Wherever you look, the news is not good for those wishing to see housing affordability relief.

First demand for rentals continues to be powered by the overseas influx. New data from the Department of Home Affairs shows that at the end of February, the number of international students in Australia hit a record high of 713,144, whereas the number of temporary migrants in Australia hit a record high of 2.8 million (nearly 2.4 million excluding visitors).

Or put it another way, the number of student visa holders in Australia is running around 80,000 above the pre-pandemic peak, while the number of temporary visa holders excluding visitors is around 400,000 above the pre-pandemic peak.

Then we can turn to the question of new housing supply. I have covered before the fact that the country is littered with half-completed construction projects, many of which are competing for labour and resources with the large number of government and commercial projects also currently running. This crowded out home builders as the major projects sucked in labour and drove up its cost.

But we also continue to see more building firms going under. In the light of this, perhaps we should not be surprised that the total number of dwellings approved fell 1.9 per cent in February (seasonally adjusted), after a 2.5 per cent fall in January, according to data released on Thursday by the Australian Bureau of Statistics (ABS).

http://www.martinnorth.com/

Go to the Walk The World Universe at https://walktheworld.com.au/

Today’s post is brought to you by Ribbon Property Consultants.

This is an edited version of a live discussion with Leith van Onselen, Chief Economist at Nucleus Wealth, and co-founder of Macrobusiness. Leith has been leading the charge in highlighting how high migration is killing the property market. Tonight we look at the latest economic trends, and also will compare New Zealand with Australia.

Go to the Walk The World Universe at https://walktheworld.com.au/

Digital Finance Analytics (DFA) Blog

DFA Live Q&A HD Replay: Leith van Onselen: Economics Now!

Most would accept that house prices in the major Australian centres are too high. Whether you use a measure of price to income, loan value to income, or price to GDP; they are all above long term trends and higher than in most other countries.

Indeed, in Sydney and Melbourne, they are arguably more than 30% higher than they should be. Today we update our thoughts on this critical topic, and identify the winners and losers.

And by the way, if you value the content we produce please do consider joining our Patreon programme, where you can support our ability to continue to make great content.

Ultra-low interest rates currently make large loans affordable for many households, yet overall household debt is as high as it has ever been and mortgage stress, even at these low interest rates is also running hot. Banking regulators are concerned about systemic risks from overgenerous underwriting criteria and they have been lifting capital ratios to try to improve financial stability, with a focus on the fast growing investment sector and underscoring the need for lenders to consider loan servicability. The Royal Commission also uncovered poor lending practice, and the potential for some households to be sitting on unsuitable loans. In many countries around the world, house prices are also high, so from New Zealand to UK, regulators are taking steps to try limit systemic risks. These rises are partly being driven by global movements of capital, ultra-low interest rates and quantitative easing, plus the finance sectors ability to “magic” loans from thin air if there are borrowers willing to borrow. And now interest rates in the USA and Europe are on their way up, creating more pressure on households just as prices are beginning to wain.

Locally of course home prices are now sliding in many centres, and we expect more in the months ahead. However, let’s think about who benefits from high and rising prices. First anyone who currently holds property (and that is two-thirds of all households in Australia) will like the on-paper capital gains. This flows through to becoming an important element in building future wealth. In addition, refinancing is up currently, and we see some households crystalising some of their on-paper gains for holidays, a new car or other purposes, helping to stimulating retail activity. An RBA research paper, suggests that low-income households have a higher propensity to purchase a new vehicle following a rise in housing wealth than high-income households. We also see significant intergenerational wealth transfer as Mums and Dads draw out equity to help their kids buy into the overinflated market. Indeed, we think the Bank of Mum and Dad is now a top 10 lender in Australia, as we discussed recently.

Those holding investment property also enjoy tax-concessions on interest and other costs; and on capital appreciation. Rising wealth generally supports the feel-good factor, and consumer confidence – though currently this is a bit wonky as prices fall, rental streams tighten and interest rates rise. Higher values stimulate more transactions, which creates more momentum. The reverse is also true.

Now, the one-third of households who are not property active, consist of those renting and those living with family, friends or in other arrangements. Their confidence levels are lower and they are not gaining from rising house prices. A relatively small proportion of these are actively seeking to buy, and they are finding the gradient becoming ever more challenging, as saving for a deposit is becoming harder, lending criteria are tightening and income growth is slowing. We have noted previously that a rising number of first time buyers have switched directly to the investment sector to get into the market. Generally younger households are yet to get on the housing escalator, whilst older generations have clearly benefited from sustained house price growth, even if more are now taking mortgages into retirement. This has the potential to become a significant inter-generational issue.

