The corporate regulator has told the Hayne royal commission that it is at a loss over how to successfully prevent misconduct in financial services, via InvestorDaily.

The Australian Securities and Investments Commission has expressed in its submission that work had to be done to stop misconduct in the industry but there was not enough evidence as to how.

“There is unfortunately currently a dearth of knowledge and research as to what effectively deters misconduct across the range of corporate sectors and, in particular, the financial sector itself,” it reads.

ASIC recognised that it had a duty to force significant cultural change in the industry and said it would begin onsite supervision in major financial institutions.

However, ASIC rejected the interim reports idea that it did not go to court or issue civil penalties.

The Hayne Interim Report made claims that ASIC rarely went to court, seldom brought civil penalty proceedings and allowed entity’s to pay infringement notices with no admission.

ASIC said it was willing to change its enforcement practices but said it regularly undertook litigation against the financial sector.

“ASIC has litigated matters (through civil and criminal proceedings) twice as much as it has accepted enforceable undertakings,” ASIC’s report read.

ASIC also rejected the emphasis the interim report placed on its track record in the past decade against the major banks.

The interim report noted how ASIC had only issued commenced 10 civil proceedings against the major banks but 45 infringement notices to the major banks and accepted 13 enforceable undertakings.

ASIC said that the figures expressed in the report do not support the proposition that ASIC presently avoids compulsory enforcement action, nor do they reflect the full variety of enforcement tools made available to ASIC.

ASIC provided no comment on the interim reports findings that the commission had never brought proceedings against a licensee who failed to report a data breach.

“As at April 2018, ASIC had never brought, or sought to have the Commonwealth Director of Public Prosecutions (CDPP) bring, proceedings against a licensee for failing to comply with the 10 day time limit for breach reporting under Section 912D of the Corporations Act 2001 (Cth) (the Corporations Act), 21 despite affirming that it believed that entities frequently fail to comply with the section,” the report read.

The commission also provided no comment to the reports findings that it had never commenced proceedings against an entity for fees for no service.

“At 30 May 2018, ASIC had never commenced, or sought to have CDPP commence, proceedings under Section 12DI of the Australian Securities and Investments Commission Act 2001 (Cth) (the ASIC Act). This prohibits accepting payment for financial services when the payee does not intend to, or there are reasonable grounds to believe it cannot, supply the service,” it read.

The latest batches of documents released by the Royal Commission into Financial Services Misconduct included a litany of poor or illegal behaviour across the broker groups. This included detailed incidents of falsifying documents and fraud, plus sexual harassment, offensive behaviour and homophobia based on 215 newly released documents from 94 groups. We can conclude this is way more than “just a few bad apples”.

While most, if not all, broker groups detailed incidents of falsifying documents and fraud, it has been revealed some of the behaviour at Aussie Home Loans included sexual harassment, offensive behaviour and homophobia.

The group has said it will continue to support reporting of such unacceptable behaviour as it to enforces a zero-tolerance policy.

When the Royal Commission into banking misconduct was first established, Commissioner Kenneth Hayne asked financial entities to provide information on misconduct or conduct falling below community standards over the last ten years.

While the incidents listed in the reports were to be the basis for many of the hearings during the Royal Commission, these 215 newly released documents from 94 groups paint a much broader picture.

Looking exclusively at submissions from broker groups, misconduct was listed alongside any action taken and subsequent outcome.

AFG submitted 12 items detailing incidents, which included brokers providing false documents, making administrative errors, breaching the privacy of clients, failing to comply with NCCP obligations and creating false approval letters.

Loan Market also made a submission which detailed 33 incidents of misconduct. Incidents included creating false documents, tampering with documentation, inappropriate use of social media, overstated consumer income and copying and pasting signatures.

Mortgage Choice has listed ten incidents including more than one case of falsifying signatures, providing false loan approval letters, misstating customer financial positions and falsifying documents. The broker group also listed three cases of failing to produce a Statement of Advice to customers.

Smartline listed incidents of altered valuation reports, failure to make reasonable enquiries about a customer’s financial circumstances and inaccurate information on loan applications.

The mortgage group also included an incident where a borrower’s credit card was allegedly fraudulently obtained and used, which at the time of submission was subject to a NSW police investigation.

It also detailed an “isolated incident” relating to theft from a customer and ended with the broker’s licence being revoked and the sale of their franchise.

