High Frequency Trading is an arms race in the quest for speed. It creates an ever more uneven playing field. This article from Zero Hedge demonstrates to what lengths the high frequency traders will go for just a few millisecond advantage – which makes in the HFT world makes all the different between billions in profits and losses – Bloomberg reports that a mysterious antenna has emerged in an empty field in Aurora, near Chicago, and a trading fortune depends on it.

Strange? Of course: as BBG’s Brian Louis admits “it was an odd transaction from the outset: $14 million, double the going rate, for a 31-acre plot of flat, undeveloped land just west of Chicago. In the nine months since, the curious use of the space has only added to the intrigue. A single, nondescript pole with two antennas was erected by a row of shrubs. Some supporting equipment was rolled in. That’s it.”

As it turns out, those antennas – as readers may imagine – were anything but ordinary. Same goes for the buyer of the property: anything but your typical land investor, although the name will be all too familiar to those who have followed our reporting on HFT over the years: it was Jump Trading LLC, “a legendary and secretive trading firm that’s a major player in some of the most important financial markets.”

Equipment on land purchased by an affiliate of Jump Trading

Jump Trading affiliate World Class Wireless purchased the 31-acre lot for $14 million, according to county records. “They paid probably twice as much as it’s worth,” said David Friedlandof Cushman & Wakefield. “I don’t see anyone else paying close to that price.”

There was a reason why Jump overpaid so much: it was an investment into guaranteed future returns.

Because ultimately the purchase was all about the location: just across the street lies the data center for CME Group, the world’s biggest futures exchange. By placing its antennas so close to CME’s servers, Jump hopes to shave maybe a microsecond off its reaction time, enough to separate a winning from a losing bid in trading that takes place at almost the speed of light. Enough to make billions in profits if done successfully millions of times every minute for year.

As Bloomberg describes the land grab, “it was the latest, and perhaps boldest, salvo in an escalating war that’s being waged to stay competitive in the high-speed trading business.”

The war is one of proximity — to see who can get data in and out of CME the quickest. A company called McKay Brothers LLC recently won approval to build the tallest microwave tower in the area while another, Webline Holdings LLC, has installed microwave dishes on a utility pole just outside the data center.

“It tells you how valuable being just a little bit faster is,” said Michael Goldstein, a finance professor at Babson College in Babson Park, Massachusetts. “People say seconds matter. This is microseconds matter.”

It also tells you something else: at its core, modern trading is simply about being faster than your competition: no thinking goes into the trade, only reaction times matter. That, and frontrunning your competition. Some more details about this literal land grab:

In October 2015, McKay Brothers, a company that sells access to its microwave network to high-speed traders, leased land diagonal to the CME data center, under the name Pierce Broadband LLC, according to DuPage County property records.

Last month, the county gave McKay approval to erect a 350-foot high microwave tower that could be 600 feet closer to the data center than its current location, records show. Two trading firms, IMC BV and Tower Research Capital LLC, own minority stakes in McKay. Co-founder Stephane Tyc said his firm may never build the tower but it would be part of the firm’s continual efforts to speed transmission time.

Then there’s Webline Holdings. In November 2015, it was granted a license to operate microwave equipment on a utility pole just outside the data center, according to Federal Communications Commission records. Webline has licenses for a microwave network stretching from Aurora to Carteret, New Jersey, where Nasdaq Inc.’s data center is located. Messages left for Webline were not returned.

Back to the mysterious antenna: according to Bloomberg, the license for the transmission dishes is held by a joint venture between World Class and a unit of KCG Holdings, another HFT trading firm that was recently acquired by Virtu Financial. In other words, the “who is who” of HFT has been unleashed on an empty field near Chicago, and to the builder will go the spoils. It could be billions in revenues.

