Having looked at events in the Property Market in 2016, we now turn to our expectations for 2017. There are many uncertainties which may impact the market, but using our surveys and modelling as a guide, we can make some educated guesses.

First, mortgage rates will be higher by the end of 2017 than they are now. We have already seen the impact of the Trump Effect on capital markets, and these higher costs are already flowing into higher mortgage rates. This process will continue as banks fight for a share of the deposit market, and at the same time continue to build their capital buffers. We think, on current trajectory rates could rise by more than half a percent, meaning the average repayment mortgage would rise by over $100 a month next year. Larger mortgages would rise by much more.

The RBA is unlikely to cut rates, and it is possible they may lift later in 2017 – but as the cash rate is disconnected from the mortgage rate, this is not necessarily such an important factor as in previous decades.

Many younger households are already using more than half their disposable income to repay their mortgage, and any increase will be very painful in a low income growth environment. We do not expect real incomes to rise at all next year, despite the rising costs of living and higher mortgage repayments.

As a result, we expect mortgage delinquency rates to continue to rise. There will be specific hot spots in the mining belts of Western Australia and Queensland, and we also expect to see problems emerging in the high-rise areas of Melbourne and Brisbane.

Households with a variable rate interest only loan will find their repayments rise more, with a half percent rise in rates translating to a monthly rise in repayments of $146. This illustrates the two problems with interest only loans, first they are more leveraged, so sensitive to rate changes, and second, households still have to find a way to repay the capital. No surprise therefore that the regulators have been forcing the banks to ensure interest only loan holders have a repayment plan, something which many currently do not possess. One third of borrowers could be impacted.

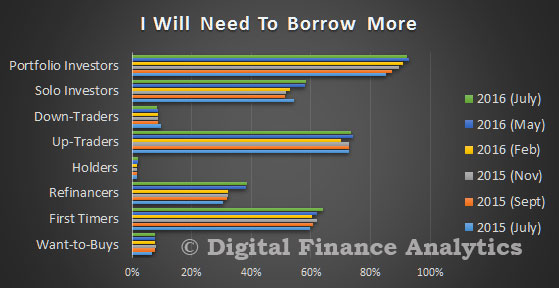

Mortgage finance will still be available, although we expect to see further tightening in underwriting standards, meaning that households will need larger deposits, and will not be able to borrow as much. Remember that our banks rely on mortgage book growth to sustain their business models, so the supply will not be turned off. We also expect to see ongoing lending from the non-traditional banking sector. Recently some of these players have been extending credit – at higher interest rates – to non-conforming loans, and foreign investors. This will continue. Regulation of the non-bank sector needs to be addressed.

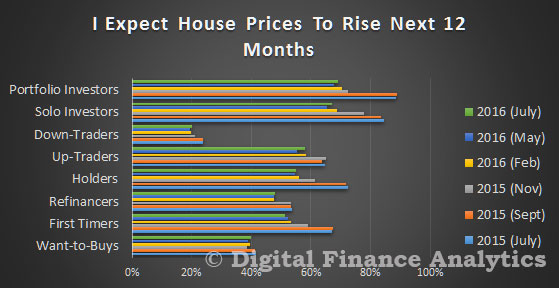

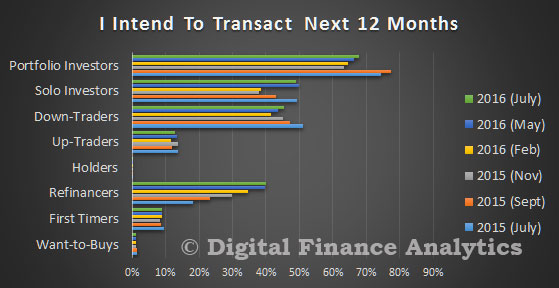

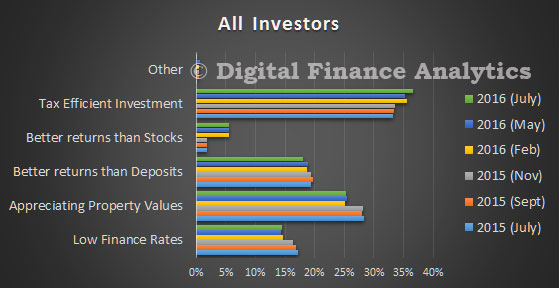

We expect property investors to continue to pile into the market, especially in the eastern states, so the volume of investment loans will continue to rise. A high proportion of these will be interest only loans. Given the current tax settings, where negative gearing and capital gains assist investors, many see this as the best investment option, including those in a self-managed super fund.

