More evidence of inflation lurking in the US economy, as the headline rate for January was higher than expected. This gives more support to the view the FED will indeed lift interest rates.

The Consumer Price Index for All Urban Consumers (CPI-U) increased 0.5 percent in January on a seasonally adjusted basis, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all items index rose 2.1 percent before seasonal adjustment.

The seasonally adjusted increase in the all items index was broad-based, with increases in the indexes for gasoline, shelter, apparel, medical care, and food all contributing. The energy index rose 3.0 percent in January, with the increase in the gasoline index more than offsetting declines in other energy component indexes. The food index rose 0.2 percent with the indexes for food at home and food away from home both rising.

The index for all items less food and energy increased 0.3 percent in January. Along with shelter, apparel, and medical care, the indexes for motor vehicle insurance, personal care, and used cars and trucks also rose in January. The indexes for airline fares and new vehicles were among those that declined over the month.

The all items index rose 2.1 percent for the 12 months ending January, the same increase as for the 12 months ending December. The index for all items less food and energy rose 1.8 percent over the past year, while the energy index increased 5.5 percent and the food index advanced 1.7 percent.

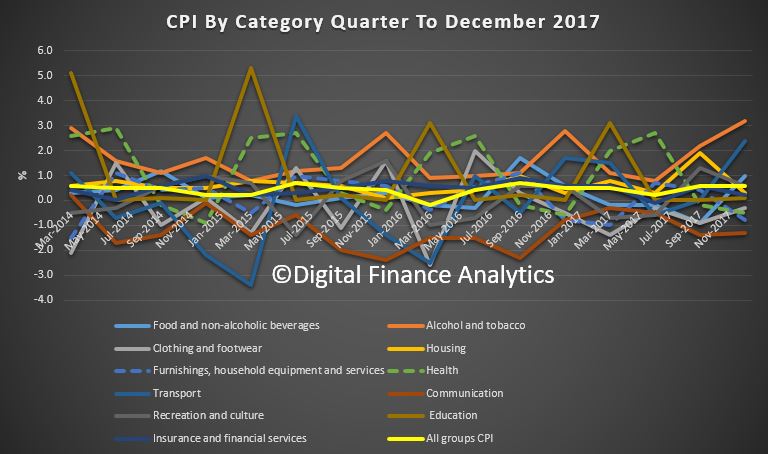

The Consumer Price Index (CPI) rose 0.6 per cent in the December quarter 2017, the latest Australian Bureau of Statistics (ABS) figures reveal. Annual inflation in most East Coast cities rose above 2.0 per cent, due in part to the strength in prices related to Housing.

This follows a rise of 0.6 per cent in the September quarter 2017. However, there were some changes in methodology which may have impacted the results.

The most significant price rises this quarter are automotive fuel (+10.4%), tobacco (+8.5%), domestic holiday travel and accommodation (+6.3%) and fruit (+9.3%). These price rises were partially offset by falls in international holiday travel and accommodation (-1.7%), audio visual and computing equipment (-3.5%) and telecommunication equipment and services (-1.4%).

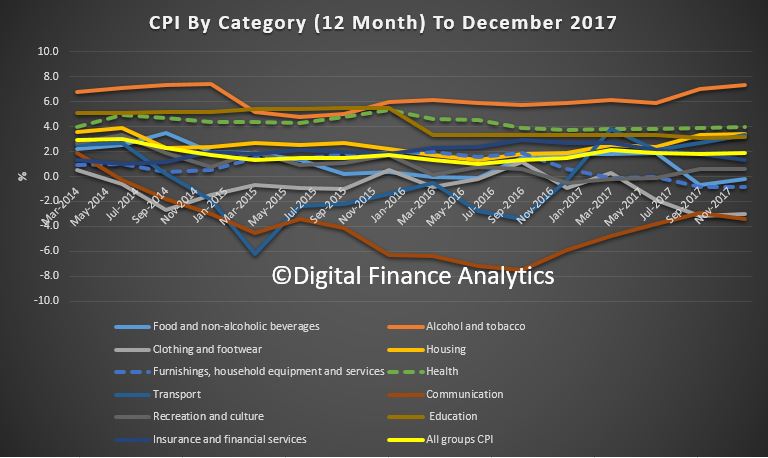

The CPI rose 1.9 per cent through the year to December quarter 2017 having increased 1.8 per cent through the year to September quarter 2017.

