Moody’s says on 23 November, the China Banking Regulatory Commission (CBRC) published a consultation paper that aims to tighten regulations for commercial banks’ off-balance-sheet activities, which have grown rapidly in recent years. If implemented, these measures would be credit positive because they would reduce risks in the banking system and curtail incentives to engage in the regulatory arbitrage that has accelerated the growth of China’s shadow banking activities.

The proposed guidelines provide a more comprehensive set of definitions for off-balance-sheet exposures to better capture the latest innovations. When the CBRC formulated the current regulations in 2011, they mainly addressed the guarantee and commitment businesses. The new rule will expand to include entrusted services (which includes entrusted loans and investment, non-guaranteed wealth-management products, agency transactions, agency issues and bond underwriting) and intermediary services (including agency collection and payments, financial advisory and asset custody). These new services have grown rapidly in recent years, raising concerns about the expansion of China’s shadow banking system.

We estimate that the shadow banking sector grew by an annualized rate of 19% in the first half of 2016 to RMB58.3 trillion, or 80% of GDP, fueled predominately by the issuance of wealth management products. A China Banking Wealth Management Registration System report showed that RMB20.18 trillion of the RMB26.28 trillion of outstanding wealth management products at the end of June 2016 were non-guaranteed products usually kept off the balance sheet of the originating or distributing bank. By remaining off balance sheet, banks have been able to circumvent regulations on loan quotas and limits and dodge capital and provision requirements.

The proposed new guidelines require banks to set provisions on impairment losses on off-balance-sheet assets and retain risk-based capital on such assets. Although many wealth management products are off balance sheet, customers perceive banks as having provided an implicit guarantee for these products. The new rule would increase regulatory capital requirements that better capture banks’ actual credit risk.

The revised guidelines also ask for more detailed disclosure and more robust risk management of off-balance-sheet exposures, and banks would have to establish risk limits for off-balance-sheet exposures. Although the People’s Bank of China plans to include off-balance-sheet items in its macro-prudential assessment and the CBRC in July issued new draft rules on banks’ wealth management products, the new proposal offers a more comprehensive regulatory framework and complements other measures already in effect. The tighter rules will help contain off-balance-sheet risks and improve financial system transparency.

Banks with higher off-balance-sheet exposures will be most affected by the new regulation. Small and midsize banks will likely be most affected by the revised measures because they have been the more active issuers of wealth management products, which at some banks have become a key revenue source.

Although the revised rules focus on general risk-management principles, they fall short in providing details on actual execution, and leave a few key questions unanswered. For example, it remains unclear which off-balance-sheet assets’ credit risks are deemed retained by the banks themselves. Also lacking are specifics about the supervision for the risk conversion factor of off-balance-sheet assets or any details on the level of capital and reserves required. Additionally, a lack of uniformity across banks remains because banks’ boards of directors are responsible for approving off-balance-sheet business, risk management and imposing risk limits. Consequently, implementation by each bank will vary.

Donald Trump’s presidency won’t hurt the rising tide of Chinese investment into the United States – in fact, the level of cash may actually increase, according to Knight Frank.

Trump’s shock election last week rattled markets around the world and analysts continue to disagree on what the Republican candidate’s victory means or how it will affect the US property market, the No 1 destination for Chinese capital. “The short answer is I am not worried about Trump’s impact on Chinese flows into America,” Knight Frank’s global capital markets head Peter MacColl told the Post during a visit to Hong Kong last week.

“Whilst he’s come out with a lot of rhetoric, what might be considered to be barmy ideas that might have an impact on the geopolitical scene globally, the American system of checks and balances through Congress, through all the advisory parties that any change has to go through, means any really radical things won’t happen overnight,” he said.

“I don’t think there will be a big downturn in the property market because of Trump, and if anything, there could be a bit of an upturn because of his policies towards business generation and self responsibility.”

In the short term, MacColl expects there to be a bit of “waiting in the wings and seeing what’s going to happen”.

“A bit of caution, a bit of a slowdown just in terms of making decisions – which is understandable – until maybe the new year when things start to pan out a bit.”

But MacColl said he didn’t see a lot of risk to mainland Chinese investors in the US from Trump’s presidency and expected the US to remain the favoured destination for Chinese capital.

There wasn’t just a pull factor, there was also a push factor, with Chinese investors keen to take their money out of the country as the yuan continued to be devalued, he said.

The total volume of Chinese outbound real estate investment between January and October is slightly down on the same period last year, according to Knight Frank research.

But not everyone was so positive. Jefferies equity analyst Mike Prew said the combination of a possible post-election Federal Reserve rate rise in December and rising bond yields compared with property yields could have an effect on the returns in the US’s $27 trillion residential market.

“Things could get messy for real estate,” he said.

He tipped Canadian residential markets of Toronto, Montreal and Vancouver to be the big property winners following the US election.

Simon Smith, head of research and consultancy for Savills, agreed that investors would stay cautious for the rest of this year and capital volumes might be more muted.

“The uncertainty continues to drive people to the United Kingdom,” he said, noting that Brexit had also worked out positively for the British property market thanks to the falling pound – something which hadn’t happened to the US dollar. “It looks like the UK remains a net beneficiary of what’s been happening.”

Trump’s indication that he would invest in infrastructure was judged as positive by investors, but question marks remain over the wider policy direction of his presidency.