Yellow Brick Road’s submission also included details of fraud and false documents. In one case a Vow Financial broker was accused of fraudulently gaining access to customer bank accounts and transferring funds.

Commonwealth Bank’s submission included details of behaviour at Aussie Home Loans. It includes details of “offensive or otherwise unprofessional behaviour” directed at employees and/or brokers.

Out of 182 total incidents, there were 29 listed as misconduct relating to false documents and/or declarations and/or misleading information.

There were 19 incidents listed in relation to NCCP breaches, including lack of reasonable care, failing to make the right enquiries and encouraging customers not to disclose the purpose of the loan.

The remaining incidents included, but were not limited, to:

Sexual harassment at a work event, and sexual harassment outside of work

Using Aussie’s IT system to send “emails containing objection material which could cause offense to a reasonable adult”

Accessing customer’s personal details

Numerous counts of unprofessional language and tone

Pretending to be the customer

Mutiple examples of ex-brokers using confidential information to contact former customers

Disclosing customer details to other parties

“Unprofessional conduct by making veiled threats to customer’s solicitor and allegedly impersonated someone else”

Customers experiencing homophobia

Derogatory and discriminatory comments

Alleged abuse of female in car park by a retail store broker and issue disclosed on Facebook

Attending a licenced venue “on a regular basis” and returning to work visibly drunk

Gaining access to an Aussie office after a work event, theft and assault

Inappropriate sexual language with fellow employee

Bullying by senior executives

A spokesperson from Aussie Home Loans said, “Media reports of submissions to the Royal Commission cited isolated incidents of unacceptable conduct involving staff and contractors over a ten year period.

“Aussie provided the Royal Commission a detailed and exhaustive table of incidents as a result of building a culture of actively encouraging and facilitating staff, contractors and customers to speak up and report unacceptable conduct.

“In each and every case of unacceptable conduct, Aussie took appropriate and swift disciplinary action, which included termination of employment and contractor agreements.

“Aussie will continue to actively encourage reporting of unacceptable conduct, to enforce its zero-tolerance policy for such conduct and to enhance its systems and process to prevent, detect and deter such conduct.”

This week the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry published all of the initial submissions from organisations from across the sector, via InvestorDaily.

Prior to the commencement of the public hearings, a number of entities were asked to provide the commission with information concerning instances of misconduct or conduct falling below community standards and expectations that the entity had identified in the past 10 years.

Commonwealth Bank of Australia (CBA)

CBA named 15 former employees who have been banned by ASIC since 2011. All of them were either Commonwealth Financial Planning (CFP) employees or operated under Financial Wisdom Limited (FWL).

The most recent case involved the banning of adviser Kimberley Holgate earlier this year.

CBA explained that the former CFP employee was banned for five years for engaging in conduct that was Holgate likely to mislead by cutting clients’ signatures from documents held on file and pasting them onto new documents.

The bank also noted that the adviser was “not acting in the best interests of her clients when advising they rollover their existing super to a new product issued by CFSIL; not acting in the best interests of her clients by advising them to cancel existing insurance policies and apply for personal insurance issued by Comm Insure; and failing to prioritise the interests of her clients when advising them to acquire financial products which entitled her, her employer and its related entities to a financial benefit.”

In the period since 1 January 2008, CBA identified 15 adverse findings against the group.

Australia and New Zealand Bank (ANZ)

Meanwhile, ANZ admitted to the royal commission that 18 financial advisers falsified customer or compliance documents over the period and had deliberately overcharged fees.

“A number of different factors caused or contributed to the improper or non-compliant conduct of advisers, including the failure of ANZ’s processes, controls and supervision to protect against that conduct,” the bank said.

National Australia Bank (NAB)

NAB’s submission detailed extensive misconduct across its lending and advice divisions over the last decade, including a number of incidents relating to the misuse of customer funds.

“Some of the conduct was or is being investigated by the Victorian Police and ASIC,” NAB said.

“One financial adviser was convicted and sentenced to imprisonment. The financial adviser has appealed the sentence.”

Despite a plethora of examples of misconduct since 2008, NAB does not consider much of the conduct to be attributable to any particular “group culture”.

Westpac Banking Corporation

Westpac identified significant misconduct across its mortgages business, including bankers forging supporting documentation and customer incomes.

