The 50bp cut to the reserve requirement ratio (RRR) for Chinese banks on Tuesday, together with record loan growth in January, could point to an increasing likelihood that the authorities are shifting policy to enable more credit-fueled growth, says Fitch Ratings. Next week’s National People’s Congress meeting should provide further information on the direction of Chinese economic policy and structural reform. Fitch maintains that a return to sustained rapid lending growth by Chinese banks would be credit negative, with leverage in the economy already high.

Fitch expects that credit growth (based on Fitch’s Adjusted Measure of Total Social Financing, FATSF) will continue slowing in 2016, to 13%. This is a necessary part of the broader structural adjustment in China’s economy to achieve more sustainable growth. However, credit growth will still be running above nominal GDP growth, meaning that total leverage (as measured by FATSF/GDP) will continue to rise, to 260% by end-2016.

A government target, announced in October, to double the size of China’s economy by 2020 also implies continued credit-fueled growth as current consumption trends would not be able to support targeted GDP without additional leverage.

The People’s Bank of China (PBOC) lowered the RRR to 17%, effective on 1 March, and Fitch expects the move implies an injection of CNY688bn (USD105bn) of liquidity into the financial system. This was the first broad-based RRR cut since October, when the central bank also reduced the ratio by 50bp. The current level for the RRR is still high in both historical terms and in relation to other countries, so there could be room for further reductions this year.

This latest RRR cut is likely to be a reflection in part of the continued economic deceleration in China and ongoing concerns about growth risks. PMI data for February, released yesterday, showed a drop in manufacturing activity, with the index falling to 49 from 49.8 in January. This marked the lowest manufacturing PMI figure since February 2009. Notably, too, the services sector PMI fell to its lowest level since the 2008 global financial crisis, which could be signaling a broader-based slowdown.

In the near term, RRR cuts could boost bank earnings by allowing banks to reinvest the liquidity freed up from the PBOC. It will also enable banks to roll over more debt and continue the trend to shift loans back on balance sheet. However, Fitch expects that the overall earnings impact from the 50bp cut, or even the series of cuts enacted since the beginning of 2015, is not likely to be significant. Furthermore, rolling over more debt will only delay and not resolve an expected rise in NPLs. Fitch expects reported NPL and ‘special mention’ loan ratios to rise in 2016 to 2.5% and 4.3%, respectively, from 1.7% and 3.8% at end-2015.

Assume you’re a trader and your job involves buying and selling on the Shanghai/ Shenzhen stock exchanges. You’ve just returned to work from your 1 January New Year break. You’re feeling bearish for a number of reasons.

First, you know the six-month ban on selling shares imposed on major stock owners of Chinese companies will expire this Friday January 8. The ban was imposed following the stock market rout of early July 2015 that saw the mainland markets lose US$4 trillion in value. Its aim was to prevent major shareholders with more than 5% in mainland A-share companies from selling their stakes. The expiry of this ban will see a number of major new potential sellers entering the market as of next week, with some analysts predicting that over 1 trillion yuan of shares may be dumped.

Second, you know that a new rule introduced late in 2015, also in response to August volatility, will come into effect today, Monday January 4, the first trading day of 2016. The new rule introduces a circuit breaker for Chinese markets, under which all trading in stocks, index futures and options is suspended whenever the CSI 300 index falls or rises by 5%. If and when the index moves by 7%, all trading for the rest of the session is halted. This means you are aware that if the index begins to fall, you want to sell and get out quickly before trading is stopped and you lose your chance.

Third, you are aware that the Caixin Purchasing Managers’ Index (PMI) released on Sunday (January 2) fell to 48.2 in December, down from 48.6 in November, contracting for a 10th month in a row. China’s factories and manufacturing sector are key to the health of the world’s biggest economy. A PMI above 50 signals expansion, while anything below indicates a weakening economy.

Fourth, you are aware of the bigger, background economic picture: China’s economy grew at its slowest place since the 1990s in 2014 and stalled even further in 2015 as Beijing struggled to transform China’s investment and manufacturing driven growth model to a more sustainable consumption and services-based economy.

So you head to work on Monday with all this in your head and trading stumbles slowly into action over the morning session as traders exchange New Year pleasantries and absorb the market news. It’s not very long at all before it becomes very obvious that the CSI 300 is heading down, down – with little or no buying relief in sight.

So of course you join the exit selling rush before you lose your chance, and of course every other trader is doing exactly the same thing.

Small wonder then that by shortly after midday (at 1.12pm to be precise) the index has fallen by 5% – triggering the first circuit breaker and causing trading to be suspended for 15 minutes. This then triggers even more panic selling when trading resumes so that by 1.33pm the 7% trigger is reached and trading is halted for the rest of the day.

Chinese stock market investors have also been in for a wild ride.Kim Kyung Hoon/Reuters

Nothing to do with the fact that China has just landed a test flight on a new airfield on the disputed Spratly Islands. Nothing to do with the “disappearance” of people connected to a Hong Kong bookstore selling books critical of the mainland government. Just another bout of flu caused by the prevailing belief that if China’s factories sneeze, the world economy catches cold.

This time it’s combined with the new circuit breaker rule, which may itself have been a large part of the problem.