But overall, the wealth effect of rising property is an umbrella which spreads widely. The sheer weight of numbers indicates that there are more winners than losers. No surprise then that many politicians will seek to bathe in the reflected glory of rising values, whilst paying lip-service to housing affordability issues. They will also start to panic if prices fall too far too fast.

There are other winners too. For states where property stamp-duty exists, the larger the transaction value and volume, the higher the income. For example, NSW, in 2016-17 added $9.7 billion to coffers thanks to stamp duties revenue which is 31.6% of the total of $30.7 billion. But now transfer duty revenue over the three years to 2020-21 has been revised down by $5.5 billion according to the state budget papers. Optimistically, they are forecasting a significant rise in property values down the track. The higher the price the larger the income. The tax-take funds locally provided services so ultimately residents benefit. But clearly they have an interest in keeping prices high.

The banks also benefit because rising house prices gives them the capacity to lend larger loans at lower risk (and which in turn allows house prices to run higher again). They have benefited from relatively benign capital requirements and funding, thus growing their balance sheet and shareholder returns. Whilst recent returns have been pretty impressive, future returns may be lower thanks to changes in capital ratios and especially if housing lending continues to moderates. On the other hand, their appetite to lend to productive business and commercial sectors is tempered by higher risks and more demanding capital requirements. The relative priority of debt to housing as opposed to productive lending to business is an important issue and whilst higher house prices can flow through to economic growth in the GDP numbers, it is mostly illusory. The truth is, lending needs to be redirected to productive purposes, not just to inflate home prices.

Finally, building companies can benefit from land banks they hold, and development projects, despite high local authority charges. We also note that some banks are now winding back their willingness to lend to the construction industry (because of potentially rising risks), and some banks have blacklists of postcodes where they will not lend, especially for newly constructed high-rise block. The real estate sector of course benefits, thanks to high transaction volumes and larger commissions. Mortgage brokers also enjoy volume and transaction related income. Even retailers with a focus on home furnishings and fittings are buoyant. But all of these sectors are under pressure as momentum ebbs.

So standing back, almost everyone appears to benefit from higher prices. That is, apart from the one third, and rising, of households renting (who tend to have lower incomes, and reside in lower socio-economic groups). But is it really a free-kick for the rest? Well, for as long as the music continues to play, it almost is. The question now is, what happens as prices continue to fall (remember that during the GFC, northern hemisphere prices fell in some places up to 40%, and several banks collapsed, though since then prices in the US, Ireland and the UK have started to recover). Given our exposure to housing, there will be profound impacts on households, banks and the broader economy if values fall significantly. Yet that looks like where we are headed.

Underlying all this, we have moved away from seeing housing as something which provides shelter and somewhere to live; to seeing it as just another investment asset class. This is probably an irreversible process, and part of the “financialisation” of society, given the perceived benefits to the economy and households, but we question whether the consequences are fully understood.