In November 2015, Westpac identified incidents of staff engaging in conduct to simulate the creation and activation of new accounts to artificially inflate metrics used to calculate their variable rewards.

“In particular, the conduct involved simulating the deposits and withdrawals of $50 to suggest that accounts were ‘active’. An internal investigation identified a number of instances of simulated account funding between January 2013 and December 2016, which resulted in the termination of a number of staff together with other disciplinary measures,” the bank admitted.

HSBC Australia

HSBC Australia detailed more than 20 examples of misconduct over the last 10 years, including a number of instances where branch staff stole money from customer accounts.

Over a number of weeks in late 2009 and early 2010, a staff member at an HSBC Australia branch allegedly made unauthorised use of a customer’s replacement bank card, withdrawing a total of $22,880. An internal investigation revealed a number of recurring breaches of HSBC Australia’s security procedures at the branch concerned, involving two further staff members.

“The employment of all three staff members was terminated for security breaches and the customer reimbursed. Other staff at the branch received supplementary training in security procedures,” HSBC confirmed.

In October 2009, a staff member spent $6,000 using a customer’s credit card. Following an internal HSBC Australia inquiry, HSBC Australia reimbursed the customer’s credit card and the staff member left HSBC Australia.

Between June 2011 and June 2017, a staff member at an HSBC Australia branch in Sydney misappropriated $913,115 from the accounts of eight customers. The bank discovered the conduct in July 2017 after an affected customer disputed a transaction and, following an internal investigation, HSBC Australia reported it to the NSW Police and ASIC.

“HSBC Australia continues to support the police investigation. All customers other than three have been reimbursed,” the bank said, adding that it is working to contact two of those customers, both of whom are foreign nationals and one of whom is presumed dead.

“The third has been contacted numerous times but is yet to provide details to allow return of funds. In the meantime, the money has been placed in holding accounts. The staff member’s employment was terminated consistent with the Consequence Management Framework.”

The upcoming round of public hearings for the financial services royal commission will focus on misconduct and conduct falling below community expectations as well as possible regulatory reform, via The Adviser.

The seventh round of hearings for the final round of the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry (RC) will be held at the Lionel Bowen Building in Sydney from 19 to 23 November and at the Commonwealth Law Courts Building in Melbourne from 26 to 30 November.

Following on from the six previous rounds (which focused on consumer lending practices; financial advice; SME loans; issues affecting Australians who live in remote and regional communities; and insurance, respectively), it has now been revealed that the seventh round of hearings will focus on “causes of misconduct and conduct falling below community standards and expectations by financial services entities (including culture, governance, remuneration and risk management practices), and on possible responses, including regulatory reform”.

The royal commission had previously stated that the seventh round would focus on “policy questions arising from the first six rounds”.

In an update, the royal commission revealed that the purpose of round seven is “to provide the commissioner with an opportunity to explore with senior executives from certain financial services entities, and the regulators of those entities, some of the policy issues identified in the interim report, and following rounds five and six of the public hearings”.

The hearings will also consider the role of the Australian Securities and investments Commission (ASIC) and the Australian Prudential Regulation Authority (APRA) in “supervising the actions of financial services entities, deterring misconduct by those entities, and taking action when misconduct may have occurred”.

According to an update from the RC, the hearings will include all four major banks (Australia and New Zealand Banking Group Limited, the Commonwealth Bank of Australia, National Australia Bank Limited and Westpac Banking Corporation) as well as AMP Ltd, Bendigo and Adelaide Bank Ltd, Macquarie Group Ltd, and ASIC and APRA.

However, the commission has said that further entities may be included before the hearings commence.

Due to the “different nature” of this next round of hearings, the RC has said that there will be no process for applications for leave to appear for this round of hearings.

Instead, a person who is summoned to give evidence before the commission may be represented by a legal representative at the hearing without the need for that representative to obtain separate authorisation, the commission revealed.

It is expected that the procedure for the next round of hearings will see the counsel assisting the commission lead and ask questions of all witnesses, after which the legal representative for the witness may ask questions of the witness (limited to matters arising out of the questions asked by counsel assisting, unless given leave to ask questions beyond those matters). The counsel assisting the commission may then re-examine the witness. Cross-examination of witnesses by other persons or entities will not be permitted.

The commission has further revealed that the commission is now “considering” the public submissions received relating to the interim report and rounds five and six, adding that “they will inform the matters that the commissioner seeks to explore during round seven”.

