Deloitte Access Economics’ Chris Richardson recently suggested that young Australians would be better off renting than trying to buy a house. He argued:

… rents today make a lot more sense than housing prices.

This may be true. However, the situation for renters is far from clear-cut. Rents continue to increase in Australian cities, and are out of reach for low- and very-low-income earners.

Renters also face substantial housing insecurity. In Australia, 50% of renters are on a fixed-term one-year lease; 20% are on a month-to-month “rolling” lease.

For renting to become a truly viable, long-term alternative to home ownership, greater rental affordability and security is needed.

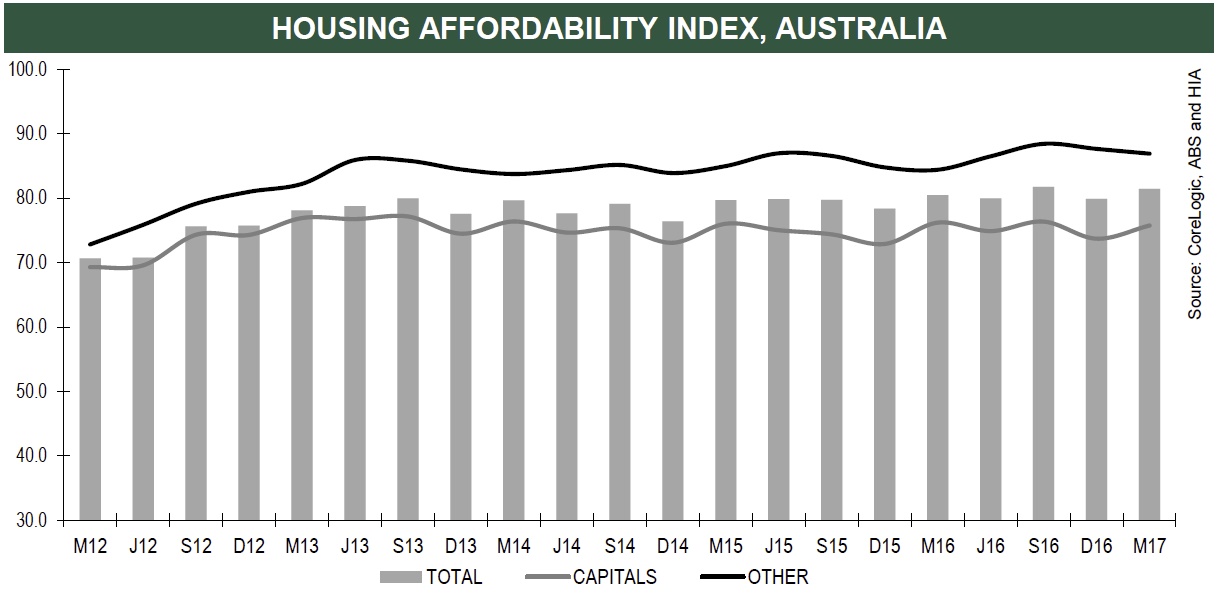

Rental affordability

Longer-term structural changes to tackle housing affordability, including boosting the supply of social housing and increasing tenure diversity, will be essential. There are some promising moves, including the recently announced proposal for a bond aggregator model to fund social and affordable housing.

Failing a substantial increase in affordable housing, there will be a need to increase rent assistance payments, particularly in high-cost regions.

This acknowledges that housing costs differ across the country and that many low-income earners need to remain in high-cost regions. This includes older people whose social and family networks are in these regions, and people who work in these areas.

Many industries in high-cost cities are dependent on people who earn low and very-low incomes. These people have a right – and need – for affordable, secure housing – and a house that is a home.

Affordability is the thin end of the wedge

For renting to become a true alternative to home ownership, greater rental security is needed.

To move toward secure rentals we need to reward long-term investment. One example might include encouraging institutional investors, including superannuation companies and other businesses that invest in large amounts of rental housing, who are in it for the long haul.

However, there is no reason to assume that institutional investors will offer more affordable rental properties, or be any better landlords than so-called “mum and dad” investors. We therefore need to pursue changes to rental laws to ensure renters, including the growing generation of long-term renters, can experience a secure sense of home. Specific changes include:

Removing no-grounds eviction. The perceived risk of eviction leads to stress for renters. And the right to no-grounds eviction can lead to retaliatory eviction by landlords when tenants exercise their rights, including rights to maintenance and repairs.

The Tenants’ Union of NSW has called for a balancing of landlord and tenant interests through tenancy laws that specify reasonable grounds for termination.

Such laws could follow the German example. In Germany, rental laws ensure security of tenancy while retaining the right of landlords to terminate a lease in certain circumstances, such as if a tenant violates the lease agreement (for example, by not paying rent) or if the landlord requires the property for personal use.

Rent increases are sometimes a “backdoor” way of evicting tenants. In a recent survey, 11% of renters reported receiving a “rent hike after requesting a repair and 10% said that their landlord or agent became angry”. We need stronger regulation of rent increases and stronger penalties for unreasonable increases.

There are precedents for this in other jurisdictions. Germany again provides a great example. There, rent increases are allowed less frequently. And they:

… must be based in the rents of three similar dwellings or a database of local reference rents and rents may not increase more than 20% over three years.

Ensuring the right to make a home. Rental laws need to ensure the right of tenants to make their house into a home, including making cosmetic changes to a property, ability to keep pets, and allowing alterations that would allow an older person or person with a disability to live there.

Some older renters I have interviewed recently have had to move after these types of adjustments were rejected by landlords who thought age-related modifications were not attractive.

In New South Wales, the right to make changes that would ensure a property is liveable for people with different housing needs is being considered as part of the current residential tenancy law review. However, the right to make cosmetic changes is excluded.

Popular wisdom often suggests that tenants and landlords have different interests. In fact, they have very similar interests. Both benefit from secure tenancies and a property that is well maintained and cared for.

Failure to ensure rental affordability and security will require a raft of policy changes in other areas, including pension income calculations that assume home ownership. It will also condemn a generation of long-term renters to increasingly unaffordable and insecure housing.

Author: Emma Power, Senior Research Fellow, Geography and Urban Studies, Western Sydney University