/

RSS Feed

Digital Finance Analytics (DFA) Blog

"Intelligent Insight"

We look at the REPO market and how it may being used to cook the books, as highlighted by the Bank for International Settlements.

We discuss the latest APRA Banking Performance Data

We review the latest finance and property news from an distinctively Australian perspective

We discuss the latest employment data and the FED’s rate hike

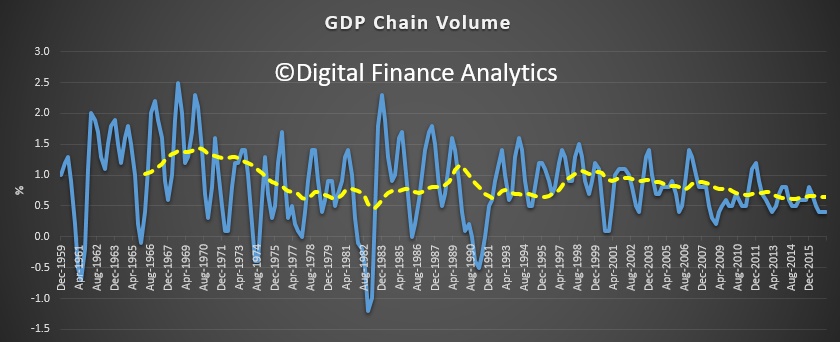

Data from the Australian Bureau of Statistics (ABS) shows the pace of growth of the Australian economy slowed in the March quarter to 0.3 per cent in seasonally adjusted chain volume terms. Through the year, GDP grew 1.7 per cent.

Investment in new housing fell by 4.4 per cent in the March Quarter 2017 which brings the sector down from record high investment in December 2016 and back to levels similar to those experienced at the start of 2016.

As Saul Estlake noted in The Conversation today:

It’s now been 103 quarters (25 years and 9 months) since Australia last had consecutive quarters of negative growth in real gross domestic product (GDP), in the March and June quarters of 1991.

Contrary to much-repeated claims, the Netherlands didn’t experience more than a quarter-century of economic growth without consecutive quarters of negative real GDP growth between the early 1980s and the global financial crisis.

The Netherlands’ real GDP declined by 0.3% in the June quarter of 2003, and by 0.01% in the September quarter of that year, according to data published by Statistics Netherlands and, separately, by the OECD. So, at best, the Netherlands went for only 22 years without experiencing a recession. Australia surpassed that benchmark in 2013.

Yes, that second quarterly decline in 2003 was almost imperceptible. But sporting records are delineated by margins as small as one one-hundredth of a second, so we can’t blithely discount a -0.01% fall in real GDP as “not relevant”.

Even if you blinked and missed that tiny second successive decline in real GDP in the September quarter of 2003, the Netherlands still wouldn’t hold the record for the longest run of continuous economic growth. That belongs to Japan – which, according to OECD data, went from the March quarter of 1960 to the March quarter of 1993 without ever registering two or more consecutive quarters of negative growth in real GDP. That’s 133 quarters, or more than 33 years.

Indeed, if Japanese GDP data were available on a quarterly basis earlier than 1960 it’s likely that this run of continuous economic growth would have been even longer, perhaps as long as 38 years, inferring from annual data available back to 1955. So Australia would need to avoid consecutive quarters of negative real GDP growth until at least 2024 if it is truly to be able to claim this “world record” as its own.

Even more importantly, the definition of a technical recession as (two or more consecutive quarters of negative growth in real GDP) is, as former RBA Governor Glenn Stevens said, “not very useful”. It was originally proposed in December 1974 by Julius Shishkin, who at that time was the head of the Economic Research and Analysis Division of the US Census Bureau (now the Bureau of Economic Analysis, which publishes the US national accounts).

It’s not used to identify recessions in the US. It takes no account of differences over time, or as between countries, in the rates of growth of either population or productivity – which are the key determinants of whether a given rate of economic growth is sufficient to prevent a sharp rise in unemployment. This is something which most people (other than economists) would use to delineate a recession.

While Australia has avoided consecutive quarterly contractions in real GDP since the first half of 1991, we’ve had two periods of consecutive quarterly declines in real per capita GDP (in 2000 and 2006). We’ve also had two periods of consecutive quarterly declines in real gross domestic income or GDI, which takes account of income gains or losses accruing from movements in Australia’s terms of trade (in 2008-09, and in 2014). Perhaps most meaningfully of all, Australia has had two episodes where the unemployment rate has risen by one percentage point or more in 12 months or less (in 2001 and 2009).