The Chinese circuit breaker is similar to one introduced in the US in 1988 following the “Black Monday” market plunge of October 1987, and also found in South Korea and India. The aim of circuit breaker rules is to provide time for a volatile market to cool, and for financial institutions and listed firms to release information allowing the market to stabilise around an agreed set of valuations. Circuit breakers also allow authorities to investigate any possible skulduggery (market manipulation) that may have caused unwanted downward volatility. But there are crucial differences between the US circuit breaker and the new Chinese rule.

First, the level at which the first circuit breaker trigger cuts in – a drop of 5% – is possibly too low for a market as volatile as China’s. Under the US system-wide circuit breaker rules as revised in 2012, the market halts for 15 minutes if the S&P 500 drops 7%, and then 13% before 3.25pm ET. A similar decline after 3.25pm will not halt trading. It needs a decline of 20% or more (regardless of when it occurs) to halt trading for the whole day.

Monday January 4 was the first day the Chinese circuit breaker went into effect. The speed at which the market fell from down 5% to down 7% (about two minutes) suggests that a more gradual and staged circuit breaker system could be more effective in stabilising China’s markets over the longer term.

The other thing that could, and probably will eventually serve to stabilise China’s markets over the longer term is to continue the process of linking the Chinese markets into other markets via “stock connect” schemes such as the Shanghai-Hong Kong stock connect launched in 2015. The stock connect remains limited to designated dual-listed A-shares, and has yet to be expanded to include bonds or other securities. Nor has the Shenzhen-Hong Kong stock connect, originally planned for late 2015, yet been launched.

The London Stock Exchange has agreed to study a possible link-up between it and the Shanghai Stock Exchange. Establishing and broadening such linkages would help connect China’s markets to those in the rest of the world and would put pressure on Chinese regulators to improve local operational mechanisms.

Author: Alice de Jonge, Senior Lecturer, International Law; Asian Business Law, Monash University

RBA’s Christopher Kent Assistant Governor (Economic) has been talking about China, and some of the implications for Australia. Commodity prices will remain under pressure, but the potential demand for services offers new export opportunities.

The easing in the growth of the Chinese economy over the past year or so has two related parts. The economy is slowing as it matures, and this is to be expected. Overlaying that, there has been a substantial slowing in the industrial sector, linked in part to earlier excesses in construction. How all of this will play out and the effects on the Australian economy are uncertain. I’ll briefly highlight some possibilities. Let me be clear though, many of these have positive implications for our economy.

It is natural for the speed of China’s economic development to ease and for its nature to evolve:

Part of this reflects slower growth of the working-age population, which is now in decline. Other than increasing the retirement age, there is little that can be done to alter that in the coming years, notwithstanding the ending of the one-child policy.

However, growth continues to be supported by the process of urbanisation, which uses commodities intensively. This has further to run, albeit at a more gradual pace.

Productivity growth appears to be slowing as windfall gains from earlier reforms have waned. But there remains a large gap between productivity in China and in advanced economies. That gap could be closed more quickly via additional reforms to allow a greater role for market forces in allocating productive resources. The authorities have expressed support for such reforms.

The authorities would also like to see growth rebalancing from investment towards consumption. That is happening gradually. It is also being accompanied by a rise in the share of activity accounted for by the services sector as the economy develops and household incomes rise.

While these longer-run changes imply a decline in the growth rates of investment and industrial production, both have also experienced a noticeable cyclical slowing over the past year or more. As earlier excesses in residential construction gave rise to a large stock of unsold housing, house prices declined and so too did housing construction. Sales and prices have recovered a bit since the start of this year, but there is little sign to date of a sustained improvement in construction activity.

Weakness in construction has been accompanied by declines in output of a range of manufactured products over the past year. Steel is one obvious example. Mining activity in China has also been affected. Indeed, a further decline in the output of unprofitable Chinese mines would provide some support to commodity prices, and would benefit other producers, including in Australia.

Although the weakness in China’s property and manufacturing sectors is clearly of concern to commodity exporters like Australia, there are a number of countervailing forces supporting broader activity in China.

First, growth in the services sector has been resilient, and should continue to be assisted by a shift in demand toward services as incomes rise.

Second, growth in household consumption has also been stable in recent quarters aided by the growth of new jobs. Of course, such outcomes cannot be taken for granted; if the industrial weakness is sustained, it might eventually affect household incomes and spending.

Third, Chinese policymakers have responded to lower growth by easing monetary policy and approving additional infrastructure investment projects. They have scope to provide further support if needed, although they may be reticent to do too much if that compromises longer-term goals, such as placing the financial system on a more sustainable footing.

There are two key implications of the slowing in China’s growth for Australia.

First, the substantial slowing in industrial production has contributed to a further decline in commodity prices over the course of this year. (This is in addition to the contribution from the substantial increase in the supply of commodities, including from Australia.) We’ve detailed the effect of the decline in commodity prices on Australia’s economy elsewhere. I would just add that commodity prices remain relatively high. The Bank’s index of commodity prices has fallen by about 50 per cent from its peak, but is still almost 80 per cent above early 2000 levels. Clearly, conditions in the industrial sector in China, and Asia more broadly, will have an important influence on the path of commodity prices over the near term. Beyond that, the changing nature of China’s development implies that the potential for commodity prices to rise from here is somewhat limited.