There will be no process for further submissions to be lodged following the conclusion of round seven.

It is expected that the seventh round will be the final round of the financial services royal commission, unless Commissioner Hayne requests, and is granted, an extension.

Commissioner Kenneth Hayne is expected to release his final report, which will include the topics of the fifth, sixth and seventh rounds of hearings (focusing on superannuation, insurance and “policy questions arising from the first six rounds”, respectively) by 1 February 2019.

On Friday, submissions to the Royal Commission into Financial Service Misconduct relating the the draft report closes. You can still make a Public Submission – a quick and painless process, and it is a once in a generation chance to shape the future of finance in Australia.

On Friday submission to the Royal Commission into Financial Service Misconduct relating the the draft report closes. You can still make a Public Submission – a quick and painless process, and it is a once in a generation chance to shape the future of finance in Australia.

This is what DFA did today, and here is a copy of what I said.

Summary

We welcome the findings from the draft report and recommend the following policy options.

The culture in the finance sector needs to change, to put the customer first. Mortgage brokers for example should have a best interest duty and commissions should be banned.

The current focus on “financial stability” is myopic, favouring large players, over small, and building structural risks into the system; the regulators have failed.

The large players are too big to fail and too complex to manage, and need to be broken apart. A modern Glass Steagall separation would achieve this, and is proven to reduce risk, and drive better customer outcomes and right size our finance sector.

The existing regulatory structure, operating in the Council of Financial Regulators needs to be changed, as its narrow focus on financial stability, and a massive “bet” on inflating the housing sector now at risk. None of the regulatory actors are without blame.

Introduction.

Digital Finance Analytics (DFA) is an Australian boutique research, consulting and advisory firm which combines primary consumer and small business research, analysis of both private and public datasets and economic modelling to analyse the dynamics of the finance and property sector. We have been operating since 2005.

Our analysis is based on a rolling 52,000 household survey, with more than 4,000 new data points added each month. From this we are able to assess the state of household finances, their future property transaction intentions, and their level of debt; and ability to service it.