“I don’t think the clouds have parted quite yet on Trump and what election promises he may or may not choose to enact. We’re still asking ourselves: is this soft Trump or hard Trump?”

New York real estate company CityRealty’s director of research Gabby Warshawer said it was difficult to predict the long-term implications of Trump’s presidency on New York property,

which was the top destination for Chinese capital investment in the first six months of this year.

“If the stock market were to be extremely unsettled for a long period of time, that would have a clear effect on real estate — for example, following the financial crisis in late 2008, it took more than three years for New York real estate prices and sales volume to bounce back,” she said in an emailed response to questions from the Post.

“That being said, analysts have not been predicting a protracted doomsday scenario for the markets following this election.”

She said it was unlikely there would be significant change in Chinese investment following the election as the buying spree had a lot to do with property market conditions in China.

“If there is significant turmoil and the United States is no longer considered as safe for real estate investments as it has been in recent years, then that would impact all international buyers,” Warshawer said.“The New York City real estate market is stable and exceptional enough that it is still generally seen as a safe long and medium-term investment by most buyers, regardless of campaign rhetoric.”

In a speech by Norman T L Chan, Chief Executive of the Hong Kong Monetary Authority, at HKMA Fintech Day, Hong Kong, in November 2016, he gave a run down on how HKMA is approaching the disruptive revolution via the Fintech Facilitation Office (FFO) which was set up in March, to build an ecosystem to promote the adoption of new technologies in the banking sector; and also discusses four Fintech projects currently in hand. The Hong Kong Monetary Authority is Hong Kong’s currency board and de facto central bank. It is a government authority founded on 1 April 1993.

The event today is organized by the Fintech Facilitation Office (FFO) of the HKMA together with our three strategic partners: the Applied Science and Technology Research Institute (ASTRI), Cyberport and the Hong Kong Science and Technology Parks (the Science Park). As you are aware, we set up the FFO in March this year with the mission to facilitate the development of fintech in Hong Kong.

In the last few months, the FFO has organized many activities to bring together users and solution providers of fintech, so as to build an ecosystem to promote the adoption of new technologies in the banking sector. The FFO will continue to develop this collaborative platform together with ASTRI, Cyberport and the Science Park. In a few moments the HKMA will be signing a Memorandum of Understanding with each of them to formalize the framework of cooperation.

Now I would like to report on the latest progress of four major fintech projects launched by the FFO earlier. First, following my announcement of the launch of the Cybersecurity Fortification Initiative (CFI) in May, the FFO has been making very good progress in developing the three pillars of the CFI. A three month industry consultation of the first pillar of CFI, the Cybersecurity Resilience Assessment Programme, was completed in August, with positive responses from the banking sector. Taking into account the comments received, the FFO is finalising the Assessment Programme and will announce the detailed framework next month for implementation by banks in Hong Kong. Regarding the second pillar of the CFI, the Cybersecurity Intelligence Sharing Platform, again good progress is being made. The computer platform will be in operation and available to the banking sector next month as planned. The last pillar of the CFI is the Professional Development Programme, a training and certification programme for the cybersecurity professionals. A six-week consultation with the cybersecurity professionals and industry associations was conducted in the summer. The industry in general welcomes the programme and has suggested the need to recognise certain equivalent qualifications in the market for conducting the cybersecurity assessment and testing. We agree with this suggestion, and have already formed an industry expert panel with the task of identifying equivalent qualifications and working out the implementation details. The programme will be rolled out next month as planned. All in all, with the support of the banking industry and the stakeholders, the CFI implementation is on track and on time.

Second, the HKMA has commissioned ASTRI to carry out a comprehensive study on distributed ledger technology (DLT). The very fact that DLT allows information or records to be transferred and updated by network participants in a trustworthy, secure and efficient way, carries enormous potential in its application. However, while the value proposition of DLT is gradually crystallising, the use of DLT in financial services may bring about new risks and challenges in its application. As a regulatory authority, the HKMA needs to have a better understanding of these issues before DLT can be adopted for wide application in the banking sector.

In this connection, I am pleased to announce that the first stage of this research project is completed and a white paper is published by ASTRI today. While the white paper affirms the good potential of DLT for application in financial services, it also highlights a number of possible issues which need to be carefully dealt with if DLT is adopted by the banking sector. For example, the decentralised model may pose some challenges for constructing an effective governance structure and oversight mechanism. Some legal issues have yet to be thoroughly examined, such as the application and enforceability of laws for the cross-border DLT models, mechanisms for handling liability and dispute resolution if there is no centralised party administrating the DLT platform, and compliance with personal data protection principles in relation to data sharing and perpetual storage. Also, traditional cybersecurity issues still apply to DLT, including denial of access attacks and other cyber attacks.

The next stage of ASTRI’s study will deliver more detailed findings from a number of the proof-of-concept trials, along with assessment on whether some of this work can be put into action. It will also address the regulatory implications of DLT, and the general control principles for DLT for the banking and payment industry. We plan to deliver the next set of results in the form of another white paper in the second half of 2017.

