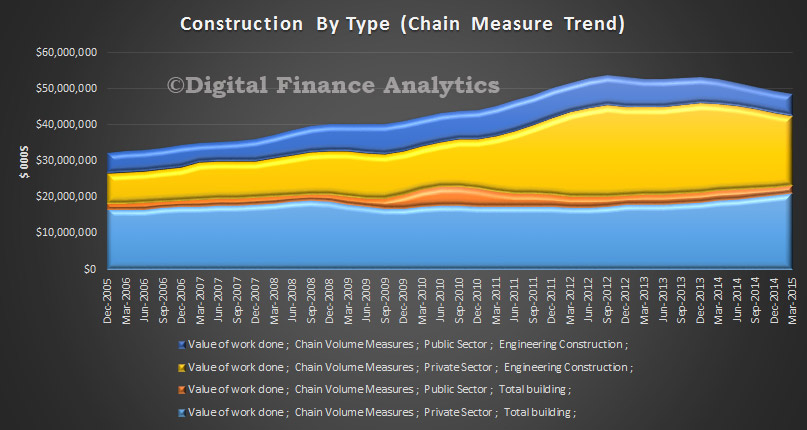

Data from the ABS yesterday and today together sum up the problem with the Australian economy. Yesterday we got the latest construction data showing that mining was dropping, and construction, especially residential construction, was up, but not enough to compensate, so the overall trend is a fall in activity. The trend estimate for total construction work done fell 1.8% in the March quarter 2015. The trend estimate for non-residential building work done rose 0.2%, while residential building work rose 3.1%. The trend estimate for engineering work done fell 4.7% in the March quarter.

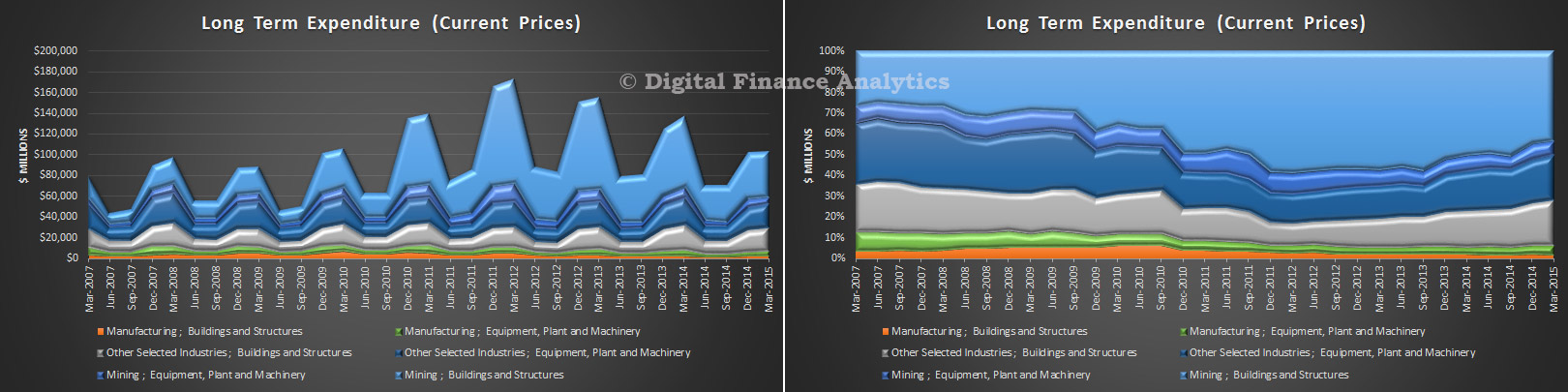

Today we got data on private sector capex. The trend volume estimate for total new capital expenditure fell 2.3% in the March quarter 2015, the trend volume estimate for buildings and structures fell 3.7% in the March quarter 2015 and the trend volume estimate for equipment, plant and machinery rose 0.7% in the March quarter 2015. Forward looking capital expenditure (a dodgy data set by definition) shows the same trend, mining falling away quicker then other part of the economy, including construction and manufacturing not filling the gap, so net trend is down.

Today we got data on private sector capex. The trend volume estimate for total new capital expenditure fell 2.3% in the March quarter 2015, the trend volume estimate for buildings and structures fell 3.7% in the March quarter 2015 and the trend volume estimate for equipment, plant and machinery rose 0.7% in the March quarter 2015. Forward looking capital expenditure (a dodgy data set by definition) shows the same trend, mining falling away quicker then other part of the economy, including construction and manufacturing not filling the gap, so net trend is down.

The painful process of re balancing away from mining is unbalanced, and we do not think the gap will be closed by a combination of residential construction, and household spending. Further rate cuts won’t do much more to assist either. It is time for a concerted look at how to drive business harder, to make productive investments in future growth. This should be a time to drive public sector construction programmes harder. Otherwise, GDP will be weaker into 2017 than the budget base case suggests.

The painful process of re balancing away from mining is unbalanced, and we do not think the gap will be closed by a combination of residential construction, and household spending. Further rate cuts won’t do much more to assist either. It is time for a concerted look at how to drive business harder, to make productive investments in future growth. This should be a time to drive public sector construction programmes harder. Otherwise, GDP will be weaker into 2017 than the budget base case suggests.