Second, the shift in demand towards services and agricultural products within China and the Asian region more broadly presents new opportunities for Australian exporters. While our comparative advantages in service industries are perhaps less obvious than they are for mineral resources, the rise in the demand for services from a large and increasingly wealthier populace in our region will no doubt be to our benefit.

Overnight, Chinese President Xi Jinping gave the strongest indication yet the country will revise down its economic growth goal to 6.5%.

The official target will not be known until China releases its highly anticipated 13th five-year plan in March next year, but play has already been made on the idea of the “economic new norm”. This means lower percentage rates of economic growth (although rates still high in international terms) coupled with structural economic reform.

Undoubtedly, the primary goal is to keep the economy growing strongly. The latest interest rate cut on October 30 was intended to stimulate the economy. As a result, the financial institution interest rate was reduced by 0.25% to 4.35%. This remains high by current international standards and leaves room for further significant cuts, a luxury not currently available in many economies.

The cut can hardly be considered a sign of economic desperation. It may have been prompted because last quarter’s GDP growth missed the 7% mark, but 6.5%, even allowing for the alleged suspect nature of Chinese economic statistics, is still a rate many economists consider consistent with the “transitioning” economy. Certainly percentage growth rates higher than these are unlikely to be seen again and growth is in fact sure to trend lower as China moves to become a developed economy.

The transition to a more consumer-based economy offers opportunities for private investors, especially given signs of official support for continuing economic liberalisation.

The services sector has grown to 52% of the country’s GDP, as opposed to 44 % in 2011. China now accounts for 34% of the world’s smart phone market, 12% of the diamond and high end jewellery market, and 18% of the online games market. But poorly developed financial markets are an impediment to investment. Accordingly, financial market reform is a matter of government concern.

The path of reform in the financial sector has proven to be difficult. The government is encouraging private capital to enter the banking sector via the privately-funded banks, but the sector remains dominated by government controlled banks. Credit provided by banks still makes up 90% of all financing.

Of course, from the perspective of lenders, financing state-owned or controlled entities (SOEs) involves less risk than financing small to medium enterprises (SMEs). One perceived problem with the economy is this lack of funding for SMEs, and naturally a goal of reform is to provide adequate credit for smaller organisations. There has been an attempt to promote private finance companies as an alternative source of credit to the state controlled bank lending markets.

The government’s overarching goal is to establish a multi-layered capital markets system including shares, debt, futures, and private equity markets. The objective is to allow markets to play a decisive role. But the continuing influence and position of the SOEs and their structure, in which the main shareholders remain local or central government authorities who exercise managerial control, makes this difficult.

Listed companies mostly remain SOEs, which need to be supported for political and social reasons, and these capture most of the credit available from the state dominated banking system and capital from risk averse investors. The protected position of SOEs discourages lenders from investing in places other than the banking sector, and in particular from supporting SMEs. The protected position of SOEs inevitably distorts the capital markets.

There has so far been little success in making SOEs more market responsive. This means further development of financial markets in China depends on the growth of credit companies, privately funded banks, and also the “third board” market, which focuses on SME listings.

Author: He Weiping, Lecturer in Law, Monash University

The UK has rolled out the red carpet for Chinese president Xi Jinping on his five-day official visit. He is being given the royal treatment, including a stay at Buckingham Palace, a ride in a state carriage along The Mall and several banquets. The trip will also include plenty of time with the British prime minister, David Cameron, who is keen to discuss the trade and investment that the UK hopes to secure from the visit.

Britain’s pivot to China is largely based on its economic strength. And yet there is cause for concern. Having been the locomotive for global growth following the financial crisis in 2008, Chinese growth has now slowed and its economy is looking increasingly fragile. The latest GDP figures came in at just under 7%, significantly down from the astounding annual rate of more than 9% per year between 1990 and 2010.

Exports from China have declined, and exports to China must battle against the depreciating yuan. China’s slowdown has depressed global commodity prices, adversely affecting big exporting countries such as Brazil and Russia.

Some leading economists have been very optimistic about China. Nobel Laureate Robert Fogel published an article in 2010 that predicted that China’s GDP will grow at an average annual rate of more than 8% until 2040, when its GDP per capita would be twice that projected for Europe and similar to that in the United States. Fogel used a textbook method of analysis to predict an unrelenting upward path.

But as countries grow, their service sectors tend to increase as a proportion of output and employment. Rates of growth of productivity in services tend to be much lower than in manufacturing or agriculture. Hence, in any economy, growth rates are likely to slow down through changes in economic structure. There are several other reasons why China’s economic growth is set to stall.

1. Demographic shifts

China will experience an adverse demographic shift in the coming decades. Three decades of the one-child policy has reduced the number of adults of working age. The recent and ongoing relaxation of that policy, plus a big decline in infant mortality, increases the number of children. Older people are living longer, due to improved healthcare and reduced poverty. Hence the average number of children and old people, which needs to be supported by each person in work, is set to increase dramatically.

GDP is way below that of the US and other developed countries. World Bank Figures for 2014 put China’s GDP per capita at about 24% of that in the US. In the 20th century, only five countries managed to grow from 24% or less of US GDP per capita to 60% or more of US GDP per capita. They were Japan, Taiwan, South Korea, Singapore and Hong Kong. China still has a long way to go.