Third, as I announced in September, we are setting up the HKMA-ASTRI Fintech Innovation Hub. I am now pleased to say that, following intensive preparation, the Hub is ready for use as from today. The Hub is equipped with high-powered computing resources and supported by the experts at ASTRI to allow banks, payment service providers, fintech firms and the HKMA to brainstorm innovative ideas, try out and evaluate new fintech solutions in a safe and efficient manner. All in all, the Hub will cater for the big and small institutions alike in supporting their research and adoption of fintech.

Last but not least, the HKMA launched the Fintech Supervisory Sandbox in September in order to create a regulatory environment that is conducive to fintech development. The Sandbox enables banks to conduct pilot trials of their fintech initiatives in a controlled production environment without the need to achieve full compliance with the HKMA’s usual supervisory requirements. So far, two banks have already made use of the Sandbox to conduct pilot trials of their biometric authentication and securities trading services. A few banks are discussing with us and planning to make use of the Sandbox for conducting their project trials in the coming few months, in areas such as blockchain, artificial intelligence and many more.

In parallel to all these fintech projects that the FFO has launched, the HKMA has issued 13 Stored Value Facilities licences in two batches under the newly established regulatory regime. These licensees range from mobile and Internet payment service providers to prepaid card issuers. As payment and SVF operators are important stakeholders in the fintech ecosystem, we have also invited five of the SVF licensees to join today’s event and share their experience in relation to the latest e-payment developments in Hong Kong.

Globalisation has opened up property markets around the world, with cashed up investors from China in the market snapping up overseas homes at an accelerating pace. They’re also venturing further afield than ever before, spreading beyond the likes of Sydney and Vancouver to lower-priced markets including Houston, Thailand’s Pattaya Beach and Malaysia’s Johor Bahru; according to Bloomberg.

If they were anywhere else in Beijing, the five young women in cowboy hats and matching red, white, and blue costumes would look wildly out of place.

But here at the city’s biggest international property fair — a frenetic gathering of brokers, developers and other real estate professionals all jockeying for the attention of Chinese buyers — the quintet of wannabe Texans fits right in. As they promote Houston townhouses (“Yours for as little as $350,000!”), a Portugal contingent touts its Golden Visa program and the Australian delegation lures passersby with stuffed kangaroos.

Welcome to ground zero for the world’s largest cross-border residential property boom. Motivated by a weakening yuan, surging domestic housing costs and the desire to secure offshore footholds, Chinese citizens are snapping up overseas homes at an accelerating pace. They’re also venturing further afield than ever before, spreading beyond the likes of Sydney and Vancouver to lower-priced markets including Houston, Thailand’s Pattaya Beach and Malaysia’s Johor Bahru.

The buying spree has defied Chinese government efforts to restrict capital outflows and shows little sign of slowing after an estimated $15 billion of overseas real estate purchases in the first half. For cities in the cross-hairs, the challenge is to balance the economic benefits of Chinese demand against the risk that rising home prices spur a public backlash.

“The Chinese have managed to accumulate very large amounts of wealth, and the opportunities to deploy that capital in their own market are somewhat restricted,” said Richard Barkham, the London-based chief global economist at CBRE Group Inc., the world’s largest commercial property brokerage. “China has more than a billion people. Personally, I think we have just seen a trickle.”

While a dearth of government statistics makes it difficult to gain a comprehensive view of cross-border real estate investments, most industry projections point to a surge in Chinese purchases. Ping An Haofang, an online real estate platform owned by China’s second-largest insurer, says its $15 billion first-half estimate, derived from market data, nearly matches the figure for all of 2015.

Fang Holdings Ltd., the country’s most popular property website, predicts overseas buying on its system will increase 130 percent this year, while transactions through September at Shenzhen World Union Properties Consultancy Inc., China’s largest broker for new-home sales, were already 50 percent above last year’s level. The country overtook Canada as the largest source of residential purchases in America last year after an estimated $93 billion of buying from 2010 to 2015, according to a May report by the Asia Society and Rosen Consulting Group.

It adds up to the world’s biggest-ever wave of overseas residential property investment, according to Susan Wachter, a professor at the University of Pennsylvania’s Wharton School who specializes in real estate markets. While Japan had a similar boom in the 1980s, it was mainly focused on commercial buildings, Wachter said.

Today’s Chinese buyers have a long list of reasons to flock overseas. The yuan’s slump is eroding their purchasing power, while returns on local financial assets — including stocks, bonds and wealth-management products — are shrinking as the $11 trillion economy slows.

Chinese real estate, meanwhile, has grown increasingly out of reach after a speculative boom sent domestic home prices to all-time highs. Residential property values in Shenzhen, Beijing and Shanghai all jumped more than 30 percent in the year through September, according to the National Bureau of Statistics.

“Properties in Shanghai are ridiculously expensive,” Chen Feng, 38, said as he evaluated prospects at a property fair in Shanghai in September, lured by television commercials for the event the night before. “With the amount of money it takes to buy a small apartment here, I can buy a building of apartments in many places in the world.”

That line of reasoning is nothing new, of course. Sydney, Vancouver, Hong Kong, London and a handful of other cities have long been popular destinations for Chinese buyers.

The difference now is that those traditional hotspots are starting to lose their appeal, due to soaring prices and new measures to deter an influx of overseas money. In Hong Kong, the government enacted a 30 percent tax on foreign property owners this month after Chinese demand pushed home values toward record highs.