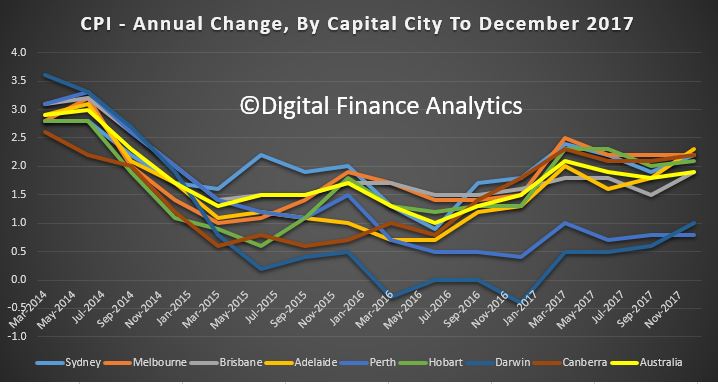

Chief Economist for the ABS, Bruce Hockman, said “While the annual CPI rose 1.9 per cent, annual inflation in most East Coast cities rose above 2.0 per cent, due in part to the strength in prices related to Housing. Softer economic conditions in Darwin and Perth have resulted in annual inflation remaining subdued at 1.0 and 0.8 per cent respectively.”

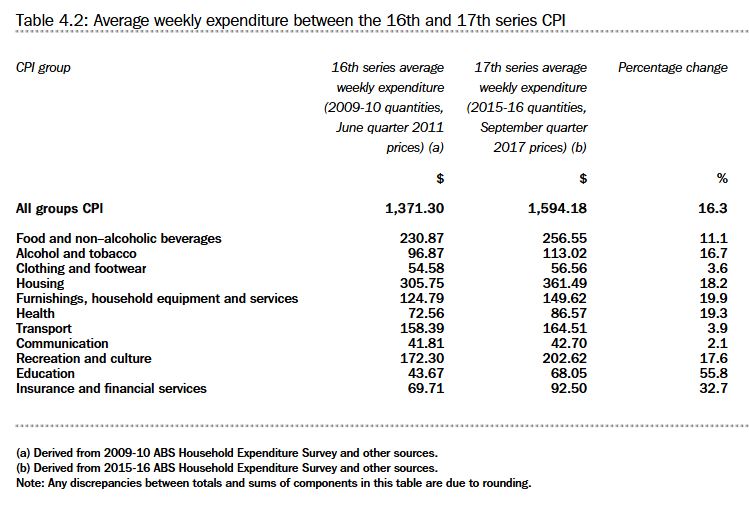

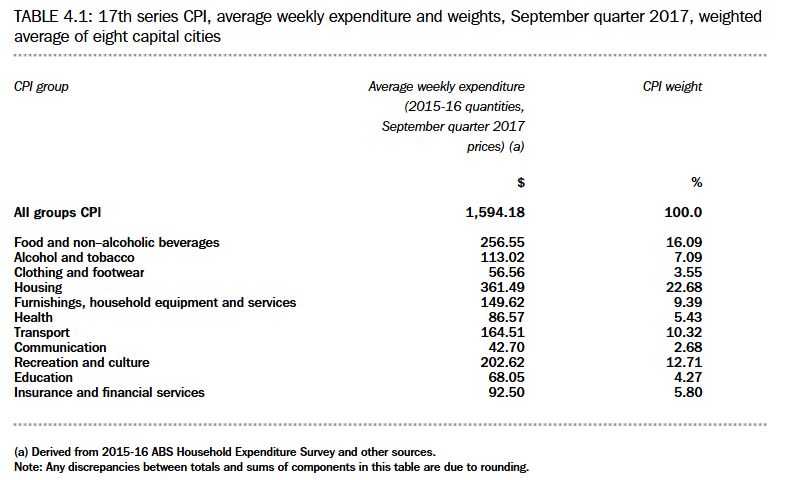

The ABS periodically reviews the CPI expenditure weights to ensure they are representative of household spending patterns on goods and services. This quarter the ABS has introduced new expenditure weights based on information sourced from the ABS Household Expenditure Survey.

In addition, this quarter the ABS has also implemented methodological changes to maximise the use of transactions data to compile the CPI. Implementation follows a period of extensive research and expert peer review, including from Professor Kevin Fox of UNSW Sydney. Professor Fox said “I strongly support the ABS decision to implement new CPI methods for the treatment of transactions data. The ABS has made a convincing case for implementation following an extended period of research. These new methods will enhance the accuracy of the Australian CPI, provide additional analytics and better inform policy formulation.”

The Australian Bureau of Statistics has now released their paper which describes the changes that will be made to the Consumer Price Index (CPI) and Selected Living Cost Indexes (SLCIs) as a result of the introduction of the 17th series expenditure patterns.

There are quite a number of technical changes, as well as different weights for specific items. Housing and power costs for example will be higher. From 2018, the CPI will be re–weighted annually in December quarters

This is likely to lead to a lower headline CPI rate, perhaps by around 0.25% or more (DFA estimate), though there are various offsetting adjustments, so we cannot be sure. More noise in the numbers!

The first publications based on the 17th series will be in respect of the December quarter 2017, which are due to be released on 31 January 2018 (CPI) and 7 February 2018 (SLCIs).