After all this frentic building of microwave tower, who is closest to the CME servers? It is unclear. Trading data first leaves CME computers via fiber cable, and then to nearby antennas that send it by microwave to other towers until it reaches New Jersey, where all the major U.S. stock exchanges house their computers. The moves in Aurora are intended to reduce the time that the data is conveyed through cable; the practical impact is shaving off a millisecond or maybe even a few nanoseconds.

At its core, the race is about latency arbitrage, and not being the slowest firm on the block – a recipe for financial ruin. Sending data back and forth between the U.S. Midwest and East Coast allows high-frequency traders to profit from price differences for related assets, including S&P 500 Index futures in Illinois and stock prices in New Jersey. Those arbitrage opportunities often last only tiny fractions of a second.

Ironically, all the land grab and overpriced land purchases could be made obsolete with one simple decision: a microwave tower could be installed on the roof of the CME data center to eliminate the need for jockeying around the site, the same way the NYSE has a microwave tower next to its NJ headquarters. The exchange is indeed looking at allowing roof access, along with CyrusOne, the company that bought the data center last year, CME said in a statement. Traders being traders, however, they may continue to battle, this time for the most advantageous position on the microwave tower itself.

“We are confident the CME can provide an alternate and better solution which offers a level playing field to all participants,” said McKay’s Tyc.

Which is ironic because at its core, modern High Frequency Trade is about everything but a level playing field: after all there are millions of traders to be frontrun, take that away, and the HFT parasites of the world have no advantage whatsoever.

Recent turbulence in the share markets has caused some experts to point the finger of culpability at computerised High-Frequency Trading (HFT). There are few complaints about HFT when computers push share markets up, but in the ebbing tide of today’s markets, it’s blamed both for exaggerating the share market dive as well as for the heightened volatility.

The logic behind the fears is this: algorithms and software do not muse about global economic events; they merely chase mechanical patterns that they are programmed to find, such as movements in trend or momentum. They do not make decisions based on real-world eventualities, such as political events.

Can the algorithms express a view on Chinese consumer confidence? The economic impacts of Middle-Eastern sectarian conflicts? These real world factors aren’t taken into account in the programming of algorithms.

Yet the computers hold substantial sway and can execute a barrage of trades that create unprecedented volatility at a rate that human reactions simply cannot match.

What is truly problematic is that the algorithms are not cognisant of when to stop or change a trade and thus can continue to pile money and exaggerate a trade well beyond what the market would consider a correct response. The computers do not have the ‘affirmative obligation’ to keep the markets orderly.

In fact, this sort of financial competition has been described as ‘a new world of a war between machines’.

Research has explained that stock prices tend to overreact to news when HFT activity is at a high volume, and that this can have ‘harmful effects’ for capital markets. Additionally, financial experts have found that HFT “exacerbates the adverse impacts of trading-related mistakes”, while also leading to “extremely higher market volatility and surprises about suddenly-diminished liquidity”, which in turn “raises concerns about the stability and health of the financial markets for regulators.”

In Australia HFT has made significant inroads into the market. In 2015 it accounted for nearly one-third of all equity market trades, a level similar to Canada, the European Union, and Japan.

ASIC estimates that HFTs in Australia are collectively earning an not inconsequential $100 million to $180 million annually.

Securities regulators have tolerated HFT so far, but as we may be entering a “new normal” of higher volatility and with algorithms helping exert a downward pressure on the markets, the regulators may find themselves revisiting the HFT issue.

Australian financial traders may also be put in jeopardy by the sheer magnitude of large foreign-funded HFT players. In recent times, the incursion of HFT into other asset classes such as interest rates futures has shown that local traders are being forced out by the computing power of internationally-funded “flash boys”.

Nonetheless, the track record of Australian regulators has been very positive and they have been proactive about creating mechanisms such as ‘kill switches’ to mitigate potential losses.

From a theoretical standpoint, the proponents of HFT have argued that it provides the most up-to-date information and thus facilitates price discovery. However, if the algorithms are merely exaggerating sentiments by moving large sums at instantaneous speeds – then they are not facilitating price discovery but in fact preventing that goal from being achieved.

