In recent years, developed countries have experienced a change in the age composition of their population. In particular, these countries have seen an increase in the age-dependency ratio, computed as the ratio of the young population (under 15) and elderly population (65 and over) to the working-age population (15 to 64).

Because the young and the elderly are the most likely to be economically dependent, analyzing their recent evolution may help us understand how changes in the age-dependency ratio could affect other economic outcomes in the developed world. In particular, the evolution of the three variables making up the age-dependency ratio—the elderly population, the young population and the working-age population—is of interest.

The figure below plots the annual age-dependency ratio for the G-7 countries over the period 1990-2012. In recent years, all these countries have experienced an increase in age-dependency ratios.

Among the G-7, Japan has experienced the largest increase in its age-dependency ratio. It was also the country where these demographic trends started first.

From the early 90s, Japan has seen a large increase in its elderly population, with 25 percent of its total population being 65 and older in 2014. Its age-dependency ratio was 61 percent.

In all the G-7 countries, the increase in the age-dependency ratio has been driven by an increase in the elderly population together with a decrease in the working-age population. This increase has happened despite a decrease in the young population ratio in all of the G-7 countries. The young, working-age and elderly populations as percentages of the entire populations of countries are shown in the figures below.

The decrease in the young population may also pose problems for the economic future of countries, since it is likely going to contribute to a reduction in labor force participation in the long run. Indeed, fertility has been declining in all these countries.

A decrease in the labor force due to demographic trends may result in a slowing down of economic growth. This could eventually spill over to developing economies. Policies aimed at alleviating these problems could address increasing productivity to counteract a shrinking working population or stimulating the labor force participation of the elderly population.

Interesting post from the Federal Reserve Bank of ST. Louis, shows that Counties with severe declines in housing net worth during the 2007-09 recession experienced larger declines in employment.

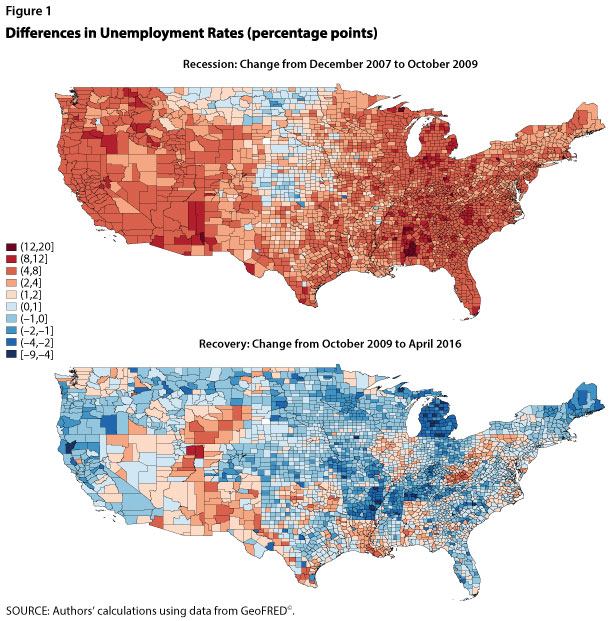

The U.S. national labor market has recovered from the effects of the 2007-09 recession. The national unemployment rate was 10 percent at the end of 2009 but now stands at only 4.7 percent, which the Federal Open Market Committee considers close to the rate’s long-run value.1 Despite the national labor market recovery, significant regional variation remains. Recent economic research highlights links between regional labor and housing markets. This essay examines the recent recession and recovery by plotting county-level unemployment rates and changes in houses prices and finds a negative correlation between the two.

National unemployment reached its pre-recession low in December 2007, with the unemployment rate in 1 in 3 counties below 4 percent. Regions with higher unemployment rates included the West Coast, Central South, and Upper Peninsula of Michigan. The Midwest and South, from Minnesota to Texas, had the lowest unemployment rates—below 3.5 percent in most counties. As the recession deepened, unemployment rates rose until only 1 in 15 counties remained below 4 percent. Figure 1 shows the percentage-point changes in county-level unemployment rates from the pre-recession low to the peak of the U.S. unemployment rate (December 2007 to October 2009) and from the peak to the most recent data (December 2007 to April 2016). Shades of red (blue) indicate increases (decreases) in county unemployment rates.2 As shown in the top panel, by October 2009, the unemployment rate in most counties increased between 4 and 20 percentage points. The areas with higher unemployment rates before the recession experienced larger increases in unemployment during the recession. For a strip of counties in the Midwest, the unemployment rate remained low, increased only slightly, or even declined.

As shown in the bottom panel of Figure 1, although some county-level unemployment rates remain slightly above their pre-recession levels, most have recovered to or below those levels. As prior to the recession, the unemployment rate in about 1 in 3 counties is below 4 percent. The unemployment rates in most counties in Arizona, New Mexico, Nevada, and Utah remain above their pre-recession levels, while counties in the Midwest remain mostly below their pre-recession levels.