Australia has produced indexes of retail price inflation going back as far as 1901. Prior to the introduction of the CPI in 1960, there were five series of retail price indexes compiled by the (then) Commonwealth Bureau of Census and Statistics. Since 1960, the Australian Bureau of Statistics (ABS) has maintained a program of periodic reviews of the CPI to ensure that it continues to meet community needs. The main objective of these reviews is to update the household expenditure information used to set the item weights in the CPI, but they also provide an opportunity to reassess the scope and coverage of the index.

The SLCIs, incorporating the Pensioner and Beneficiary Living Cost Index (PBLCI) and the Analytical Living Cost Indexes (ALCIs) have also been reviewed as part of the 17th series. These indexes are produced as a by-product of the CPI, with weights also derived from the Household Expenditure Survey (HES).

The 17th series review is a minor review of the CPI and SLCIs, consisting of an update of the upper level (expenditure class) weights in line with the latest HES, and a simple examination of structures and methodologies.

This information paper provides an overview of the changes to the CPI and SLCIs that will be introduced with the 17th series from the December quarter 2017. It describes the household expenditure data used to calculate the weights and the ways in which some of the data have been adjusted to align with CPI and SLCI requirements. The paper also presents the updated weighting patterns and some background on the major shifts in weights between the 16th and 17th series. There are no changes to the classification structure or publications in respect of the 17th series.

They also continue to explore options for a more frequent and timely monthly measure.

Interesting speech from RBA’s Guy Debelle, highlighting issues around measuring an number of economic factors. He calls out CPI as one area of uncertainly, especially as the ABS does a quarterly report (unlike many other countries who publish monthly) and the changes in weightings which will impact ahead. There is a lot of noise in the data…!

For inflation – which is also published quarterly in Australia – we won’t get an official read on the current rate until the December quarter Consumer Price Index (CPI) is released in late January, three months from now. In most other countries, the CPI is published monthly, so the wait to get an assessment on current inflation is not so long elsewhere.

