A nice summary piece from CoreLogic’s blog.

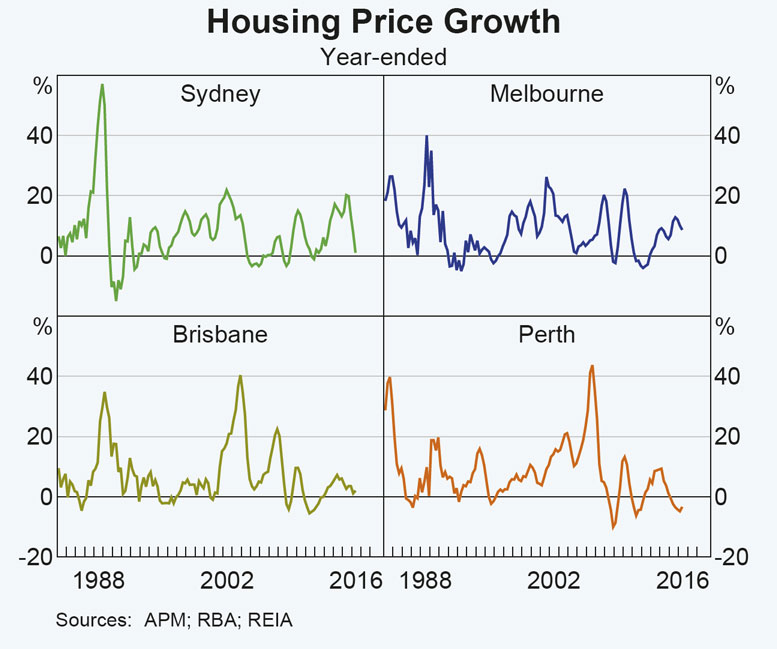

The housing market appears to be responding to a number of factors which have spurred further growth in home values. Official interest rates are at historic low levels which has encouraged borrowing for housing and driven housing debt to record-high levels. The low interest rate setting is also seeing significant competition amongst lenders which has resulted in substantial discounts to headline mortgage rates. Furthermore, while the total number of homes available for sale is similar to levels a year ago, there has been significantly fewer newly advertised properties listed for sale over the past few months relative to previous years. The low number of newly advertised dwellings available for sale has created a sense of urgency for buyers in the market, particularly in Sydney and Melbourne, and resulted in further increases in home values over this growth cycle which has been running for more than four years.

While the banking regulator has implemented policies aimed at slowing investment related credit demand, his has not resulted in a significant cooling in the housing market. The pace of investment related credit growth has slowed from a peak of nearly 11% per annum to 5% over the most rent 12 months period, however we are now seeing an uplift in lending to investors once more. Following the most recent interest rate cut, auction clearance rates have elevated to levels not seen for more than a year, particularly in Sydney, the nation’s least affordable housing market.

Interest rates

On August 2, the Reserve Bank (RBA) decided to cut official interest rates by 25 basis points to 1.5%. While interest rates were lowered to historic lows, headline variable mortgage rates were generally reduced by much less, with each of the Big 4 banks lowering their mortgage rates by no more than 14 basis points. Despite the fact that the interest rate cuts were not passed on in full to mortgage holders, mortgage rates below 4% are available for those who wish to move from their current lender. With most mortgages on a variable rate, any cut to mortgage rates will improve a household’s disposable income. Furthermore, it has become clear that it will also give them more confidence to increasingly purchase more expensive homes, well in Sydney and Melbourne at least.

Housing debt

Each quarter the RBA publishes ratios of household finances which include the ratio of household debt to disposable income. The latest data to March 2016 shows that the typical level of housing debt is 134.7% higher than household disposable income. The current ratio is a record-high but it is important to remember that it is a national snapshot and conditions across different housing markets are likely to vary substantially. Since the current phase of growth in home values commenced in the June 2012 quarter, this ratio has lifted from 119.0%.

