The currently running Senate inquiry into bank branch closures has flushed out that while banks are claiming they are following their customers into a digital future, actually, they ae rather setting that agenda, removing ATMS and Branches and forcing people to go digital, whether they want to or not.

And some banks have all but admitted they are fudging the figures, to buttress their strategy, never mind the impact on real customers.

While politicians are keen to step back from the argument on the basis banks are commercial entities and should be able to make what ever strategic decisions they want, the truth is banks are a government protected species, who have received massive financial support from us tax-payers via the Term Funding Facility and other measures.

And to reinforce the argument that we are being lied to, according to a news.com.au exclusive article, a former ANZ employee has alleged that the bank is forcing customers out of branches and then using their absence to justify branch closures.

Phillip, a pseudonym told news.com.au that during the time he worked at an ANZ branch in a metropolitan area, staff were directed not to serve customers who came to the branch.

http://www.martinnorth.com/

Go to the Walk The World Universe at https://walktheworld.com.au/

Breaking news, as Westpac reverses its decision to close some of its regional branches, in response to the pressure form the Senate inquiry (which we managed to get up). I discuss this with Robbie Barwick from the Citizens Party.

The job is not done yet, and we need to ensure the Treasurer reverses his support for a totally independent Central Bank!

Giving up authority over the RBA – The ultimate BETRAYAL of the Australian people https://youtu.be/EA7FhBZxfuM

For the final time in Australia, I caught up with Robbie Barwick from the Citizens Party. We looked at the progress towards the establishment of a Public Bank in the light of recent failures, and the inquiry into Regional Banking.

Importantly, there are just two more weeks to get your submission to the Inquiry. Have your say! and support the transformational policy.

Make a submission to regional bank closures inquiry

Submissions to the inquiry are due by 31 March. All communities, organisations, businesses, and individuals impacted by the banks’ war on cash are strongly urged to make a submission, including to support a government post office bank.

A submission can be a formal representation from an organisation, or as simple as a letter or email, which explains to the Committee your experience and views.

Elderly and vulnerable regional bank customers, who are disproportionately affected, are especially encouraged to hand-write or type physical letters and mail them to the Committee through the post.

Mail your submission to the Committee at this address:

Committee Secretary Senate Standing Committees on Rural and Regional Affairs and Transport PO Box 6100 Parliament House Canberra ACT 2600

Email your submission to the Committee at rrat.sen@aph.gov.au

Upload your submission, and get more information, at the inquiry website

For more information, phone the Committee on 02 6277 3511.

http://www.martinnorth.com/

Go to the Walk The World Universe at https://walktheworld.com.au/

In the final part of my discussion with Ex-ANZ Director John Dahlsen, ahead of the closing date for submissions into the Senate Inquiry into Banking Structural Separation, we discussed the core questions, and what barriers really need to be overcome.

It promises to be a dog fight Royale. The four big banks can be expected to behave

like uncontrollable Pit Bulls, determined to savage Senator Hanson’s Banking

System Report (Separation of Banks) Bill 2019.

This Bill is about re-establishing confidence in the banking system by

separating ‘core banking’, called retail and commercial banking where deposits

are protected, from the risky wholesale and investment banking.

By Patricia Warren,Byron Echo Vol 33 #40 March 13, 2019 p21

By default the

recent Haynes Royal Commission has brought focus on how banks are currently

structured to do business. It’s their

power base and they will fight to defend it. Fur will fly because bankers do not want a firewall

between deposits and the flow of these into their trading activities. Bloodletting can be expected should this Bill

stand in the way of using your money to cover their gambling in high return

investments, including derivatives.

Learned from the GFC?

People are

reminded that it was the collapse of the derivatives market that brought about

the Global Financial Crisis 2007/08.

Nothing has been learned. In December

2018 “The notional value of the

derivatives cleared worldwide is 4.4 times world GDP, up from 2.8 times in

2008.” While not all derivatives

are evil, it is estimated that Australian banks are currently exposed to more

than $37Tr in derivatives and billions in short term debt. The global derivatives markets are vast,

unregulated, some deliberately untraceable in off-shore entities and commonly

off the books. Currently, there is

potentially US$540Tr of global derivatives set to ignite a global financial

crisis.

Divorce time

The idea of separating core banking activities from the higher

risk investment banking is not new.

