Macquarie Group today announced a net profit after tax attributable to ordinary shareholders of $A1,604 million for the full year ended 31 March 2015 (FY15), up 27 per cent on the full year ended 31 March 2014 (FY14) and above expectations. Profit for the second half of the year (2H15) was $A926 million, up 37 per cent on the first half (1H15). The six months to 31 March 2015 saw Macquarie’s annuity-style businesses (Macquarie Asset Management (MAM), Corporate and Asset Finance (CAF) and Banking and Financial Services (BFS)) continue to perform well with combined net profit contribution1 up four per cent on 1H15 and up 29 per cent on 2H14. Macquarie’s capital markets facing businesses (Macquarie Securities Group (MSG), Macquarie Capital and Commodities and Financial Markets (CFM)) also delivered an improved result with combined net profit contribution1 up significantly on 1H15, and up 24 per cent on 2H14. Macquarie’s annuity-style businesses’ FY15 combined net profit contribution1 increased by $A710 million, or 33 per cent, on FY14. Macquarie’s capital markets facing businesses’ FY15 combined net profit contribution1 increased by $A216 million, or 19 per cent, on FY14.

Net operating income of $A9.3 billion for FY15 was up 14 per cent, while total operating expenses of $A6.8 billion were up 12 per cent on the prior year. Key drivers of the change from the prior year were:

- A 17 per cent increase in combined net interest and trading income to $A3.8 billion, up from $A3.3 billion in FY14, resulting from loan portfolio growth for both CAF and BFS and improved trading results in CFM and MSG

- A 24 per cent increase in fee and commission income to $A4.8 billion, up from $A3.9 billion in FY14, primarily driven by higher base and performance fees in MAM, improved levels of advisory fee income in Macquarie Capital and CFM and higher debt capital markets activity

- An 18 per cent decrease in other operating income and charges to $A0.7 billion, from $A0.9 billion in FY14. Increased gains on business and asset sales, predominately in CAF, were offset by higher impairment charges and collective provisions as well as non-recurrence of FY14 items such as the dividend income and gain on disposal of SYD and OzForex

- Total operating expenses increased 12 per cent, driven by: an 11 per cent increase in employment expenses resulting primarily from improved Group performance; increased technology costs due to higher development activity to support business growth as well as increased regulatory compliance; increased other operating expenses largely driven by an overall increase in the Group’s operating activity; and the impact of the depreciation of the Australian dollar on offshore expenses.

Staff numbers were 14,085 at 31 March 2015, up from 13,913 at 31 March 2014.

The income tax expense for FY15 was $A899 million, up nine per cent from $A827 million in the prior year. The effective tax rate of 35.9 per cent was down from 39.5 per cent in FY14 driven by the nature and geographic mix of income and tax uncertainties.

Retail deposits increased by 12 per cent to $A37.3 billion at 31 March 2015, with total deposits increasing during the year from $A36.9 billion to $A39.7 billion at 31 March 2015. During FY15, $A21.5 billion of new term funding was raised covering a range of sources, tenors, currencies and product types.

While Macquarie continued to build on the strength of its Australian franchise, its international income accounted for 70 per cent of the Group’s total income for FY15. This reflects the growth of international operations, particularly in the Americas which was the largest contributing region with 36 per cent of total income, as well as the favourable impact of foreign exchange movements.

The effective tax rate for FY15 was 35.9 per cent, down from 39.5 per cent in FY14.

Macquarie’s assets under management (AUM) at 31 March 2015 were $A486.3 billion, up 14 per cent from $A426.9 billion at 31 March 2014 largely due to additional investments and favourable foreign exchange and market movements.

A final ordinary dividend of $A2.00 per share (40 per cent franked), up from the 1H15 ordinary dividend of $A1.30 per share (40 per cent franked) will be paid. The total ordinary dividend payment for the year was $A3.30 per share, up from $A2.60 in the prior year. This represents an annual ordinary dividend payout ratio of 68 per cent. The record date for the final ordinary dividend is 20 May 2015 and the payment date is 2 July 2015.

