The Treasure released a working paper today – “Foreign Investment and Residential Property Price Growth“. This paper explores the relationship between foreign investment in Australian residential real estate and property prices.

They take the number of foreign approvals (with exceptions), and look, at a postcode level for differences in purchase price, between those with high foreign transactions, and those will little or none. They conclude that the increase in prices attributable to foreign investors is small when compared to the average quarterly increase in property prices of around $12,800 in Sydney and Melbourne during the study period. Across Sydney and Melbourne, for a typical postcode, foreign demand increases prices by between $80 and $122 on average in each quarter. Almost nothing. We were not convinced.

They take the number of foreign approvals (with exceptions), and look, at a postcode level for differences in purchase price, between those with high foreign transactions, and those will little or none. They conclude that the increase in prices attributable to foreign investors is small when compared to the average quarterly increase in property prices of around $12,800 in Sydney and Melbourne during the study period. Across Sydney and Melbourne, for a typical postcode, foreign demand increases prices by between $80 and $122 on average in each quarter. Almost nothing. We were not convinced.

The number of foreign investment approvals has trended up in recent years, which has coincided with strong property price growth in many parts of Australia. While domestic buyers make up the vast majority of demand for property, it may be the case that, at the margin, foreign buyers are affecting property prices. This is because the stock of dwellings is relatively fixed in the short run so any increase in demand, whether from domestic or foreign sources, would be expected to result in higher prices, at least until increased prices have provided an incentive for the construction of additional supply. In the longer term, the high level of house prices in Australian capital cities, relative to those in other countries, likely reflects supply constraints. These constraints include state government land release and zoning policies, infrastructure provision and local government development approval processes.

Australia’s policy for foreign investment in residential real estate aims to increase Australia’s housing stock. As such, applications from non-residents to purchase new properties are usually approved without conditions, but non-residents are prohibited from purchasing established dwellings. Temporary residents can apply to purchase one established property to use as a residence while they live in Australia. The majority of approvals have been granted for investment into new, as opposed to existing dwellings. This suggests that foreign demand is being channelled into increasing the property supply as intended. While some commentators have argued that foreign demand is pricing out first home buyers, it is not clear that this is the case. The number of foreign investment approvals granted for new properties is especially noteworthy given new properties make up a very small proportion of the total number of properties in Australia and because first home buyers tend to buy established properties.

In recent years the level of foreign demand for Australian property has increased strongly. This has been driven largely by increasing applications from Chinese nationals, which rose from around 50 per cent of total foreign investment approvals in mid-2010 to around 70 per cent in early 2015. The increased importance of Chinese demand to Australian real estate increases Australia’s exposure to factors affecting the Chinese economy. Further, any change to the relative attractiveness of holding assets outside of China or ability to do so will likely affect foreign demand for Australian property, which may have domestic economic and financial implications.