Households Are Overextended

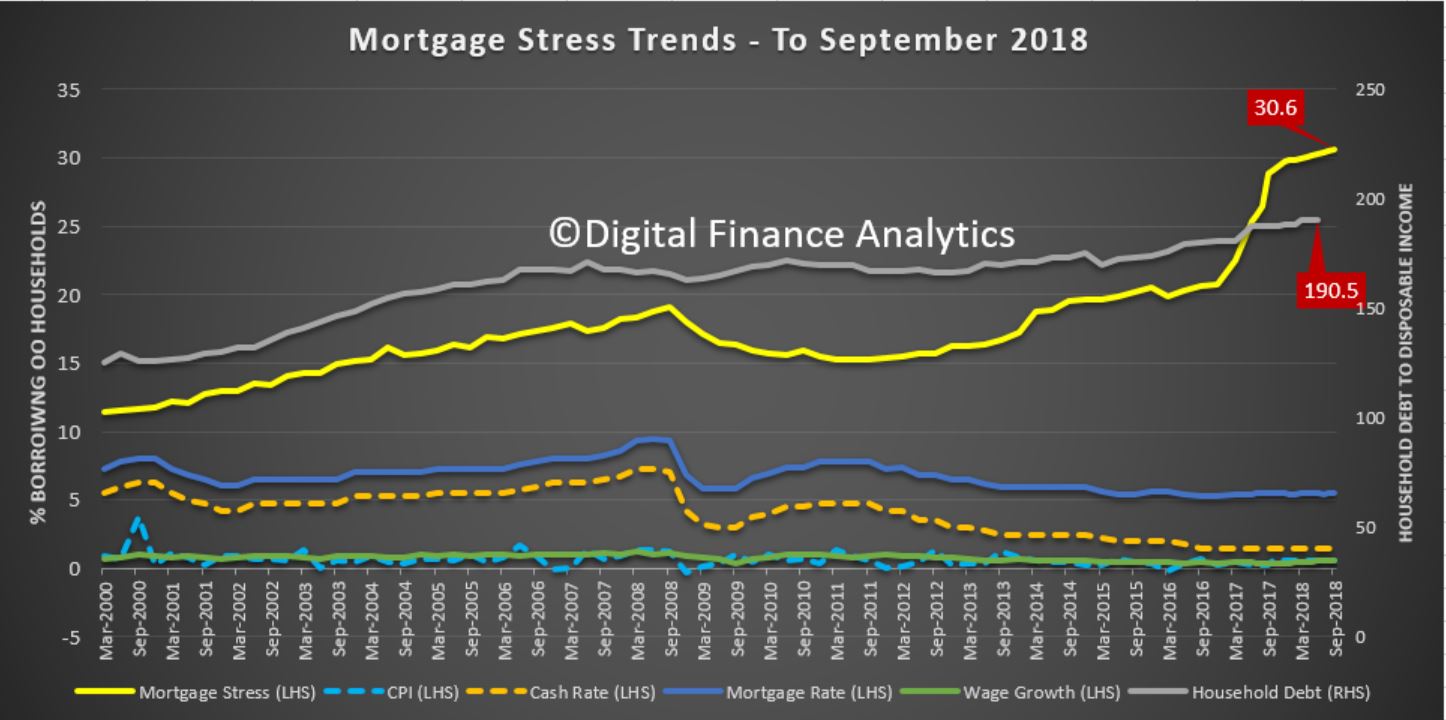

We have observed a considerable expansion of household debt in recent years, driven by low interest rates, more generous lending standards, and some degree of “not suitable” lending and fraud. The RBA reports that the household debt to income ratio is now around 190 and the debt to GDP ratio is one of the highest in the world.

As a result, more households are in financial stress, as tracked in our mortgage stress trends (defined in cash flow terms, not a set percentage), and last month more than one million households with owner occupied mortgages were in difficulty, despite the ultra-low interest rates. This equates to 30.6% of all borrowing households.

This has been exacerbated by flat incomes, and rising costs, but poor lending practice is the underlying cause. We also believe that as interest rates rise, and property prices fall further, the financial state of households will decline further. This is because many are enjoying the “wealth effect” of property gains in recent years, but this is only a paper gain, and now prices are falling. The expectation is prices will fall further and faster.

The Cause of Property Price Falls

Following many years of over-free lending, the regulators have now intervened to an extent and as a result lending standards are tightening, with up to a 40% fall in borrowing power for many compared with a year ago. In the main though this is a result of the existing regulations now being applied as originally intended, rather than new laws, as incomes and expenses are being tested, as opposed to using a formula based on HEM (Household Expenditure Measures).

This resetting of lending standards marks a significant change in the market, and as a result according to our surveys, demand for property is easing, at the time when foreign buyers are receding, and property investors are getting twitchy. According to Bank of England research, property investors are significantly more likely to exit the market in a down turn compared with owner occupied borrowers.

Property investors, who have driven the market higher in recent years are choosing to exit, sometimes forced by the switch from interest only loans to principal and interest loans (estimated at around ~$120 billion per annum), of the $1.7 trillion total mortgage lending pools.

Our modelling shows that it is credit availability which pumped up property prices (and which allowed the Banks and other Lenders to growth their balance sheets, and profits) and the reverse is also true. The normalising of lending standards will rightly reduce credit, thus driving home prices and banks profitability lower. The catch here is that for more than a decade, Australia’s economic performance has been built on the back of ever greater mortgage and consumer debt, home price growth, and construction. Thus from a policy perspective Government, and the RBA will defend high levels of credit and home prices, despite the risks.

The other factor to consider is that as banks were so reliant on home lending to drive profitability, the incentives were there to over lend, bend the rules, and reward poor behaviour. They have not followed regulatory guidelines nor have they met community expectations. In a word, GREED, as your draft report shows.

The Policy Challenge

Our view is that whilst the restatement of the current lending standards will assist, there are more significant structural questions to be considered. Regulation and changes to the law alone cannot address the issues you call out.

The culture within the finance sector needs to be changed, to put customers at the centre of their business. Whilst talk is cheap however, there is little evidence of substantial change as yet. The removal of commissions should be a corner stone, as conflicted remuneration remains a significant problem. Mortgage brokers, for example, should have a responsibility to act in the best interest of their customers. The industry will resist this, but it is essential.

Currently, the capital adequacy rules favour mortgage lending relative to productive lending to business and as a result according to our Small and Medium Enterprise surveys, many businesses are unable to obtain finance (or can only do so by securing their property). We believe the various risk weights reflect a myopic view of the financial system and they need to be changed. Too much of the bank’s portfolio of loans – up to 65% – is against residential property – this is extraordinarily high by international standards, and presents a significant risk, to say nothing of the lack of business investment which has resulted.