Why did unemployment rise so severely in some areas but stay low in others? One explanation may be related to the elasticity of the housing supply. Gascon, Arias, and Rapach (2016) argue that areas with an inelastic housing supply (i.e., the supply does not respond much to changes in house prices) are more vulnerable to recessions and experience worse downturns than areas with a more elastic supply. An inelastic housing supply leads to larger house price drops and declines in net worth during downturns, leading to larger declines in local consumption spending that further depress the local economy. Mian and Sufi (2014) show that counties with severe declines in housing net worth during the 2007-09 recession experienced larger declines in employment.3

We illustrate this correlation using county-level house price data from the CoreLogic Home Price Index. The scatter plots in Figure 2 show for the two periods noted above, respectively, the percent change in county house prices relative to the percentage-point change in the county unemployment rate, weighted by the county population in 2007.4 The size of each dot represents the county population. The figure shows a strong negative correlation between changes in house prices and changes in the unemployment rate: During the recession, counties with larger decreases in house prices experienced larger increases in the unemployment rate (left panel), while during the expansion the opposite has been true (right panel).

2 We downloaded county-level unemployment data from GeoFRED® and then applied the Census Bureau’s X-13 ARIMA seasonal adjustment program to look at percentage-point changes in the unemployment rate from peak to trough and from peak to peak.

3 Mian and Sufi (2014) show that housing net worth mostly affects nontradable employment, or employment in industries that are not tradable outside the local labor areas. For example, restaurants and retail shops are nontradable, while agriculture production is tradable.

4 Because county-level house price data are not as available as unemployment rate data, fewer counties are included in Figure 2 than Figure 1. House price data were also seasonally adjusted using the Census Bureau’s X-13 ARIMA seasonal adjustment program. April 2016 is the most recent month for which county-level house price data are available.

A few key economic indicators may give some forecasters reason to think a recession is on the horizon. But when put into historical context, it seems that the economy is still expanding heading into the last half of the year.

On July 29, the Bureau of Economic Analysis (BEA) released the advance estimate for second-quarter gross domestic product (GDP). Also included in this report was the annual update to the national income accounts that resulted in revisions to the past three years of data.

The advance estimate indicated that real GDP rose at a 1.2 percent annual rate in the second quarter.1 Although the economy rebounded modestly from its anemic growth rate of 0.8 percent in the first quarter, the advance estimate was much weaker than the consensus estimate of 2.6 percent.2

Moreover, the BEA reported that real GDP growth was measurably weaker over the previous three quarters (2015:Q3 to 2016:Q1) than earlier estimates suggested. As a result, real GDP growth over the past four quarters now stands at 1.2 percent, its lowest four-quarter growth rate in three years.3

Slowing Economic Growth Rate

As seen in the figure below, the economy’s growth rate has decelerated sharply since the first quarter of 2015 (3.3 percent). Although the economy’s growth rate is barely above 1 percent, there have been episodes over the past few years when growth had also slowed sharply. Thus, this episode may be another example of a temporary slowdown, the result of periodic shocks that hit the economy. Still, it is also possible that this slowing is the leading edge of something more substantial—perhaps a recession.

The state of the business cycle plays an important role in the St. Louis Fed’s new characterization of the U.S. macroeconomic and monetary policy outlook.4 In this characterization, the economy is viewed as operating in a specific regime that tends to be persistent. These regimes could be periods of low productivity growth or business expansion or recession. And since optimal monetary policy is dependent on the regime the economy finds itself in, identifying when the economy slides into a recession is vitally important.

Recession Checkpoints

Although recessions are rarely forecastable events, economists nonetheless have a variety of checkpoints for examining the state of the economy. One checkpoint is consumer expenditures, especially on big-ticket items like autos and appliances. The outlook appears reasonably good based on this indicator: Real expenditures on durable goods rose at a robust 8.4 percent rate in the second quarter and are up nearly 4.5 percent from a year earlier.

Two other checkpoints in the national income accounts are expenditures on residential and nonresidential fixed investment. Like durable goods, a person’s decision to buy a house or a business’s decision to invest in a piece of equipment or to build a new structure depends importantly on the individual’s or the firm’s expectation of future income and earnings (and profits), respectively.

During periods of slow or slowing growth, real incomes, earnings and profits tend to slow as well. In response, firms and households typically trim their current and future expenditures. This is why fixed investment outlays are highly cyclical—that is, sensitive to the state of the business cycle.

Here is where the clouds appear a bit more ominous:

On the business side, real nonresidential fixed investment (NRFI) declined at a 2.3 percent rate in the second quarter. This was the third consecutive quarterly decline in NRFI.

On the housing side, real residential fixed investment (RFI) fell at a 6.1 percent rate in the second quarter, its largest decline in nearly six years. The decline in real RFI was somewhat unusual given the recent strength in the housing sector.

A Historical Look at Fixed Investment

By employing the lens of history, the two figures below can help gauge whether the declines in real NRFI and RFI are likely to be temporary developments or potentially signaling the next recession.

Each figure shows the average growth rate eight quarters before and after the business cycle peak, as determined by the National Bureau of Economic Research. By definition, business expansions occur before the peak and recessions occur after the peak. Recessions are much shorter than expansions.

The average growth rates are culled from periods around the eight business cycle peaks that prevailed from the second quarter of 1960 to the fourth quarter of 2007. In the figures, the average growth before and after the recession is indicated by the orange line. The shaded areas indicate the range of values before and after the business cycle peak. The blue line shows the growth rate of each series from the first quarter of 2014 to the second quarter of 2016.