3. Lack of democracy

While there is some evidence that autocratic governments can help economic development at lower stages of development, particularly by promoting basic industry and infrastructure, there is strong evidence that democratic institutions are much more suited to higher levels of development. Notably, when Japan, Taiwan and South Korea reached about 45% of US GDP per capita, they were established or emerging democracies. A transition to a more democratic government may be necessary as China develops, but this would be very difficult to achieve – and could be highly disruptive.

4. Lack of openness

A democratic government is but one part of a constellation of vital institutions. As Nobel Laureate Douglass North and his colleagues have argued, dynamic modern economies need checks, balances and countervailing power to minimise arbitrary confiscation by the state. Legal systems have to develop significant autonomy from the political elite. In my book Conceptualizing Capitalism I show that absolute GDP per capita in a sample of 97 countries is strongly correlated with absence of corruption and openness of government. China is not an outlier in this test.

5. Problems with land and property rights

Unrest in the Chinese village of Shangpu was triggered over an unpopular land deal.REUTERS/James Pomfret

China’s population is divided into two classes. Chinese citizens are registered with either an urban or rural classification, depending on where they are born. Urban registrants have better education and health services.

Many rural registrants, meanwhile, have rights to the use of land. But these are often anulled after local party officials are bribed by business speculators and sell the land for profit. Frequent local protests result and the whole system of land use is in dire need of radical reform. Currently it fosters corruption and inhibits the skill development of half of the Chinese population.

6. Lack of homegrown talent

Although there are many small firms in China, there are still few mainland-registered large firms. Barry Naughton has noted that of the top ten firms in China exporting high-tech products, nine were foreign. Offshore registration is understandable, because fear of state sequestration persists in a country that did not recognise private property rights in its constitution until 2007. China’s financial system is very heavily concentrated in state hands, with punitive penalties on private lending.

Thus, there are weighty institutional and demographic drags on further rapid growth in China, especially as it enters intermediate levels of economic development that are ill-suited to the continuance of a one-party state. China can succeed, but only through massive and potentially destabilising reform of its political and economic institutions. We should not be surprised by even lower growth rates in the future.

Author: Geoffrey M. Hodgson, Research Professor, Hertfordshire Business School, University of Hertfordshire

A Chinese “hard landing” would have a significant impact on global growth and economic stability, with economies in Asia and major emerging market commodities exporters among the hardest hit, says Fitch Ratings. Besides China itself, Hong Kong, Korea and Japan would be the most affected major economies in the event of a sharp slowdown in Chinese GDP growth.

Fitch’s base case forecasts China’s economy to expand by 6.8% and 6.3% in 2015 and 2016 respectively. But in the latest Global Economic Outlook report, Fitch assessed an alternative scenario in which China’s economic growth falls below 3% in 2016 driven by a collapse in public and private investment. Our assumptions in the shock scenario included a contraction in public investment of 4% in 2016 and deceleration in consumption growth to 5.6% in 2017 from 8.3% in 2014. This would result in asset-quality deterioration with a spike in the banking system NPL ratio to 8%, a cumulative 10% depreciation in CNY/USD, a double-digit percentage decrease in foreign direct investment and a peak to trough fall in home prices of over 4%.

According to the analysis, which used Oxford Economics’ global macroeconomic model, the impact would be greatest within Asia. The resulting decline in trade combined with the regional investment exposures to China would weigh most on the export-centred economies of Hong Kong and Korea, with the cumulative reduction in GDP from the 2017 baseline amounting to 4.5pp and 4.3pp respectively. Japan would enter a deep recession, with the economy contracting in both 2016 and 2017 and its GDP down by 3.6pp by 2017 versus our base case estimates. Taiwan and Singapore would also face significant slowdowns, though not as severe, with GDP falling by 3.3pp and 3.0pp from the baseline respectively.

GDP growth in the Association of Southeast Asian Nations (ASEAN) economies of Indonesia, Malaysia, Thailand and the Philippines would be less affected by the direct feedthroughs of a China hard landing, though they would still face a cumulative GDP effect of around -2pp.

Australia would be affected to a similar extent as the aforementioned ASEAN economies. Australia has large exposures through its direct trading relationship with China, but it would be able to offset some of the negative impact through counter-cyclical policy. As a ‘AAA’-rated developed economy, Australia benefits from sound fundamentals, which will help to stabilise the economy during a broader global downturn.

At the global level, a Chinese contraction would intensify deflation risks. This is especially the case for the euro zone, where demand has remained persistently weak and inflation low. That said, developed countries other than Japan would fare relatively better than their EM counterparts. Relative to the baseline, the cumulative effect on US and euro zone GDP would be -1.5pp and -1.7pp respectively, implying average annual growth rates of around 1.7% in the US and 0.8% in the euro zone for 2016-2017.

Major emerging markets outside Asia, especially the commodities exporters such as Brazil and Russia, would be doubly impacted by the effects on energy and materials prices and the risk premium shock that would raise borrowing costs and weigh on domestic demand. However, they would not be as heavily affected as the trade-reliant economies within Asia, with a Chinese hard landing likely to reduce GDP from the baseline by around 3pp for Brazil and 2.8pp for Russia.

According to FitchRatings latest in their Global Perspectives series, policy responses to sharp corrections in financial markets should be expected as the Chinese government adheres to a core principle of maintaining stability.

