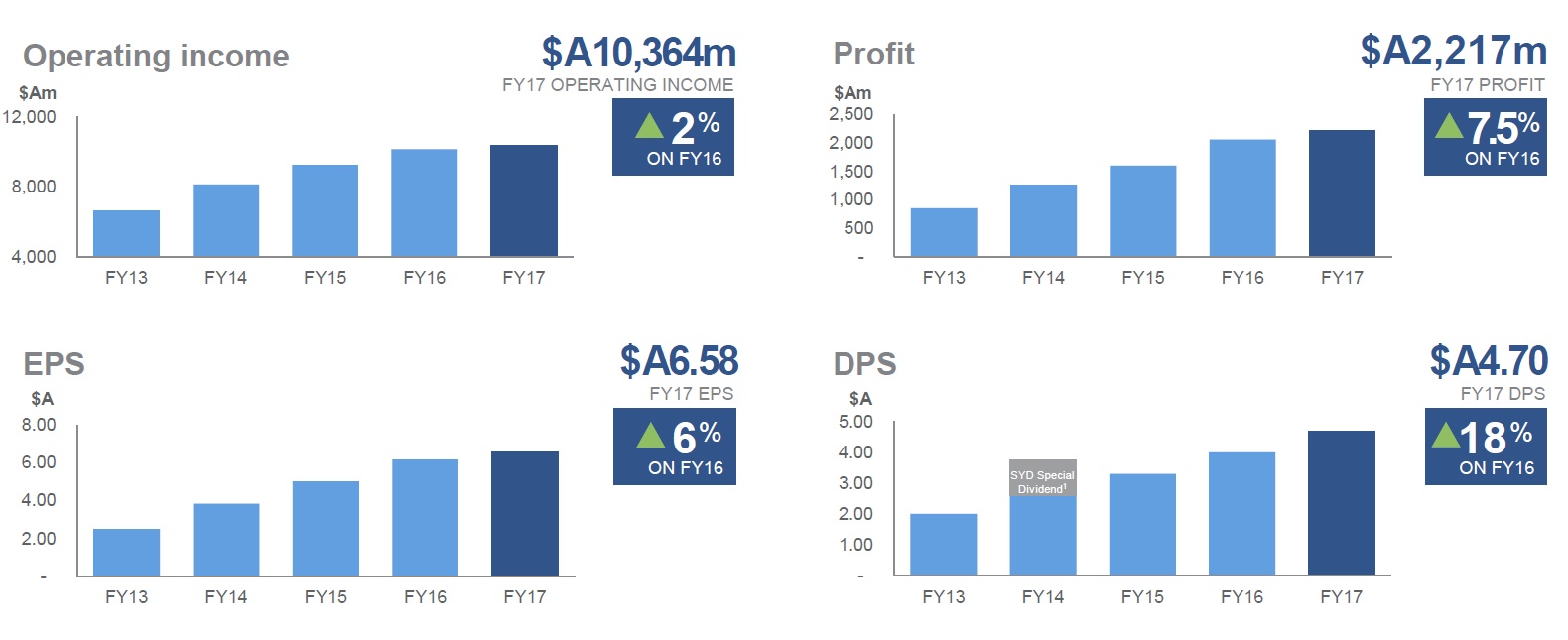

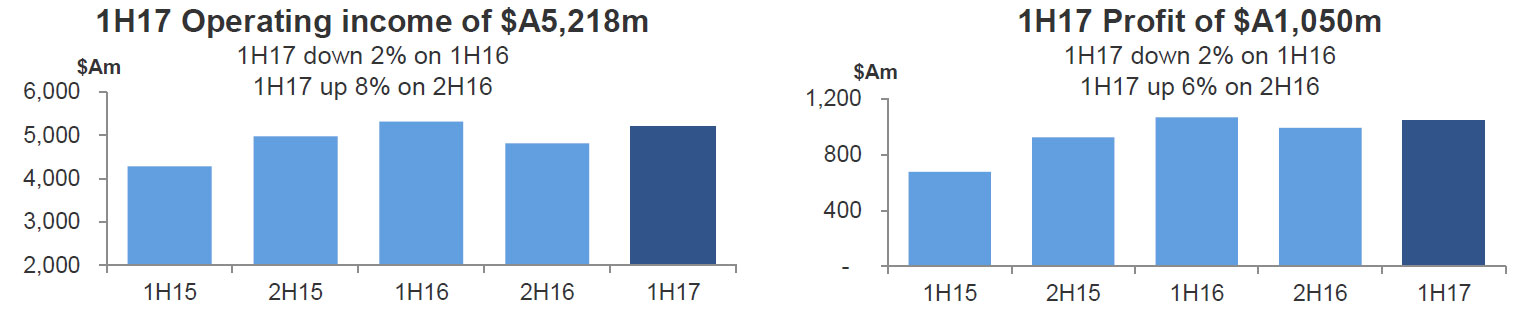

Macquarie Group today announced a net profit after tax attributable to ordinary shareholders of $A1,050 million for the half-year ended 30 September 2016 (1H17), down two per cent on the half-year ended 30 September 2015 (1H16) and