The cyclical indicator properties of each fixed investment series is seen in the figures. On the business side, the growth of real NRFI tends to be positive until the peak, but then growth turns negative, on average, for six consecutive quarters.

On the housing side, the growth of real RFI, on average, turns negative two quarters before the business cycle peak. The growth of real RFI then remains negative during the first two quarters of the recession. But as the shaded areas indicate, there are exceptions to this pattern for both series.

Recession Looming?

Are current fixed investment developments worrisome from an historical standpoint? Two points are worth noting. First, the recent pattern of negative real NRFI growth is somewhat different than the pattern typically seen prior to a business cycle peak. On average, negative NRFI growth is associated with negative real GDP growth for more than one quarter, and we have yet to see that in the current expansion. Subsequent revisions may show that the economy entered into a recession during the fourth quarter of 2015 or the first quarter of 2016, when real GDP growth was less than 1 percent, but that seems unlikely given the economic strength in other areas—especially labor markets.

Second, the decline in real RFI would be consistent with previous prerecession patterns if the U.S. economy was nearing a tipping point in the expansion. Recall that the message from the above figure was that housing usually leads the economy into the recession, posting negative growth rates six months before the peak.

At this point, the majority of industry analysts and professional forecasters remain optimistic about the housing sector over the remainder of 2016 and into 2017. Key positive developments in this regard include expectations of continued strength in labor markets, low mortgage interest rates and relatively high levels of housing affordability.

Conclusion

To sum up, the declines in residential and nonresidential fixed investment are worrying because they are often viewed as reliable leading indicators of the cyclical strength or weakness of the economy. Although economists and other economic analysts find it very difficult—if not impossible—to predict recessions in real time, the available evidence suggests that the economy, though exhibiting stubbornly weak real GDP growth, continued to expand heading into the second half of 2016.

Notes and References

1 Unless noted otherwise, growth rates are expressed at compounded annual rates using seasonally adjusted data.

2 Consensus forecasts for key economic data can be found on the Calendar of Releases cover page of the Federal Reserve Bank of St. Louis’ U.S. Financial Data.

3 Over the past four quarters, the decline in business inventory investment has subtracted 0.6 percentage points from real GDP growth. In the national accounts, final sales is the measure of GDP that removes the contributions to growth from changes in inventory investment. Thus, while growth is measurably stronger according to real final sales, the pattern of final sales growth has also shown the sharp deceleration noted in the figure for real GDP.

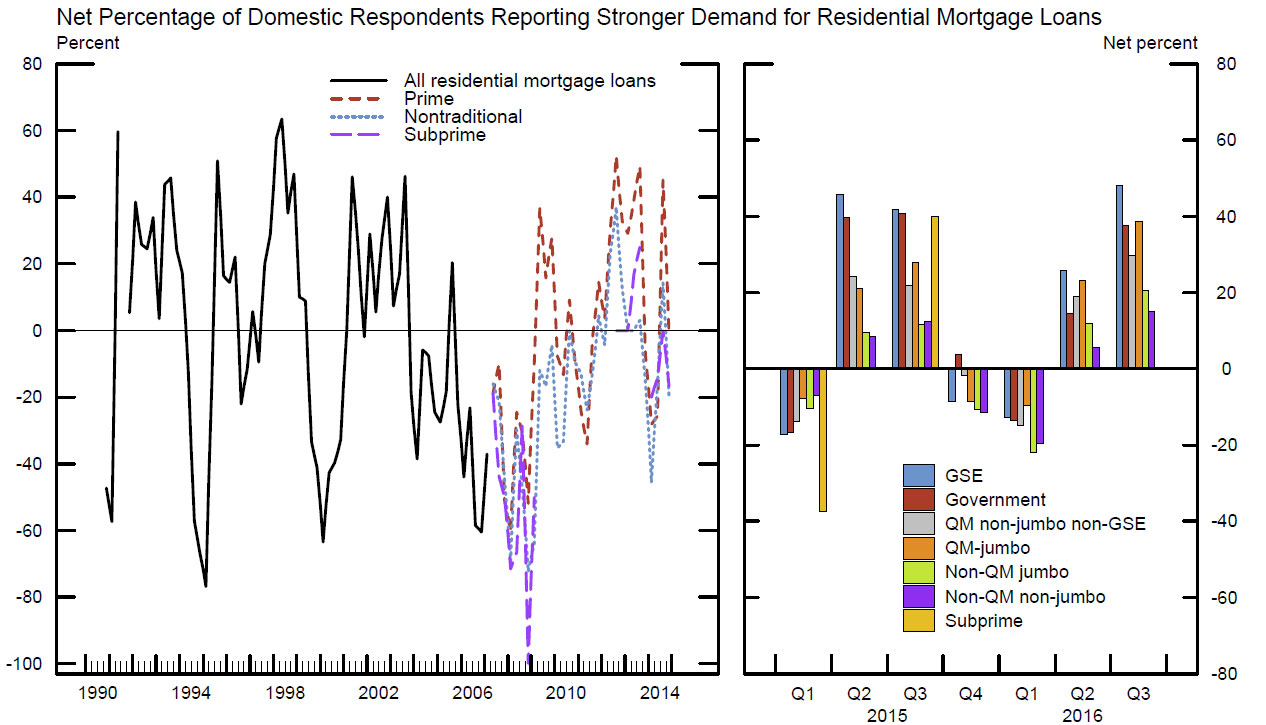

The FED says banks reported that demand for most types of Residential Real Estate loans strengthened over the second quarter.