Much Western criticism of Chinese policy responses to the equity market sell-off as clumsy and ineffective misreads critical points on China. Common views expressed are that Chinese officials don’t fully understand how markets operate, are manipulating the market, or have not yet developed policy channels and tools that are sufficiently sophisticated and adept to affect the market.

Stability a Higher Priority than Market Principle

The easiest misconception to take issue with is that intervention by Chinese policymakers confirms a lack of market insight. Even casual observers of China in recent decades would recognise the increased role of foreign firms and private innovation and the diminished role of the state. State enterprises retain a dominant role in critical areas of the economy, but private enterprise and market-based solutions have been vital to the country’s rapid industrialisation and development.

But the Chinese authorities’ deep aversion to instability – broadly defined, including financial instability – means there are limits to their embrace of market-based principles. Although the equity market is small from a macroeconomic perspective, a period of free-fall would sit uncomfortably with a government that does not hide its desire to retain and control the status quo in so many other areas.

In this context, recent equity market interventions were less about denying market principles than about confirming a stronger preference for stability, and for the state to have a primary role in providing it. The preference for stability would have been better placed had it come prior to the equity bubble inflating, but the government actually had an active role last year in encouraging investment in the market. This provided even stronger motivation to intervene during the market correction.

Collective Policymaking and Possibly More Debt

Even if public opinion could be swayed, creditors may take the view that there is still the need for significant policy change in Greece, and that debt relief would simply address the consequences of previous shortcomings, not the root causes. Greece still needs to undertake major reforms to deliver sustainable public finances and more robust economic growth, and creditors may be reluctant to surrender the ongoing conditionality provided by support programmes that could be discontinued if there were wholesale debt forgiveness. The risk would be that Greek imbalances re-emerge, eventually threatening the viability of the eurozone again.The various policy responses to the decline in the equity market have two familiar features – they involve a large number of participants and there is likely to be a resulting increase in debt.

The “national team” of public institutions involved in providing direct and indirect support to the equity markets has been portrayed by some observers as disjointed and ineffectual, primarily because there were several initiatives announced to which there was little or no market response. In addition, it has been argued that with so many institutions involved, including the Ministry of Finance and the People’s Bank of China (PBOC), none took a clear lead or stood out as having the credibility or authority to single-handedly sway the markets in the way that the Federal Reserve and European Central Bank were able to during episodes of stress in their markets.

But this misses the point that China’s patchwork of financial supervision and regulation is consistent with a deliberately diffused policy framework. This arrangement is in place not because a consensus-driven approach to decision-making is favoured – in fact, in some cases responsibilities are overlapping and initiatives at cross-purposes. Instead, policy diffusion is intended to ensure that state organisations operate collectively under the ultimate guidance of the country’s political leaders. As such, China’s authorities are unlikely to conclude from criticisms of the “national team” that they need a Greenspan or a Draghi to personify economic influence and authority. It is equally unlikely that there will be a regulatory overhaul to raise one institution to a coordinating “super-regulator”, as has been proposed by some foreign observers.

Just as the equity market was egged higher during its upswing in part by increases in debt – specifically via margin and peer-to-peer lending – elements of the policy responses to the downturn are also likely to raise debt levels. In July the China Securities Regulatory Commission (CSRC) relaxed some margin lending requirements of brokers, reversing a trend towards tightening earlier this year. The CSRC is also reported to have extended credit of RNB260bn to brokers, with funding from the bond market, banks and liquidity provided by the PBOC. Additionally, the China Banking Regulatory Commission has allowed banks to take a more flexible approach to corporate loans collateralised by equities, and has encouraged them to lend to listed companies engaged in stock buy-backs and to the CSRC.

The specific equity market initiatives that may increase debt should not be interpreted as a change in policy direction, as one of the authorities’ overriding objectives remains a reduction of indebtedness in the economy. The risks of potential solvency problems at current debt levels have been central to the acceptance and adoption of lower economic growth targets. But, as with other immediate policy challenges in China, the authorities see a further build-up in debt as a reliable – and presumably short-term – solution.