The risk of similar measures in other cities can’t be ruled out as politicians including Donald Trump, the U.S. president-elect, tap into local discontent over rising living costs, according to CBRE Group’s Barkham.

Ocean Views

Chinese buyers have responded by branching out to cheaper cities. In the U.S., they’re increasingly searching for properties in Houston, Orlando and Seattle, which displaced San Francisco in the first quarter as the third-most viewed U.S. market on Juwai.com, a Chinese search engine for offshore real estate.

At the national level, countries in Southeast Asia have grown more popular. Juwai.com’s queries on Thailand are surging at a 72 percent annual rate, helping it surpass Britain as one of the top five most-targeted destinations worldwide earlier this year.

In Pattaya Beach, Chinese investors have snapped up 20 percent of the luxury condos on offer from Kingdom Property Co. over the past year. The properties offer Gulf of Thailand views for as little as $120,000, or less than a quarter of what buyers would pay for a typical apartment in central Shanghai, according to Han Bing, a 30-year-old anchor in Chinese television shows who doubles as a sales agent for the Bangkok-based developer.

“It’s a cool bargain for a retirement plan,” Han said.

Capital Controls

In the Malaysian state of Johor, across the Northern border of Singapore, major Chinese builders including Country Garden Holdings Co., Greenland Holdings Corp. and Guangzhou R&F Properties Co. are all developing new projects. Country Garden agents handed out fliers for the firm’s $37 billion Forest City development at the Beijing property fair in September, advertising permanent property rights, zero inheritance taxes, long-term residence visas and high-quality hospitals.

One challenge for Chinese investors is getting money out of a country that caps individuals’ foreign-currency purchases at $50,000 a year. While that limit hasn’t always been strictly enforced, the yuan’s slump is prompting policy makers to clamp down. This year, they’ve banned the use of friends’ currency quotas, curbed on the cross-border activities of underground banks and asked lenders to reduce foreign-exchange sales.Still, alternative routes abound. Many business owners finance their homes through offshore trading companies, while some Chinese developers allow clients to pay for overseas units in yuan. Foreign-currency mortgages also play a role, helping to fund more than 80 percent of China’s international property purchases, according to an estimate by Fang Holdings based on user searches and surveys.

Planning Ahead

“Where there’s a will, there’s a way,” said David Ley, a professor at the University of British Columbia who wrote a book on the flood of wealthy migrants from east Asia in the 1980s and 1990s.

This year’s purchases could be just be the tip of the iceberg. Chinese holdings of global real estate, including commercial properties, will probably swell to $220 billion by 2020 from $80 billion in 2015, according to Juwai.com.

As the first generation born after China’s opening in the late 1970s approaches middle age, many of them want an overseas base for family members to travel, study and work. Chinese parents with children at foreign schools have been a major source of demand, accounting for an estimated 45 percent of cross-border buying, according to Fang Holdings.

Zha Liangliang, a 31-year-old owner of commercial wheat farms in China’s eastern Jiangsu province, said he purchased a $587,000 apartment in Sydney in August and plans to add five more before sending his children to high school in Australia. He’s flying to the country this month to view homes and farmland, hoping to buy before the yuan weakens any further.

For some investors, it’s never too early to pull the trigger. Richard Baumert, a partner at Millennium Partners Boston, tells the story of a 33-year-old Chinese man who purchased a luxury home for his future children in August, convinced they’re destined to attend one of the city’s prestigious universities.

The buyer shelled out $2.4 million for the property, Baumert said, unfazed by the fact that he’s single and it could be two decades before he has kids old enough for college.

Donald Trump’s victory promises a further departure from the traditional Asia-Pacific order created during the Cold War years. This was when the US provided military and economic dominance through a system of defence alliances with the major trading partners in the region, including Australia.

The old Asia-Pacific order was based on the exchange of security for free trade. With the demise of the Soviet Union and the rise of China’s market economy, the Asia-Pacific order is now in an evolutionary phase.

Now the hierarchy of countries is splitting between security – still dominated by the US, and the economic order- which is being overtaken by China.

In the middle of this competition between the US and China, there are the Asia-Pacific countries dealing with China for economic gains without giving away American security patronage. Japan and Australia best exemplify these countries.

For example, both are negotiating the Trans Pacific Partnership and the Regional Comprehensive Economic Partnership, while keeping vast numbers of US troops and nuclear armaments on their soils. Both clearly benefit from the status quo and don’t wish for the day to come when they have to choose a bundled security-economic dependency with either the US or China, in Cold War-like dynamics.

The stability of the current dual order between the US and China depends first and foremost on the US ability and willingness to provide its Asia-Pacific allies with a security bulwark against destabilising actors (for example, North Korea, ISIS, and the various nationalistic forces). Trump’s isolationist foreign policy may put an abrupt end to this dynamic.

Recent issues in the South China Sea show that China may grow impatient in sharing the limelight with the US.Reuters

On the other hand, it’s still not clear whether China is going to be satisfied with economic dominance alone and with its current geopolitical restraint with its trading partners in the region. China may soon gradually use its trade and investment might to push smaller Asian countries away from their strong bilateral security ties with the US, in exchange for tighter multilateral economic cooperation.

The perfect example of this new dynamic is the recent alignment of the Philippines with China. Philippines President Rodrigo Duterte claimed that “America has lost” both militarily and economically.