While the ratio of housing debt to disposable income has increased and is at a record-high, the ratio of housing assets to disposable income has also risen as home values have increased. In the June 2012 quarter, the typical value of household assets was 394.4% higher than household disposable income. By March 2016, the ratio had increased to 470.8% indicating a significant increase in the value housing assets. Again, it should be remembered that this is a national measure and local market ratios are likely to be vastly different especially within areas of very little value growth over that time as well as those areas in which home values have fallen.

Properties listed for sale

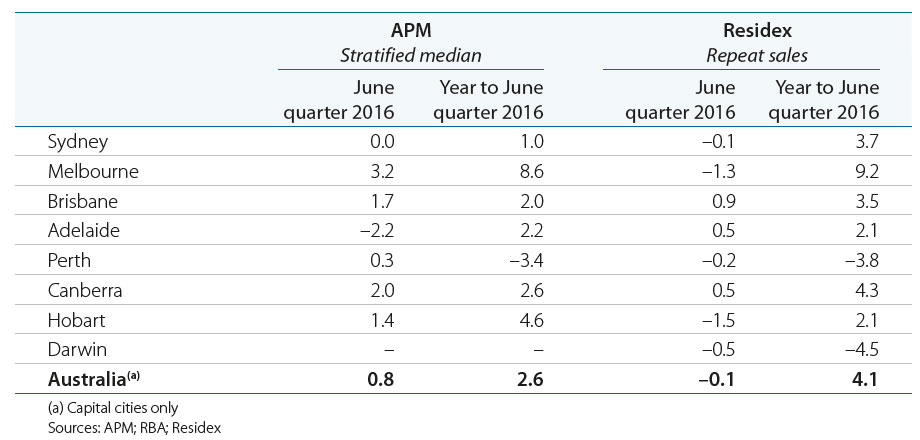

Over the four weeks ending August 21 2016 there were 39,676 new (not previously advertised for at least six months) residential properties listed for sale and 229,386 total (includes new and relisted properties) properties advertised for sale. The number of newly advertised properties listed for sale was -3.4% lower than at the same time last year and new listings have been lower each week year-on-year since early June 2016. Meanwhile, total listings are -0.9% lower than they were a year ago and on a weekly basis have been consistently lower year-on-year since early July of this year. New and total listings are now starting to increase as we head closer to the beginning of the Spring Selling Season as they do each year.

While the national figures show fewer listings than a year ago, the trends are very different across individual capital cities, particularly in Sydney and Melbourne where home value growth conditions are strongest.

In Sydney, over the past four weeks there were 6,299 newly advertised and 18,951 total properties advertised for sale. Year-on-year, new listings have now been lower than they were the previous year fairly consistently since last November and are currently -20.6% lower than they were a year ago. Over the past four weeks there were 17,949 total listings in Sydney which was 0.8% higher than a year ago. While total listings are slightly higher than a year ago, there is very little new stock being listed for sale. New listings are arguably more important than relisted properties, especially if the relisted stock has been for sale for a long period of time and vendors aren’t adjusting their price expectations. Even though spring is just around the corner, there is very little fresh stock being added to the market.

It is a similar story in Melbourne where there were 7,177 new and 25,846 total residential properties listed for sale over the four weeks to 21 August 2016. The number of new listings was -9.4% lower year-on-year and total listings were -0.8% lower. Again, with spring just around the corner there is a relatively low supply of newly advertised properties hitting the market for sale.

Mortgage demand

One of the big challenges the RBA has is the quality and regularity of mortgage data collection. While housing finance data is published each month, owner occupier housing finance commitments are published both on a number and value basis while investor housing finance commitments are only published on the basis of value not the number of loans. With the investment segment having become so prevalent, it is a challenge not knowing both the number and value, particularly when investment is so strong in Sydney and Melbourne at a time when home value growth is also so strong. Adding to the challenge of interpreting housing finance data is the lack of clarity about how off-the-plan unit purchases are captured in the data. It is unclear as to whether they are classified as construction of dwellings or purchase of new dwellings. Finally re-classification of large swathes of mortgages from lenders away from investment and toward owner occupiers has made reading the market even more difficult.

