures that smooth the impact of market

movements. This will support market functioning.

The Bank of England has operations in place to make loans to banks in all major currencies on a weekly basis. Banks have pre-positioned collateral with the Bank of England enabling them to borrow around £300 billion through these facilities.

The actions announced today by the three

policy committees of the Bank of England comprise a comprehensive and

timely package to allow UK businesses and households to bridge a

temporarily difficult period and thereby to mitigate any longer-lasting

effects of Covid-19 on jobs, growth and the UK economy.

The normal line of argument has been that its central banks pumping liquidity into the financial markets which have led to falling real interest rates, and that they might indeed take them into negative territory. This is all to do with “secular stagnation” (reflecting poor productivity, globalisation, weak wages growth, and monetary policy intervention by central banks).

Last year the IMF in a working paper suggested that a cut of 4% or there abouts would be required to react to a financial crisis similar to the scale of the GFC. That would pull rates deeply negative, and of course so far (Sweden apart) no one has found a way back, as Japan and the Eurozone illustrates.

Many sovereign rates sit in negative territory, and there is an unprecedented $10 trillion in negative-yielding debt. This new interest rate climate has many observers wondering where the bottom truly lies.

Now, most economists are on a quest to return to a “stable positive rate”, eventually, considering negative rates to be there for am emergency, and temporary.