China’s elites have long held the view of the US as a declining power and China as its natural heir in the region. Long-established research in political science and economics shows countries rise as they use asymmetric trade relations to turn economic dominance into a military dominance for geopolitical gains.

China’s world trade policy is to assert regional leadership to integrate and upgrade in the global economy. China will eventually seek to translate this trade leadership into regional security and then political dominance also at a global level, as the Asia-Pacific region carries the bulk of world economic growth.

On the one hand, this co-dependency restrains China from an exceedingly aggressive foreign policy, but on the other hand is pushing China’s strategic interests out of the Asia-Pacific regional shell. In fact, as early as November 2014, China’s President Xi Jinping openly advanced the idea of a “major-power diplomacy with Chinese characteristics”. In other words, to secure national interests with a more assertive foreign policy reflecting China’s rising economic power.

With Trump’s victory, and also considering the recent issues in the South China Sea, it would be hard to believe that China is going to be satisfied in a dual order under the US security umbrella. The ultimate issue is whether China will decide to pursue hardline policies to push the US outside of Asia in the short term, or instead patiently wait for the US to naturally recede from the region as its economic power wanes.

Before Trump’s victory, there was reason to believe that Xi Jinping and the Chinese government would opt for the latter option. This was because it’s not in China’s best economic interest to ignite geopolitical tensions in Asia, especially as the American retreat may lead Japan to reinstate a significant military capability.

As China currently benefits from a stable, open and secure system of free trade, Trump’s trade protectionist agenda may instead push China towards hardline foreign policies. This would compel its co-dependent trading partners like Australia to soon make a clear choice between the US and China.

Author: Giovanni Di Lieto, Lecturer, Bachelor of International Business, Monash Business School, Monash University

The Executive Board of the International Monetary Fund (IMF) concluded the Article IV consultation with China.

China continues its transition to sustainable growth, with progress on many fronts yet also many challenges. Growth slowed to 6.9 percent in 2015 and is projected to moderate to 6.6 percent this year owing to slower private investment and weak external demand. The economy is advancing on many dimensions of rebalancing, particularly switching from industry to services and from investment to consumption. But other aspects are lagging, such as strengthening SOE and financial governance and containing rapid credit growth.

Inflation dipped below 1.5 percent in 2015 and is expected to pick up to around 2 percent this year, reflecting the rebound in commodity prices and the exchange rate depreciation since mid-2015.

Infrastructure spending picked up and credit growth accelerated in the second half of 2015. Accommodative macro policies are projected to continue supporting activity over the remainder of 2016.

The current account surplus is projected to decline to 2.5 percent of GDP this year (from 3 percent of GDP in 2015) as imports increase and the services deficit widens with continued outbound tourism. The balance of payments came under pressure in 2015 due to large capital outflows, mainly related to repayment of external debt. The volume of outflows is expected to moderate this year. After appreciating 10 percent in real effective terms through mid-2015, the renminbi has depreciated some 4.5 percent since then and remains broadly in line with fundamentals.

Executive Board Assessment

Executive Directors commended the Chinese authorities for their strong determination to achieve more balanced, sustainable growth. They noted that economic growth continues to moderate and is driven increasingly by services and consumption. Directors welcomed the impressive progress on structural reforms in many areas, notably interest rate liberalization, internationalization of the renminbi, and urbanization. They also welcomed the 13th Five‑Year Plan, with its ambitious goals centered on economic rebalancing.

Directors noted that China’s economic transition will continue to be complex, challenging, and potentially bumpy, against the backdrop of heightened downside risks and eroding buffers. They stressed the need for decisive action to tackle rising vulnerabilities; reduce the reliance on credit‑financed, state‑led investment; and improve governance, risk pricing, and resource allocation in the state‑owned enterprise (SOE) and financial sectors. Directors emphasized that consistent, well‑coordinated, and clearly‑communicated policies are key to a smooth, successful transition, which will eventually benefit the global economy.

Directors highlighted the urgency of addressing the corporate debt problem through a comprehensive approach. They encouraged the authorities to harden budget constraints on SOEs; triage and restructure or liquidate over‑indebted firms; and recognize losses and share them among relevant parties, including the government if necessary. Piloting a few SOEs would make a strong start to the process. Directors recommended that the authorities complement these measures with targeted social assistance for displaced workers, and initiatives to facilitate entry of new, dynamic private firms.

Directors concurred that macroeconomic policies should be geared at lowering vulnerabilities, which would likely entail somewhat slower growth in the short term. They welcomed the authorities’ intention to rely on fiscal support if growth falls sharply in the near term. To this end, they saw merit in using on‑budget, pro‑consumption measures, which would help promote internal and external rebalancing. Measures could include raising pensions; increasing social, education and health spending; providing restructuring funds; and cutting minimum social security contributions. Continued efforts are also needed to ensure full implementation of the new budget law, improve fiscal transparency, and modernize the tax system.

Directors underscored the importance of further enhancing financial stability. Priorities include encouraging banks to proactively recognize loan losses and strengthen capital ratios; enhancing supervisory focus on liquidity risk management and funding stability risks; and addressing vulnerabilities in shadow products. Directors also recommended a major upgrade of the supervisory framework to foster cross‑agency information sharing and policy coordination, reduce the scope for regulatory arbitrage, and enhance crisis management capabilities. They looked forward to the forthcoming Financial Sector Assessment Program Update.