up six per cent on the half-year ended 31 March 2016 (2H16).

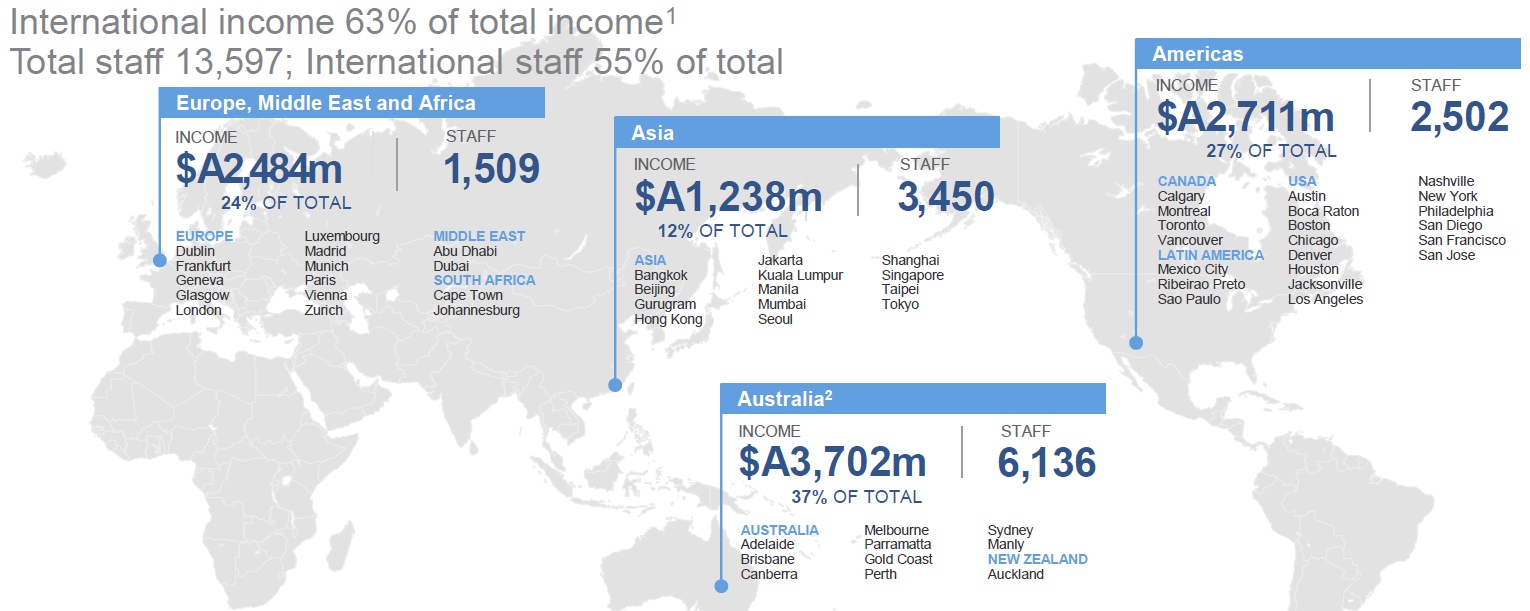

Net operating income of $A5,218 million for 1H17 was down two per cent on 1H16, while total operating expenses of $A3,733 million were up one per cent on 1H16. Around 60% came from international sources.

