ASIC will now look at individual loan files, especially from lenders with high IO portfolios, in the light of the responsible lending provisions.

Announced in April 2017, the review was a targeted industry surveillance examining whether lenders and mortgage brokers are inappropriately recommending more expensive interest-only loans.

With many lenders, including major lenders, charging higher interest rates for interest-only loans compared with principal-and-interest loans, lenders and brokers must ensure that consumers are not provided with unsuitable interest-only home loans.

ASIC has concluded the first stage of its targeted review, which involved data collection from 16 home loan providers (including large banks, mid-tier and smaller banks, and non-bank lenders).

ASIC found that Australia’s major banks have cut back their interest-only lending by $4.5 billion over the past year. However, other lenders have partially offset this decline by increasing their share of interest-only lending.

The 16 lenders reviewed by ASIC provided $14.3 billion in interest-only loans to owner-occupiers in the June 2017 quarter, down from $19 billion in the September 2015 quarter.

ASIC’s interest-only lending review has also found:

- Borrowers who used brokers were more likely to obtain an interest-only loan compared to those who went directly to a lender

- Borrowers approaching retirement age continue to be provided with a significant number of interest-only owner-occupier loans

ASIC has now moved into the second stage of its review, and will be reviewing individual loan files from both lenders and mortgage brokers. These lenders and mortgage brokers have been selected based on a number of criteria, including their relative share of interest-only home lending.

ASIC will examine individual loan files to ensure that lenders are providing interest-only home loans in appropriate circumstances. ASIC will carefully review cases where owner-occupiers have been provided with more expensive interest-only home loans, to ensure that consumers are not paying for more expensive products that are unsuitable.

Under the responsible lending obligations, lenders and brokers are required to make sure that a loan meets the requirements and objectives of a consumer, in addition to making sure that the loan is affordable. Lenders and brokers must have a reasonable basis for suggesting that a consumer apply for a particular loan product, and no consumer should be surprised by the type of home loan product that they have obtained.

In providing the update, ASIC Deputy Chair Peter Kell said he expected lenders offering these types of loans to be making thorough enquiries into the financial status and the needs of their clients:

“The spotlight has been firmly on interest-only lending for some time, and there are no excuses for lenders and brokers not meeting their legal obligations,” he said.

“While interest-only loans may be a reasonable option for some borrowers, lenders must make appropriate enquiries into the needs and financial circumstances of their customers, and they must be able to demonstrate that they have done so.”

ASIC will consider appropriate enforcement action if breaches of the law are identified.

Background

ASIC collected data from the following lenders covering their interest-only lending activities over the last two years:

- Australia and New Zealand Banking Group Limited

- Australian Central Credit Union Ltd (trading as People’s Choice Credit Union)

- Bank of Queensland Limited

- Bendigo and Adelaide Bank Limited

- Citigroup Pty Limited

- Commonwealth Bank of Australia

- ING Bank (Australia) Limited

- La Trobe Financial Services Pty Limited

- Liberty Financial Pty Ltd

- Macquarie Bank Limited

- Members Equity Bank Limited

- National Australia Bank Limited

- Pepper Group Limited

- Suncorp-Metway Limited

- Teachers Mutual Bank Limited

- Westpac Banking Corporation

ASIC has provided guidance to industry in Regulatory Guide 209 Credit licensing: Responsible lending conduct (refer: RG 209).

In 2015, ASIC reviewed interest-only loans provided by 11 lenders and issued REP 445 Review of interest-only home loans (refer: REP 445), which made a number of recommendations for lenders to comply with their responsible lending obligations (refer: 15-297MR).

In 2016, ASIC reviewed the practices of 11 large mortgage brokers and released REP 493 Review of interest-only home loans: Mortgage brokers’ inquiries into consumers’ requirements and objectives (refer: REP 493). REP 493 identified good practices as well as opportunities to improve brokers’ practices.

