I caught up with Stephan Livera of Bitcoin Podcast fame https://stephanlivera.com/about/ to discuss Bitcoin and where it stands today, and where it might head in the future.

Blog")

/

RSS Feed

Digital Finance Analytics (DFA) Blog

"Intelligent Insight"

I caught up with Stephan Livera of Bitcoin Podcast fame https://stephanlivera.com/about/ to discuss Bitcoin and where it stands today, and where it might head in the future.

I discuss the upcoming halving of Bitcoin in May with Adrian Przelozny, CEO of local crypto exchange Independent Reserve.

Is the Bank of England right to say its trading volatility means Bitcoin cannot be a real currency?

Economist John Adams and Analyst Martin North discuss the trend towards zero interest rates, the removal of cash from circulation, and the use of digital currency to control the system.

Is the black economy initiative all that it seems to be?

When I made my first video on Digital and Cyber Currencies – What Is Money? I said I would return to Bitcoin.

Now, today I am not going to discuss the mechanics of the digital currency, there are plenty of others who have done that; nor am I going to discuss the limited supply, which is mirroring gold, other than to note this one of the fundamental design criteria of the crypto currency.

Now, today I am not going to discuss the mechanics of the digital currency, there are plenty of others who have done that; nor am I going to discuss the limited supply, which is mirroring gold, other than to note this one of the fundamental design criteria of the crypto currency.

But institutional investors are getting more interested.

For example, Goldman Sachs announced it will be opening a crypto derivatives trading desk “within weeks,” as well as recently hiring a cryptocurrency trader as vice president of their digital asset markets. It will trade Bitcoin futures in a principal, market-making capacity and will also create non-deliverable forward products.

Then last week there was some more potentially important news out of the USA. There are rumours that the New York Stock Exchange may be planning to offer ‘Physical Delivery’ of Bitcoin. If this is true, it could mark a significant transformation in the role of digital currencies like Bitcoin.

The suggestion from unnamed “multiple sources” is that NYSE’s parent company Intercontinental Exchange or ICE is planning to offer Bitcoin (BTC) swap contracts but these contracts would be settled with the delivery of Bitcoin itself. Think about that, a mechanism to allow the physical delivery of a digital currency. If this IS true, this would have significant consequence for the future of crypto.

While there are Bitcoin futures contracts currently being offered on Chicago based CME Group derivatives marketplace or CME (since December 2017) and Chicago Board Options Exchange CBOE, these are ultimately settled in dollars.

The suggested crypto swap contracts would be settled in Bitcoin, and this would be a significant milestone which may signal a major Wall Street adoption of crypto.

Significantly it could mean that the ICE has a custody solution. As Bitcoin are generally bearer instruments it means you have to have a third-party custody option if institutional investors are going to get seriously involved.

There are so called “Cold storage custodian solutions” offered by small operators.

It’s not clear whether ICE is likely to build an in-house cold storage solution or to outsource it. In fact, ICE has made no comment at all on this, so it might be just speculation.

But here’s the thing, if ICE can offer a custodian solution that meets SEC rules and compliance requirements, this could “open the floodgates” to institutional capital, resulting in some “big price moves” in the crypto markets.

A custody solution would also open the door for pensions and endowments and so become an emergent asset class…most obviously at the expense of gold.

The Bitcoin price is still sitting well below the previous highs and the markets did not really respond to the rumours. But if this is true, then it may mark a significant inflection point in evolution of crypto. It might go mainstream.

The Bank for International Settlements Committee on Payments and Market Infrastructures has released a report “Central bank

digital currencies“. It looks at both wholesale and more generally available models. The former, they say might be useful for payments but more work is needed to assess the full potential. Although a CBDC would not alter the basic mechanics of monetary policy implementation, its transmission could be affected. A general purpose CBDC could have wide-ranging implications for banks and the financial system. Customer deposits may become less stable, as deposits could more easily take flight to the central bank in times of stress.

Interest in central bank digital currencies (CBDCs) has risen in recent years. The Committee on Payments and Market Infrastructures and the Markets Committee recently completed work on CBDCs, analysing their potential implications for payment systems, monetary policy implementation and transmission as well as for the structure and stability of the financial system.