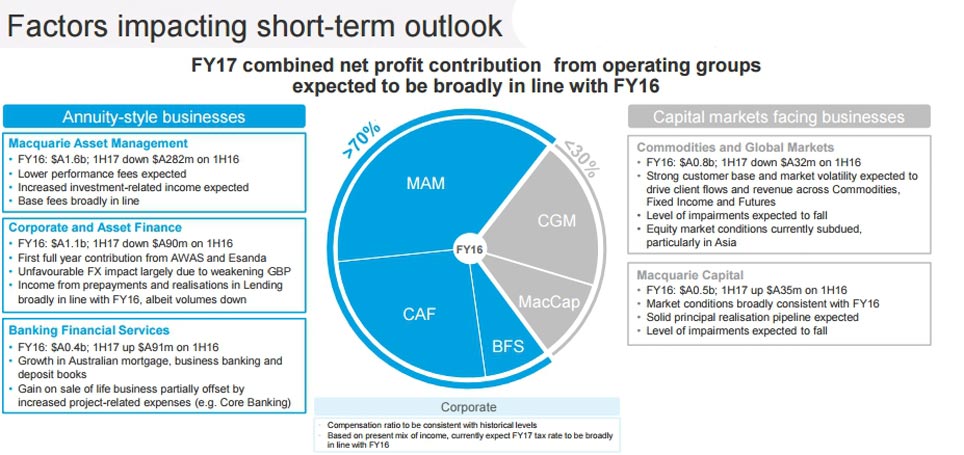

Macquarie’s annuity-style businesses (Macquarie Asset Management, Corporate and Asset Finance and Banking and Financial Services), which represent approx. 70% of the Groups’ performance, continued to perform well with a full period contribution from AWAS/Esanda as well as a gain on the disposal of Macquarie Life compared to a pcp which benefited from significant performance fees in MAM (1H16) and gave a combined net profit contribution of $A1,639 down 15% on 1H16 and up 36% on 2H16.

Macquarie’s annuity-style businesses (Macquarie Asset Management, Corporate and Asset Finance and Banking and Financial Services), which represent approx. 70% of the Groups’ performance, continued to perform well with a full period contribution from AWAS/Esanda as well as a gain on the disposal of Macquarie Life compared to a pcp which benefited from significant performance fees in MAM (1H16) and gave a combined net profit contribution of $A1,639 down 15% on 1H16 and up 36% on 2H16.

Macquarie’s capital markets facing businesses (Macquarie Securities Group, Macquarie Capital and Commodities and Financial Markets) benefited from lower impairments and increased principal realisations in MacCap and CFM, offset by lower trading activity gave a combined net profit contribution of $A695m broadly in line with 1H16 and up 15% on 2H16.

Operating expenses were $A3,733m, up 1% on 1H16 and up 9% on 2H16.

Macquarie announced an interim ordinary dividend of $A1.90 per share (45 per cent franked), up from the 1H16 dividend of $A1.60 per share and down from the 2H16 dividend of $A2.40 per share, both 40 per cent franked. This represents a payout ratio of 62 per cent.

Key drivers of the change from the prior corresponding period (1H16) were:

- An 18 per cent decrease in combined net interest and trading income to $A1,864 million, down from $A2,273 million in 1H16. The reduction was across a number of operating groups. MSG was impacted by limited trading opportunities due to market uncertainty. In CAF, there was an overall decline in net interest and trading income mainly driven by the timing of prepayments and realisations, and lower loan volumes in the Lending portfolio, as well as increased funding costs due to the AWAS portfolio acquisition, partially offset by the contribution from the Esanda dealer finance portfolio. CFM also reported lower net interest and trading income compared to 1H16 due to reduced client flow, particularly in oil. Partially offsetting these declines was increased net interest and trading income in BFS, mainly driven by volume growth in the Australian loan and deposit portfolios

- A 21 per cent decrease in fee and commission income to $A2,202 million, down from $A2,794 million in 1H16. Performance fees were $A170 million in 1H17, down 73 per cent on 1H16 which benefited from significant performance fees of $A629 million, while mergers and acquisitions, advisory and underwriting fees of $A471 million in 1H17 decreased 12 per cent from $A537 million in 1H16 due to more subdued equity capital markets activity in most key regions. Brokerage and commissions income of $A419 million was also down on 1H16 as market uncertainty impacted the levels of client trading activity, particularly in Asia.