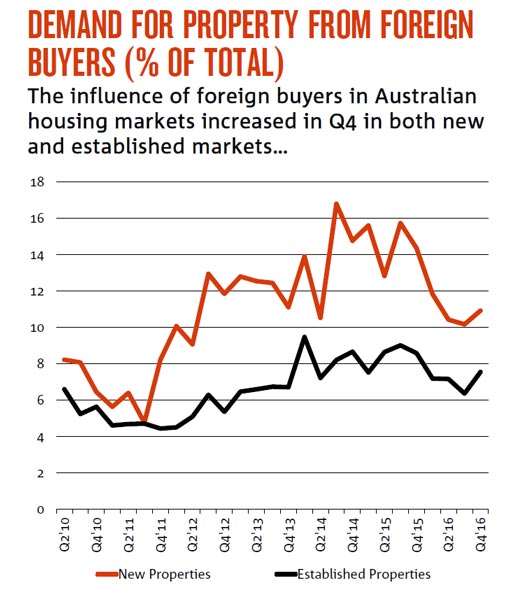

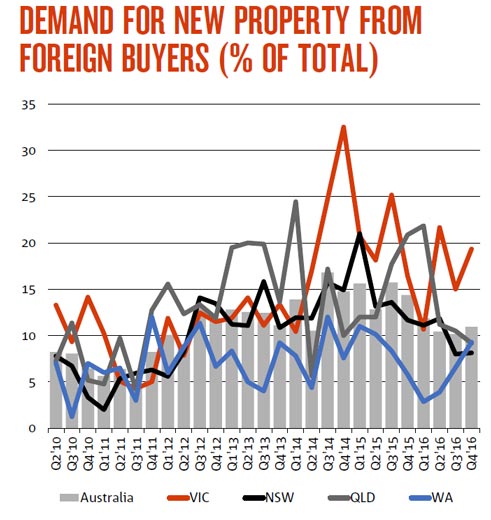

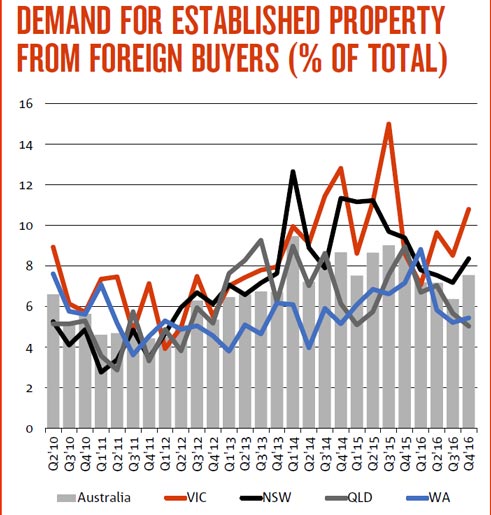

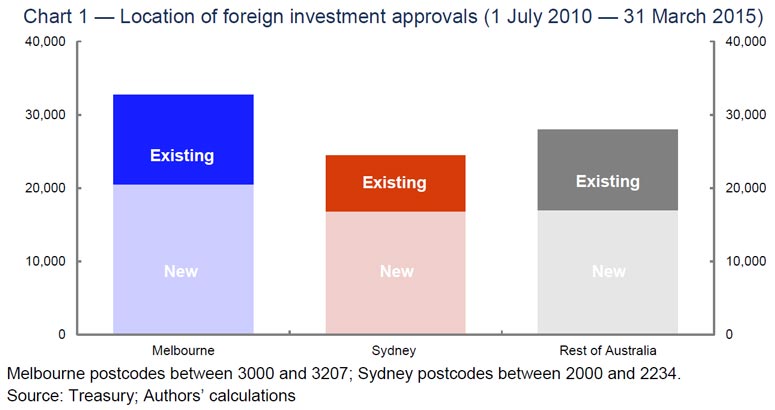

Over the period of this study, foreign investment in residential real estate has been concentrated in Melbourne and Sydney (Chart 1).

But despite Melbourne receiving more foreign investment approvals than Sydney, price growth in Sydney has been much stronger than in Melbourne over the period. As such, it is difficult to directly attribute price growth in Sydney to foreign investors alone. Other factors, such as the relatively low number of building approvals, commencements and completions in the late 2000s are potential longer term drivers of the recent price growth in Sydney.

But despite Melbourne receiving more foreign investment approvals than Sydney, price growth in Sydney has been much stronger than in Melbourne over the period. As such, it is difficult to directly attribute price growth in Sydney to foreign investors alone. Other factors, such as the relatively low number of building approvals, commencements and completions in the late 2000s are potential longer term drivers of the recent price growth in Sydney.

To estimate the sensitivity of property prices to changes in foreign demand we develop a fixed effects model of postcode level price growth using foreign investment approvals data from the Foreign Investment Division of the Treasury as the main explanatory variable.

Despite these shortcomings the data from the Foreign Investment Division at the Treasury is preferable to alternative measures of foreign investment in residential property. These alternative measures, such as from the National Australia Bank, are problematic because they are based on survey data from

industry participants and it is not clear how these industry participants determine whether property buyers are foreign.

Under almost all model specifications there is a statistically significant and economically meaningful relationship between foreign investment approvals and property price growth, but the majority of price growth experienced in recent times does not appear to be attributable to increased foreign demand. Instead, the fact that property price growth has been strong over an extended period is likely to have been primarily driven by other factors such as impediments to supply, especially in some regions where natural and human-imposed constraints on supply are especially limiting.