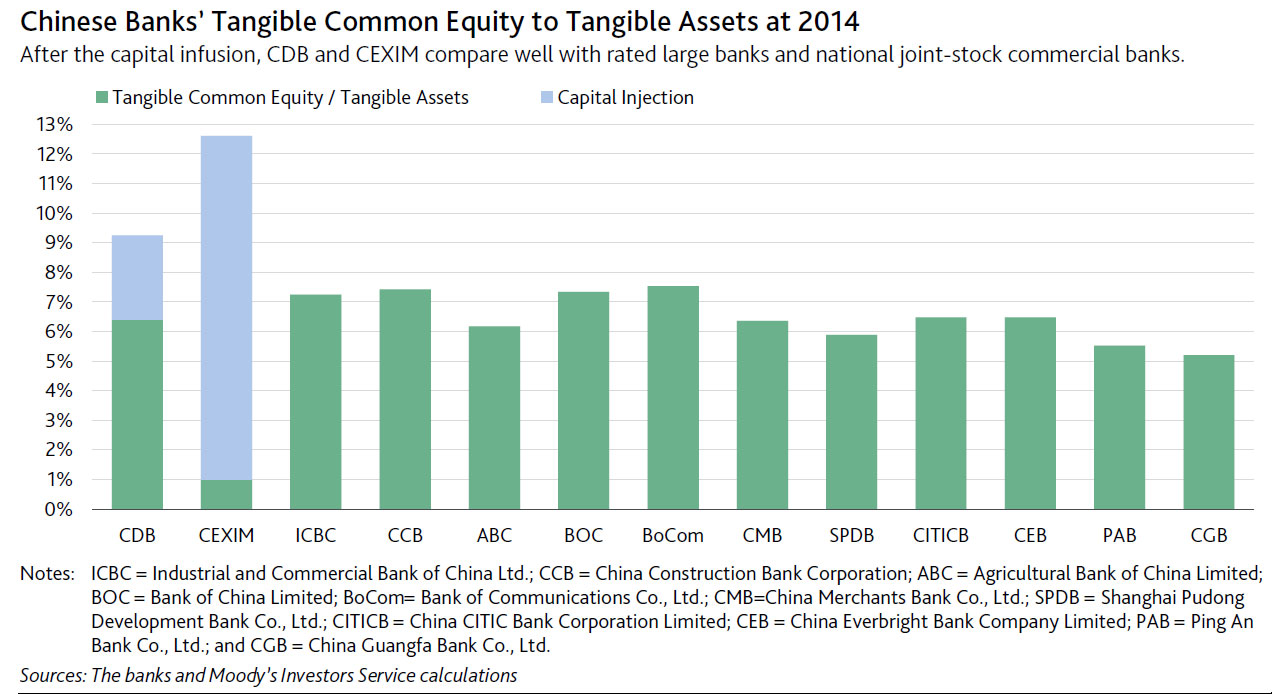

In a research note Moody’s says that last Tuesday, China’s official Xinhua News Agency reported that the People’s Bank of China (PBOC) had injected $48 billion of equity capital into China Development Bank Corporation and $45 billion into The Export-Import Bank of China (CEXIM).

The injections were made through Wutongshu Investment Platform Co. Ltd., an entity that invests China’s foreign currency reserves. The massive equity infusions are credit positive for CDB and CEXIM. CDB’s capital adequacy ratio rises to about 11.8% from 9.1% under Basel III at year-end 2014, while CEXIM’s capital adequacy ratio, which it does not disclose, rises significantly. The injections also add to both banks’ loss-absorption capacity. Against the backdrop of heightened asset-quality risks at domestic banks, we think the enhanced loss-absorption implies that regulators are likely to impose minimum capital requirements on the banks.

The capital infusions are consistent with the Chinese government’s goal to strengthen Chinese policy lenders’ capital positions. After the injections, both banks’ ratios of tangible common equity to tangible assets compare well with those of the rated Chinese large and national joint-stock commercial banks.

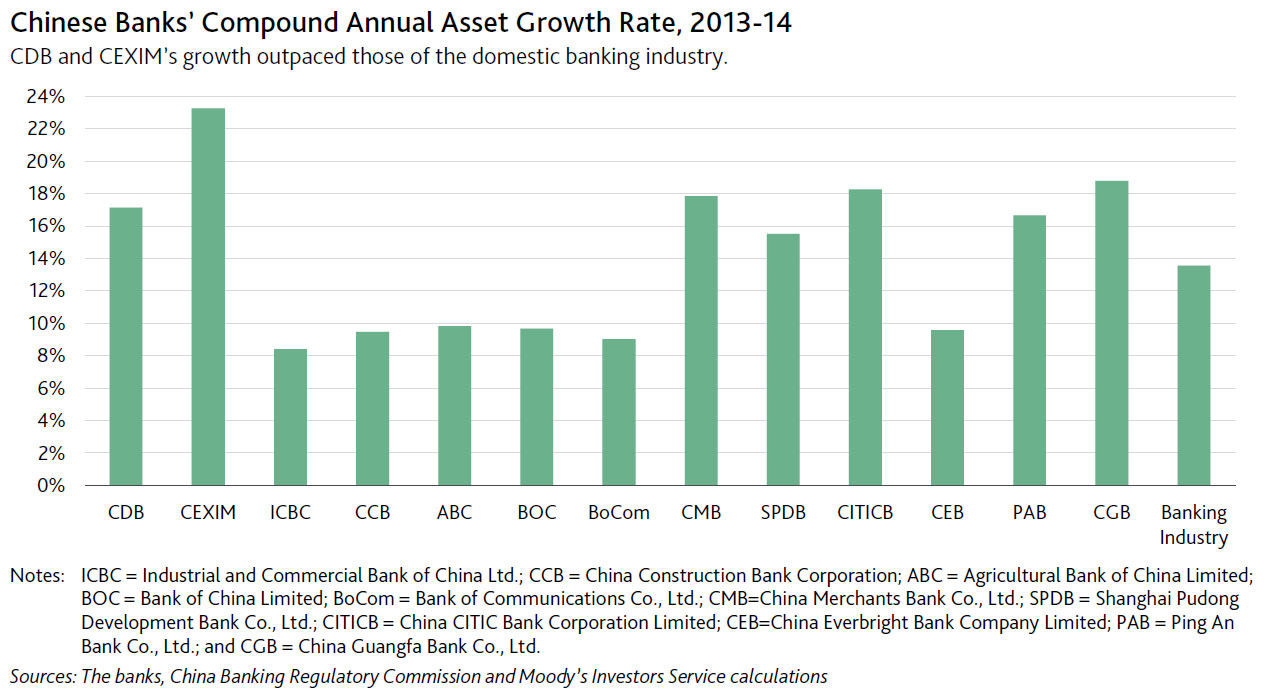

In the past several years, CDB and CEXIM have taken on key roles as policy-driven banks in financing priority projects and supporting the growth of Chinese corporates expanding overseas. For 2013-14, CDB’s compound annual asset growth rate was 17.1% and CEXIM’s 23.2%, compared with an average 13.6% rate for the Chinese banking industry during the same period