- A 20 per cent increase in net operating lease income to $A476 million, up from $A397 million in 1H16, mainly driven by the AWAS portfolio acquisition in CAF.

- Other operating income of $A684 million in 1H17 increased significantly from a charge of $A83 million in 1H16. The primary drivers were increased gains on the sale of investments and businesses; and lower provisions for impairment mainly due to reduced exposures to underperforming commodity-related loans in CFM. Gains on the sale of businesses and investments included a significant gain from BFS’ sale of Macquarie Life’s risk insurance business, as well as increased contributions from Macquarie Capital, CFM and MAM, partially offset by a loss on the sale of BFS’ US mortgages portfolio.

- Total operating expenses increased one per cent, driven by increased non-salary technology expenses mainly due to elevated project activity as well as a change in approach to the capitalisation of software expenses in relation to the Core Banking platform in BFS, offset by decreased brokerage, commission and trading-related expenses mainly due to decreased trading-related activity, while employment expenses remained broadly in line with 1H16.

Staff numbers were 13,816 at 30 September 2016, down from 14,372 at 31 March 2016.

The income tax expense for 1H17 was $A438 million, down 17 per cent from $A530 million in 1H16 mainly due to a decrease in operating profit before income tax, as well as changes in the geographic composition of earnings, with increased income being generated in Australia and the UK, and lower income in the US. The effective tax rate of 29.4 per cent was down from 33.1 per cent in 1H16.

Total customer deposits increased by 5.7 per cent to $A46.1 billion at 30 September 2016 from $A43.6 billion at 31 March 2016. During 1H17, $A4.0 billion of new term funding was raised covering a range of sources, tenors, currencies and product types.