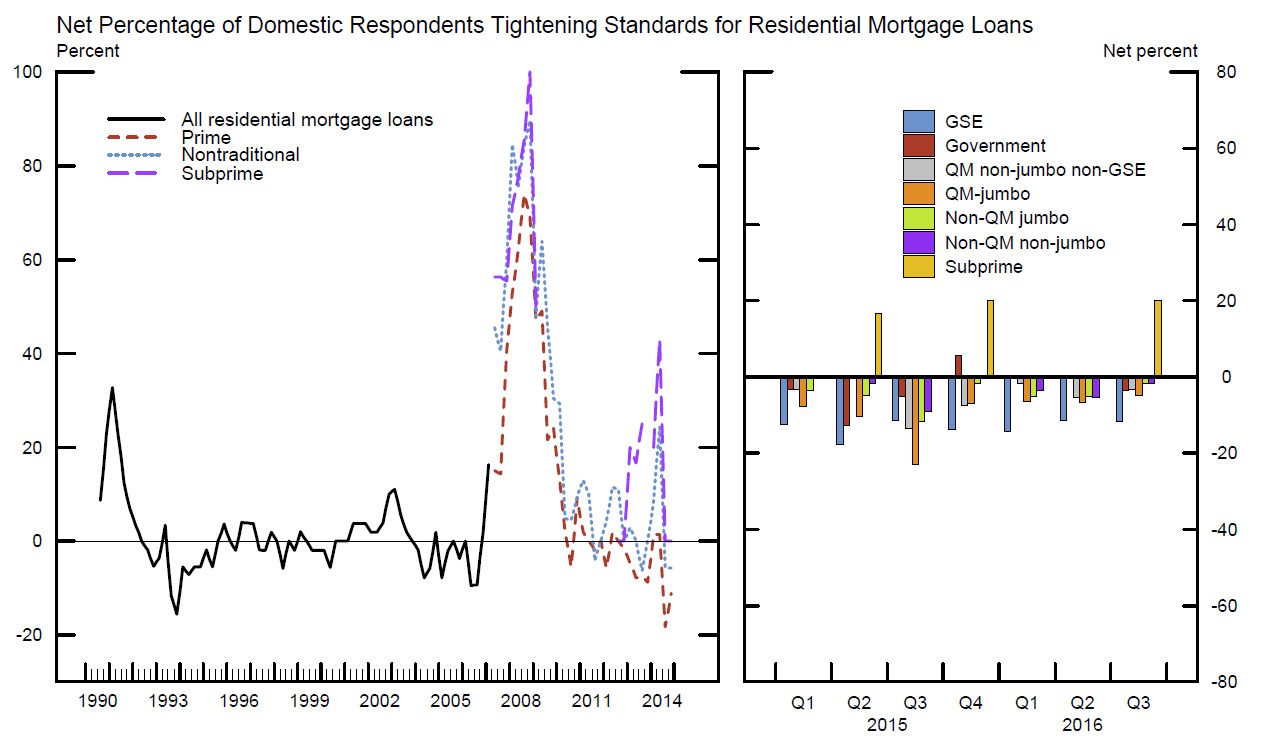

Responses to a set of special annual questions on the approximate levels of lending standards suggested that banks’ lending standards banks continued to report in the July 2016, that on balance, domestic banks lending standards for all five categories (GSE-eligible mortgages, government-insured mortgages, jumbo mortgages, subprime mortgages, and HELOCs) remained tighter than the midpoints of the ranges observed since 2005. Of note, a major net fraction of banks reported that the current level of standards on subprime residential mortgage loans is tighter than the reference point.

The report also discusses commercial lending and consumer loans.

Regarding loans to businesses, the July survey results indicated that, on balance, banks tightened their standards on commercial and industrial (C&I) and commercial real estate (CRE) loans over the second quarter of 2016. The survey results indicated that demand for C&I loans was little

changed, while demand for CRE loans had strengthened during the second quarter on net.

Banks’ lending standards for all categories of C&I loans are currently easier than the midpoints of the ranges that have prevailed since 2005, except

for syndicated loans to below-investment-grade firms. However, banks also generally indicated that standards on all types of CRE loans are currently tighter than the midpoints of their respective ranges.

Banks indicated that changes in standards on consumer loans were mixed, while demand strengthened across all consumer loan types.

The Fed just released their latest update on monetary policy, and once again kept the rate at its current low level. The tone of the note was slightly more positive. They are still chasing the 2% inflation target and underscore that future cash rate lifts will be slow. The market hardly moved on the news.