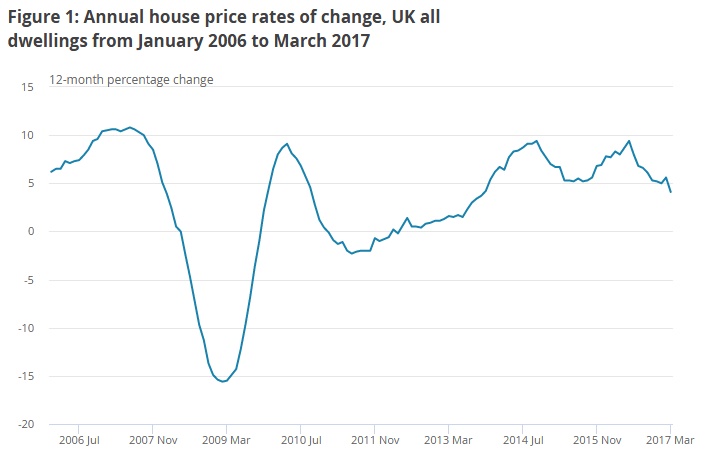

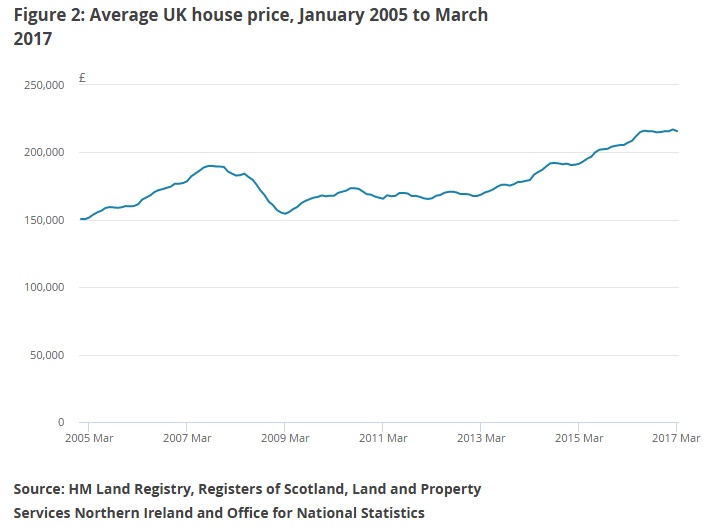

According to the UK’s Office for National Statistics, average house prices in the UK have increased by 4.1% in the year to March 2017 (down from 5.6% in the year to February 2017). This continues the general slowdown in the annual growth rate seen since mid-2016.

The average UK house price was £216,000 in March 2017. This is £9,000 higher than in March 2016 and £1,000 lower than last month.

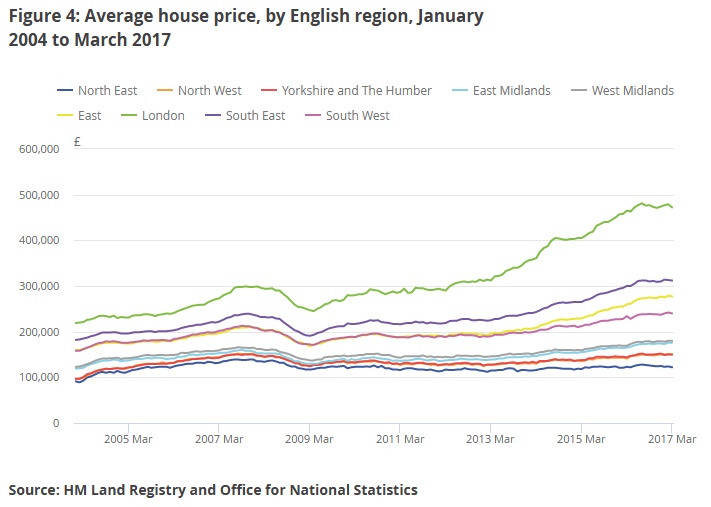

On a regional basis, London continues to be the region with the highest average house price at £472,000, followed by the South East and the East of England, which stand at £312,000 and £277,000 respectively. The lowest average price continues to be in the North East at £122,000.

The East of England and the East Midlands both showed the highest annual growth, with prices increasing by 6.7% in the year to March 2017. This was followed by the West Midlands at 6.5%. The lowest annual growth was in the North East, where prices decreased by 0.4% over the year, followed by London at 1.5%.

The UK HPI is a joint production by HM Land Registry, Land and Property Services Northern Ireland, Office for National Statistics and Registers of Scotland.

The UK House Price Index, introduced in June 2016, includes all residential properties purchased for market value in the UK. However, as sales only appear in the UK HPI once the purchases have been registered, there can be a delay before transactions feed into the index. As such, caution is advised when interpreting prices changes in the most recent periods as they are liable to be revised.

The problem is the political weight from home owners, banks, and the construction industry are all wedded to ever rising prices. The number of first time buyers are relatively small, so they have little political impact. Numbers count.

In addition, the regulators go out of their way to say all is well. We have questioned their stance on a number of occasions.

States benefit from high stamp duty returns, financial institutions can swell their balance sheets, and existing tax concessions assist investors who have enjoyed amazingly strong capital growth.

Tackling supply-side issues is indeed one factor, but we suspect there will be much talk and little action to address the long-term systemic issues – this is because the majority of households (and so voters) prefer prices to keep rising. So real political intervention is untenable, unless political leaders stand up. We think this is unlikely.

In addition, we have a diverse set of outcomes across the states, from rabid house price inflation in Sydney, to falling prices in Perth. There can be no-one size fits all solution, so the issues are complex and long term, and beyond the political cycle.