Directors noted the staff’s assessment that the renminbi is broadly in line with fundamentals, although the external position in 2015 was moderately stronger than consistent with fundamentals. They welcomed steps toward an effectively floating exchange rate regime and encouraged the authorities to build on this progress while carefully managing the transition, and with the support of a more market‑based monetary framework. Directors supported a cautious approach to capital account liberalization that is carefully sequenced with the progress on exchange rate flexibility and financial sector reforms.

Directors encouraged the authorities to continue to improve data quality and policy communications, which would help reduce uncertainty, align expectations, and guard against market turbulence.

Property purchase enquiries from Chinese buyers increased by 87% in 2015, according to new data.

The data released by online Chinese property portal Juwai.com show that Chinese buyers made enquires worth USD$34.9 billion over the year, with Victoria ranking as the most popular state.

The top five cities where Chinese buyers directed their property purchase enquires were Melbourne, Sydney, Brisbane, Adelaide and the Gold Coast. Enquiries for Melbourne property increased by 177% in 2015.

Chinese buyers are active across the entire range of prices, but that more than half of Chinese buyers are seeking property in the $200,000 to $500,000 range.

The RBA released the latest edition of the Financial Stability Review. Whilst they highlight the risks in emerging markets and higher bank funding costs, they argue local banks have limited exposure to these issues, households and business are financially sound and banks have tightened lending standards (as shown by lower LVRs and bigger affordability buffers) so predicted losses remain low, whilst profitability is strong. They are not concerned about high household debt ratios. The RBA also highlights the capital improvements which are in train. So overall they argue the financial sector is well positioned (though with a few issues to work though, for example, exposures to New Zealand Dairy and Property, Resource sector, property development, Insurance sector). They also say the tighter access to credit for households could pose near-term challenges in some medium- and high-density construction markets given the large volume of building activity that was started several years ago. They also suggest some foreign banks operating here could be under more pressure.

They examined Chinese buyers in the Australian Property Market.

Chinese investment in Australian residential and commercial property has increased significantly in recent years. This interest in property from Chinese households, institutional investors and developers is not unique to Australia; they are also active in the property markets of other countries, such as the United States, the United Kingdom, Canada and New Zealand.

The Australian banking system’s direct exposure to Chinese property investors and developers appears to be small. However, if Chinese demand were to decline significantly, that could weigh on domestic property prices and so lead to losses on the banks’ broader property-related exposures. Non-resident Chinese buyers own only a small portion of the Australian housing stock, but industry contacts suggest that they account for a significant and increasing share of purchases. These purchases are largely concentrated in off-the-plan apartments (especially in Sydney and Melbourne), in part because all foreign buyers, other than temporary residents, are generally restricted to purchasing newly constructed dwellings. Consistent with observations by industry contacts, the limited and partial data available from the Foreign Investment Review Board (FIRB) suggest that approvals for all non-residents applying to purchase residential property have increased substantially of late. The majority of these approvals are for new dwellings in New South Wales and Victoria. China is the largest source of approved investment in (residential and commercial) real estate and its share of total approvals is growing, but it still only accounts for a small fraction of overall market activity.

Nonetheless, if a significant subset of buyers reduce their demand sharply, this can weigh on housing prices, and Chinese buyers are no exception to this given their growing importance in segments of the Australian market. Such a reduction in housing demand could result from a number of sources, including:

A sharp economic slowdown in China that lowers Chinese households’ income and wealth. Any accompanying depreciation of the renminbi against the Australian dollar could further reduce their capacity to invest in Australian housing. In the extreme, Chinese investors may need to sell some of their existing holdings of Australian property to cover a deteriorating financial position at home. A macroeconomic downturn in China could also be expected to have knock-on effects on other countries in the region, which could also affect those countries’ residents’ capacity and appetite to invest in Australian property. On the other hand, if economic prospects in China deteriorate this could make investment abroad, including in Australia, more attractive and result in an increase in demand for Australian property.

A further tightening of capital controls by the Chinese authorities that restricts the ability of Chinese households to invest abroad.

A domestic policy action or other event that lessens Australia’s appeal or accessibility as a migration destination, including for study purposes. Industry contacts suggest that in addition to wealth diversification, many Chinese purchases are dwellings for possible future migration, housing for children studying in Australia or rental accommodation targeted at foreign students. If so, this demand could be expected to be fairly resilient to shorterterm fluctuations in conditions in China or developments in the domestic property market, but more sensitive to changes in migration or education policy.

A substantial reduction in Chinese demand would likely weigh most heavily on the apartment markets of inner-city Melbourne and parts of Sydney, not only because Chinese buyers are particularly prevalent in these segments but also because other factors would reinforce any initial fall in prices. These include the large recent expansion in supply in these areas as well as the practice of buying off the-plan, which increases the risk of price declines should a large volume of apartments return to the market if the original purchases fail to settle.

The Australian banking system has little direct exposure to Chinese investors. Australian owned banks engage in some lending to foreign households to purchase Australian property, but the amounts are small relative to their mortgage books. Australian-owned banks also have tighter lending standards for non-residents than domestic borrowers, such as lower maximum loan-to-valuation ratios, because it is harder to verify these borrowers’ income and other details, and because the banks have less recourse to these borrowers’ other assets should they default on the mortgage.