The capital injections demonstrate the Chinese government’s strong commitment to support the two lenders, whose policy roles are increasingly important for stimulating domestic economic growth. CDB and CEXIM are likely to take on greater credit exposure and their lending may have a greater strategic rationale rather than an economic one. For instance, the additional capital should facilitate CDB and CEXIM financing of overseas projects that are part of China’s One Belt, One Road initiative to boost infrastructure and economic connectivity across Eurasia.

Our assumption of a very high level of government support for CDB and CEXIM’s reflects strong government backing to offset their greater risks, given the two banks’ strategic importance as agents of the Chinese government in the implementation of development initiatives.

The Financial Stability Board (FSB) published today its peer review of China. The review concludes that the authorities have made good progress in addressing the FSAP recommendations on both topics, but that there is additional work to be done. A unifying theme behind the findings and recommendations is the need for closer coordination and information sharing between the authorities to handle a dynamic financial system. The report published today describes the findings and conclusions of the peer review of China. The draft report was prepared by a team of experts drawn from FSB member institutions and led by Jon Cunliffe, Deputy Governor of the Bank of England.

The peer review examined two topics relevant for financial stability and important for China: the macroprudential management framework and non-bank credit intermediation. The review focused on the steps taken by the authorities to implement reforms in these areas, including by following up on relevant recommendations in the 2011 Financial Sector Assessment Program (FSAP) report by the International Monetary Fund (IMF) and the World Bank.

The peer review concludes that the authorities have made good progress in addressing the FSAP recommendations on both topics, but that there is additional work to be done. A unifying theme behind the peer review findings and recommendations (see below) is the need for closer coordination and information sharing between the authorities to handle a dynamic financial system. Enhancing inter-agency coordination and developing an integrated risk assessment framework will promote a common understanding of objectives and risks, which will in turn facilitate joint policy actions and public communication.

In particular, the peer review found that the People’s Bank of China and financial sector regulatory agencies (China Banking Regulatory Commission, China Securities Regulatory Commission and China Insurance Regulatory Commission) have made important strides in developing a macroprudential management framework. Notable achievements include the elaboration of monitoring frameworks and toolkits by each agency to assess systemic risk in the sectors under their respective mandates; data improvements and ongoing work to develop a shared statistical platform; and enhanced inter-agency coordination through the Financial Crisis Response Group directly under the State Council and the Financial Regulatory Coordination Joint Ministerial Committee (JMC). Importantly, the authorities have a broad range of tools that can be used for macroprudential purposes, and have deployed them frequently in response to economic and financial system developments.

Building on what has been done to date, and as is being grappled with in many jurisdictions, additional work is needed to flesh out and operationalise a comprehensive and coordinated macroprudential policy framework. The peer review recommends:

Clarifying the mandate and roles of different inter-agency bodies in assessing systemic risks and designing macroprudential policies, and strengthening the supporting infrastructure accordingly.

Further developing an integrated systemic risk assessment framework that incorporates the views of different agencies and takes into account cross-sectoral policy interactions and implications for the overall stance of macroprudential policy.

Developing an inter-agency protocol specifically for financial stability monitoring/assessment and related information sharing, based on the respective role of each authority in the macroprudential policy framework.

Publishing the outcome of key inter-agency meetings and deliberations periodically as a means of communicating the authorities’ macroprudential outlook and policy stance.

Non-bank credit intermediation has accounted for an increasing proportion of funding to the Chinese economy – around 20% of new financing flows over the period 2012-14 – although the most recent figures indicate that its growth has moderated. The peer review found that the authorities have improved their monitoring of non-bank credit intermediation in recent years and have taken steps to contain identified risks. Specific examples include the augmentation of data collection, enhanced cooperation between the authorities via the JMC, and policy actions to mitigate identified risks related to the interbank market, the trust sector and banks’ wealth management products.

Notwithstanding these accomplishments, challenges remain in assessing and mitigating emerging risks in this sector – both in terms of data collection and, more importantly, in terms of undertaking coordinated and comprehensive risk assessments to inform the use of policy tools. This is not unique to China, as many other jurisdictions are in the process of improving their monitoring and developing policy tools to ensure that non-bank activities develop into a transparent, resilient and sustainable source of market-based financing. The peer review recommends that the authorities:

Continue to enhance efforts to collect and disclose comprehensive and granular data relating to non-bank credit intermediation (e.g. on various forms of wealth and asset management products), and routinely share them for risk monitoring purposes.

Enhance their ability to assess systemic risks stemming from non-bank credit intermediation by extending the analytical framework to focus on the liquidity, maturity transformation, credit and reputational risks for banks stemming from these products, the impact of second-round effects, and the use of crisis simulation exercises.