The increase in prices attributable to foreign investors is small when compared to the average quarterly increase in property prices of around $12,800 in Sydney and Melbourne during the study period. Across Sydney and Melbourne, the models which we consider to be the best specified indicate that, for a typical postcode, foreign demand increases prices by between $80 and $122 on average in each quarter. This is based on the average postcode in these two cities receiving around 0.6 more foreign investment approvals each quarter over time. Further, for each additional foreign investment approval beyond this typical increase of 0.6, median property prices are estimated to rise by between $145 and $222.

Given that the typical increase in the number of foreign investment approvals from one quarter to the next in Sydney and Melbourne is only around 0.6, one additional foreign investment approval beyond this trend increase would be a relatively large spike in the number of approvals. As such, it can be seen that foreign demand has accounted for only a small proportion of the increase in property prices in recent years.

While the results of this study show a consistent, but small positive relationship between foreign investment approvals and property price growth, there are some limitations. This includes the data limitations set out in Section 3, particularly around compliance and that the data reflects intentions to purchase and not actual purchases. The foreign investment data also may not pick up purchases by a citizen or permanent resident on behalf of family members overseas. Quantifying the effect of these limitations is difficult. It is also important to note that while the results suggest the impact across Australia and the capital cities is small, the impacts in certain areas or at particular times may be more intense.

Whilst we applaud the Treasury for trying to bring science to this complex issue, we think there are fundamental flaws in the analysis, which devalues the conclusions significantly.

First, we think the modelling needs to look at total demand, at a post code level by purchaser type. We know from our own surveys, demand varies significantly driven by mix of prospective purchasers. In some locations, – for example Wolli Creek, we see high demand for foreign purchasers, first time buyers, other property investors and down traders – demand is outstripping supply, and here investors are outbidding first time buyers. This is the point, supply is not uniform, and therefore the pricing equilibrium will be quite different in individual locales. Reading their method, we think this is a significant issue.

Second their measure of foreign demand is the number of foreign investment approvals. This data are sourced from the Foreign Investment Division at the Treasury and it not available to the public, so the data cannot be validated, or independently reviewed. Recent inquiries however have called into question the accuracy of the approvals data. It likely understates the volume. Why not release the data, so we can judge?

They did not include data on advanced off-the-plan foreign investment approvals, nor price data from off-the-plan sales from such developments. We believe that this is likely to miss bulk approvals from developers who, at a single application, and approval gets multiple property transactions approved.

They make the point that foreign investment approvals are concentrated in a relatively small number of postcodes — more than three quarters of postcodes receive less than one approval every three months. Approvals do not represent actual purchases. For example, a foreign person may receive a foreign investment approval but later decide not to purchase a dwelling. No data are available regarding properties sold by foreigners. As such, the foreign investment data are an indication of gross foreign demand not net foreign demand. For instance, if a property is sold by one foreign person to another, there is no net change in foreign demand for

dwellings but an additional foreign investment approval will be recorded. It is unclear when an approval for foreign investment will be acted upon because the approval is valid for 12 months. However, anecdotal evidence suggests that in most cases approvals are acted upon soon after being granted. In some cases an approval may be sought shortly after a

contract is entered into but before the conveyancing and settlement period is finalised. As such, they consider leading and lagging relationships in the Results section. This yields some insights into the behaviour of foreign investors.

Foreign investment approvals data do not distinguish between houses and units, so in postcodes with price data for both houses and units, they aggregate prices for these two property types. Specifically, this aggregation is weighted by the proportion of houses and units in each postcode. In postcodes where no price data are available for a particular property type at any time — for example, units in a regional postcode — but price data are available for the other property type — for example, houses — they use the available price data as a measure of postcode

level price.

They do not control for changes in the quality of properties in each postcode through time. We do not consider this to be a major limitation because of the relatively short time period of our study. However, the lack of hedonic adjustment could be problematic where price data are derived from a small number of sales. That is, where postcode level property markets are relatively illiquid and the quality of transacted properties changes through time even though the quality of properties in the postcode more broadly does not change.

So, we conclude this exercise may generate some heat, but we are not sure it casts light on the real issues surrounding foreign buyers. The data limitations and surrounding processes need to be improved if we are to get a handle on the true story.