However, we hold the view that the major financial sector players are too complex to be managed effectively, scale is now a disadvantage. Thus we believe there is a case to break up the banks into smaller units. This would involve both vertical disaggregation (separation of advice, sales and product manufacture) and horizontal disaggregation (separate of wealth, insurance, retail banking and investment banking). In addition, there are significant risks from their operations in derivatives, and in an integrated environment, costs, risks and profits are cross linked. Given the size of the derivatives sector (significantly larger than before the GFC), the systemic risks are significant. To counter this, we advocate the implementation of a modern Glass Steagall separation, where the high-risk speculative activities are separated from the normal lending, payment and deposit functions within banking. This would have the added benefit of reducing the potential risks of a bank deposit bail-in in a time of crisis. Evidence suggests that the existence of a modern Glass Steagall separation would reduce risk and limit systemic risk. In a post Glass Steagall world, bank lending would be more aligned with the deposits available, so their ability to make loans “from thin air” as in the current system would be curtailed. They would also be more inclined to make loans for truly productive purposes.

We also need to consider the role of the regulators and the RBA. Murray’s Financial System Inquiry recommended that the effectiveness of the current regulatory system be monitored. The Council of Financial Regulators is the peak body, chaired by the RBA, where key policy is set, with the Treasury, ASIC, APRA and others. However, none of their deliberations are made public, and it appears that all entities have been sharing the same view that growing housing credit was the chosen growth lever of choice following the mining boom. It appears that the weak supervisory approach from ASIC and APRA stemmed from this policy, and was supported by policy rates being set too low. As a result, the systemic risks have been underestimated, and the economic platform for the country narrowed.

We believe that there should be a stronger advocate for the consumer within the regulatory system, perhaps the ACCC should take this role. But more broadly the role of individual regulators and how they connect needs clarity. The Royal Commission highlighted the lack of coherence, and alignment. We also would argue (perhaps beyond the scope the current inquiry) that APRA has myopically focussed on financial stability, at the cost of good consumer outcomes and competition, that the regulations favour large players over small players, that the RBA policy rates are too low, and the ASIC so far is still perceived as a weak and ineffective regulator. Thus the area of appropriate and effective regulation is critical.

Despite the revelations of the Royal Commission, ASIC is still experiencing deliberate delays from financial institutions in meeting reporting requirements, via Financial Standard.

On Friday, ASIC chair James Shipton told the Parliamentary Joint Committee on Corporations and Financial Services that the regulator is still experiencing “slow and delayed responses from financial institutions and, in some cases, overly technical responses aimed at delay.”

This is despite a key finding of the Royal Commission’s interim report being that the industry has been repeatedly dishonest with both the community and regulators, Shipton said.

“And unfortunately, whilst we are hearing important acknowledgements from leaders of financial institutions about change, such change is not happening as quickly as it should,” he said.

“Due process is important, but it must not be manipulated to disrupt the achievement of fair, appropriate and honest outcomes.”

He then warned institutions of the ramifications if such conduct continues.

“If institutions lie, or are otherwise dishonest with us, we will use every power available to us to punish that behaviour. I am a firm believer in the importance and effectiveness of court-based enforcement tools. They are the foundation of any regulator,” Shipton said.

Further, in defending ASIC on criticisms of its effectiveness in recent years, Shipton questioned whether the entity he leads should be resourced differently to meet community expectations.

Shipton said any comments as to ASIC’s regulatory approach should be considered in the context of its size, stating: “ASIC has been designed over the arc of its history and how Australia’s financial system has evolved over the years to have its own unique characteristics.”

He said now is the right time to discuss whether ASIC and its peers are “right sized” in relation to the new industry funding model; unique characteristics of Australia’s financial system; size of Australia’s financial markets; number of consumers; number of people engaged in the industry; and the clear expectations of the community.

Shipton clarified that he was not demanding greater resources, but instead looking to start an important policy conversation.

“For me, my own experience as a regulator in Hong Kong, in a system that also has an industry funding model, is instructive. There, on an adjusted basis (in terms of financial services GDP and financial services population), Hong Kong’s financial regulators are three times the size of Australia’s,” he said.

