It has been interesting reading the media coverage of the recently released ASIC report. Some suggest brokers have been “slammed”, others suggest its more a touch on the tiller in terms of commission models. Having read the ASIC report in full – more than 240 pages, I think there are three points worth making.

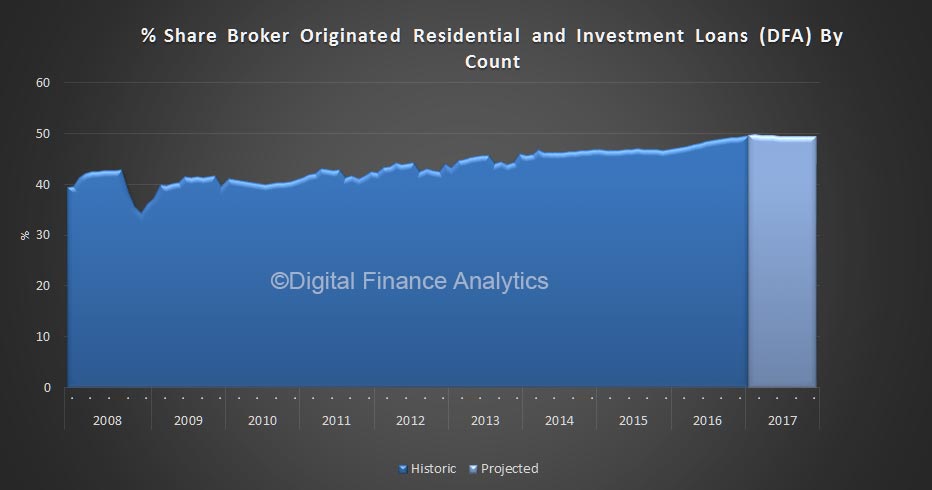

First, around half of mortgages are originated via the broker channel, it varies by lender of course, but consumers get more responsive assistance and access to industry knowledge via a broker, and our surveys indicate much higher satisfaction ratings than those going direct to a bank. Because brokers look across lenders, they should have access to a wider range of options, and (perhaps) better pricing. Different types of customers use brokers differently. But there is a valid and important role for brokers.

Broker originated loans may be more “risky” but this is more to do with the types of consumers who choose to use them.

Second, the current commission models are complex and not transparent, especially as it relates to soft commissions, incentives and other elements. In addition, the ownership of brokers is unclear. As a result consumers cannot be sure they are getting unbiased advice, and it may be the ownership structures and commissions get in the way. As ASIC says:

Remuneration and ownership structures can, however, inhibit the consumer and competition benefits that can be achieved by brokers.

ASIC also says:

Brokers almost universally receive commissions paid by the ‘supply side’ of the market (i.e. the lender or aggregator), rather than by the consumer. Our review identified significant variability and complexity in remuneration structures between industry participants. The common element across all remuneration structures for brokers, however, was a standard commission model made up of an upfront and a trail commission.

ASIC are not suggesting the removal of the commission model, but they are suggesting significant changes to it. There will be ongoing consultation on the nature of those changes. But I think the enhanced requirements for disclosure of ownership structures is as important. Transparency is good. Better transparency is better.

We did a piece on brokers on our video blog (in 2016) – in the Truth About Mortgage Brokers.

But third, there is something which continues to bug me. Financial Advisors have a requirement to provide “best interest” advice (see ASIC’s report today), whereas Brokers and Lenders dealing with often the largest transaction a household will undertake have a lower hurdle of “not unsuitable”. This bifurcation of the supervision regime makes no sense.

Both advisors and brokers should be clearly working in the best interest of the clients. So why not create a standard and unified regulatory framework, covering all product and financial advice? Now, I understand ASIC has two departments, separately looking at financial advice and mortgage lending but this is not a good enough reason. Time to put all advice, whether for wealth or lending, under the same regime. Not least because investment property loans are actually about wealth building, and should be considered as part of a wealth management strategy. One third of mortgages are for investors, and our research highlights investors are more likely to access brokers.

The requirement for transparency, quality of the advice, and consumer outcomes should be the same. Far fetched? No.

The Financial Markets Authority in New Zealand says:

Financial advisers are people who give advice about investing and other financial services and products as part of their job or business. They include financial planners, mortgage and insurance brokers and people working for insurance companies, banks and building societies that provide advice about money, financial products and investing.

They do not have this bifurcation.

All financial advisers must exercise the care, diligence and skill that a reasonable financial adviser would exercise in the same circumstances. In determining what a reasonable financial adviser would do, the following matters must be taken into account:

- the nature and requirements of the financial adviser’s client or clients

- the nature of the service and the circumstances in which it is provided

- the type of financial adviser

See more in section 33 of the Financial Advisers Act 2008. See examples below of how these obligations apply to advice on insurance and credit products.