The latest housing finance data showed that in June 2016 there was $32.6 billion worth of commitments with the value having increased by 2.3% over the month following a 1.8% rise in May. Although mortgage lending is rising, it remains -2.1% lower than its peak in April of last year. Over the month, there was $20.8 billion in commitments to owner occupiers and $11.8 billion in commitments to investors. Both segments of lending rose over the month however, owner occupier lending is -2.4% lower than its December 2015 peak while investment lending is -22.0% lower than its April 2015 peak.

Owner occupier lending remains quite strong and although investment lending has slowed significantly, there is now scope for it to increase over the coming months. Without additional details on the number of investment loans it is difficult to know whether the increase is being driven by larger loan sizes, a larger number of loans or a combination of both.

Auction clearance rates

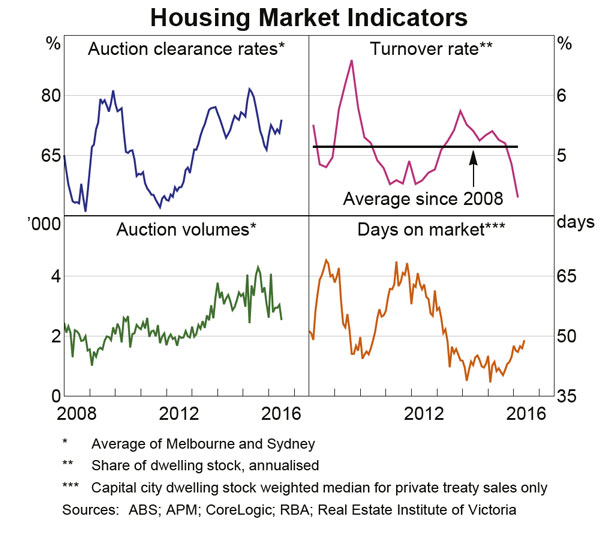

Auction clearance rates are one of the timeliest indicators of the housing market and they tend to be indicative of the broader housing market trends. It is important to remember that far more homes sell by private sale than by auction and auctions are only a significant proportion of sales in the Sydney, Melbourne and Canberra housing markets.

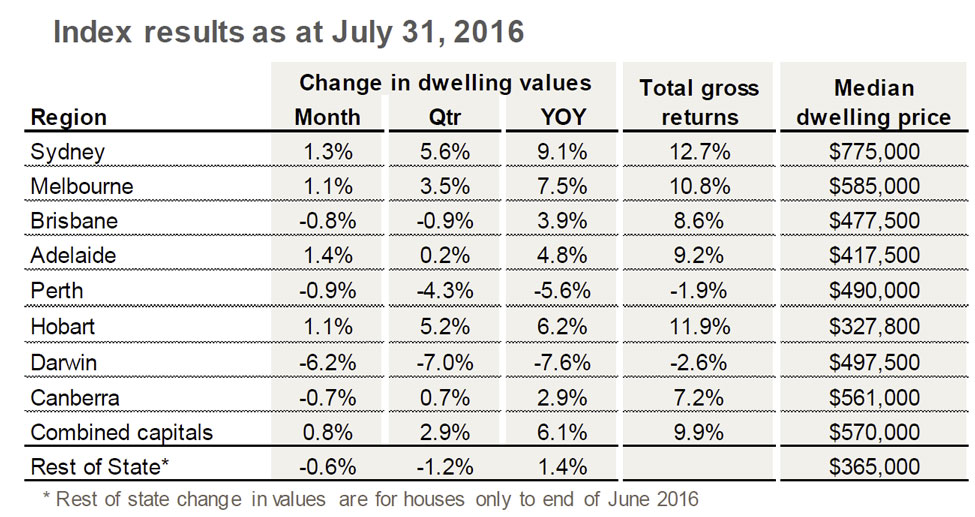

Auction clearance rates in Sydney last week were at their highest levels in more than a year. Sydney’s auction clearance rate has been above 70% for 18 consecutive weeks and in Melbourne they have been above 70% for 7 consecutive weeks.