We believe that the current long term trends in housing are detrimental to Australians, and this is having a significant negative impact on the economic performance of the country.

We are not in a housing bubble, but we have a chronic problem. This is because the rapid growth in prices in recent years has not kept pace with many households ability to pay, forcing significant numbers into high debt to income ratio’s, the selection of properties in less accessible and less convenient locations and the exclusion of considerable numbers from the market. In total 2.3 million households are not active in the property market at all.

In addition, discretionary spending has been blotted up by higher housing costs. Households are highly leveraged today, and if interest rates were to rise, mortgage stress would become more significant.

Banks have grown their balance sheets in-line with growth in demand – especially supporting high levels of investment loans, and as a result they are not adequately providing reasonable lending services to a considerable number of small and medium enterprises, who could create economic value to the country. This is influenced by the relative capital costs of housing lending versus commercial lending under the Basel rules. Lending ever more loans to households to purchase property does not create real growth, it just inflates prices.

We believe there are significant supply-side issue, with at least 200,000 properties required to meet current and expected demand. A significant proportion of these should be aligned with the needs of the large number of “Want-to-Buy” households, who cannot access the market today. Today 1.2 million households are directly excluded from the market. Many of these are younger, less well-off and in rental property at the moment.

Local government policies and reliance on stamp duties are part of the problem, together with planning restrictions and high development fees and charges, all leading to poor supply of affordable homes. The proportion of high-rise developments is increasing.

Many First Time Buyers are only able to access the market with direct financial assistance from family or friends. The focus of First Time Buyer incentives being aligned to new-builds is welcome, but we believe that these incentives actually lift prices, and do long term harm.

In addition, we note there is considerable demand from both local and overseas investors, contending with potential First Time buyers.

Ultra-low interest rates are not helping because it is stimulating demand from the investment sector, lifting the size of loans, and negatively impacting affordability. Note that the banks rightly utilize buffers to test for affordability, so low rates do not flow into greater loan availability.

Negative gearing has been one of the most significant incentives for many investors, but it is widely accepted as a costly tax advantage which has pushed up prices, and driven First Time Buyers from the market.

For many, property has ceased to be primarily a place to live, it is rather an investment first and foremost. This is a concerning trend. Self-Managed Super Funds are also accessing investment property, thanks to the attractive tax sheltering which exists today.

DFA recommends the consideration of the following to help address affordability and accessibility of housing in Australia.

Australia should develop a strategic housing plan which guides ongoing development, be it in current centres, or expansion into new towns. Current tactical plans are not sufficient. The plan should specifically address the supply of affordable housing.

Strategies should be devised to increase land supply. State governments should reduce the current high levels of access fees for new development and revise planning criteria and processes. This has the potential to create considerable economic growth.

Overseas investors should not be able to access first-time buyer incentive schemes, and the Foreign Investment Review board rules should be strengthened to reduce the impact of foreign investors on the local market.

The RBA should have a direct multi-segmented housing affordability metric within its measurement framework. Affordability should be targeted at trend average, not rates experienced since the debt explosion of the 2000 onwards.

Macro-prudential policies should be employment to control the growth in lending. In line with the recommendations from the Bank of International Settlement debt to income servicing ratios should be employed as the policy tool of choice.

Negative gearing should be tapered away and removed for new transactions.

Joint equity schemes like the UK’s Help to Buy Scheme should be considered as a tactical step to assist some of the “Want-to-Buys.”