The movie, The Big Short, based on the book by Michael Lewis, (who also wrote about “flash boys”) has infused narratives of the financial world with a “human element”. They have put faces to the names we read about in financial scandals.

However, if HFT grows in size and share markets continue to perform negatively, it may be that the computerised antagonists of finance’s future, the diaboli ex machina, may have no face at all.

Author: Usman W. Chohan, Doctoral Candidate, Economics, Policy Reform, UNSW Australia

High-frequency trading and dark liquidity have been two of the most topical market structure issues globally over recent years. During 2015, ASIC have undertaken two new reviews of high-frequency trading and dark liquidity. The aim of these reviews has been to update and build on their earlier analysis of equity markets and to assess the effect of high-frequency trading on the futures market.

No further regulation specifically addressing high-frequency trading or dark liquidity is proposed at this stage but ASIC says they will continue to monitor developments involving these and other markets issues.

The 2015 reviews involved:

(a) stakeholder engagement, including over 40 meetings with fund managers, market participants, high-frequency traders and market operators. Over 20 separate meetings on principal trading and facilitation with market participants, fund managers and overseas regulators;

(b) in-depth analysis of equity and futures order and trade data; and

(c) literature review, including research by academics and other regulators

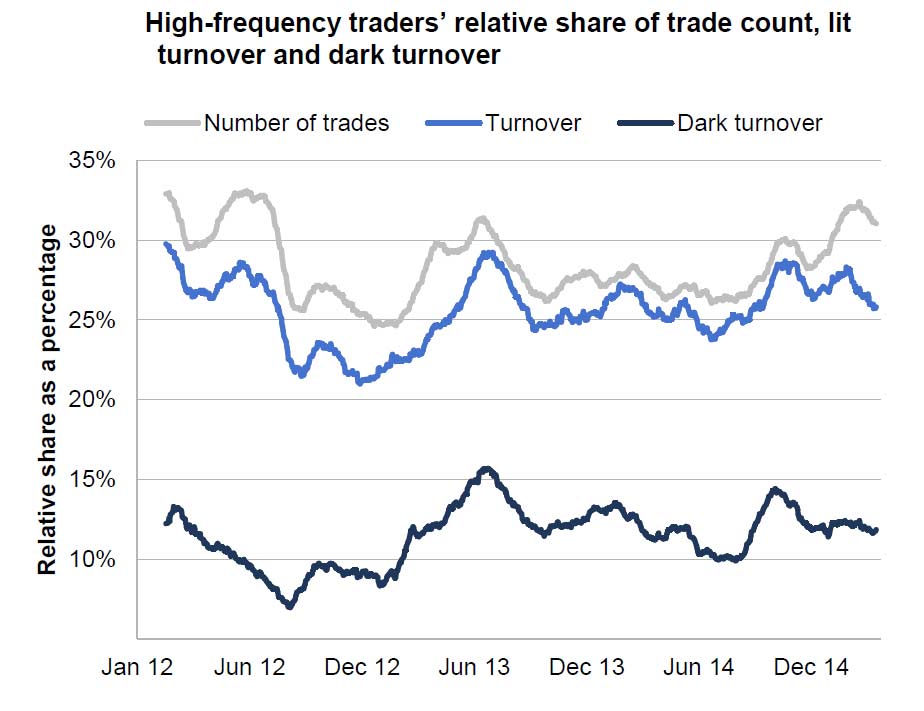

High frequency trades make up more than 30% of all trades, and dark turnover is sitting at about 12%.

ASIC’s Key Findings

High Frequency Trading – Equity Markets

The level of high-frequency trading in our equity markets is reasonably steady at 27% of total turnover (this is comparable to Canada, the European Union and Japan).

However, the concentration of high-frequency trading in our markets is higher, with 30% fewer high-frequency trading accounts. Trading is also more active in mid-tier securities than in 2012.