Information received since the Federal Open Market Committee met in June indicates that the labor market strengthened and that economic activity has been expanding at a moderate rate. Job gains were strong in June following weak growth in May. On balance, payrolls and other labor market indicators point to some increase in labor utilization in recent months. Household spending has been growing strongly but business fixed investment has been soft. Inflation has continued to run below the Committee’s 2 percent longer-run objective, partly reflecting earlier declines in energy prices and in prices of non-energy imports. Market-based measures of inflation compensation remain low; most survey-based measures of longer-term inflation expectations are little changed, on balance, in recent months.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee currently expects that, with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace and labor market indicators will strengthen. Inflation is expected to remain low in the near term, in part because of earlier declines in energy prices, but to rise to 2 percent over the medium term as the transitory effects of past declines in energy and import prices dissipate and the labor market strengthens further. Near-term risks to the economic outlook have diminished. The Committee continues to closely monitor inflation indicators and global economic and financial developments.

Against this backdrop, the Committee decided to maintain the target range for the federal funds rate at 1/4 to 1/2 percent. The stance of monetary policy remains accommodative, thereby supporting further improvement in labor market conditions and a return to 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. In light of the current shortfall of inflation from 2 percent, the Committee will carefully monitor actual and expected progress toward its inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant only gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction, and it anticipates doing so until normalization of the level of the federal funds rate is well under way. This policy, by keeping the Committee’s holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions.

Voting for the FOMC monetary policy action were: Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Lael Brainard; James Bullard; Stanley Fischer; Loretta J. Mester; Jerome H. Powell; Eric Rosengren; and Daniel K. Tarullo. Voting against the action was Esther L. George, who preferred at this meeting to raise the target range for the federal funds rate to 1/2 to 3/4 percent

Following the financial crisis, many new regulations have been implemented to address systemic risk within the U.S. financial system, including measures that address capital requirements, liquidity ratios and leverage levels, among others. Even with the enactment of the Dodd-Frank Act, which has yet to be fully implemented, debate continues as to whether “too big to fail” (TBTF) remains an issue or whether the legislation has mitigated this risk to the U.S. economy. Among those who believe TBTF remains a key problem for the U.S. economy, proposals to address the issue range widely. Recent symposiums held at the Minneapolis Fed, under the leadership of President Neel Kashkari, explored several of these proposals.1 In this column, I provide a brief overview of them and share some of my perspectives on the topic.

Some researchers, such as Simon Johnson from MIT, have suggested limiting bank size. Others, such as Anat Admati from Stanford, have suggested much higher capital requirements for large banks. A third proposal, by John Cochrane from Stanford, emphasizes changing the treatment of leverage in the tax code as a way to mitigate financial fragility. A fourth proposal seeks to improve the bankruptcy laws in a way that will allow a financial firm that is in trouble to more readily go through bankruptcy court. While this last proposal has garnered attention, it is also fraught with technical complications. Therefore, I will focus on the first three proposals.

Bank Size Limits: I have been an advocate of a system with smaller financial institutions which can be allowed to fail, if necessary. Generally speaking, however, size restrictions seem arbitrary. Why should a particular bank size be risky and another size not be risky? In addition, recent evidence suggests that substantial economies of scale exist, perhaps even for the largest financial institutions.2 Furthermore, the primary concern could be that complexity or interconnectedness is the trigger toward financial fragility rather than size itself. For these reasons, some analysts have concluded that a size restriction by itself may not be the most natural solution to the TBTF problem.

Higher Capital Requirements: Raising capital requirements for large financial institutions is emphasized in the Dodd-Frank Act. The idea is that higher capital requirements provide a larger buffer to absorb significant shocks to the institutions, reducing their risk of failure. Admati and others argue that capital requirements should be even larger, which would make their equity capital levels more comparable to those of nonbanks. These researchers also point out that banks had much higher levels of capital in earlier eras when owners and shareholders were personally liable for paying the banks’ creditors, if necessary.3 This suggests that the market solution is to have banks hold more capital than they do today.

Is there a connection between capital requirements and size requirements? Recent comments by Fed Gov. Jerome Powell and other Fed officials suggest that higher capital requirements may cause firms to rethink their optimal size.4 Some of the largest firms, such as GE Capital, have divested in an effort not to be designated as systemically important within the Dodd-Frank Act, a designation that can lead to higher capital requirements.

Leverage: Many have suggested that leverage—rather than capital—is the issue, in which case Cochrane’s proposal to rethink the tax treatment of leverage might be a good idea. Keep in mind what happened during the “tech” bubble in the late 1990s and early 2000s, when firms had to raise their financing through equity. Although investors lost money when the market crashed, the repercussions for the economy were not as significant as the crash of the housing bubble several years later. The U.S. tax system favors bond financing: Interest payments on debt instruments are tax-deductible, while dividend payments to shareholders are not. Giving a less favorable tax treatment to bond financing and a more favorable tax treatment to equity financing might lead to enhanced stability.

These are certainly interesting ideas, but there is also a global aspect. In particular, we have seen efforts on a global level to limit systemic risk through coordinated regulatory policies across countries. In my experience, however, other countries often seem to be less concerned about TBTF as an issue than we are in the U.S. There is sometimes a tendency to view large financial firms as national champions, deserving of protection. In part because of this, we are evolving globally toward a regulated utility model—whereby very large financial institutions are under heavy regulation, which in my view makes them unlikely to innovate effectively in the future. This may leave them vulnerable to coming waves of financial innovation. This is an additional consideration in the ongoing TBTF debate.

