VIDEO

Join us for a live Q&A as I discuss the latest from our surveys and core market model. I also had the DFA post code engine on line.

https://walktheworld.com.au/

Original live replay and chat also available: https://youtu.be/KrzLjg5IhRg

Go to the Walk The World Universe at https://walktheworld.com.au/

VIDEO

And we will also have our post code engine online tonight…

This is an edited edition of our latest live event.

CONTENTS

0:00 Start

The original edition with live chat replay is also available: https://youtu.be/mYWJ-b3lkfQ

Join us for a live Q&A as I discuss the current market with Michael Invests – host of his own channel. https://www.youtube.com/channel/UC2FiWOXQosY8RU5bxQCqmIg

https://walktheworld.com.au/

Digital Finance Analytics (DFA) Blog

DFA Live Q&A Replay 29th Dec 2020 [Podcast]

Play Episode

Pause Episode

Mute/Unmute Episode

Rewind 10 Seconds

1x

Fast Forward 30 seconds

00:00

/

01:27:32

Subscribe

Share

VIDEO

This is an edited edition of our latest live event.

CONTENTS

0:00 Start

The original edition with live chat replay is also available: https://youtu.be/mYWJ-b3lkfQ

Join us for a live Q&A as I discuss the current market with Michael Invests – host of his own channel. https://www.youtube.com/channel/UC2FiWOXQosY8RU5bxQCqmIg

Go to the Walk The World Universe at https://walktheworld.com.au/

VIDEO

Join us tonight for a live discussion on investing over the past year, and what might be ahead – and ask a question live!

Join us for a live Q&A as I discuss the current property market with Edwin, our property insider.

This is an edited version of the livestream, the original, with chat replay is also available. https://youtu.be/3IDlbNoqmwU

https://www.ribbonproperty.com.au/ https://walktheworld.com.au/

Digital Finance Analytics (DFA) Blog

DFA Live Q&A HD Replay - Edwin Almeida: Property Insider [Podcast]

Play Episode

Pause Episode

Mute/Unmute Episode

Rewind 10 Seconds

1x

Fast Forward 30 seconds

00:00

/

01:35:59

Subscribe

Share

VIDEO

Join us for a live Q&A as I discuss the current property market with Edwin, our property insider.

https://www.ribbonproperty.com.au/

https://walktheworld.com.au/

Join us for a live Q&A as I discuss the current markets with Nucleus Wealth Head of Investment Damien Klassen. This is an edited HD edition. The original, with live chat replay is at: https://youtu.be/FZMeB0PTE50

Go to the Walk The World Universe at https://walktheworld.com.au/

Digital Finance Analytics (DFA) Blog

DFA Live HD Replay: Santa Rally Or Bust? [Podcast]

Play Episode

Pause Episode

Mute/Unmute Episode

Rewind 10 Seconds

1x

Fast Forward 30 seconds

00:00

/

01:33:45

Subscribe

Share

VIDEO

This is the edited edition of our latest live show.