High-frequency traders are trading somewhat more aggressively than in 2012, while still contributing significantly to the orders at the best displayed prices. Average holding time is between 50 and 60 minutes.

High-frequency traders appear to have become more sophisticated. Compared to 2012, they are better at avoiding interacting with one another and they are extracting larger gross trading revenues. ASIC estimate that they earned $110–180 million in aggregate over the 12 months to 31 March 2015. This translates to a cost of 0.7 to 1.1 basis points to other market users. This is material, but substantially less than other figures suggested by some, and less than some other trading costs (e.g. average bid–offer spreads are 13 basis points).

High-frequency trading does not appear to be a key driver of transaction costs. It appears that higher levels of high-frequency trading assist in lowering transaction costs for low turnover securities.

Some concerns about predatory trading remain (i.e. where trading is undertaken to exploit others or unfairly induce them to trade). While not excessive in our markets, predatory trading can adversely affect the trading outcomes for fundamental investors (those who buy or sell on an assessment of intrinsic value). Fundamental investors remain ASIC’s regulatory priority and unchecked predatory trading can undermine our objectives for those investors to have confidence and trust in our markets and for our markets to be fair, orderly, transparent and efficient.

High Frequency Trading – Futures market

High-frequency trading has grown rapidly in the futures market (130% since December 2013), although from previously low levels. High-frequency trading in the S&P/ASX 200 Index Futures Contract (SPI) accounts for 21% of traded volume and in the Three Year and Ten Year Commonwealth Treasury Bond Futures Contracts (bond futures) it accounts for 14% of traded volume. While these levels do not currently concern ASIC, they are closely monitoring growth

ASIC are conducting inquiries into a number of traders for excessive order entry and cancellation in the ASX 24 market during the quarterly expiries (i.e. the ‘roll’). This practice affects other market users because it prevents the prioritisation of their orders and forces them to cross the spread (i.e. pay more). ASIC has asked ASX to consider what steps may be taken to discourage this practice.

Dark liquidity

There has been a partial shift back to using dark liquidity for its original purpose, namely large block trades to reduce market impact. This is a positive development and, in part, a response to the lowering of block trade thresholds in May 2013

Many of the concerning trends with crossings systems that ASIC identified in 2012 have abated. The reasons for this are likely due to buy-side clients demanding improved standards and ASIC market integrity rules introduced to enhance fairness and improve transparency around the operation of crossing systems

There has been a decline in the use of crossing systems and growth in the use of the exchange dark venues (i.e. ASX Centre Point and Chi-X hidden orders). This is likely a response to the trade with price improvement rule introduced in May 2013, and a lack of price improvement opportunities in crossing systems

There is a trend here and overseas toward exchange and crossing system operators seeking to preference some market users over others (e.g. better or worse order execution priority) for dark trading. These developments have the potential to undermine fair and non-discriminatory trading and may be inconsistent with operators’ obligations. ASIC is unlikely to support any form of preferencing where it unduly favours some market users over others, unfairly limits access to market facilities, or otherwise results in the unfair treatment of orders or market users

ASIC has concerns about how some market participants are managing their conflicts of interest for principal trading and client facilitation. Market participants should review their arrangements to protect clients’ trading intentions, manage conflicts of interest, avoid the risks of insider trading, conduct compliance and supervision and have appropriate incentive structures. They should avoid situations where staff are responsible for the participant’s own trading while having access to unexecuted client orders. Additional controls, including physical separation, should be put in place to manage the conflicts and conduct risk arising from active facilitation

We think high frequency trading is of concern, because it is clear, those who invest in major IT systems to reduce transaction times have significant market advantage – it has become an arms race, where smaller players cannot win. The system is essentially gamed.

The volatility on global equity markets in August was at its highest since 2011. On Black Monday (August 24, 2015), the Dow Jones Industrial Average fell by more than 1,000 points and the S&P500 index plummeted 5.3% in the first four minutes after the opening. During the first 30 minutes, more than two billion shares were traded and, over the morning, the market quickly recovered about half of what was lost during the first four minutes.