Last month, the Federal Reserve announced that 31 out of 33 U.S. banks had passed its latest “stress test,” designed to ensure that the largest financial institutions have enough capital to withstand a severe economic shock.

Passing the test amounts to being given a clean bill of health by the Fed. So are taxpayers – who were on the hook for the initial US$700 billion TARP bill to bail out the banks in 2008 – now safe?

But beyond this, the stress tests highlight a significant shortcoming in how regulators hope to prevent the next wave of bank failures: They’re focusing way too much on size, particularly with the designation of so-called systemically important, “too-big-to-fail” banks.

U.S. lawmakers in search of a solution are currently working on legislation that would make it easier for too-big-to-fail banks to actually fail through bankruptcy. While doing so would be a good thing, it still raises important questions.

Are policymakers right to focus on size in determining whether a bank poses a major risk to the financial system and taxpayers? Would splitting larger banks into smaller ones free taxpayers from the repeated burden of rescuing them during times of crisis? Does calling a bank “too big to fail” even mean anything?

To me, this focus on size and “too big to fail” seems misplaced. I’m among those who advocate replacing our current system with something known as “narrow banking,” which would totally separate deposits from riskier lending activities. This would have the best chance of protecting taxpayers from having to foot the bill for future bailouts, as I’ll explain below.

Dodd-Frank also says that banks and other companies that “could pose a threat to the financial stability of the United States” if they fail or engage in very risky activities must write bankruptcy plans known as living wills and meet stricter capital requirements.

Some policymakers contend that the increased regulation and capital are not enough and have called for breaking up big banks into smaller ones in order to reduce the probability of having to use taxpayer money to bail them out.

Neel Kashkari, president of the Minneapolis Fed, has called for breaking up the big banks.Brendan McDermid/Reuters

A question of size

In order to make sense of the too-big-to-fail slogan, we first must agree (or disagree) on what we mean by “big.” So, let us examine the biggest bank in the U.S.: JPMorgan Chase.

JPMorgan maintains about $1.39 trillion worth of deposits. Suppose we break up JPMorgan into four banks, each with approximately $348 billion of depositors’ money. Are these “baby” JPMorgan banks now “too small to fail”? Clearly not, since in the event of a bank failure, taxpayers may still be on the hook for up to $348 billion, each.

So if that’s not small enough, let’s divide them another time, into eight banks that each handles $174 billion in deposits. Could we now regard these new “baby-baby” banks as “too small to fail?”‘ Again, should we consider $160 billion not a small sum if the bank goes under and needs to be rescued by the government?

By this logic, we’d of course also need to break up the other big banks, such as Bank of America and Wells Fargo (each with just under $1.3 trillion in deposits) and Citibank ($947 billion).

The idea that breaking up banks into smaller banks reduces risks is an abstraction since our repeated experience (from the Great Depression to the Great Recession) shows that many banks tend to fail at the same time like dominoes, which by definition we call a “financial crisis.”

Would it really matter to the taxpayer whether a large JPMorgan fails or several “baby JPMorgans” collapse at the same time?

So size does not matter after all. If the term “big” does not make a lot of sense, then why do regulators and central banks keep repeating this slogan?

JPMorgan is the biggest bank in the U.S.Eric Thayer/Reuters

Unintended consequences

In fact, my reading of too big to fail is that, intentionally or unintentionally, it sends banks the wrong message. That is, regulators and central banks are basically telling the “big” banks that they should not worry very much because taxpayers and the Fed will always rescue them because they are too big to fail.

Therefore, intentionally or not, the assertion of too big to fail and passing artificial stress tests may actually generate exactly the opposite incentive for financial institutions, which may encourage large banks to continue taking risks with depositors’ money. In fact, using data for more than 200 banks in 45 countries, a New York Fed paper found that banks classified by rating agencies as more likely to receive government support engage in more risk-taking. The authors also show that riskier banks are more likely to take advantage of potential government support.

The stated logic behind the classification of too big to fail was to impose more restrictions on these financial institutions and conduct stress tests so they will become less likely to fail. The additional restrictions that central bankers are now considering imposing on banks, such as maintaining capital ratios as high as 16 percent to 18 percent, still do not free the taxpayer from bearing the remaining 80 percent of the bailout cost.

Although 16 percent seems like a high number compared with the 12.3 percent capital that large banks were assumed to maintain during the recent stress test, even 20 percent capital requirement leaves banks with substantial leverage. (A capital ratio just shows how much of a bank’s assets are backed by cash or cash-like instruments, as opposed to leverage, or debt.)

Let banks fail

If the TBTF and stress tests send the wrong message to banks, then I would suggest replacing too big to fail with “all banks, regardless of size, should be allowed to fail” with no taxpayer bailout.

The problem is such a statement suffers from what economists call “time inconsistency.” That is, policymakers may be able to take a hard line now, but once the banking system collapses, there is no government in the world (democratic or otherwise) that would be able to resist the political pressure to pay the banks whatever they want just to bring them back to life.

To solve the time inconsistency problem – and ensure policymakers let banks fail – we need to prepare in advance for the next wave of bank failures by protecting depositors’ money, instead of just focusing on stress tests or size reductions.

And this is actually easier to implement than one may think.