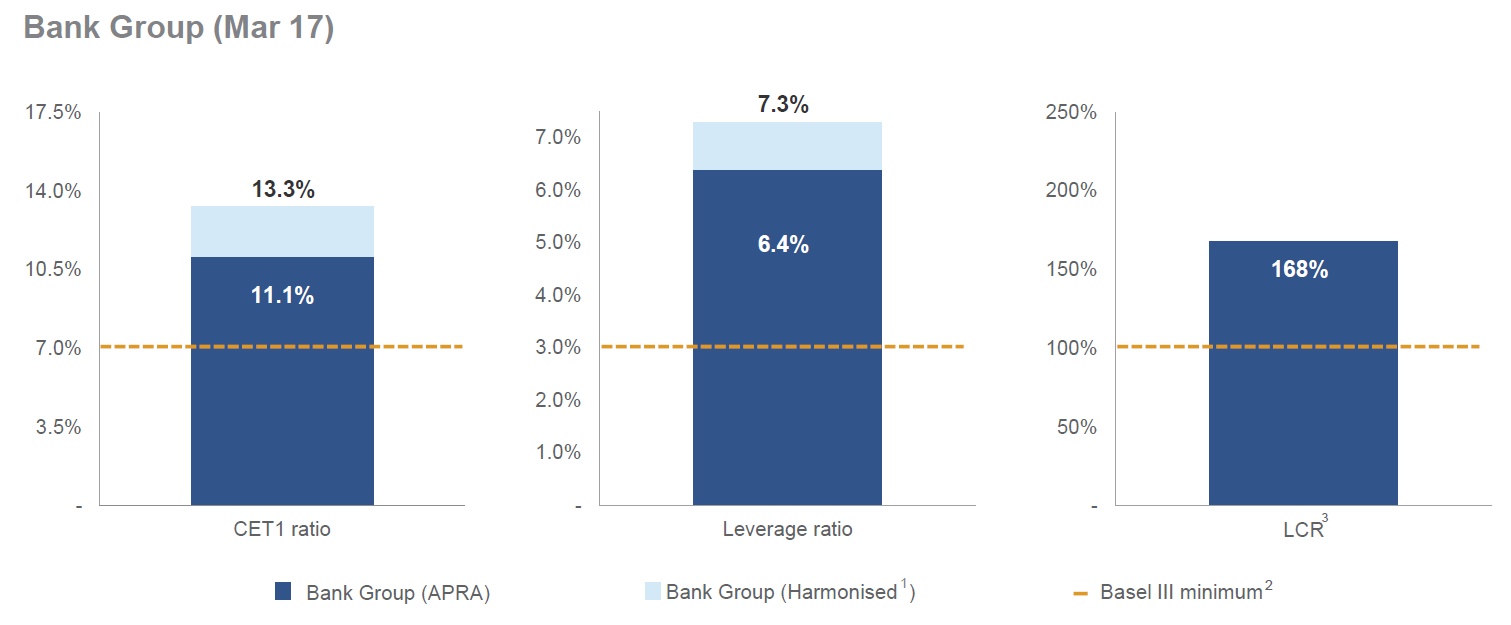

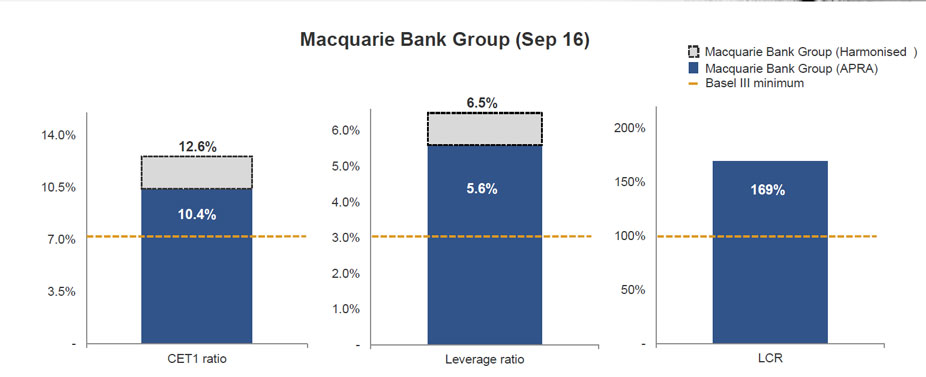

Macquarie Group’s financial position comfortably exceeds APRA’s Basel III regulatory requirements, with Group capital surplus of $A3.7 billion at 30 September 2016, which was down from $A3.9 billion at 31 March 2016.

The Bank Group APRA Basel III Common Equity Tier 1 capital ratio was 10.4 per cent (Harmonised: 12.6 per cent) at 30 September 2016, down from 10.7 per cent at 31 March 2016. The Bank Group’s APRA leverage ratio was 5.6 per cent (Harmonised: 6.5 per cent) and average LCR was 169 per cent.

Operating group performance

Macquarie Asset Management delivered a net profit contribution of $A857 million for 1H17, down 25 per cent from $A1,139 million in 1H16, and up 70 per cent from $A505 million in 2H16, mostly due to performance fees and investment-related income. Performance fee income in 1H17 decreased 72 per cent from a particularly strong 1H16 of $A609m, and increased 102 per cent from $A84 million in 2H16, and included performance fees from Macquarie Atlas Roads (MQA), Macquarie Korea Infrastructure Fund (MKIF), Australian managed accounts and from co-investors in respect of infrastructure assets. Investment-related income included gains from the partial sale of MIRA’s holding in MQA, gains on sale of unlisted real estate holdings in MIRA and income from the sell down of infrastructure debt in Macquarie Specialised Investment Solutions (MSIS). Base fee income was broadly in line as investments made by MIRA-managed funds, growth in the MSIS Infrastructure Debt business and positive market movements in MIM, were largely offset by small net AUM outflows in the MIM business, asset realisations by MIRA-managed funds and foreign exchange impacts. Assets under management of $A491.3 billion decreased two per cent on 30 September 2015.