The CBOE Volatility Index (VIX) also known as the fear index peaked that day at 40.74. During less stressful times in the market, VIX values are usually below 20. Values greater than 30 are generally associated with high levels of volatility. For example, during the global financial crisis, the index reached an intraday high of 89.53 on October 24, 2008.

Chicago Board Options Exchange SPX Volatility Index 2014-15Bloomberg Business

The speed of adjustments in the market during the last few weeks have seen many market commentators question whether the higher level of volatility is the “new normal”. For instance, the former European Central Bank President Jean-Claude Trichet suggests that “we have to live now with much higher, high-frequency level volatility”.

Things change

What has changed and who are the market participants that are contributing to the high-frequency volatility that we are observing?

The chiefs of banking giants Commonwealth Bank and ANZ have laid the blame on high-frequency traders. ANZ chief Mike Smith argues HFT is a problem because it’s moving the market “very, very dramatically both ways”.

High frequency traders use computers and complex algorithms to move in and out of stocks very quickly. These movements are typically milliseconds apart, involving the trading of very large volumes of shares. Some market commentators believe HFT has intensified the recent volatility by causing the market to react rapidly to news that may not be significant. In response to the market swings that we are currently experiencing, some argue that the reactions observed are much more volatile than what is expected.

HFT and market quality

Doug Cifu, the co-founder of one of the largest electronic market making firms in the world and biggest high-frequency trading firm, Virtu, has defended the role of HFT. Virtu trades about 11,000 financial instruments in 225 markets across 35 countries. Cifu argues that HFT does not cause volatility but absorbs volatility as they participate in the market as a market maker. Market makers help the trading process by acting as the counterparty when others want to trade, and earn a fee in the process.

High-frequency trading firms have argued they provide liquidity to investors and make trading cheaper by reducing spreads between bids and offers across the markets.

My colleagues and I at the University of Western Australia Business School and University of Nagasaki studied the effects of HFT on liquidity on the Tokyo Stock Exchange. We found evidence to support the argument that trading by high-frequency trading firms improves market quality during normal market conditions. This is consistent with prior research conducted using data from the New York Stock Exchange.

However, we found HFT does not improve market quality during periods associated with high levels of market uncertainty. This is particularly worrisome because high frequency traders appear to consume liquidity when liquidity is needed the most.

Actions by regulators

Market operators and regulators have considered different strategies to increase market stability. Some have implemented circuit breakers to halt trading when the market moves by certain percentages, while others have considered imposing transaction taxes on high-frequency traders.

In response to the latest market swings, the China Financial Futures Exchange (CFFE) took a more drastic response by suspending 164 investors who were found to have high daily trading frequency. According to the China Securities Regulatory Commission (CSRC), the trading by these investors is believed to amplify market fluctuations.

In the US, it is estimated that about three-quarters of daily trading is by HFT and ETFs using “slice and dice” type strategies. In an Australian Securities and Investments Commission report released in 2013, HFT is found to account for 27% of total turnover in S&P/ASX200 securities.

These traders are unlikely to go away. It’s now important for us to get a good understanding of what is the new normal. This is what will help regulators in their tough task of monitoring and ensuring market stability.

Author: Marvin Wee, Associate Professor, Accounting and Finance at University of Western Australia

The Bank of England just published a research paper examining how High-Frequency Trading impacts Market Efficiency. High-frequency trading (HFT), where automated computer traders interact at lightning-fast speed with electronic trading platforms, has become an important feature of many modern financial markets. The rapid growth, and increased prominence, of these ultrafast traders have given rise to concerns regarding their impact on market quality and market stability. These concerns have been fuelled by instances of severe and short-lived market crashes such as the 6 May 2010 ‘Flash Crash’ in the US markets. One concern about HFT is that owing to the high rate at which HFT firms submit orders and execute trades, the algorithms they use could interact with each other in unpredictable ways and, in particular, in ways that could momentarily cause price pressure and price dislocations in financial markets.