Depositors should be simply allowed to have access to accounts that maintain 100 percent reserves. That is, every cent of their savings would be backed by hard currency. Research of mine has shown that moving in this direction improves social welfare relative to the current system of purely fractional banking, in which banks only hold a fraction of their deposits. Currently they are allowed to lend up to 90 percent (keeping 10 percent as reserves).

There are several ways to implement that. One is to allow each depositor to open an online account with the central bank. This could be done via existing commercial banks or directly with the central bank. In addition, if central banks, such as the Fed, provide direct access via nonbank money transmitters (such as PayPal, Square, Western Union or even Wal-Mart’s Bluebird), depositors would be able to secure their money in advance against any loss, even in the event many banks and money transmitters fail. In fact, Mark Carney, governor of the Bank of England, recently announced that the U.K. central bank will expand direct access to nonbank payment providers.

Why haven’t I mentioned the Federal Deposit Insurance Corporation (FDIC), which was set up explicitly to protect deposits in the case of bank failure? Simple: In 2015, the FDIC fund had just $67.8 billion. Dividing this amount by total U.S. deposits implies that the FDIC can bailout only 1.06 percent. In fact, even if JPMorgan is the only bank that fails, the FDIC can only bailout 5 percent of this bank’s deposits, thereby making the FDIC totally irrelevant during a financial crisis.

On the other hand, a 100 percent reserves policy would break our current system’s bundling of risk-taking with the job of keeping accounts safe and offering payment services. Only then, by ensuring depositors (and voters) aren’t at risk when there’s a crisis, would governments have the will to let banks fail – without any regard to their size – and at no cost to taxpayers.

Author: Oz Shy, Senior Lecturer in Economics, Massachusetts Institute of Technology

The Federal Reserve Board has announced it has not objected to the capital plans of 30 bank holding companies participating in the Comprehensive Capital Analysis and Review (CCAR). The Board objected to two firms’ plans. One other firm’s plan was not objected to, but the firm is being required to address certain weaknesses and resubmit its plan by the end of 2016.

CCAR, in its sixth year, evaluates the capital planning processes and capital adequacy of the largest U.S.-based bank holding companies, including the firms’ planned capital actions such as dividend payments and share buybacks and issuances. Strong capital levels act as a cushion to absorb losses and help ensure that banking organizations have the ability to lend to households and businesses even in times of stress.

When considering a firm’s capital plan, the Federal Reserve considers both quantitative and qualitative factors. Quantitative factors include a firm’s projected capital ratios under a hypothetical scenario of severe economic and financial market stress. Qualitative factors include the strength of the firm’s capital planning process, which incorporate the risk management, internal controls, and governance practices that support the process. The Federal Reserve may object to a capital plan based on quantitative or qualitative concerns. If the Federal Reserve objects to a capital plan, a firm may not make any capital distribution unless expressly authorized by the Federal Reserve.

“Over the six years in which CCAR has been in place, the participating firms have strengthened their capital positions and improved their risk-management capacities,” Governor Daniel K. Tarullo said. “Continued progress in both areas will further enhance the resiliency of the nation’s largest banks.”

The Federal Reserve did not object to the capital plans of Ally Financial, Inc.; American Express Company; BancWest Corporation; Bank of America Corporation; The Bank of New York Mellon Corporation; BB&T Corporation; BBVA Compass Bancshares, Inc.; BMO Financial Corp.; Capital One Financial Corporation; Citigroup, Inc.; Citizens Financial Group; Comerica Incorporated; Discover Financial Services; Fifth Third Bancorp; Goldman Sachs Group, Inc.; HSBC North America Holdings, Inc.; Huntington Bancshares, Inc.; JP Morgan Chase & Co.; Keycorp; M&T Bank Corporation; MUFG Americas Holdings Corporation; Northern Trust Corp.; The PNC Financial Services Group, Inc.; Regions Financial Corporation; State Street Corporation; SunTrust Banks, Inc.; TD Group US Holdings LLC; U.S. Bancorp; Wells Fargo & Company; and Zions Bancorporation. M&T Bank Corporation met minimum capital requirements on a post-stress basis after submitting an adjusted capital action.

The Federal Reserve did not object to the capital plan of Morgan Stanley, but is requiring the firm to submit a new capital plan by the end of the fourth quarter of 2016 to address certain weaknesses in its capital planning processes. The Federal Reserve objected to the capital plans of Deutsche Bank Trust Corporation and Santander Holdings USA, Inc. based on qualitative concerns. The Federal Reserve did not object to any capital plans based on quantitative grounds.