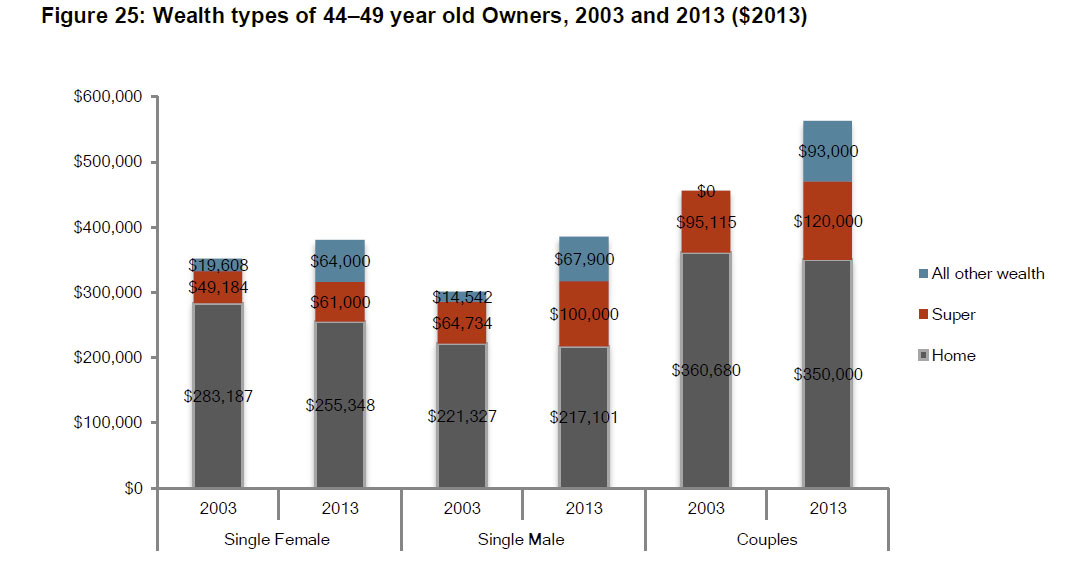

New research by the Swinburne Institute for Social Research, shows the wealth effect of holding property, and the risks in retirement of those unable to get on the ladder. In fact, a comfortable retirement is unlikely for those renting, because they are excluded from capital growth, which makes up such a large element of household wealth.

They also show that households who invested in property in 2013 were far more highly leveraged than those from 2003, reflecting changes in tax concessions, and growing household debt.

The report examined the wealth of people aged 40 to 64 years and recent retirees.

It evaluated the degree to which households can accumulate wealth for retirement, focusing on housing, and the impact of relationships and divorce or separation.

Lead researcher Dr Andrea Sharam says lone person and couple-only renters over 45 years of age tend to have little wealth.

“There are currently 425,000 people in lone person or couple households over 50 renting in Australia with this number expected to rise to 600,000 by 2030 and again to 830,000 by 2050.

“This number of impoverished older people equates to a huge increase in demand for housing assistance.”

Men and women are revealed to have different pathways into rental poverty in old age. For women the cost of care and the gender wage gap negatively affects them, while for men low educational achievement, consequential limited employment prospects and disability are factors.

“Relationship breakdown typically adversely impacts wealth with one if not both former partners often falling out of home ownership and not later recovering home ownership.

“Single mothers with young children are particularly vulnerable,” Dr Sharam says.

Policy recommendations

The report recommends a number of policy changes, including substantial community investment in social housing, and new affordable housing tenures aimed at midlife households who may not be eligible for social housing but also cannot afford full market house pricing.

“Social housing eligibility should be widened to order to cater for a broader range of incomes,” Dr Sharam says.

This would help prevent the loss of wealth associated with being a private renter and minimise the danger of retirees exhausting their resources before end of life.

The report also recommends better rights for renters, including:

security of tenure in residential tenancies legislation,

institutional investment in rental housing,

age-specific rental supplements, and

a National Rental Affordability Scheme (NRAS) type program targeted to age pensioners.

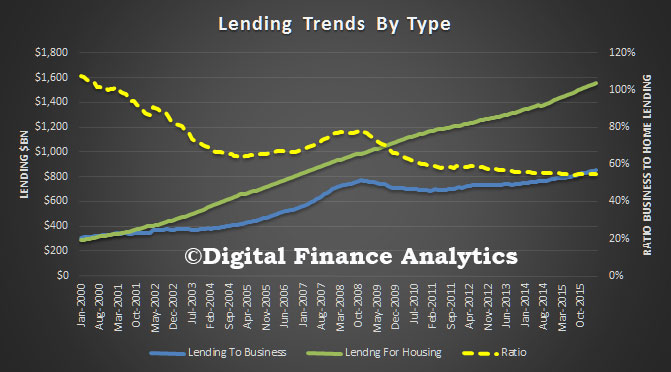

A snapshot of data from the RBA highlights the root cause of much of the economic issues we face in Australia. Back at the turn of the millennium, banks were lending relatively more to businesses than to households. The ratio was 120%. Roll this forward to today, and the ratio has dropped to below 60%. In other words, for every dollar lent now it is much more likely to go to housing than to business. This is a crazy scenario, as we have often said, because lending to business is productive – this generates real productive growth – whilst lending for housing simply pumps up home prices, bank balance sheets and household balance sheets, but is not economically productive to all.