Develop a more activity-based regulatory approach in order to discourage regulatory arbitrage and ensure a level playing field in non-bank credit intermediation.

Continue to promote a more diversified and resilient financial system by increasing reliance on market-based pricing mechanisms via the removal of implicit guarantees, and by further developing capital markets and an institutional investor base as an alternative pillar to bank financing.

The Chinese stock markets have experienced significant turmoil in recent weeks, with the Shanghai Composite Index – the country’s major reference – falling by 32% since June 12. But this fall was preceded by an equally sharp rise of 150% over the previous nine months. In the 20 years since I have been working in finance, I’ve never seen anything like this. So what is going on with the Chinese stock market?

There are several reasons for this unusual behaviour: firstly, when I teach stock market investment to my Chinese students, I always remind them that the Shanghai stock exchange should be thought of more as a casino, rather than as a proper stock market. In normal stock markets, share prices are – or, at least, should be – linked to the economic performance of the underlying companies. Not so in China, where the popularity of the stock market directly correlated with the fall in casino popularity.

Stocks and casinos

In China, given the low credibility of the financial statements published by listed companies, investors need to rely on other tools to predict share price performance. These tools include a heavy reliance on technical analysis and charts – a method that tends to predict future share price based purely on the company’s past performance, with no regards to its fundamentals. Even the name of the company is often neglected; all that matters is the historic price performance.

While this technique is also used in Western markets, my experience in China is that it is the predominant method for investment. Hence the disconnect between a share’s price movements and economic fundamentals.

There has been, however, a strong correlation between the stock market’s performance and the revenues of the casinos in Macau. While gambling revenues were growing at a fast pace in Macau, people largely ignored the stock market – whose performance was, largely, uninteresting for a number of years. But since China’s president, Xi Jinping, launched a campaign against corruption, gambling activity has started to decline. This was when the stock market started to move up. Coincidence?

Real estate

The other reason why the stock market experienced a sharp increase between September 2014 and June 2015 relates to the Chinese real estate market. In recent years, investment in real estate has been the only way for ordinary citizens to get returns higher than the paltry 3% offered by bank deposits (yes, 3% is paltry in an economy that grows at more than 10% a year in nominal terms). But high capital requirements and growing regulations on the purchase of real estate has meant that benefiting from this growing market has been increasingly difficult for ordinary citizens.

Macau: the traditional home of Chinese gambling.Shutterstock

Commercial banks therefore – in an effort to mimic real-estate returns – started to offer so-called “wealth management products”, which are basically funds that invest in the real estate market. These funds were then repackaged and resold in the retail market. Chinese individuals would take their savings out of current accounts and placed them into these wealth management products and achieve returns similar to those available to buyers of real estate.

This was the modus operandi until the beginning of 2014, at which point the economy and the real estate markets started to show signs of weakness. The once-easy money coming from the property market started to disappear and people with wealth management products started to get into financial trouble and some of them even defaulted on their payments (the government bailed them out, so no individual was at a loss).

Monetary policy

From November 2014 the Chinese central bank, worried about the slowing economy, decided to institute an aggressive monetary policy to rapidly lower interest rates with the aim of stimulating the economy, which also caused current account rates to decline. This created a perverse scenario where individuals who were already seeking returns higher than those offered by current accounts were then denied the opportunity to get them through real estate because of the falling market. As a result, deposit rates were cut further and the return on current accounts became even more dissatisfying. Commercial banks found themselves in a quandary.

The Shanghai Composite Index’s growth and decline in recent months.Yahoo finance

With the casino route closed and real estate off the table, what was left? The Shanghai and Shenzhen stock markets: the two main stock markets that had remained dormant for years.

Banks then turned the old real estate wealth management products into investment vehicles to purchase shares directly on the stock markets. A large portion of customer deposits were then directly invested in the stock market, which then surged on the back of that demand.

An empty bubble?

Meanwhile, however, nothing happened to the earnings forecasts of the underlying companies. In fact, if anything, they should have been revised down because of the deteriorating macroeconomic condition of the Chinese domestic economy. But of course, as we said before, no one really looks at earnings and price ratios.

Due to the desire to maximise returns, many individuals then used leverage so that the inflow of money in the stock market was even higher. For example, if someone wishes to purchase shares for a total value of 100RMB, but only has available cash in his deposit account of, say, 60RMB, he could borrow the remaining 40RMB from the brokerage house. By doing this, the original source of 60RMB was turned into an upward push of the stock price equivalent to the full 100RMB. This drove strong share price growth between September 2014 and June 12 2015.

What happened on June 12 2015? Nothing. Just some smarter investors (generally large institutional investors, which represent 20% of all market volumes) started to sell and the rest of the market followed suit. Fear got hold of small investors (who represent 80% of the market) and selling accelerated, with margin calls making those selling do so even faster, and here we are today – a 32% drop and counting since the peak of mid-June.

In the past few days, the Chinese government has adopted a number of measures to try to mitigate this crash. The market finally reacted positively to a relaxation of restrictions on margin requirements. But this measure simply transfers the risks from investors to brokerage houses – it does not change the fact that the market has increased by 70% over the last year. The bubble, if it is a bubble, still has a long way to go.

Author: Michele Geraci, Head of China Economic Policy Programme, Assistant Professor in Finance at University of Nottingham