In the just released results, Bendigo and Adelaide Bank has announced a profit of $423.9 million to June 30 2015. However, this is more from efficiency and provision adjustment than underlying business momentum, in our view, in a tough market. Nevertheless, they do have a good core franchise, with a relatively high customer satisfaction rating.

Underlying cash earnings were up 13.1%. Net interest margin was squeezed by 4 basis points to 2.20%, reflecting competition in the low interest rate environment. It dropped further in 2H15 to 2.17%. Common equity tier 1 ratio increased 15 basis points to 8.17%. Total capital increased 118 basis points to 12.57%. They continue to focus on achieving advanced capital accreditation, but are not there yet.

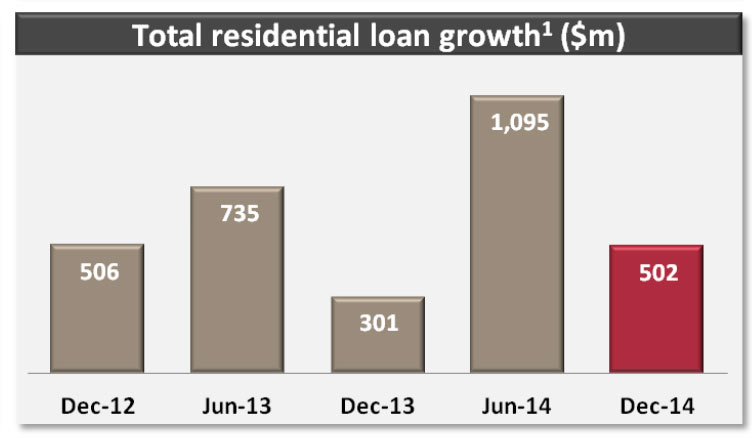

Lending growth at 5.3% was below system (7.5%), whilst business lending was 10%, above system, of 8.3%. Home lending was also slower than system growth, and they noted a 20% increase in excess repayments.

Great Southern specific provisions were reduced from $323.8m to $257.7m since December 2014.

They have been focussing on efficiency management, with the expense to incomes ratio down, though overall operating expenses rose 6.6% to $878m.

Looking at the segmentals, retail banking and rural were up, whilst wealth and third party banking were down.

Bad and Doubtful debt provisions were down 16.6%, to $68.1m. However, 2H15 were higher due to $15.9m provision for Great Southern. We note that 90 day+ arrears were up for residential to (~1.3%) and business to (~1.7%). Rural, their highest growth sector, had highest arrears around 5.5%.

Bad and Doubtful debt provisions were down 16.6%, to $68.1m. However, 2H15 were higher due to $15.9m provision for Great Southern. We note that 90 day+ arrears were up for residential to (~1.3%) and business to (~1.7%). Rural, their highest growth sector, had highest arrears around 5.5%.