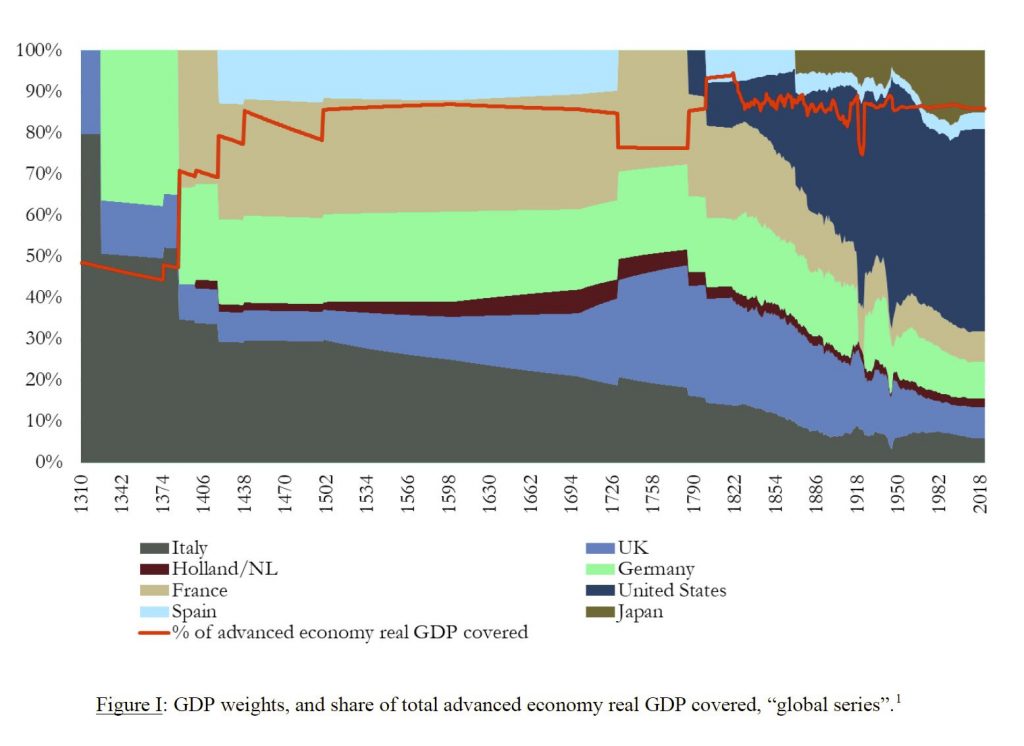

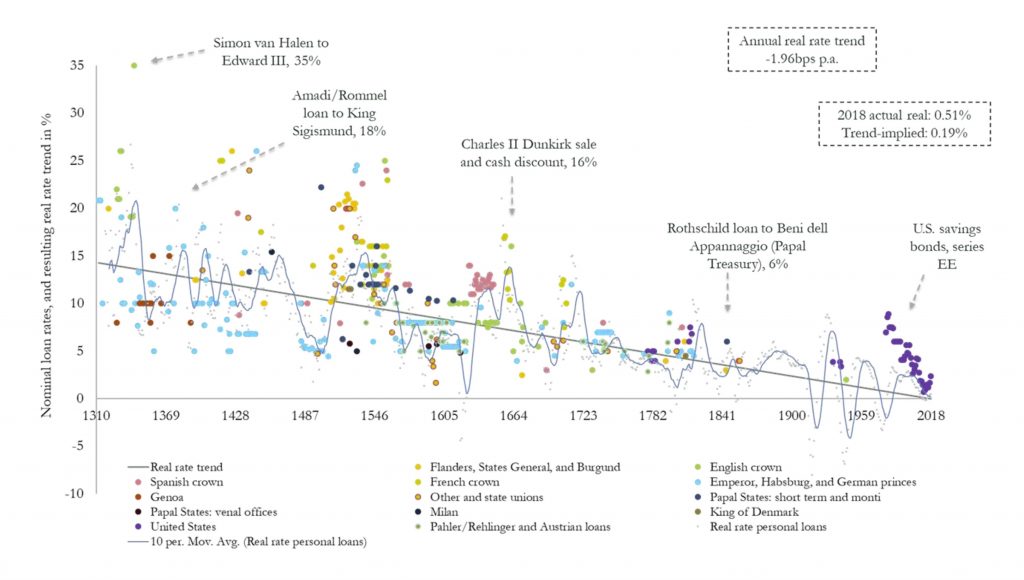

The paper creates a long term global series, weighted by GDP from 1310 to the present day. The series only includes yields which are not contracted short-term, which are not paid in-kind, which are not clearly of an involuntary nature, which are not intra-governmental, and which are made to executive political bodies. In other words, cash lending against annual payments in “chicken” and other commodities, or against leases for offices, against jewellery, land or other real estate with no known equivalent cash value are all excluded.

The GDP weights over time, and the share of advanced economy GDP covered by the series varies as history played out and empires rose and fell.

Data robustness is an issue, as the paper recognises as late medieval and early modern data can of course never be established with the same granularity as modern high-frequency statistics. One still has to rely on interpolations, deal with the peculiarities of early modern finance, and acknowledge that the permanency of wars, disasters, and destitution since medieval times may have irrecoverably destroyed a significant share of the evidence desired. However, the story is pretty clear.

The data here suggests that the “historically implied” safe asset provider long-term real rate stands at 1.56% for the year 2018, which would imply that against the backdrop of inflation targets at 2%, nominal advanced economy rates may no longer rise sustainably above 3.5%. Whatever the precise dominant driver –simply extrapolating such long-term historical trends suggests that negative real rates will not just soon constitute a “new normal” – they will continue to fall constantly. By the late 2020s, global short-term real rates will have reached permanently negative territory. By the second half of this century, global long-term real rates will have followed.

The standard deviation of the real rate – its “volatility” – meanwhile, has shown similar properties over the last 500 years: fluctuations in benchmark real rates are steadily declining, implying that rate levels are set to become both lower, and stickier. But downward-trending absolute levels, and declining volatilities have persisted against a backdrop of a secularly growing importance of public and monetary balance sheets. This would suggest that expansionary monetary and fiscal policy responses designed to raise real interest rates from current levels may at best have a cyclical effect in the longer-term context.