There are many reasons why things have changed. The finance sector has been deregulated, larger companies can now access capital markets directly and so do not need to borrow from the bank, generous tax breaks (negative gearing and capital gains) have lifted the demand for loans for housing investment, and the Basel capital ratios now make it much cheaper for banks to lend against secured property compared to business. In fact the enhanced Basel ratios were introduced in the early 2000’s and this is when we see lending for housing taking off.

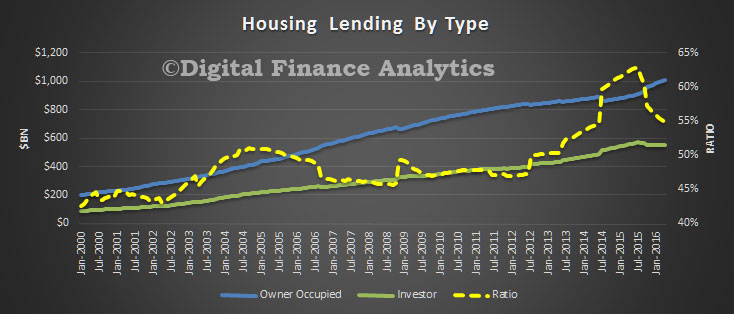

So how much of the mix is explained by tax breaks for investors? If we look at the ratio of home lending for owner occupation, to home lending for investment, there has been an increase. In 2000, it was around 45%, now its 55% (with a peak above 60% last year). This relative movement though is much smaller compared with the switch away from lending to business. Something else is driving it.

We therefore argue that whilst the election focus has been on proposed cuts to negative gearing and capital gains versus a company tax cut, the root cause issue is still ignored. And it is a biggie. The international capital risk structures designed to protect depositors, is actually killing lending to business, because it makes lending for housing so much more capital efficient. Whilst recent changes have sought to lift the capital for mortgages at the margin, it is still out of kilter. As a result, banks seek to out compete for mortgages and offer discounts and other incentives to gain share, whilst lending to business is being strangled. This is exacerbated by companies being more risk adverse, using high project hurdle thresholds (despite low borrowing rates) and smaller businesses being charged relatively more – based on risk assessments which are directly linked to the Basel ratios. Our SME surveys underscore how hard it is for smaller business to get loans at a reasonable price.

The run up in house prices is a direct result of more available mortgage funding, and this in turn leaves first time buyers excluded from the market. But it is too simple to draw a straight line between negative gearing and first time buyer exclusion. The truth is much more complex.

We are not convinced that a corporate tax cut, or a further cut in interest rates will stimulate demand from the business sector. Nor will reductions in negative gearing help that much. We need to re-balance the relative attractiveness of lending to business versus lending for housing. The only way to do this (short of major changes to the Basel ratios) is through targeted macro-prudential measures. In essence lending for housing has to be curtailed relative to lending to business. And that is a whole new box of dice!

According to the Domain House Price Report for the March Quarter, Melbourne and Hobart are the only capital cities where house prices are still rising. Sydney’s house prices fell, recording a quarter-on-quarter drop of 1.5 per cent, bringing the median down under the $1 million mark to $995,804. This 1.5 per cent drop when coupled with the 3.2 per cent fall in the December quarter, means prices have now dropped 4.7 per cent over six months. It’s an even bigger drop than Sydney experienced over 2008 during the global financial crisis, when the median dropped 4.6 per cent over the full year.

Canberra house prices fell by 1.4 per cent after five consecutive quarters of growth.

In Perth, house prices dropped by 1.3 per cent to $579,914 over the quarter, while Adelaide recorded a 0.5 per cent drop to $491,422, and prices in Brisbane fell by 0.05 per cent to $512,809.

The report showed that house prices in Hobart surged during the March quarter, rising by 4.3 per cent to $360,212, while Melbourne house prices rose by 1.2 per cent to $726,962.

Darwin house prices dropped sharply by 4.9 per cent to $610,305.

“Weakening economic activity and growing uncertainty is impacting fragile consumer and investment sentiment, leading to falling house and unit prices in most capital cities,” Domain chief economist Andrew Wilson said.

“The outlook for house prices remains subdued, with capital city growth likely to continue to track at best just above the inflation rate for the remainder of 2016.

“The prospect of weaker house price growth, however, will be welcomed by prospective first home buyers still struggling to get into the market.”