As already discussed, the supply of homes available for sale, particularly in Sydney and Melbourne, is much lower than it has been over recent years. This is particularly evident when looking at auction volumes. Over 2016 so far there have been 18,619 auctions in Sydney compared to 25,399 auctions at the same point in 2015. This represents a -26.7% decline in the number of auctions in Sydney over the year to-date. In Melbourne there have been 23,779 auctions so far this year which is -9.5% lower than the 26,282 auctions to the same point last year. The low volume of auction stock is likely to be resulting in the ongoing strength in clearance rates across each city. Less stock for sale creates a sense of urgency for those looking to purchase.

So what does this mean for Spring?

It is too early to say definitively what will happen this Spring but I would be very comfortable stating that what happens with property listings will have a substantial influence on the market’s performance over the period. Spring is typically characterised by a fairly significant upswing in stock for sale, this is driven by the belief that Spring is the best time of year to sell (that is a topic for another day). As supply increases, the value growth performance can slow and as we saw last year, auction clearance rates can actually start to dip. So the amount of stock which becomes available for sale will be an important factor for the strength of the Sydney housing market.

The recent interest rate cut is another important consideration for the market’s performance. Although mortgages and the availability of them, is calculated on the borrower’s ability to repay the mortgage at a much higher interest rate, lower mortgage rates impact households by giving them the option to reduce mortgage repayments and therefore having more money each week in their pocket. This is because most mortgages are on a variable rate and changes to the interest rate on their largest commitment (the mortgage) have an immediate impact on household balance sheets. With the recent cut to interest rates, it is unlikely to mean that people that could not previously borrow now can, but it does mean that households that previously weren’t considering moving home or buying an investment property may now be more inclined to do so. This may result in more confidence from those looking to upgrade their property to list their home which means that they also become an additional purchaser. If someone is now starting to consider buying an investment property it also means additional demand for housing. How many new buyers there are in Spring remains to be seen but it may encourage an increase in demand for purchase and could result in more people looking to sell their home.

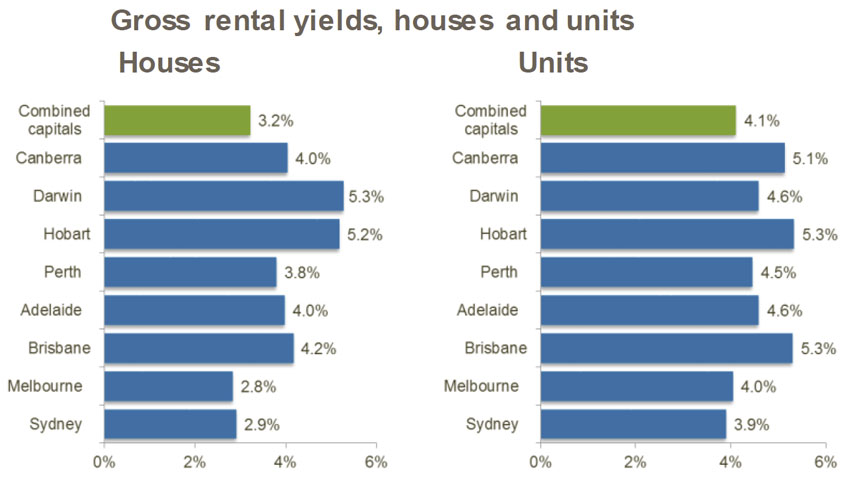

The other major consideration, particularly in Sydney and Melbourne, but also across the rest of the country is what the prospects are for additional increases in home values over the short and medium term. Combined capital city home values have been rising for more than four years now however, this has largely been driven by Sydney and Melbourne due to their much stronger economies. While the economies in these cities remain strong, the increasing cost of housing due to the four plus years of value growth may be starting to deter buyers. When you also consider that rents are increasing at record low levels (falling in some areas) and gross rental yields are at record lows, purchasing a property, particularly an investment, is looking less attractive than it has for some time. Especially when you also factor in the heightened level of housing construction, most of which is inner city units, which is currently underway.

It is going to be interesting to see how all of these factors play out over the next few months and ultimately how the housing market performs.