Leading financial commentator, Alan Kohl wrote of his random sampling of

10,140 submissions to the Royal Commission, “ Without exception they called for the banks to be broken up and most

of them, surprisingly, used the term ‘Glass Steagall’ suggesting that the

now-repealed American law that used to forcibly separate banking from insurance

and investment banking be introduced into Australia”. Hanson’s Bill has been crafted after the Glass

Steagall and modified to suit the Australian conditions.

There is widespread support for the breaking up of the banks,

including that coming from former CEOs of major banks, academics and former

Prime Minister Paul Keating. In fact,

there are now more people supporting the breakup of the banks since the Royal

Commission than before it.

The banks are powerful and effective lobbyists exercising undue

influence not only in the market place where they work like an oligopoly but

with both major political parties to which they reportedly have donated $2.6m.

Their relationship with Treasury and the regulator, Australian Prudential

Regulatory Authority (APRA) has been described as ‘incestuous’.

Currently there is approximately $2.8Tr held in deposits as

unsecured loans in Australian financial institutions of which over 80% is

concentrated in the four big banks. Banks are currently paying very little interest

on deposits whilst using a significant proportion of funds to trade in high

risk areas.

BAIL IN

Under Australia’s BAIL IN legislation, where there is no explicit

exclusion of deposits in the law, deposits are exposed to cover the gambling

risks of financial institutions in times of financial crisis in the global

system. So, if the derivatives market

collapses, as it did in the GFC, then cash will be used to BAIL IN and stablise

failing global institutions be it from peoples’ term deposits, business

operating and superannuation fund accounts. Politicians have refused to amend the

Financial Sector Legislation Amendment (Crisis Resolution Powers and Other

Measures) Act 2018 (FSLA) to exclude deposits from this and hence are

protecting the bankers and their risk taking behavior.

Deny Risk

CEO’s of the major banks and other leading financial institutions

deny that deposits are at risk. They argue they are controlled by APRA’s

prudential standards and that ‘currently’

and ‘as the legislation sits’, only

‘capital instruments’ can be called upon to stablise a failing

institution. But APRA can change this

under the secrecy provisions of the FSLA to capture deposits as part of BAIL

IN. There is a loop hole which allows

APRA to change its standards to include ‘instruments’ ‘that are not currently considered capital under prudential standards.”

Failed

Gatekeeper

No CEO responded to concerns raised directly with them months ago

about that provision. Nor did APRA! APRA has failed as the gatekeeper on our financial system.

APRA takes recommendations directly from the International Bank of

Settlement (IBS). This means our

financial institutions are influenced by the motivation of the central bankers

to protect the global financial system above depositors.

Under the

Banking System Reform (Separation of Banks) Bill 2019 it is intended to break

that direct connection. Instead, APRA must

not only come before an Australian parliamentary committee for “prior express written approval and consent” to

act before implementing any recommendations or decisions of any foreign bank,

or foreign authority but have Parliamentary approval to change its prudential

standards for the purpose of regulating our financial institutions.

Public Inquiry

Parliament’s

Senate Standing Committee on Economics is currently holding a public inquiry on

the Bill and calling for submissions.

It is a numbers game and broad based support of the Bill is needed to

counter what can be expected from the banks, Treasury and APRA.

Submissions

need only read: I support the Banking System Reform

(Separation of Banks) Bill 2019 and I support the separation of retail commercial banking

activities involving the holding of deposits from wholesale and investment

banking as proposed in the Bill. Submissions

need to be sent to economics.sen@aph.gov.au or mailed to the Senate Standing Committee

on Economics PO Box 6100 Canberra ACT 2600 by 12 April 2019. If you want your cash made more secure then

you’re encouraged to make a submission.

Alternatively, there is always under the

mattress.

I discuss the latest on the Senate Inquiry into Banking Separation (Glass-Steagall) with Robbie Barwick from the CEC. We have a significant opportunity to drive the change to benefit Australians and Australia.

The Senate has initiated an inquiry into the structural separation of

the banks, following the Hayne report, and the bill represented to the

chamber.

I discuss the critical issues surrounding this with businessman John

Dahlsen, who was a director at ANZ for many years. John and I were

both mentioned in the Hansard on this topic!

There are so many compelling reasons to support structural

separation, yet there are powerful forces which will resist the concept.

