As former GE CEO Jack Welch famously said, “Change before you have to.” Some financial firms have thrived in the digital age, adopting technology to not just better serve their consumers, but to upend their own business models. Investment firm BlackRock disrupted how it does business to build the investing platform, Aladdin, that now manages $225 trillion in assets—that’s 7% of the world’s financial assets. Others, unfortunately, have not been so innovative and are starting to hemorrhage clients to robo-advisers, online banks, and traditional incumbents that have been better able to leverage technology to steal market share.

It’s not shocking to acknowledge that the rising ability of consumers to understand and easily manage finances without a traditional broker or bank represents an existential threat to the industry. However, it is shocking to see that some institutions are pretending this trend does not apply to them—that their customers who are older or wealthier will not embrace this new tech. However, with the impending “great wealth transfer,” millennials will be inheriting $30 trillion from their baby boomer progenitors—and with loyalty waning among this group, they’re not likely to stick with their parents’ advisors. The big question is whether they’ll look to financial institutions to manage this new wealth or turn to financial startups that provide them with new tools to manage their money themselves.

Consider shifting consumer attitudes

Since today’s consumers are digitally savvy and always on the go, they’ve come to expect simple user experiences coupled with information that’s easy to understand and always at their fingertips. Millennials, in particular, bank differently. They are generally more informed and more wary than other consumers. According to Nielsen’s second-quarter 2015 Consumer Confidence Report, millennials are cautious spenders and savers, but less trusting of traditional financial and investment strategies.

They’ve taken a do-it-yourself approach to finance. How can incumbent financial institutions maintain market share and maintain trust and loyalty as consumers expect the same on-demand, customer- first digital experiences from their banks that they do from Amazon or Uber?

Push for a cultural shift as much as a digital one

Banks are great at risk management, financial governance, investing, and asset management, as we expect them to be. For most traditional financial services companies, digital services aren’t a priority. However, banks must learn to bring technology to the forefront to drive enhanced customer experiences while still mitigating risks.

Doing this requires a cultural shift as much as a technological one. Leveraging the vast amount of consumer insights can help banks deliver outstanding user experiences and become more effective marketers. However, hiring technologists is not enough—growth requires a deep organizational shift that supports risk and experimentation, while still enforcing a high degree of oversight to ensure that customer’s wealth and privacy are protected.

This balancing act is not easy, and it’s the reason why incumbent financial institutions embrace innovation slowly. When upwards of 50% of new products and business fail, can we expect more from internal projects? Furthermore, can we expect banks to fund projects that have a 50% fail rate? While startups with much less to lose can claim that failure is the new R&D, it’s a hard ethos for an incumbent to adopt, but it must be considered and embraced.

Innovation requires rebuilding

The biggest technology challenges facing financial organizations don’t stem from insufficient budgets. They result from the over-engineered legacy systems that are expensive and painfully difficult to maintain or innovate within. Legacy platforms require armies of engineers to maintain systems in antiquated languages that are older than the web itself. Not only does this stymie innovation, it outright kills it.

The level of protectionism that exists in institutional IT organizations is a double-edged sword. It can be unnerving to innovators, especially those from other industries, who strive to move fast and crave the efficiencies of modern technology. However, protecting the bank’s technology infrastructure is as critical as protecting its vault. Giving an inch in this mission can be disastrous, wiping out trust in the institution. This is why IT wields its protectionist muscle reflexively.

Getting past this reflex is not easy and requires leadership that understands the implications of transformation, and works through it to build platforms, processes, and systems that are user-first versus systems-first. This requires teams that yearn to move faster, to build on modern frameworks, to leverage the same technology and marketing stacks that are powering the contemporary customer experiences we’ve come to expect from Uber, Netflix, Amazon, Facebook, and others.

It’s not adequate to optimize one aspect of the customer experience while another relies on a process that is as old as the bank itself. Instead, banks and financial services organizations need to deliver a customer-first experience at every point of interaction. Focused on delivering an innovative customer experience, digital providers like Wealthfront, FutureAdvisor, and Betterment are not capturing new customers simply due to lower fees, they are driving growth by delivering outstanding interactions at every touchpoint, something most institutions are still struggling to do.

Create content to cultivate trust

Confidence in banks and financial advisors has eroded over time. According to Nielsen, millennial consumers want a transparent and authentic relationship with their financial institutions. Because of this, many are focused on re-evaluating the way they deliver products and services. Smart financial institutions are building trust through increased transparency, re-aligned products, and direct education.

A simple way to build trust is by giving people an easy way to understand how their money is working for them. Leading the pack, JPMorgan Asset Management focuses on simplifying complex financial topics for its financial advisors, so they can do the same for clients. This investment in education and transparency makes clients feel like they’re in the driver’s seat, positioning the brand as the trusted authority that can engage clients on their terms, in their language. The digital realm makes communicating with teams and customers easier and cost effective. However, with a slew of competitors a mere click away, financial brands have to create truly engaging and useful content. Those leveraging videos, infographics, tutorials, and interactive tools to explain complex topics will win the consumer.

Find the right partners

Ask a CEO at a bank or financial institution what success means to them. They’ll likely be more concerned with managing risk, liquidity, and return on investments for shareholders. Critical, yes—but holistic success is also tied to excellence in digital marketing, innovation, analytics, and understanding the customer journey. As technology continues to change the customer experience, financial organizations need to seek partners that are aligned with the needs and behaviors of their end users.

It’s critical to find a partner that understands how to marry financial services, especially the regulatory aspects, with an overarching digital strategy to serve these users. A solid partner should be thinking about the experience across the full customer lifecycle, rather than a single transaction or channel, in order to cultivate trust and longer term relationships.

Investments in easily digestible content and user-centric experiences will not only help mitigate the generational wealth transfer, but allow some incumbents to benefit from it. Financial services organizations that ultimately succeed in navigating disruption are those that effectively leverage data and digital touchpoints to reduce costs and drive growth.

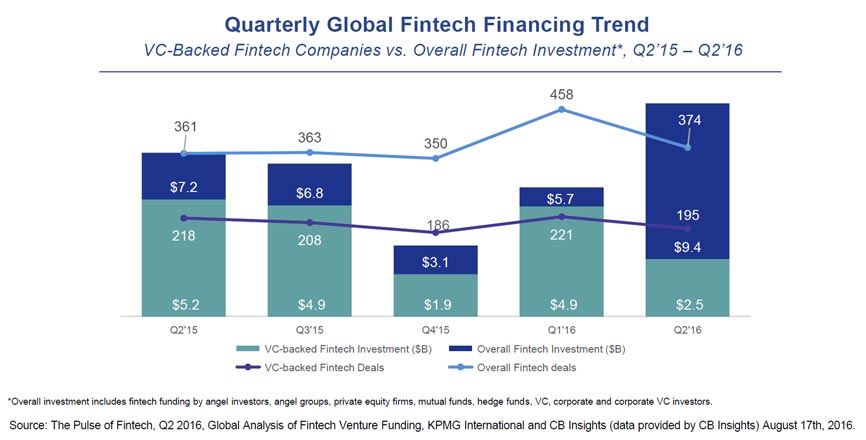

They say that in 2016, concerns about high valuations, the lack of significant IPO exits and macro-economic factors seem to have led investors to be more cautious. Over the first 2 quarters, VC investors focussed on more experienced companies with proven technologies or business models.

They say that in 2016, concerns about high valuations, the lack of significant IPO exits and macro-economic factors seem to have led investors to be more cautious. Over the first 2 quarters, VC investors focussed on more experienced companies with proven technologies or business models.