Australian branches of Chinese-owned banks appear to be more willing to lend to Chinese investors because they are often in a better position to assess these borrowers’ creditworthiness, particularly where they have an existing relationship. Nonetheless, although the direct exposures are small, if a reduction in Chinese demand did weigh on housing prices this could affect banks’ broader mortgage books to some extent.

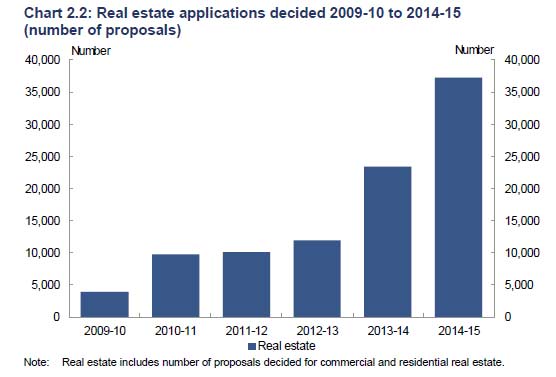

China foreign investment in real estate in Australia doubled that last year, according to the Foreign Investment Review Board (FIRB) in their annual report for the year 2014-2015. Total foreign investment approvals across all categories were worth $194.6 billion. No applications were rejected last year, though some were approved only with conditions.

Looking at the real estate sector, we see significant growth in applications compared with previous years.

Approved investment in real estate (comprising commercial and residential proposals) was $96.9 billion in 2014-15 (compared with $74.6 billion in 2013-14). Residential approvals rose from $34.7 billion in 2013-14 to $60.75, of which $49.25 billion were for development.

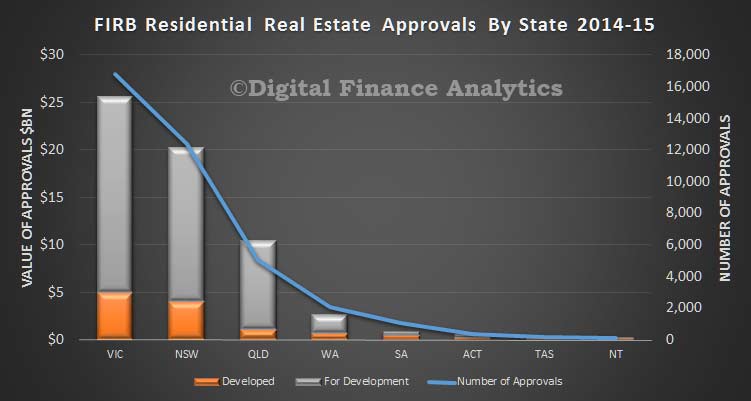

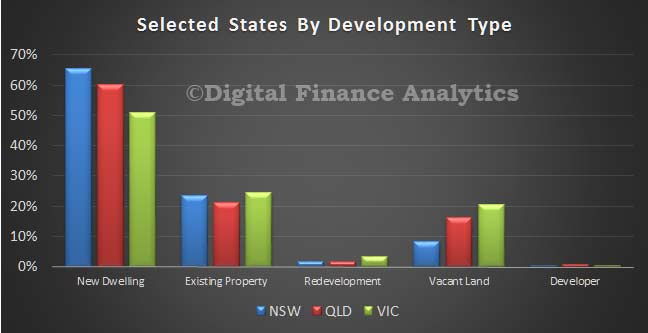

Looking at the state analysis, VIC leads the way in terms of the number and value of approvals. For example VIC had $20.6 billion of developments for approval, compared with $16.24 billion in NSW.

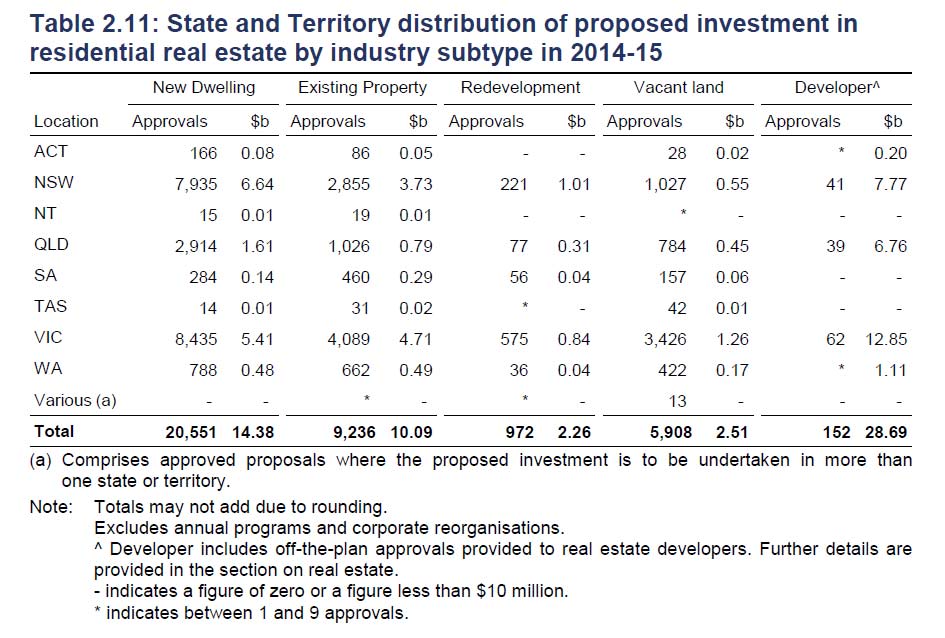

The FIRB report includes a state analysis by type of development

Our analysis shows the largest proportion of new dwelling approvals in NSW, compared with VIC and QLD. On the other hand, VIC had the highest proportion of existing property and vacant land approvals.