The bottom line is structural separation would be good for customers,

good for shareholders, and good for businesses seeking finance; and

reduce the structural risks in the banking system thanks to derivatives

and too big to fail. So why is structure a dirty word?

This will help you to prepare a submission to the inquiry when its formally sought!

The Senate has initiated an inquiry into the structural separation of the banks, following the Hayne report, and the bill represented to the chamber.

I discuss the critical issues surrounding this with businessman John Dahlsen, who was a director at ANZ for many years. John and I were both mentioned in the Hansard on this topic!

There are so many compelling reasons to support structural separation, yet there are powerful forces which will resist the concept.

The bottom line is structural separation would be good for customers, good for shareholders, and good for businesses seeking finance; and reduce the structural risks in the banking system thanks to derivatives and too big to fail. So why is structure a dirty word?

This will help you to prepare a submission to the inquiry when its formally sought!

We review the recommendations from the PC Report, out today, which highlights that much needs to be done to put power back into the consumer. We are being taken the the cleaners at the moment…

Last Thursday, the House of Representatives Standing Committee on Economics released their third report on their Review of the Four Major Banks. They highlight issues relating to IO Mortgage Pricing, Tap and Go Debt Payments, Comprehensive Credit and AUSTRAC Thresholds.

Looking back at the issues The Committee raised since inception in 2016, they have had a significant impact on the banks and again shows how the landscape is changing, outside of a Banking Royal Commission. It also suggests The Commission will not necessarily deflect scrutiny!

Here are the key points from their report:

Since the House of Representatives Standing Committee on Economics commenced its inquiry into Australia’s four major banks in October 2016, the Government has announced significant reforms to the banking and financial sector to implement the committee’s recommendations.

The Treasurer requested that the House of Representatives Standing Committee on Economics undertake – as a permanent part of the

committee’s business – an inquiry into:

the performance and strength of Australia’s banking and financial system;

how broader economic, financial, and regulatory developments are affecting that system; and

how the major banks balance the needs of borrowers, savers, shareholders, and the wider community.

In November 2016, the committee published its first report, which followed the first round of hearings a year ago in October 2016. The report contained 10 recommendations to reform the banking sector, including calling for new legislation and other regulatory changes to improve the operation of the banking sector for Australian consumers. In a second report in April 2017, following hearings in March, the committee reaffirmed the 10 recommendations of its first report and made an additional recommendation in relation to non-monetary default clauses.

In the 2017 Budget, the Treasurer announced the Government would be broadly adopting nine of the committee’s 10 recommendations for banking sector reform. These recommendations include putting in place a one-stop shop for consumer complaints, the Australian Financial Complaints Authority (AFCA); a regulated Banking Executive Accountability Regime (BEAR); and, new powers and resources for the Australian Competition and Consumer Commission (ACCC) to investigate competition issues in the setting of interest rates. The government also adopted the committee’s recommendations in relation to establishing an open data regime and changing the regulatory requirement for bank start-ups in order to

encourage more competition in the sector.

The Committee’s Third Report makes the following recommendations to Government:

The committee is concerned by the increase in transaction costs merchants

now face as a result of the shift to tap-and-go payments. These costs are

ultimately borne by customers. If the banks do not act by 1 April 2018, regulatory action should be taken to ensure that merchants have the choice of how to process “tap and go” payments on dual network cards. At present merchants are forced to process these transactions through schemes such as Visa and MasterCard rather than eftpos. It is estimated that this forced processing costs merchants hundreds of millions of dollars in additional annual fees at present;

The Australian Competition and Consumer Commission, as a part of its inquiry into residential mortgage products, should assess the repricing of interest‐only mortgages that occurred in June 2017;

Despite many commitments by banks in the past to implement CCR, little

progress has been made. The Government should introduce legislation to mandate the banks’ participation in Comprehensive Credit Reporting as soon as possible; and

The Attorney‐General should review the major banks’ threshold transaction reporting obligations in light of the issues identified in the Australian Transaction Reports and Analysis Centre’s (AUSTRAC) case against the Commonwealth Bank of Australia.