Responsible lending is a key priority for ASIC in its regulation of the consumer credit industry. ASIC’s targeted surveillance of interest-only lending follows considerable regulatory activity focused on responsible lending compliance:

- Treasury releases ASIC’s Review of Mortgage Broker Remuneration.

- ASIC announces further measures to promote responsible lending in the home loan sector (refer: 17-095MR).

- ASIC filed civil penalty proceedings against Westpac in the Federal Court on 1 March 2017 for alleged breaches of the National Consumer Credit Protection Act 2009 (refer: 17-048MR).

Borrowers with concerns about their ability to make home loan repayments should contact their lender in the first instance. ASIC’s MoneySmart website has guidance for consumers who are having problems paying their mortgage, including how to approach their lender. They can also access free external dispute resolution, through either the Financial Ombudsman Service or Credit and Investments Ombudsman.

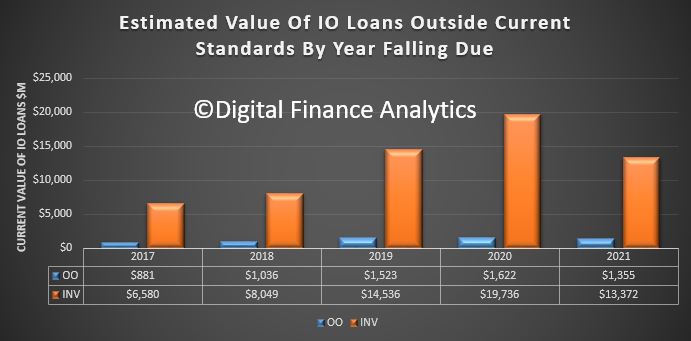

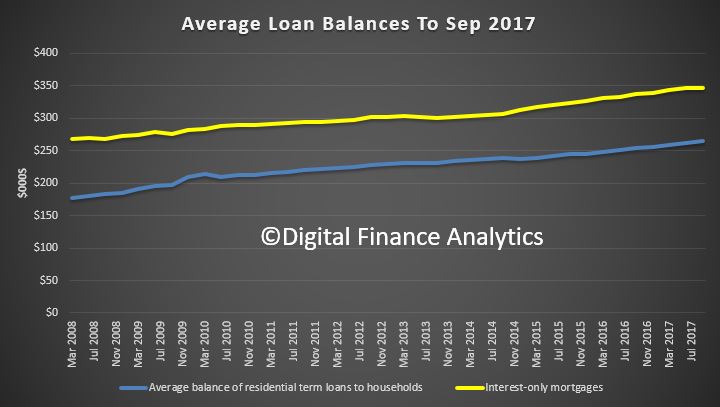

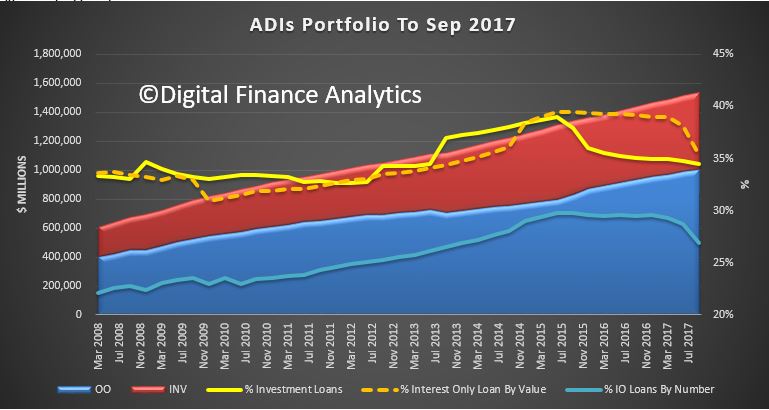

We also see a fall in the volume of investment loans being held on book. As the lions share of interest only lending has been for investment purposes, this is of no surprise.

We also see a fall in the volume of investment loans being held on book. As the lions share of interest only lending has been for investment purposes, this is of no surprise.