More timely and more frequent estimates of output and inflation are not unambiguously desirable. There is clearly a trade-off between timeliness and accuracy. But, in the case of inflation, a more frequent estimate would help to identify changes in the trend in inflation sooner; it probably comes with more noise, but we have ways to deal with that. Any reading on inflation always contains varying degrees of signal and noise about the ‘true’ inflation process. At the moment, we need to wait three more months to gain a better understanding as to whether any particular read on inflation is signalling a possible change in trend or is just noise. That is one of the reasons why the RBA has long advocated a shift to monthly calculation of the CPI.

That said, we do not depend solely on GDP and the CPI to assess the current state of the economy. We spend a lot of time and effort piecing together information from a large number of other sources. These include higher frequency and more timely data, including from the ABS, but also from a wide range of other data providers. The information we obtain from talking to people, particularly through our business liaison program, is also invaluable.

The question then arises as to how we can filter the information we receive from all these different sources to gain an overall picture about inflation and the state of the overall economy. Take GDP as an example. Some of the data released before the national accounts, such as monthly retail sales and international trade, feed directly into the calculation of GDP. So we have a direct read on those. We ‘nowcast’ other components of GDP using data that are more timely. Let me illustrate for household consumption. We get a good measurement of consumption of goods by looking at monthly retail sales and sales of motor vehicles and fuel. But there is very little timely information on household consumption of services, so the nowcast of this component relies more on statistical relationships. Some of these relationships are pretty weak, so we also supplement this with information on sales from our regular discussions with our business liaison contacts. This then gives us an estimate of consumption for the quarter. To get a preliminary nowcast for GDP growth for the quarter, we aggregate our best estimate for each of the relevant components. We then ask ourselves whether this estimate is consistent with other information that we have, such as the monthly labour market data, as well as predictions from our macro forecasting models.

The nowcast can be then updated with new information as it comes to hand. That said, my observation from a couple of decades of forecasting is that your first estimate of GDP (three months out) is often the best, and that additional information is often noise rather than signal.

Measurement uncertainty

Aside from when data are published, uncertainty about the present also arises from how things are measured. This takes two forms. First, there is the methodology used to actually measure the variable in question. Second, there are the revisions to data after they were first published.

On the first, a good example is the CPI. The CPI measures prices for a large number of items purchased by households. When aggregating these to calculate the overall consumer price index, each item is assigned a weight based on its average share of household expenditure. That is, the aim is to weight each price by the amount households spend on it, on average, in the period in question.

Obviously, these weights can change through time. But the weights used in the CPI are only updated each time the ABS conducts a Household Expenditure Survey, which, in recent times, has been every five or six years.

In between each household expenditure survey, a number of things can happen. First of all, some new goods and services can come along that weren’t there before. One example you might think of is a mobile phone. Though it’s not quite that straightforward, as before mobile phones, households spent money on landline phone bills and on cameras. So often these ‘new’ goods are providing similar services to something that was there before. Nevertheless, the ABS needs to take account of these new goods coming in, as well as some old items dropping out.

Secondly, households adjust their spending in response to movements in prices and income. In practice, households tend to substitute towards items that have become relatively less expensive, and substitute away from items that have become relatively more expensive. But the expenditure weights in the CPI are only updated every five or six years. Over time, the effective expenditure weights in the CPI become less representative of actual household expenditure patterns. That is, they are putting more weight on items whose prices are rising than households are actually spending on them. This introduces a bias in the measured CPI – known as substitution bias – which only is addressed when the expenditure weights are updated. Because households tend to shift expenditure towards relatively cheaper items, infrequent updating of weights tends to overstate measured CPI inflation.

The ABS will very shortly update the expenditure weights in the CPI. Because of substitution bias, history suggests that measured CPI inflation has been overstated by an average of ¼ percentage point in the period between expenditure share updates. While we are aware of this bias, we are not able to be precise about its magnitude until the new expenditure shares are published, because past re-weightings are not necessarily a good guide. It is also not straightforward to account for this in forecasts of inflation. However, from a policy point of view, the inflation target is sufficiently flexible to accommodate the bias, given its relatively small size.