“Did you think to yourself that taking money to which there was no entitlement raised a question of the criminal law?” Commissioner Kenneth Hayne asked Nicole Smith, who resigned as chair of NAB’s superannuation trustee, NULIS, a little more than a month before she fronted the banking royal commission.

Smith’s evidence related to NAB skimming A$87 million from superannuation accounts by charging 220,000 members “service fees” for which no service was provided. As head of the board of the superannuation trustee, it was Smith’s job to act solely in the best interests of the members. Instead she acted in the best interests of NAB.

Her admissions and the evidence from the royal commission that more than $A1 billion has been taken from superannuation accounts for no service show we need better supervision of the trustees who oversee more than A$2.7 trillion in superannuation assets.

Trustees are surrounded by temptation, to preference the interests of their sponsoring organisations, to act in the interests of other parts of their corporate group, to choose profit over the interests of members, and to establish structures that consign to others the responsibility for the fund and thereby relieve the trustee of visibility of anything that might be troubling.

The entrenched practice of retail super funds using superannuation trust funds as profit-making enterprises undermines the integrity of the whole superannuation sector. Focused regulatory action and oversight are imperative to protect it.

Super duties

Super trustees are subject to a range of stringent duties.

There are “equitable” duties, which arise from trustees being fiduciaries – responsible for acting in the best interests of the owners of the assets they manage. As fiduciaries, super trustees must avoid conflicts of interest and account for any profit they make.

As trustees specifically, they must act in the best interests of the beneficiaries and exercise powers conferred to them as trustees (trust powers) with real and genuine consideration.

All trustees are legally obliged to act in the best interests of the people whose money they are entrusted with. Superannuation trustees have an even greater obligation, because of the social importance of superannuation. The High Court has ruled that public expectations mean superannuation trustees have “more intense” obligations than other private trusts.

This is underlined by the “statutory” duties of the Superannuation Industry (Supervision) Act 1993. It states directors of corporate superannuation trusts must perform their duties in the best interests of their beneficiaries, superannuation fund members.

The act also establishes supervision and oversight of super trustees by the Australian Prudential Regulation Authority (APRA), the Australian Securities and Investments Commission (ASIC) and the Commissioner of Taxation.

Irregular regulation

Yet clearly this oversight has been failing. The evidence from the royal commission is that many super trustees having been ignoring their duties. They have gone along with rubber-stamping unjustifiable fees purely because their parent institutions wanted the money.

In 2017 the prudential regulator was given the power to directly disqualify directors of superannuation trustee corporations. It already had the power to do so by applying to the Federal Court. Over the past decade, however, it has sought just one disqualification.

The regulator’s deputy chair, Helen Rowell, has argued this is due to APRA trying to protect the public interest, avoiding the risk of a run on a fund. But its inaction has arguably emboldened super trustees to ignore their duties because of the low risk of being penalised.

Previous reform proposals

The royal commission may result in criminal charges against banks and financial institutions. One outcome that must come is stronger oversight of super trustees.

It is therefore critical the royal commission recommend strong action, including reforms proposed by previous inquiries into the financial services sector.

These include the Financial System Inquiry, which recommended in 2015 that super funds must have a majority of independent directors on their trustee boards. It also proposed new civil and criminal penalties for directors failing to act in the best interests of fund members.

Additional reforms might include:

establishing a specific conduct regulator for corporate superannuation trustees

making it mandatory for ASIC to prosecute superannuation trustees and related entities (such as banks) for duty breaches, with much higher penalties

stronger oversight over responsibilities that corporate trustees outsource to third parties

mandatory reporting of corporate fee structures, with regular review to determine if these are justified.

The trust remains the most appropriate legal mechanism to manage savings accumulated over a long time. Much stronger behavioural controls and civil penalties are necessary to ensure super trustees act honestly and in good faith for the benefit of the beneficiaries. That they are, in short, trustworthy.

Author: Samantha Hepburn Director of the Centre for Energy and Natural Resources Law, Deakin Law School, Deakin University

I discuss the potential impact of an Australian Glass-Steagall banking separation with Robbie Barwick from the CEC.

There is a bill in the Parliament currently, and The Banking Royal Commission is taking submissions on strategic issues such as the structure of banking in Australia, so this is a timely discussion.

It also offers a mechanism to protect bank deposits and to restore trust to mainstream banking, something sorely needed as the Commission revealed.