That’s still a better track record than almost any other advanced economy during the past quarter-century or so – and it reflects well on the quality of economic management (and the nature of our luck) over this period. Nonetheless, we shouldn’t be in the business of awarding ourselves prizes to which we’re not entitled.

And the long term trend also highlights a slowing, so we need new growth engines if we are to keep the growth ball in the air!

Growth was recorded across the economy with 17 out of 20 industries growing during the quarter. Strong growth was observed within the service industries including Finance and Insurance Services, Wholesale Trade, and Health Care and Social Assistance.

Agriculture, Forestry and Fishing decreased after strong growth in the previous two quarters, while Manufacturing decreased for the tenth time in eleven quarters.

Chief Economist for the ABS, Bruce Hockman said; “This broad-based growth was tempered by falls in exports and dwelling investment. Dwelling investment declined in all states, except Victoria, and overall is the largest decline for Australia since June 2009.”

Compensation of employees (COE) increased 1.0 per cent in the March quarter, a pick up from the negative growth recorded in the December quarter, and is consistent with other labour market data. COE is still only 1.5 per cent higher through the year, continuing to contribute to the reduction in the household saving rate. The household saving ratio fell to 4.7 in the March quarter, half the rate it was in March quarter 2013.

Mr Hockman said; “Even though there was a fall in dwelling investment this quarter, levels are still historically high. There was also positive growth in household consumption, albeit in non-discretionary items such as electricity and fuel purchases. The softer growth in household consumption is broadly in line with modest income growth.”

Once in a while an insight will change the world. In this months Bank of England’s Quarterly Bulletin (2014 Q1), there is an article on money creation, and an primer on money. Actually these were pre-released on 12 March, and both are worth a read.

In the primer on money, we are reminded that it is essentially a trusted IOU and there are three main types, currency, bank deposits and central bank reserves. Each form is really an IOU between one sector of the economy and another. In the modern economy, most money is in the form of bank deposits, which are created by the commercial banks.

You can see a video made by the bank here.

You can see a video made by the bank here.

The second article though is revolutionary, in that is has the potential to rewrite economics. “Money Creation in the Modern Economy” turns things on their head, because rather than the normal assumption that money starts with deposits to banks, who lend them on at a turn, they argue that money is created mainly by commercial banks making loans; the demand for deposits follows.

“In the modern economy, most money takes the form of bank deposits. But how those bank deposits are created is often misunderstood: the principal way is through commercial banks making loans. Whenever a bank makes a loan, it simultaneously creates a matching deposit in the borrower’s bank account, thereby creating new money. The reality of how money is created today differs from the description found in some economics textbooks:

• Rather than banks receiving deposits when households save and then lending them out, bank lending creates deposits.

• In normal times, the central bank does not fix the amount of money in circulation, nor is central bank money ‘multiplied up’ into more loans and deposits.

Although commercial banks create money through lending, they cannot do so freely without limit. Banks are limited in how much they can lend if they are to remain profitable in a competitive banking system. Prudential regulation also acts as a constraint on banks’ activities in order to maintain the resilience of the financial system. And the households and companies who receive the money created by new lending may take actions that affect the stock of money — they could quickly ‘destroy’ money by using it to repay their existing debt, for instance. Monetary policy acts as the ultimate limit on money creation. The Bank of England aims to make sure the amount of money creation in the economy is consistent with low and stable inflation. In normal times, the Bank of England implements monetary policy by setting the interest rate on central bank reserves. This then influences a range of interest rates in the economy, including those on bank loans. In exceptional circumstances, when interest rates are at their effective lower bound, money creation and spending in the economy may still be too low to be consistent with the central bank’s monetary policy objectives. One possible response is to undertake a series of asset purchases, or ‘quantitative easing’ (QE). QE is intended to boost the amount of money in the economy directly by purchasing assets, mainly from non-bank financial companies. QE initially increases the amount of bank deposits those companies hold (in place of the assets they sell). Those companies will then wish to rebalance their portfolios of assets by buying higher-yielding assets, raising the price of those assets and stimulating spending in the economy. As a by-product of QE, new central bank reserves are created. But these are not an important part of the transmission mechanism. This article explains how, just as in normal times, these reserves cannot be multiplied into more loans and deposits and how these reserves do not represent ‘free money’ for banks.”

They made a video which explains some of the key concepts.

This could be seen as a self-justification for the years of QE, and low interest rates in the UK, but I think it is really a radical insight. The world of money just changed!