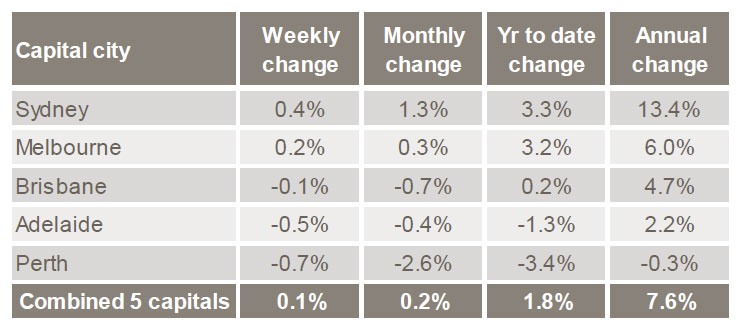

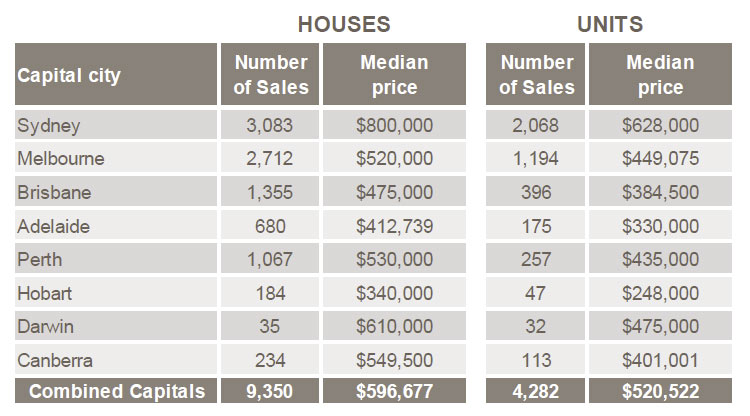

The ABS released their data on Residential Property Prices to March 2015. The total value of Australia’s 9.5 million residential dwellings increased to $5.5 trillion. The mean price of dwellings in Australia is now $576,100, an increase of $8,400 over the quarter. Sydney continues to drive residential property price increases with the Residential Property Price Index (RPPI) for Sydney rising 3.1 per cent in the March quarter 2015 and 13.1 per cent in the previous year. Established house prices for Sydney rose 3.8 per cent and attached dwelling prices rose 2.2 per cent.

The price index for residential properties for the weighted average of the eight capital cities rose 1.6% in the March quarter 2015. The index rose 6.9% through the year to the March quarter 2015. The capital city residential property price indexes rose in Sydney (+3.1%), Melbourne (+0.6%), Brisbane (+0.4%), Adelaide (+0.7%), Canberra (+1.1%) and Hobart (+0.5%) and fell in Darwin (-0.2%) and Perth (-0.1%). Annually, residential property prices rose in Sydney (+13.1%), Melbourne (+4.7%), Brisbane (+3.9%), Adelaide (+2.5%), Canberra (+3.0%) and Hobart (+1.9%) and fell in Darwin (-0.4%) and Perth (-0.3%).