Going forward, the ABS will update the expenditure shares annually, rather than every five or six years. This will reduce substitution bias in the measured CPI.

The Consumer Price Index (CPI) rose 0.6 per cent in the September quarter 2017, the latest Australian Bureau of Statistics (ABS) figures reveal. This follows a rise of 0.2 per cent in the June quarter 2017.

The most significant price rises this quarter are electricity (+8.9%), tobacco (+4.1%), international holiday travel and accommodation (+4.1%) and new dwelling purchase by owner-occupiers (+0.8%). These rises are partially offset by falls in vegetables (-10.9%), automotive fuel (-2.3%) and telecommunication equipment and services (-1.5%).

The CPI rose 1.8 per cent through the year to September quarter 2017 having increased to 1.9 per cent in the June quarter 2017.

Chief Economist for the ABS, Bruce Hockman, said “Utilities prices rose strongly in the September quarter 2017. The most significant rises relate to electricity and gas prices, with increases in wholesale prices being passed on to consumers. Increases in wholesale prices have been observed across the National Electricity Market (NEM), with the most significant rises this quarter in electricity being observed in Adelaide; Sydney; Canberra and Perth.”

The Consumer Price Index (CPI) rose 0.2 per cent in the June quarter 2017, the latest Australian Bureau of Statistics (ABS) figures reveal. This follows a rise of 0.5 per cent in the March quarter 2017.

So nothing here to reinforce the need to raise the cash rate! However, our data suggests many households are experiencing much faster price growth, especially for power and child care.

The most significant price rises for the quarter were medical and hospital services (+4.1 per cent), new dwelling purchase by owner-occupiers (+0.9 per cent) and tobacco (+1.0 per cent). These rises are partially offset by falls in domestic holiday travel and accommodation (-3.2 per cent) and automotive fuel (-2.5 per cent).

The CPI rose 1.9 per cent through the year to June quarter 2017 having increased to 2.1 per cent in the March quarter 2017.

Chief Economist for the ABS, Bruce Hockman, said: “Inflation in Australia remains low. Price falls for automotive fuel; and ongoing competition in the clothing and food retail markets has contributed to this quarter’s result. In addition, the ABS continues to closely monitor the impact of Cyclone Debbie on fruit and vegetable prices. While strong price rises were recorded for select fruit and vegetables such as tomatoes, beans, cucumbers, melons, berries and bananas in the June quarter 2017 – these rises were offset by falls in seasonally available fruits such as oranges, mandarins and apples.”

Almost nothing is to be seen of Australia’s housing crisis in the latest inflation figures.

Wednesday’s Consumer Price Index (CPI) from the Australian Bureau of Statistics showed just a 0.5 per cent increase in inflation this quarter, up 2.1 per cent over the past 12 months.

Over the same period, house prices grew 1.4 per cent, and by 75 per cent over the past five years.

The biggest increases in the CPI were in fuel, healthcare, power and, yes, housing.

However, as pointed out recently by Commonwealth Bank senior economist Gareth Aird, this ‘housing’ figure, which accounts for 22 per cent of the CPI calculation, does not truly reflect the struggle of many Australians to get onto the property ladder.

“The CPI is a poor barometer of changes in the cost of living for people who don’t own a dwelling and aspire to purchase one,” Mr Aird wrote.

That’s because the CPI measure of ‘housing’ only counts rents, utilities and the cost of building a new dwelling. It doesn’t include the cost of the land the dwelling sits on. And it doesn’t include the interest costs of repaying a mortgage.

If the full cost of housing was factored in, Mr Aird estimated it would add roughly 55 percentage points to headline inflation.

As mentioned above, the CPI ‘housing’ measure also doesn’t include interest charges. It used to, but they were removed in 1998 after lobbying from the Reserve Bank, which argued that rising mortgage interest rates would push up inflation, thereby requiring official cash rate rises, which would then push mortgage rates even higher, in a vicious loop.

The RBA said then that “excluding interest charges would in no way distort the outcome over the long run”.