Interest Only Mortgage Loans

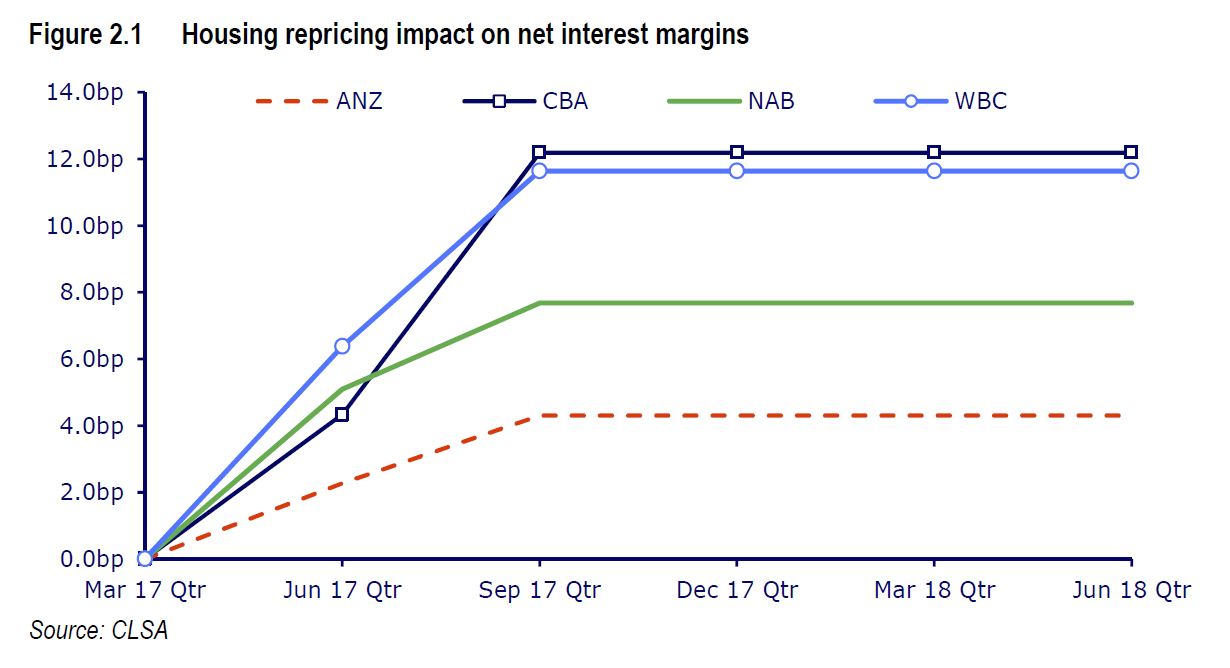

Specifically on the IO loan situation, while the banks’ media releases at the time indicated that the rate increases were primarily, or exclusively, due to APRA’s regulatory requirements, the banks stated under scrutiny that other factors contributed to the decision. In particular,banks acknowledged that the increased interest rates would improve their profitability. A key reason for such an improvement is that the major banks increased rates on both new and existing interest-only loans in June 2017. This is despite APRA’s interest-only measure only targeting new lending. As of 6 October 2017, analysts at CLSA estimated that the banks’ net interest margins increased by up to 12 bps following the rate increases announced in June and March.

The improvement in net interest margins is forecast to be so beneficial for Westpac that several analysts upgraded their outlook following the price announcements in June 2017.

The ACCC is currently conducting an inquiry into residential mortgage products. This inquiry was established to monitor price decisions following the introduction of the Major Bank Levy. As a part of this inquiry, the ACCC can compel the banks affected by the Major Bank Levy to explain any changes to interest rates in relation to residential mortgage products. The inquiry relates to prices charged until 30 June 2018.

The committee recommends that the ACCC analyse the banks’ internal documents to assess whether or not they are consistent with their statements in their June 2017 media releases and subsequent public commentary. In particular, the ACCC should analyse the banks’ decisions to increase interest rates on existing borrowers despite APRA’s measure only targeting new borrowers. Further, the ACCC should consider whether the banks’ public statements adequately distinguish between new and existing borrowers. The ACCC should consider whether the media statements suggest rates on existing interest-only mortgages rose as a direct consequence of APRA’s regulatory requirement. It will be important that the ACCC conducts granular analysis of the financial modelling of the banks. The ACCC will need to understand the true financial impact on the banks of APRA’s regulatory changes, and assess that impact against the public statements of the banks.

Blog")