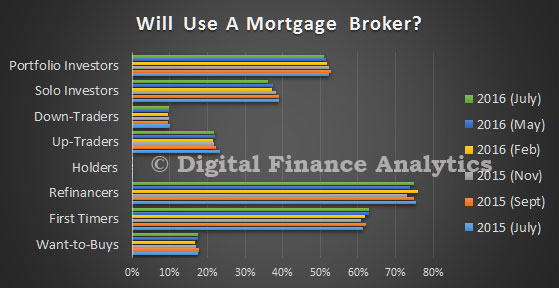

We expect momentum in owner occupied lending will slow, as the rate of refinancing eases. In the first part of the year, we expect a rise in the volume of fixed rate loans, as households decided to fix at a rate lower than the market’s expectation. But beware, most fixed loans already imply a hike in rates, so many of the best deals have already gone. More households will turn to mortgage brokers for assistance, and we expect they will grow their market share to well above fifty percent.

Foreign investors will still be attracted to the market here, and migration will continue, so we expect to see ongoing support to prices in the main markets of Sydney and Melbourne and they will remain above long term fundamentals.

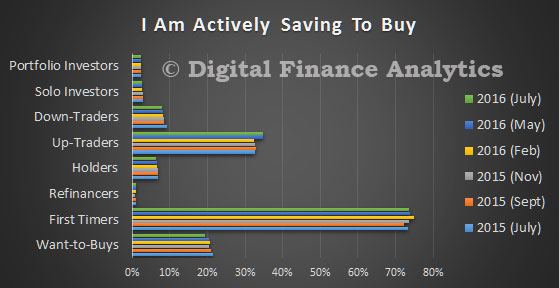

First time buyers will continue to be squeezed from the market, thanks to higher underwriting standards and flat incomes. A proportion of these households will choose to go direct to the investment sector as a result.

But net-net, demand will remain strong, auction clearance rates will be elevated, and property in many places will be in short supply.

As a result, we think home prices will in most centres continue to rise. We are certainly not anticipating a dramatic fall. This is because supply of new property is likely to slow in line with the fall in building approvals.

There will be specific areas across Australia however where prices are likely to fall. We expect further weakness in Western Australia and Queensland, and also in the apartment markets in Brisbane and Melbourne, as well as across a number of regional centres. But the core Sydney market, and houses in the broader Melbourne and Brisbane markets will remain strong.

We are expecting underemployment to become an important thematic next year. Many households, even those with multiple jobs, are not getting the levels of income they need to maintain their lifestyle. Whilst the core unemployment rate is unlikely to rise significantly, cash flow with be a major issue for many households. As a result, we do not expect to see any significant growth in personal credit – other than in the short-term credit sector, where online origination will stimulate demand. Household mortgage stress will continue to rise.

A number of factors are likely to weigh on household financial confidence next year. Rises in mortgage repayments, flat incomes and rising costs will all take their toll. However, ongoing property price growth, higher returns on bank deposits and higher stock market prices will counteract the drag. We expect property investors and home owners in the eastern states to remain quite bullish, despite depressed rental income growth. However, in WA, QLD and some regional centres, and among those living in rented accommodation, confidence will be significantly lower.

Banks will largely be able to buttress their profits, thanks to improved margins and low levels of mortgage default. As a result, we think the majors will mostly be able to maintain their payouts to their shareholders at current levels. Regional banks will remain under severe pressure, and we are not convinced that their drive to move to advanced capital models will be a panacea. We will also know the required final capital settings from Basel. We expect banks will need to hold more capital, and the benefits of advanced capital models be further reduced.

So in summary, expect higher mortgage rates and delinquencies to slow the property market a little, but momentum in the major centres is unlikely to stall completely because the banks need mortgage book growth to sustain their businesses. As a result, we expect household debit to be extended further.

Finally, a word on the broader economy. Housing momentum is not sufficient to replace the drop-off in mining investment, and given the reluctance of businesses to invest in growth, we think overall growth will still be sluggish. We might get a free kick from higher commodity prices – if they continue – but we do not have a realistic path to sustained growth. This structural issue needs to be addressed, and soon, if in the longer term the property market is to not go into a spiral of decline. However, we do not think 2017 will be the start of that down cycle.