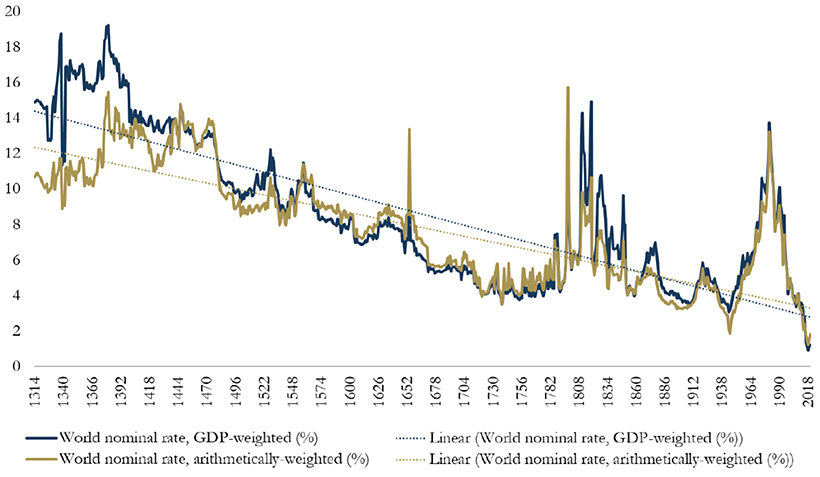

According to the report, another trend has coincided with falling interest rates: declining bond yields. Since the 1300s, global nominal bonds yields have dropped from over 14% to around 2%.

He concludes:

I sought to suggest that a long-term reconstruction of real rate developments points towards key revisions concerning at least two major current debates directly based on – or deriving from – the narrative about long-term capital returns.

First, my new data showed that long-term real rates – be it in the form of private debt, non-marketable loans, or the global sovereign “safe asset” – should always have been expected to hit “zero bounds” around the time of the late 20th and early 21st century, if put into long-term historical context.

In fact, a meaningful – and growing – level of long-term real rates should have been expected to record negative levels. There is little unusual about the current low rate environment which the “secular stagnation” narrative attempts to display as an unusual aberration, linked to equally unusual trend-breaks in savings-investment balances, or productivity measures. To extent that such literature then posits particular policy remedies to address such alleged phenomena, it is found to be fully misleading: the trend fall in real rates has coincided with a steady long-run uptick in public fiscal activity; and it has persisted across a variety of monetary regimes: fiat- and non-fiat, with and without the existence of public monetary institutions.

Secondly, sovereign long-term real rates have been placed into context to other key components of “nonhuman wealth returns” over the (very) long run, including private debt, and real land returns, together with a suggestion that fixed income-linked wealth has historically assumed a meaningful share of private wealth. There is a very high probability, therefore, to suggest that “non-human wealth” returns have by no means been “virtually stable”, only if business investments have both shown an extreme increase in real returns, and an extreme increase in their total wealth share, could the framework be saved.

If compared to real income growth dynamics we equally detect a downward trend across all assets covered in the above discussion.

There is no reason, therefore, to expect rates to “plateau”, to suggest that “the global neutral rate may settle at around 1% over the medium to long run”, or to proclaim that “forecasts that the real rate will remain stuck at or below zero appear unwarranted” as some have suggested.

With regards to policy, very low real rates can be expected to become a permanent and protracted monetary policy problem – but my evidence still does not support those that see an eventual return to “normalized” levels however defined, who contemplate a “nadir” in global real rates in the 2020s): the long-term historical data suggests that, whatever the ultimate driver, or combination of drivers, the forces responsible have been indifferent to monetary or political regimes; they have kept exercising their pull on interest rate levels irrespective of the existence of central banks, (de jure) usury laws, or permanently higher public expenditures. They persisted in what amounted to early modern patrician plutocracies, as well as in modern democratic environments, in periods of low-level feudal Condottieri battles, and in those of professional, mechanized mass warfare.

In the end, then, it was the contemporaries of Jacques Coeur and Konrad von Weinsberg – not those in the financial centres of the 21st century – who had every reason to sound dire predictions about an “endless inegalitarian spiral”. And it was the Welser in early 16th century Nuremberg, or the Strozzi of Florence in the same period, who could have filled their business diaries with reports on the unprecedented “secular stagnation” environment of their days. That they did not do so serves not necessarily to illustrate their lack of economic-theoretical acumen: it should rather put doubt on the meaningfulness of some of today’s concepts.

So negative rates are coming and are here to stay!

Blog")