The boom’s over, but no crash is imminent. As Dr Wilson points out, the most recent drop in Sydney is less than the one in December. So there could be an even smaller fall in June. It’s not as if there’s been any major trigger to substantiate a more significant correction, like a large rise in interest rates or a jump in unemployment.

An interesting IMF working paper “Mitigating the Deadly Embrace in Financial Cycles: Countercyclical Buffers and Loan-to-Value Limits” examines the limitations of Basel III in the home loan market, and makes the point that the risk-weighted focus, even with enhancement, does not cut the mustard especially in a rising or falling property market. Indeed, there is a “deadly embrance” between housing, house prices, and bank mortgages which naturally leads to housing boom and bust cycles, which can be very costly for the economy and difficult for central banks to manage. They find that macroprudential measures may assist, but even then the deadly embrace remains.

The financial history of the last eight centuries is replete with devastating financial crises, mostly emanating from large increases in financial leverage. The latest example, the Global Financial Crisis of 2008-09, saw the unwinding of a calamitous run-up in leverage by banks and households associated with the housing market. As a result, the financial supervision community has acknowledged that microprudential regulations alone are insufficient to avoid a financial crisis. They need to be accompanied by appropriate macroprudential policies to avoid the build-up of systemic risk and to weaken the effects of asset price inflation on financial intermediation and the buildup of excessive leverage in the economy.

The Basel III regulations adopted in 2010 recognize for the first time the need to include a macroprudential overlay to the traditional microprudential regulations. Beyond the requirements for capital buffers, and leverage and liquidity ratios, Basel III regulations include CCBs between 0.0 and 2.5 percent of risk-weighted assets that raise capital requirements during an upswing of the business cycle and reduce them during a downturn. The rationale is to counteract procyclical-lending behavior, and hence to restrain a buildup of systemic risk that might end in a financial crisis. Basel III regulations are silent, however, about the implementation of CCBs and their cost to the economy, leaving it to the supervisory authorities to make a judgment about the appropriate timing for increasing or lowering such buffers, based on a credit-to-GDP gap measure. This measure, however, does not distinguish between good versus bad credit expansions and is irrelevant for countries with significant dollar lending, where exchange rate fluctuations can severely distort the credit-to-GDP gap measure.

One of the limitations of Basel III regulations is that they do not focus on specific, leverage-driven markets, like the housing market, that are most susceptible to an excessive build-up of systemic risk. Many of the recent financial crises have been associated with housing bubbles fueled by over-leveraged households. With hindsight, it is unlikely that CCBs alone would have been able to avoid the Global Financial Crisis, for example.

For this reason, financial supervision authorities and the IMF have looked at additional macroprudential policies. For the housing market, three additional types of macroprudential regulations have been implemented: 1) sectoral capital surcharges through higher risk weights or loss-given-default (LGD) ratios;3 2) LTV limits; and 3) caps on debt-service to income ratios (DSTI), or loan to income ratios (LTI). Use of such macroprudential regulations has mushroomed over the last few years in both advanced economies and emerging markets. At end-2014, 23 countries used sectoral capital surcharges for the housing market, and 25 countries used LTV limits. An additional 15 countries had explicit caps on DSTI or LTI caps. The experience so far has been mixed.in a sample of 119 countries over the 2000-13 period find that, while macroprudential policies can help manage financial cycles, they work less well in busts than in booms. This result is intuitive in that macroprudential regulations are generally procyclical and can therefore be counterproductive during a bust when bank credit should expand to offset the economic downturn.

Macroprudential regulations are often directed at restraining bank credit, especially to the housing market. They do not, however, take into account the tradeoffs between mitigating the risks of a financial crisis on the one side and the cost of lower financial intermediation on the other. In addition, given that these measures are generally procyclical, they can accentuate the credit crunch during busts. More generally, an analytical foundation for analyzing these tradeoffs has been lacking. MAPMOD has been designed to help fill this analytical gap and to provide insights for the design of less procyclical macroprudential regulations.

The MAPMOD Mark II model in this paper includes an explicit housing market, in which house prices are strongly correlated with banks’ credit supply. This corresponds to the experience prior and during the Global Financial Crisis. This deadly embrace between bank mortgages, household balance sheets, and house prices can be the source of financial cycles. A corollary is that the housing market is only partially constrained by LTV limits as the additional availability of credit itself boosts house prices, and thus raises LTV limits.