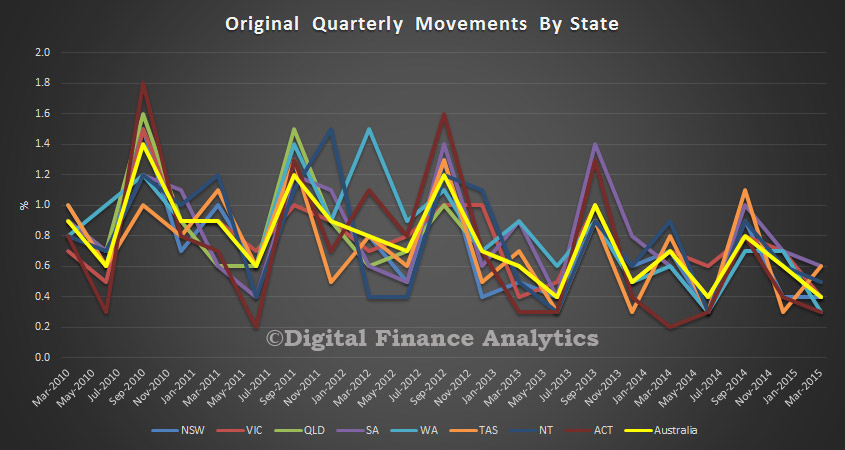

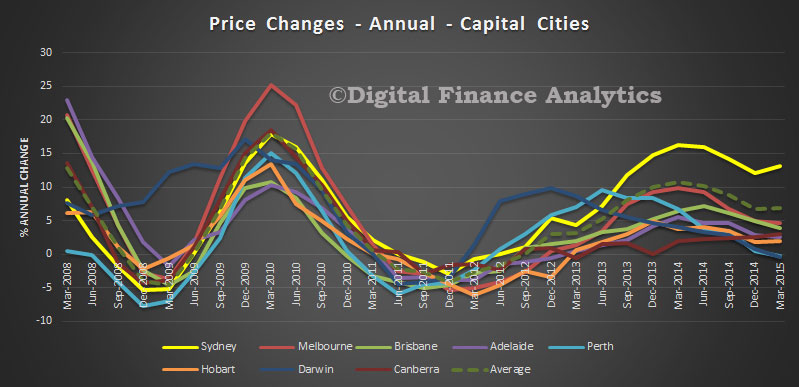

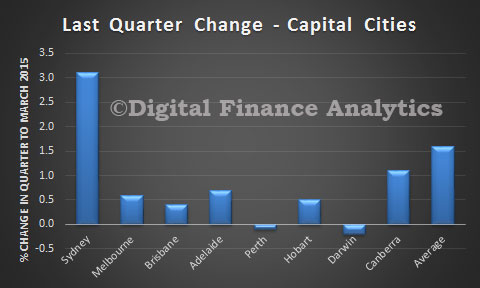

We see how Sydney steamed ahead of other states in the last quarter.

We see how Sydney steamed ahead of other states in the last quarter.

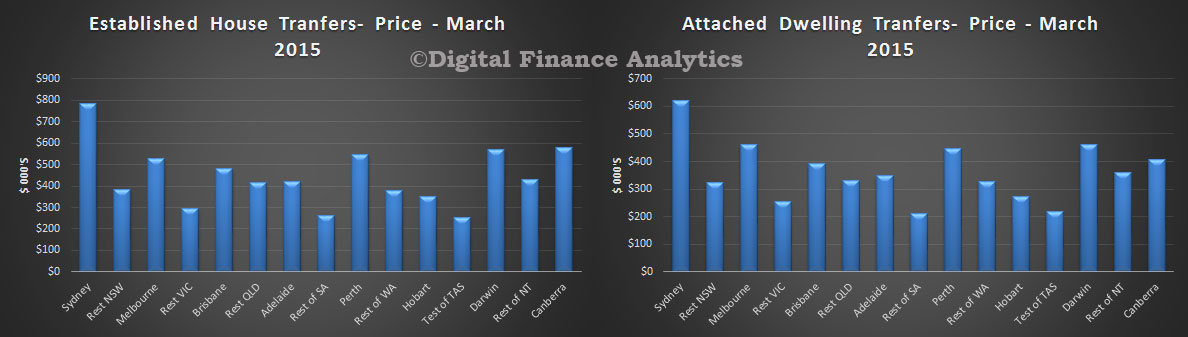

We also see significant differences between the relative price of established houses and attached dwellings in Sydney compared with other centres, the rest of the states outside the capital cities.

We also see significant differences between the relative price of established houses and attached dwellings in Sydney compared with other centres, the rest of the states outside the capital cities.

A review of the Residential Property Price Indexes was undertaken in 2014 as a response to planned reductions to the ABS work program. The outcomes of the Review were released on the ABS website in a feature article in the September 2014 issue of Residential Property Price Indexes: Eight Capital Cities. The implementation of the review outcomes is occurring in this issue.

In summary, the changes in this issue are:

- all Australian residential property sales data used to compile the price indexes and related statistics are now supplied to the ABS by CoreLogic RP Data;

- from the March quarter 2015 the suite of residential property price indexes are considered final;

- the method of calculating prices in the total value of the dwelling stock has been modified due to the change in timing of this release;

- the unstratified median price and number of dwelling transfers series are now being published up to the current quarter.