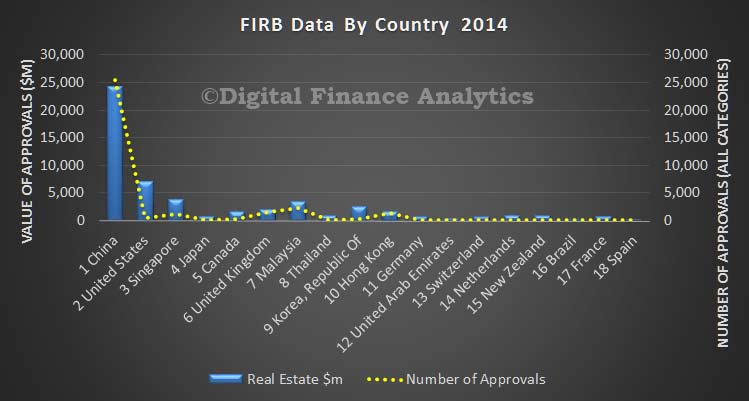

The Country data provided by the FIRB report does not separate residential real estate from commercial property. That said, the data shows China as the largest investor, based on number of approvals and value. In the previous year, China originated 14,716 approvals, compared with 25,431 in 2014-15 overall, whilst real estate was worth $12.4 billion in 2013-14 compared with $24.3 billion in 2014-15.

Major Chinese banks’ results for 2015, which are due to be released next week, should show continued subdued earnings growth amid margin compression and asset deterioration, says Fitch Ratings.

Fitch expects these trends to continue in 2016, underscoring our negative sector outlook. Chinese bank profits are likely to decline this year unless authorities relax the minimum NPL provisioning requirement of 150%.

System-wide net profit for China’s banking sector grew by only 2.4% in 2015 as net interest margins declined by around 12bp to 2.53%. A combination of interest-rate cuts and worsening asset quality will continue to have an impact on profitability in 2016. The quarterly run-rate in reported NPLs decelerated in 4Q15, while we believe this is due partly to more substantial NPL write-offs/disposals towards the end of the year as banks struggled to meet their provisioning requirements.

The provision coverage ratio at state banks and joint-stock banks had fallen to 172% and 181%, respectively, on average by end-2015. The need to maintain this ratio above 150% will restrain earnings growth in 2016 – unless this ratio is relaxed. The floor could also encourage further under-reporting of NPLs.

Reports from local media today suggest that the authorities are considering lowering the provisioning requirement to 130%-140% for selected banks. Fitch believes a relaxation would run counter to a need for conservative provisioning at a time when asset quality is deteriorating and the concerns around the true level of NPLs in the system. That said, such changes in regulations in isolation should not have major rating implications as our analysis takes into account factors and performance trends beyond reported profitability figures.

The reduction in the interest burden for borrowers following successive rate cuts and other monetary loosening through 2015 should keep reported NPLs below 2% for most banks. The system-wide NPL ratio and “special-mention” loan ratio were 1.67% and 3.79%, respectively, at end-2015, up from 1.25% and 3.11% a year ago. The trend in overdue loans may paint a more interesting picture, though, as Chinese banks tend to report very similar NPL ratios despite varying levels of overdue loans.

Furthermore, changes in investment income or revaluation reserves may also signal deterioration in the quality of non-loan credit, especially in mid-tier banks. This may take the form of investment receivables representing a growing share in the asset mix.

Loss-absorption trends could be a key rating driver for most banks while profitability and asset quality weaken and pressure on provisioning increases. Major Chinese banks were key issuers of Additional Tier 1 (AT1) instruments in 2015, owing to increased pressure to shore up capital due to balance-sheet growth and slowing profitability. However, as long as assets continue to grow at a rapid pace and profitability remains subdued, there will be little underlying improvement in core capitalisation levels. Such capitalisation pressures continue to weigh on Fitch’s assessment of Chinese banks’ Viability Ratings, especially those of the mid-tier banks.

The expansion of non-interest income is likely to be a key earnings driver in 2015-2016, especially for mid-tier banks, driven by strong card and underwriting fees as well as the sale of wealth management products (WMPs). But Fitch views excessive reliance on WMPs as risky for banks, and a significant shift in the business towards this area could lead to increased credit and liquidity risks.

The proposed guidelines provide a more comprehensive set of definitions for off-balance-sheet exposures to better capture the latest innovations. When the CBRC formulated the current regulations in 2011, they mainly addressed the guarantee and commitment businesses. The new rule will expand to include entrusted services (which includes entrusted loans and investment, non-guaranteed wealth-management products, agency transactions, agency issues and bond underwriting) and intermediary services (including agency collection and payments, financial advisory and asset custody). These new services have grown rapidly in recent years, raising concerns about the expansion of China’s shadow banking system.