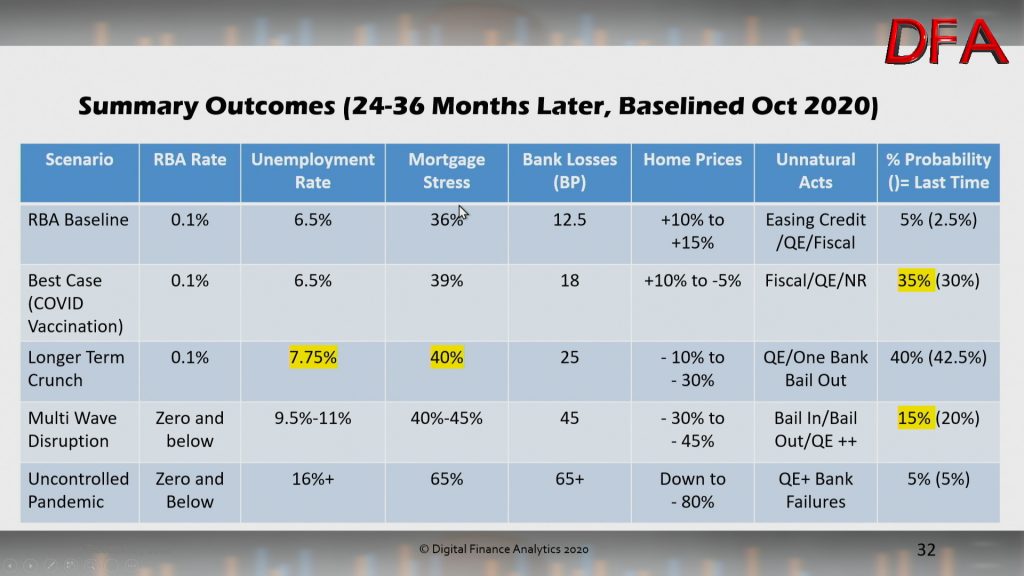

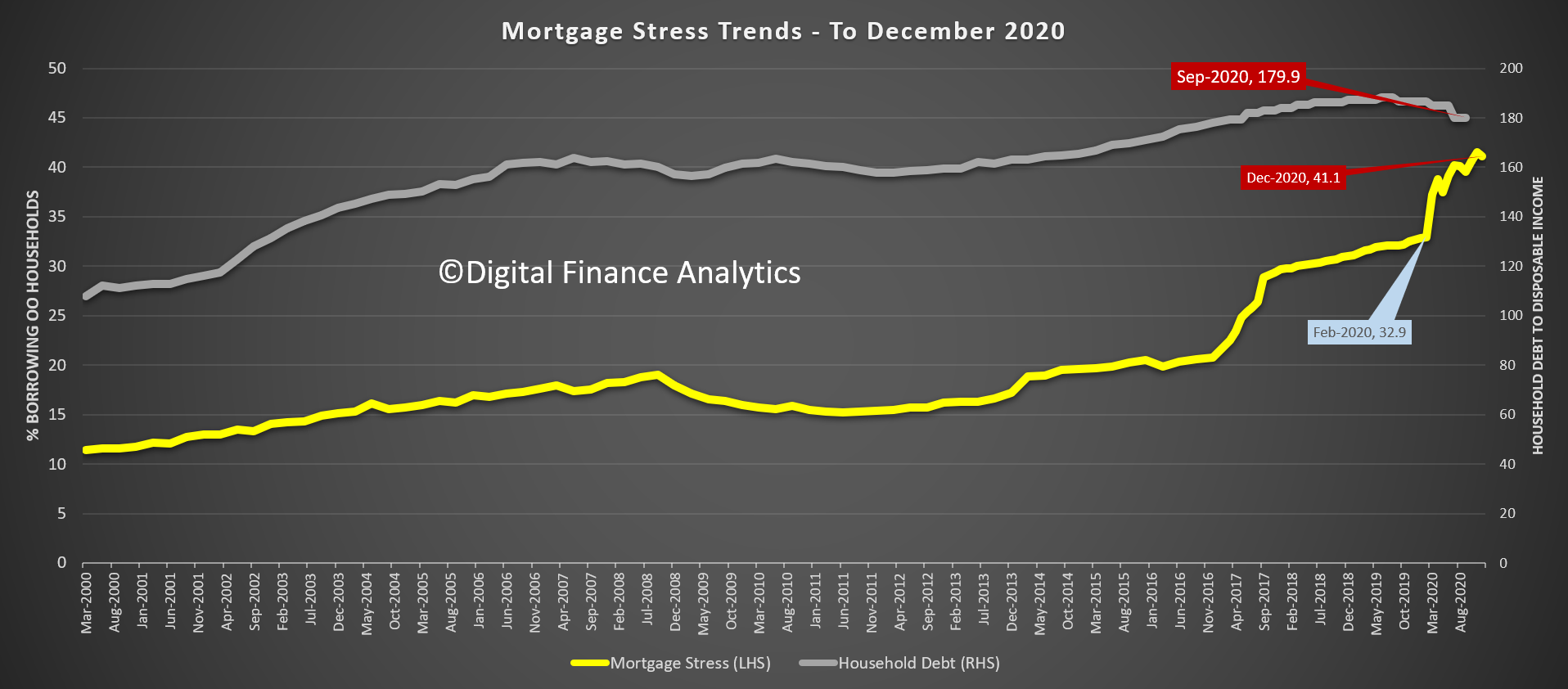

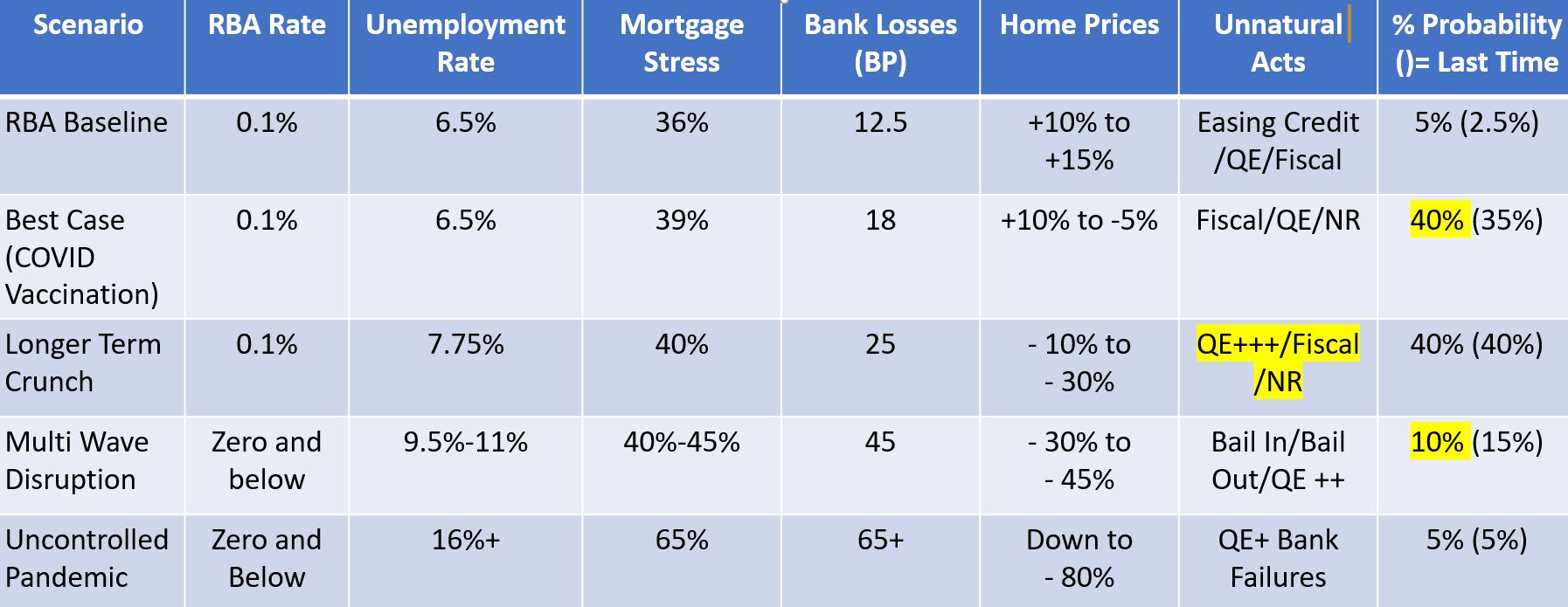

Join us for a live Q&A as I discuss the latest results from our surveys and explore the impact at a post code level.

00:00 Start

https://walktheworld.com.au/

Original edition with live chat replay at: https://youtu.be/6h4730QSG94

The latest edition of our finance and property news digest with a distinctively Australian flavour.

Go to the Walk The World Universe at https://walktheworld.com.au/

This is the edited edition of our latest live show.

00:00 Start

https://walktheworld.com.au/

Original edition with live chat replay at: https://youtu.be/6h4730QSG94

Digital Finance Analytics (DFA) Blog

DFA Live Q&A HD Replay - Scenario and Stress Update [Podcast]

Play Episode

Pause Episode

Mute/Unmute Episode

Rewind 10 Seconds

1x

Fast Forward 30 seconds

00:00

/

01:36:47

Subscribe

Share

Blog")