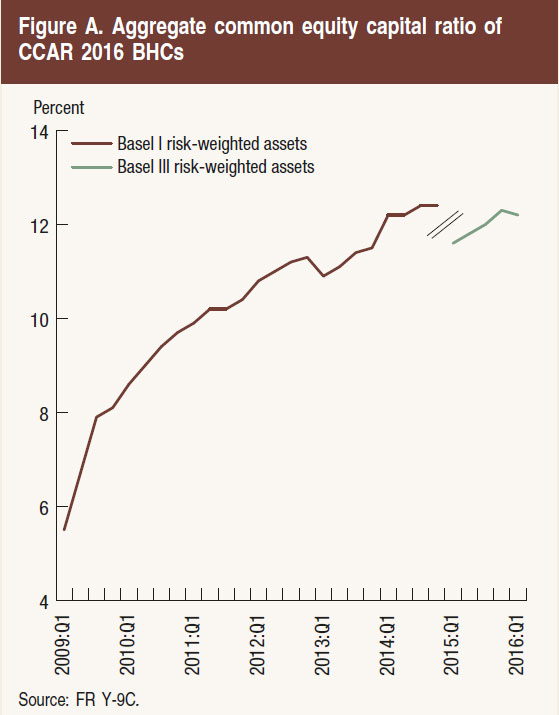

U.S. firms have substantially increased their capital since the first round of stress tests led by the Federal Reserve in 2009. The common equity capital ratio–which compares high-quality capital to risk-weighted assets–of the 33 bank holding companies in the 2016 CCAR has more than doubled from 5.5 percent in the first quarter of 2009 to 12.2 percent in the first quarter of 2016. This reflects an increase of more than $700 billion in common equity capital to a total of $1.2 trillion during the same period.

My baseline expectation has been that our economy is likely to continue on its path of growth at around 2 percent. I have also expected the ongoing healing in labor markets to continue, with healthy wage increases and job creation. As the economy tightens, I have expected that inflation will move up over time to the Committee’s 2 percent objective.

For some time, the principal risks to that outlook have been from abroad. Global economic and financial conditions are particularly important for the U.S. economy at the moment. Weakness in economic activity around the world and related bouts of financial volatility have weighed on the performance of our economy. Given the stronger performance of the U.S. economy, the trade-weighted value of the dollar has risen roughly 20 percent since 2014. Such a large appreciation of the dollar means that we will “export” some of our strength to our trading partners and “import” some of their weakness.

Growth and inflation remain stubbornly low for most of our major trading partners. European and Japanese authorities have limited scope to respond, with daunting longer-run fiscal challenges and policy rates already set below zero. In China, stimulus measures should support growth in the near term, but may also slow China’s necessary transition away from its export- and investment-led business model. Emerging market nations such as Brazil, Russia and Venezuela face challenging conditions.

These global risks have now shifted even further to the downside, with last week’s referendum on the United Kingdom’s status in the European Union. The Brexit vote has the potential to create new headwinds for economies around the world, including our own. The risks to the global outlook were somewhat elevated even prior to the referendum, and the vote has introduced new uncertainties. We have said that the Federal Reserve is carefully monitoring developments in global financial markets, in cooperation with other central banks. We are prepared to provide dollar liquidity through our existing swap lines with central banks, as necessary, to address pressures in global funding markets, which could have adverse implications for our economy. Although financial conditions have tightened since the vote, markets have been functioning in an orderly manner. And the U.S. financial sector is strong and resilient. As our recent stress tests show, our largest financial institutions continue to build their capital and strengthen their balance sheets.

It is far too early to judge the effects of the Brexit vote. As the global outlook evolves, it will be important to assess the implications for the U.S. economy, and for the stance of policy appropriate to foster continued progress toward our objectives of maximum employment and price stability.

I am often asked why rates remain so low now that we are near full employment. A big part of the answer is that, at least for the time being, the appropriate level of rates is simply lower than it was before the crisis. As a result, policy is not as stimulative as it might appear to be. Estimates of the real interest rate needed to keep the economy on an even keel if it were operating at 2 percent inflation and full employment–the “neutral rate” of interest–are currently around zero. Today, the real short term interest rate is about negative 1-1/4 percent, so policy is actually only moderately stimulative. I anticipate that the neutral rate will move up over time, as some of the headwinds that have weighed on economic growth ease.

Interesting observations about household credit from the US Federal Reserve. In general, fewer households are responding that it is a good idea to buy things on credit. The share with positive answers decreased from 32.4 percent in 2004 to 29.7 percent in 2007 to 25.2 percent in 2013. A similar pattern is observed for answers about vacation, coat/jewelry, car and educational expense categories. The only category with an increase in the share with positive answers is “living expenses.”

Overall, the results suggest that households’ attitude toward credit has changed, signaling a reduction in credit demand. This is an important topic for further research, because the policy recommendations are very different if the reduction in household credit was caused by a reduction in the availability of credit (credit supply) or by households’ attitude toward credit.

In previous articles, we saw that household debt has been declining and why debt has dropped since the financial crisis. Total household debt, which peaked in 2009, stabilized at 13 percent below the previous peak in the first quarter of 2013. One of the most relevant questions regarding this trend is: Was it caused by supply or demand factors?

While credit supply factors capture the behavior of lenders (banks and other financial institutions), credit demand factors represent the willingness of households to borrow. In this blog post, we present data on households’ attitude toward credit to evaluate potential changes in credit demand.

We used data from the Survey of Consumer Finances (SCF). This survey asks households questions on credit attitudes. In particular, households are asked if they think it is generally a good or bad idea for people to buy things by borrowing or on credit. The survey also asked specifically about borrowing money:

To cover the expenses of a vacation trip

To cover living expenses when income is cut

To finance the purchase of a fur coat or jewelry

To finance the purchase of a car

To finance educational expenses

The figure below shows the percentage of individuals who answered that it is generally a good idea to buy things on credit.