Corporate and Asset Finance delivered a net profit contribution of $A521 million for 1H17, down 15 per cent from $A611 million in 1H16. The decrease was mainly driven by lower income due to the timing of prepayments and realisations as well as lower loan volumes, which resulted in a reduced contribution from the Lending portfolio. This was partially offset by profit from the AWAS portfolio acquisition and the acquisition of the Esanda dealer finance portfolio in the prior year. The AWAS and Esanda acquisitions have been successfully integrated and continue to perform in line with expectations. CAF’s asset and loan portfolio of $A38.1 billion increased 17 per cent on 30 September 2015.

Banking and Financial Services delivered a net profit contribution of $A261 million for 1H17, up 54 per cent from $A170 million in 1H16. The improved result reflects increased income from growth in Australian lending, deposit and platform volumes, as well as a gain on sale of Macquarie Life’s risk insurance business.

This was partially offset by a loss on the disposal of the US mortgages portfolio, increased costs mainly due to elevated project activity as well as a change in approach to the capitalisation of software expenses in relation to the Core Banking platform, and increased impairment charges on loans, equity investments and intangible assets ($A78m). BFS deposits of $A42.2 billion increased nine per cent on 30 September 2015 and funds on platform of $A62.1 billion increased 33 per cent on 30 September 2015. The Australian mortgage portfolio of $A28.6 billion increased four per cent on 30 September 2015, representing approximately two per cent of the Australian mortgage market. Business lending grew by 8%.

Macquarie Securities delivered a net profit contribution of $A18 million for 1H17, down from $A240 million in 1H16. 1H16 benefited from strong trading revenues, particularly in Asia, while trading opportunities in 1H17 were limited due to market uncertainty. Macquarie was ranked No.1 in Australia for IPOs and No.2 for equity, equity-linked and rights deals in calendar year 2016.

Macquarie Capital delivered a net profit contribution of $A205 million for 1H17, up 21 per cent from $A170 million in 1H16. The increase was predominately due to increased income from principal realisations, lower M&A, advisory and underwriting fees and increased operating expenses. During 1H17, Macquarie Capital advised on 201 transactions valued at $A65 billion including being adviser to Brookfield Infrastructure, together with its institutional partners, on the acquisition of Asciano Limited; adviser on behalf of Seoul Tunnel Co., Ltd. in connection with Seoul Jemulpo Tunnel Project; adviser to Siris Capital on its acquisition of Polycom and sole bookrunner and sole lead arranger on the debt financing to support the acquisition; and capital raising and acquisition in conjunction with CFM of a 50 per cent principal investment in the 299MW Tees Renewable Energy Plant.

Commodities and Financial Markets delivered a net profit contribution of $A472 million for 1H17, up 67 per cent from $A282 million in 1H16. The result reflects an increase in income generated from the sale of equity investments and a reduction in provisions for impairment compared to prior periods. This was partially offset by reduced commodities-related net interest and trading income compared to 1H16, which benefited from higher levels of volatility across a number of commodities, particularly oil. CFM continued to experience strong results across the energy platform, particularly from Global Oil and North American Gas, and increased customer activity in foreign exchange, interest rates and futures markets due to ongoing market volatility. Macquarie Energy maintained its Platts ranking of No.3 US physical gas marketer in North America.

Outlook

Macquarie currently expects the year ending 31 March 2017 (FY17) combined net profit contribution from operating groups to be broadly in line with the year ended 31 March 2016 (FY16).

The FY17 tax rate is currently expected to be broadly in line with FY16.

Accordingly, the Group’s result for FY17 is currently expected to be broadly in line with FY16.

The Group’s short-term outlook remains subject to a range of challenges including:

- market conditions

- the impact of foreign exchange; and

- potential regulatory changes and tax uncertainties

Mr Moore said: “Macquarie remains well positioned to deliver superior performance in the medium-term due to its deep expertise in major markets, strength in diversity and ability to adapt its portfolio mix to changing market conditions, the ongoing benefits of continued cost initiatives, a strong and conservative balance sheet and a proven risk management framework and culture.”