Australia Institute senior research fellow David Richardson said if the CPI were to include land prices, the inflation rate would be pulled too hard by almost out of control house prices.

“Imagine if things went up 15 per cent a year in price,” Mr Richardson told The New Daily.

“Lots of contracts in Australia are indexed against the CPI. If they’re sort of fiddled then you’re talking billions and billions in consequences.”

Marcel van Kints, program manager with the Prices Branch of the ABS Macroeconomic Statistics Division, told The New Daily: “The ABS CPI aligns with international standards, an international respected measure of inflation.”

The ABS also published a FAQ with Wednesday’s release in which they pointed to their reasoning behind the exclusion of land from the CPI.

They said that housing is included in the Selected Living Cost Indexes, which are “particularly suited to assessing whether or not the disposable incomes of households have kept pace with price changes”.

Inflation outpaces wages

All of this is seeing many Australians left behind as both housing and the prices of popular consumer goods rise while wages stagnate.

Over the past 12 months, the CPI rose 2.1 per cent while wages grew by only 1.9 per cent, according to the latest ABS data.

The Australia Institute’s David Richardson said this is leaving many Australians worse off.

“I suspect that as professionals and skilled white collar workers, we’re all in the same boat,” he said.

“What we’re seeing now is a symptom of structural change that’s been creeping up on us for a long time.”

The data from the ABS today shows that the Consumer Price Index (CPI) rose 0.5 per cent in the March quarter 2017. This follows a rise of 0.5 per cent in the December quarter 2016. The CPI rose 2.1 per cent through the year to March quarter 2017. The trimmed mean was 1.9 per cent. Housing costs rose 2.5 per cent is the past year.

In original terms, Melbourne prices rose 0.9% in the quarter, highlighting the pressure on households there. As we said the other day, average CPI is understating what is happening in Victoria at the moment.

This data confirms the next RBA cash rate adjustment is more likely up, than down. It also underscores the flat, or falling income growth households are experiencing. More pressure, more mortgage stress as cost of living rises outstrip income growth, in a rising mortgage rate market.

The most significant price rises this quarter are automotive fuel (+5.7 per cent), medical and hospital services (+1.6 per cent) and new dwelling purchase by owner-occupiers (+1.0 per cent). These rises are partially offset by falls in Furnishings, household equipment and services (-1.0 per cent) and Recreation and culture (-0.7 per cent).

Vegetable prices have risen 13.1 per cent through the year to March quarter 2017. Adverse weather conditions in major growing areas over previous periods continue to impact supply for particular vegetables (potatoes, salad vegetables, cabbages and cauliflower). Offsetting these rises are price falls for capsicums and broccoli.

According to the US Bureau of Labor Statistics, real (adjusted for inflation) average hourly earnings were unchanged from January 2016 to January 2017. Before adjusting for inflation, average hourly earnings increased 2.5 percent over the 12 months ending in January 2017. Over the same period, the Consumer Price Index for all Urban Consumers (CPI-U), which is used to adjust average hourly earnings for inflation, also increased 2.5 percent.

Since 2009, the 12-month change in average hourly earnings ranged from 1.5 percent (in October 2012) to 3.6 percent (in December 2008 and January 2009). Over the same period, the 12-month change in the CPI-U ranged from −2.0 percent (in July 2009) to 5.5 percent (in July 2008). The 12-month change in real hourly earnings ranged from −2.4 (in July 2008) percent to 4.8 percent (in July 2009).

The 12-month changes in average hourly earnings and the CPI-U were equal in April, May, and June 2014. From that time until December 2016, the change in hourly earnings was greater than the change in the CPI-U, resulting in positive changes in real average hourly earnings.

These data are from the Current Employment Statistics program and are seasonally adjusted. Data for the most recent 2 months are preliminary.

