How to fix the UK’s housing crisis has been the subject of national debate for decades. Universal home ownership is a popular goal, which successive governments have failed to achieve. This is largely because they have been faced with the paradox of increasing the supply of affordable housing while not encouraging house prices to fall, as this is widely regarded as political suicide.

One solution has been to promote policies that make it easier to get a mortgage or boost disposable income so that it rises faster than house prices. In fact, nearly ten years after a global financial crisis caused by the ready availability of mortgages to households with no ability to repay them, the UK government maintains its “Help to Buy” initiatives. These focus on helping people to borrow the large sums necessary to pay for unaffordable homes.

What has been missing from the debate is the role that renting can play in solving the UK’s housing problems. The government’s latest white paper is significant in that it features policies to help renters. But ownership remains the ultimate goal.

In the UK there is social and political pressure for people to “get a foot on the housing ladder” – even when, in many cases, it is financially preferable for households to rent. Although the benefits of home ownership are many, one should ask whether it is wise for governments to encourage – and subsidise – people to take on debt that they would otherwise not be able to afford, in order for them to place all of their financial resources into an asset that may be overvalued or unsuitable.

Must you get on the ladder? shutterstock.com

Eggs in one basket

One of the most basic rules of investment is “don’t put all your eggs in one basket”. Yet most households do just that when they buy a home and then they leverage this investment by borrowing money.

This is much riskier than placing all of your money in a fund that tracks the global stock market. Not only is it difficult to sell a house when you urgently need the money, if house prices fall – even by a not unusual 10% – your losses will be multiplied by the gearing effect of the mortgage. For example, if all of your savings amount to £20,000 and you use this as a 10% deposit to buy a £200,000 home, then you borrow the remaining £180,000, a 10% price fall will leave you with no savings and owing money to the bank if you then try to sell.

For previous generations, from the late 1970s onwards, the risk of homeownership has paid a commensurately high return because inflation has been generally positive but benign. And, at the same time, interest rates have trended down from double digits towards zero.

For those contemplating buying their first home today, however, the outlook for both interest rates and inflation is more uncertain. For example, Japan and more recently some eurozone countries have experienced prolonged periods of deflation. In the UK, despite efforts to keep inflation positive, actual realised inflation has been consistently below the Bank of England’s forecasts from the second quarter of 2013 until January.

Don’t bet on inexorable rises. shutterstock.com

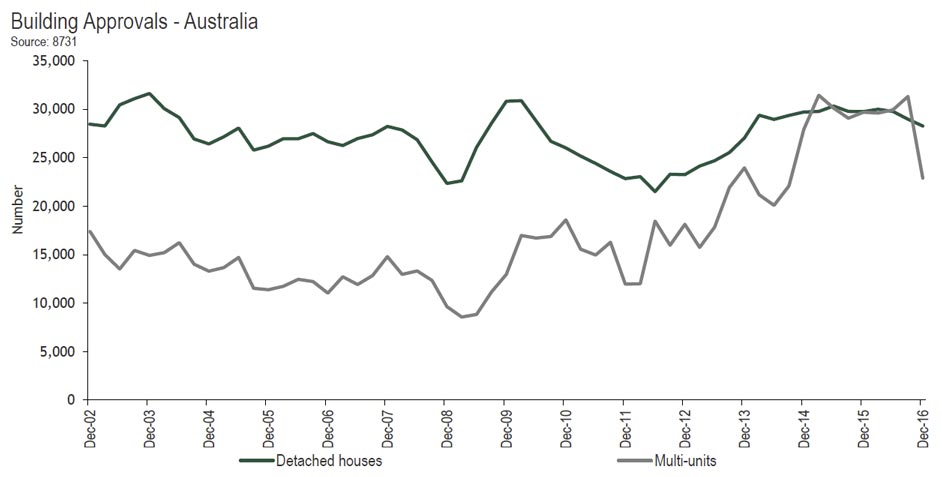

House prices vary substantially over time relative to both GDP and household income – confirming that housing is a risky investment. Furthermore, in markets where building land is in short supply (such as Japan and many parts of the UK), this variability is greater than in markets such as the US where it is more readily available to meet demand.

When renting is better

In a recent paper I demonstrate that renting can be a better financial option than buying in a number of circumstances. These include: if you do not plan to live in the same house for at least five to ten years; or if inflation is negative (deflation); or if the net rent saved by owning is less than your mortgage interest or the return you could have achieved by putting your money in other investments with a similar level of risk.

This is because rent typically includes substantial ownership costs such as building insurance, property maintenance and furnishing. So the money saved by owning a house is considerably less than the rent not paid. Another reason is that buying and selling houses incurs substantial transaction costs in the form of legal fees, transaction tax (stamp duty) and selling agents’ fees. These are much higher than rental transaction costs. So unless you plan to stay in the new home for a considerable time, the chances are that these higher costs will not be recouped by savings from rent or price appreciation.

Plus, although prices have tended to drift up in the long term, prices can and do fluctuate substantially in the medium term (five to ten years). So if you plan to relocate within a few years there is a greater risk of being unlucky in your timing and suffering a price loss.

Finally, purchasing a home fixes your housing costs and often incurs a substantial mortgage liability. This is good if prices and wages are generally rising – because the mortgage payments become more affordable as incomes rise. But, in a world of low inflation or deflation, mortgage liabilities remain fixed, but incomes, prices and rents tend to decline making it harder to sustain mortgage payments and harder to recoup the capital invested in buying.

There are many ways that governments can influence the affordability of housing besides helping financially constrained households to concentrate all of their savings into risky assets that they would not otherwise be able to afford. Allowing house prices to drop will always be politically difficult – homeowners tend to make up the bulk of the electorate that turns out to vote. But they could do much more to encourage renting, even if it does require a radical rethink in the British mindset when it comes to home ownership.

Author: , Senior Lecturer in Finance, Director of the MSc in Finance, University of Stirling

The Treasurer’s media release said

The Treasurer’s media release said

The Lend Lease housing development in London is designed to provide affordable housing but also ensure profits for developers. Picture: Ella Pellegrini

The Lend Lease housing development in London is designed to provide affordable housing but also ensure profits for developers. Picture: Ella Pellegrini