Using a unique data set on the transactions of individual high-frequency traders (HFTs), we examine the interactions between different HFTs and the impact of such interactions on price discovery. Our main results show that for trading in a given stock, HFT firm order flows are positively correlated at high-frequencies. In contrast, when performing the same analysis on our control sample of investment banks, we find that their order flows are negatively correlated. Put differently, aggressive (market-“taking”) volume by an HFT will tend to lead to more aggressive volume, in the same direction of trade, by other HFTs over the next few minutes. For banks the opposite holds, and a bank’s aggressive volume will tend to lead to aggressive volume in the opposite direction by other banks. As far as activity across different stocks is concerned, HFTs also tend to trade in the same direction across different stocks to a significantly larger extent than banks.

We find that HFT order flow is more correlated over time than that of the investment banks, both within and across stocks. This means that HFT firms tend more than their peer investment banks to buy or sell aggressively the same stock at the same time. Also, a typical HFT firm tends to simultaneously aggressively buy and sell multiple stocks at the same time to a larger extent than a typical investment bank. What does that mean for market quality? A key element of a well-functioning market is price efficiency; this characterises the extent to which asset prices reflect fundamental values. Dislocations of market prices are clear violations of price efficiency as they happen in the absence of any news about fundamental values.

Given the apparent tendency to commonality in trading activity and trading direction among HFTs, we further examine whether periods of high HFT correlation are associated with price impacts that are subsequently reversed. Such reversals might be interpreted as evidence of high trade correlations leading to short-term price dislocations and excess volatility. However, we find that instances of correlated trading among HFTs are associated with a permanent price impact, whereas instances of correlated bank trad- ing are, in fact, associated with future price reversals. We view this as evidence that the commonality of order flows in the cross-section of HFTs is the result of HFTs’ trades being informed, and as such have the same sign at approximately the same time. In other words, HFTs appear to be collectively buying and selling at the “right” time. The results are also in agreement with the conclusions of Chaboud, Chiquoine, Hjalmarsson, and Vega (2014), who find evidence of commonality among the trading strategies of algorithmic trades in the foreign exchange market, but who also find no evidence that such commonality appears to be creating price pressures and excess volatility that would be detrimental to market quality.

A final caveat is in order. The time period we examine is one of relative calm in the UK equity market. This means that additional research on the behaviour of HFTs, particularly during times of severe stress in equity and other markets, would be necessary in order to fully understand their role and impact on price efficiency.

DFA’s perspective is a little different. The underlying assumption in the paper is that more transactions gives greater market efficiency, and therefore HFT is fine. We are not so sure, as first the market efficiency assumption should be questioned, second it appears those without HFT loose out, so are second class market participants – those with more money to invest in market systems can make differentially more profit. This actually undermines the concept of a fair and open market. We think HFC needs to be better controlled to avoid an HFC arms race in search of ever swifter transaction times. To an extent therefore, the paper missed the point.

Strange? Of course: as BBG’s Brian Louis admits “it was an odd transaction from the outset: $14 million, double the going rate, for a 31-acre plot of flat, undeveloped land just west of Chicago. In the nine months since, the curious use of the space has only added to the intrigue. A single, nondescript pole with two antennas was erected by a row of shrubs. Some supporting equipment was rolled in. That’s it.”

Strange? Of course: as BBG’s Brian Louis admits “it was an odd transaction from the outset: $14 million, double the going rate, for a 31-acre plot of flat, undeveloped land just west of Chicago. In the nine months since, the curious use of the space has only added to the intrigue. A single, nondescript pole with two antennas was erected by a row of shrubs. Some supporting equipment was rolled in. That’s it.”Equipment on land purchased by an affiliate of Jump Trading

ASIC’s Key Findings

ASIC’s Key Findings