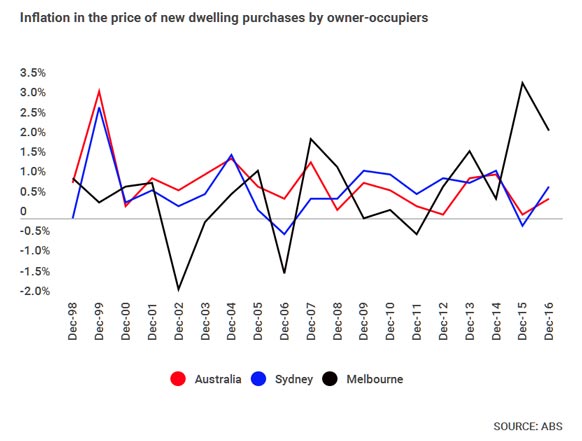

Despite Wednesday’s “worryingly” low inflation result, house prices have continued their upward march right where it hurts the most: the overheated capital cities.

Not only does the consumer price index measure things like groceries and petrol, it also measures changes in the price of buying a new home.

In fact, this measure contributes almost a tenth (9 per cent) to the Australian Bureau of Statistics’ theoretical basket of goods and services bought by the average consumer in the eight capitals, making it the single-biggest contributor.

The ABS reported on Wednesday that the overall rate of inflation was 1.5 per cent for 2016, and that the price of buying a new home rose 0.5 per cent in the December quarter.

As seen in the chart below, this continues the national trend of housing price growth, especially in Melbourne. Over 2016, new house prices increased a total of 1.9 per cent, according to the ABS’ inflation measure.

This is despite the recent GDP contraction, disappointing jobless figures, sluggish wage growth, constant predictions of a property market crash, and the fact that Perth is dragging down the average.

And this may not tell the full story.

Martin North, principal at Digital Finance Analytics, said the ABS measure “understates” the true impact of rising housing costs on household budgets.

“The costs of what it really is to live in a place anywhere close to the centre of the major cities, particularly Sydney and Melbourne, is much, much higher than will be stated or imputed in the CPI,” Mr North told The New Daily.

“There is no doubt that everyone is now recognising that house prices relative to incomes – or relative to any other metric you can think of – are way off, they are way too high.”

Another concern: the Reserve Bank’s reaction

Industry Super Australia is predicting the Reserve Bank will be forced to cut the cash rate target by 50 basis points in 2017: 25 points in the first half of the year followed by a further 25 points near the end.

However, this may not benefit the average new borrower or household on a variable rate mortgage, as the big banks are currently lifting borrowing rates despite the fact Australia’s central bank has been in a holding pattern.

“While this 50 basis points might seem very attractive, what it’s more than likely to do is just offset what’s going on in wholesale markets,” Industry Super Australia chief economist Dr Stephen Anthony told The New Daily.

“Therefore, what gets passed on to the consumer may be very little.”

Despite this, Dr Anthony still saw the inflation result as carrying an important warning for mortgage borrowers.

“Whilst it may be a ‘no change’ result for households, the most significant risk to the Australian economy in 2017 is vulnerability at the postcode level,” he said.

“If I am wrong and the Reserve Bank starts raising rates, that combined with developments in wholesale markets probably means that the level of mortgage stress will rise exponentially and that would be a significant risk to dwelling investment and obviously house prices would fall accordingly.”

Finance analyst Mr North said he saw a rate rise in 2017 as both prudent and far more likely than any cuts.

“I personally think rates should be higher than they currently are. We are stoking the housing market way beyond what is sensible,” he said.

“The problem we’ve got is that rates will at some point continue to rise. Most people have already experienced a rise of 15 to 65 basis points over the last little while because of bank repricing. That’s having a significant impact on a number of households – 20 per cent plus are finding it difficult to accommodate any rise.

“So if we take the rates even lower we are seeding a longer-term problem. The simplistic idea of ‘cutting rates and hoping’ is not going to work.”

From the March quarter 2017, the ABS will adjust the way it measures prices changes in new dwellings to ‘more robustly’ reflect the rising popularity of apartments.