The starting point of the MAPMOD framework is the factual observation that, in contrast to the loanable funds model, banks do not wait for additional deposits before increasing their lending. Instead, they determine their lending to the economy based on their expectations of future profits, conditional on the economic outlook and their regulatory capital. They then fund their lending portfolio out of their existing deposit base, or by resorting to wholesale funding and debt instruments. Banks actively seek new opportunities for profitable lending independently of the size or growth of their deposit base—unless constrained by specific regulations.

In MAPMOD, Mark II, we extend the original model by introducing an explicit housing market. We use the modular features of the model to analyze partial equilibrium simulations for banks, households, and the housing market, before turning to general equilibrium results. This incremental approach sheds light on the intuition behind the model and simulation results.

The housing market is characterized by liquidity-constrained households that require financing to buy houses. A house is an asset that provides a stream of housing services to households. The value of a house to each household is the net present value of the future stream of housing services that it provides plus any capital gain/loss associated with future changes in house prices. We define the fundamental house price households are willing to pay to buy a house the price that is consistent with the expected income/productivity increases in the economy. If prices go above the fundamental house price reflecting excessive leverage, we refer to this as an inflated house price. The supply of houses for sale in the market is assumed to be fixed each period. House prices are determined by matching buyers and sellers in a recursive equilibrium with expected house prices taken as given. We abstract from many real-world complications such as neighborhood externalities, geographical location, square footage or other forms of heterogeneity.

Bank financing plays a critical role in the determination of house prices in the model. If banks provide a larger amount of mortgages on an expectation of higher household income in the future, demand for housing will go up, thus inflating house prices. Conversely, if banks reduce their loan exposure to the housing market, demand for houses in the economy will be reduced, leading to a slump in house prices. House prices therefore move with the credit cycle in MAPMOD, Mark II, just as in the real world.

Nonperforming loans and foreclosures in the housing market occur when households are faced with an idiosyncratic, or economy-wide, shock that affects their current LTV or LTI characteristics. Banks will seek to reduce the likelihood of losses by requiring a sufficiently high LTV ratio to cover the cost of foreclosure. But they will not be able to diversify away the systemic risk of a general fall in house prices in the economy. Securitization of mortgages in MAPMOD is not allowed. And even if banks were able to securitize mortgages, other agents in the economy would need to carry the systemic risk of a sharp fall in house prices. At the economy-wide level, the systemic risk associated with the housing market is therefore not diversifiable. The evidence from the Global Financial Crisis on securitization and credit default swaps confirms that this is the case, regardless of who holds mortgage-backed securities.

This paper presented a new version of MAPMOD (Mark II) to study the effectiveness of macroprudential regulations. We extend the original MAPMOD by explicitly modeling the housing market. We show how lending to the housing market, house prices, and household demand for housing are intertwined in the model in a what we call a deadly embrace. Without macroprudential policies, this naturally leads to housing boom and bust cycles. Moreover, leverage-driven cycles have historically been very costly for the economy, as shown most recently by the Global Financial Crisis of 2008–09.

Macroprudential policies have a key role to play to limit this deadly embrace. The use of LTV limits for mortgages in this regard is ineffective, as these limits are highly procyclical, and hold back the recovery in a bust. LTV limits that are based on a moving average of historical house prices can considerably reduce their procyclicality. We considered a 5 year moving average, but the length of the moving average used should probably vary based on the specific circumstances of each housing market.

CCBs may not be an effective regulatory tool against credit cycles that affect the housing market in particular, as banks may respond to higher/lower regulatory capital buffers by reducing/increasing lending to other sectors of the economy.

A combination of LTV limits based on a moving average and CCBs may effectively loosen the deadly embrace. This is because such LTV limits would attenuate the housing market credit cycle, while CCBs would moderate the overall credit cycle. Other macroprudential policies, like DSTI and LTI caps, may also be useful in this respect, depending on the specifics of the financial landscape in each country. It is, however, important to recognize that all these macroprudential policies come at a cost of dampening both good and bad credit cycles. The cost of reduced financial intermediation should be taken into account when designing macroprudential policies.

Note: IMF Working Papers describe research in progress by the author(s) and are published to elicit comments and to encourage debate. The views expressed in IMF Working Papers are those of the author(s) and do not necessarily represent the views of the IMF, its Executive Board, or IMF management.

Blog")