CBDC is potentially a new form of digital central bank money that can be distinguished from reserves or settlement balances held by commercial banks at central banks. There are various design choices for a CBDC, including: access (widely vs restricted); degree of anonymity (ranging from complete to none); operational availability (ranging from current opening hours to 24 hours a day and seven days a week); and interest bearing characteristics (yes or no).

Many forms of CBDC are possible, with different implications for payment systems, monetary policy transmission as well as the structure and stability of the financial system. Two main CBDC variants are analysed in this report: a wholesale and a general purpose one. The wholesale variant would limit access to a predefined group of users, while the general purpose one would be widely accessible.

Wholesale CBDCs, combined with the use of distributed ledger technology, may enhance settlement efficiency for transactions involving securities and derivatives. Currently proposed implementations for wholesale payments – designed to comply with existing central bank system requirements relating to capacity, efficiency and robustness – look broadly similar to, and not clearly superior to, existing infrastructures. While future proofs of concept may rely on different system designs, more experimentation and experience would be required before central banks can usefully and safely implement new technologies supporting a wholesale CBDC variant.

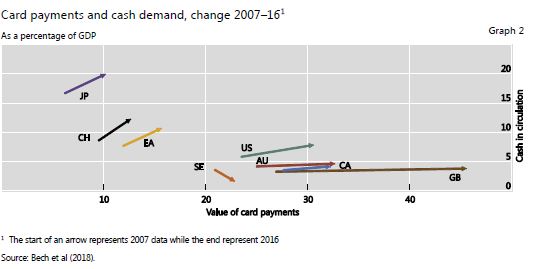

In part because cash is rapidly disappearing in their jurisdiction, some central banks are analysing a CBDC that could be made widely available to the general public and serve as an alternative safe, robust and convenient payment instrument.

In circumstances where the traditional approach to the provision of central bank money – in physical form to the general public and in digital form to banks – was altered by the disappearance of cash, the provision of CBDC could bring substantial benefits.

However, analysing whether these goals could also be achieved by other means is advisable, as CBDCs raise important questions and challenges that would need to be addressed. Most importantly, while situations differ, the benefits of a widely accessible CBDC may be limited if fast (even instant) and efficient private retail payment products are already in place or in development.

Although a general purpose CBDC might be an alternative to cash in some situations, a central bank introducing such a CBDC would have to ensure the fulfilment of anti-money laundering and counter terrorism financing (AML/CFT) requirements, as well as satisfy the public policy requirements of other supervisory and tax regimes. Furthermore, in some jurisdictions central banks may lack the legal authority to issue a CBDC, and ensuring the robust design and operation of such a system could prove to be challenging. An anonymous general purpose CBDC would raise further concerns and challenges. Although it is unlikely that such a CBDC would be considered, it would not necessarily be limited to retail payments and it could become widely used globally, including for illegal transactions. That said, compared with the current situation, a non-anonymous CBDC could allow for digital records and traces, which could improve the application of rules aimed at AML/CFT.

The introduction of a CBDC would raise fundamental issues that go far beyond payment systems and monetary policy transmission and implementation. A general purpose CBDC could give rise to higher instability of commercial bank deposit funding. Even if designed primarily with payment purposes in mind, in periods of stress a flight towards the central bank may occur on a fast and large scale, challenging commercial banks and the central bank to manage such situations. Introducing a CBDC could result in a wider presence of central banks in financial systems. This, in turn, could mean a greater role for central banks in allocating economic resources, which could entail overall economic losses should such entities be less efficient than the private sector in allocating resources. It could move central banks into uncharted territory and could also lead to greater political interference.

Last week, the Anti-Money Laundering and Counter-Terrorism Financing Amendment Bill 2017 was passed into law. The new law, for the first time, regulates Australia’s growing digital currency sector. Similar measures are already in place in the US, Canada and the EU.

It amended the Anti-Money Laundering and Counter-Terrorism Financing Act 2006 to:

One important change was that operators of Australian exchanges for Bitcoin and other digital currencies will now need to register with the country’s anti-money laundering agency.

It also sets out the conditions under which they may trade.They must identify and verify their customers, keep records of transactions, report threshold transactions and suspicious matters, and run an anti-money laundering and counter-terror financing program.

It is now a criminal offence to provide digital currency exchange services without being registered with AUSTRAC and penalties for non-compliance start from two years’ jail and/or $105,000 for failing to register. They go as high as seven years jail and $2.1 million in penalties for corporations and $420,000 for individuals for severe offences.