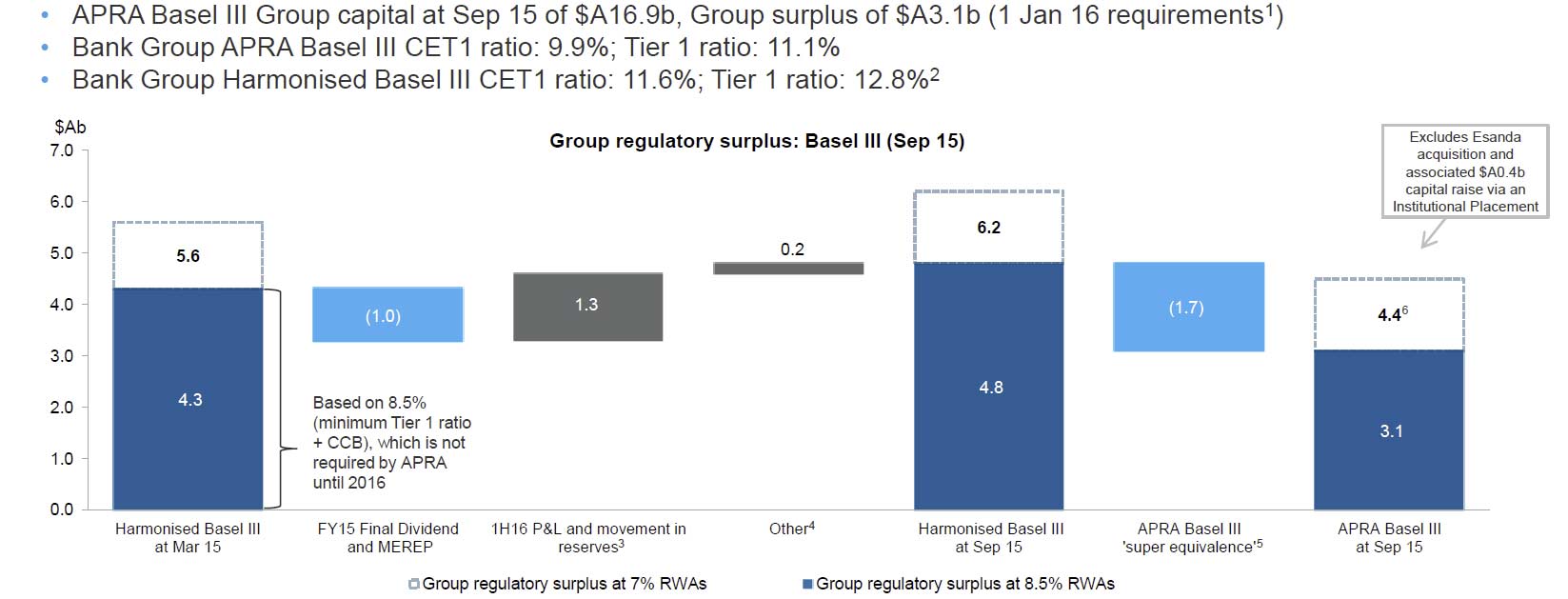

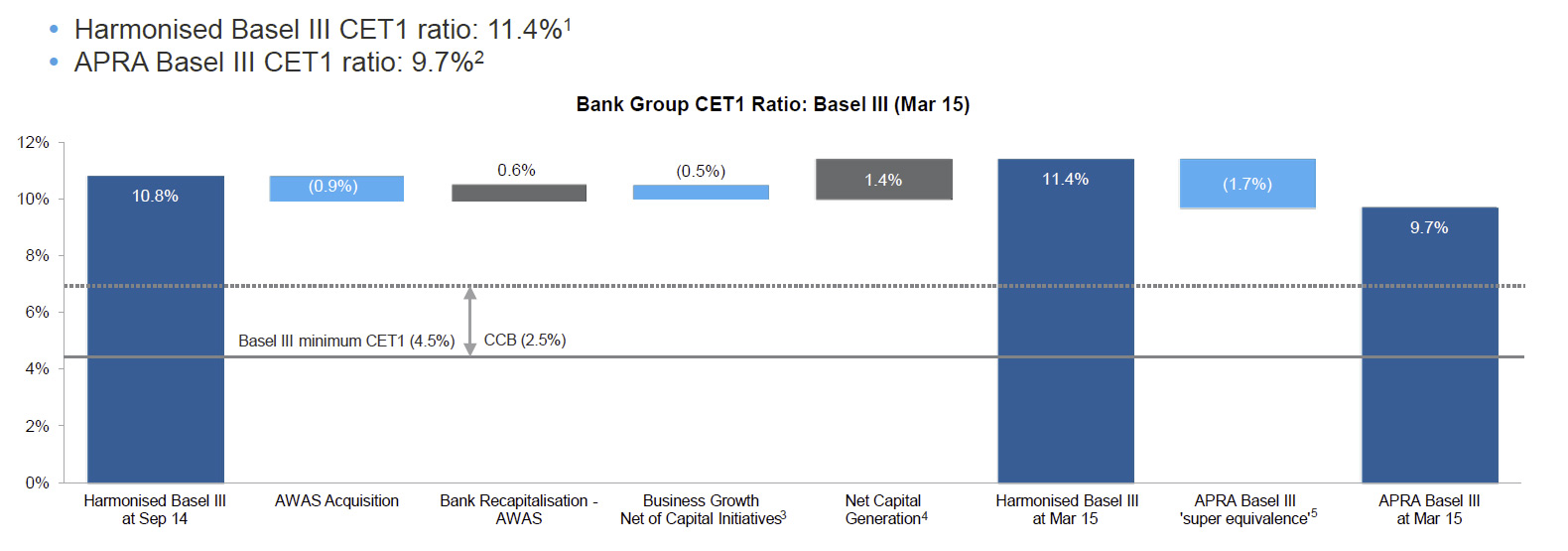

Macquarie Group remains very well capitalised with APRA Basel III Group capital of $A16.1 billion at 31 March 2015, a $A2.7 billion surplus to Macquarie’s minimum regulatory capital requirement from 1 January 20167. The Bank Group APRA Basel III Common Equity Tier 1 capital ratio was 9.7 per cent at 31 March 2015, slightly up on 31 March 2014.

Macquarie intends to purchase approximately $A390 million of shares on-market to satisfy the requirements of the Macquarie Group Employee Retained Equity Plan (MEREP) for FY15. The buying period for the MEREP will commence on 18 May 2015 and is expected to be completed by 10 July 20159. No discount will apply for the 2H15 Dividend Reinvestment Plan (DRP) and the shares required under the DRP are to be acquired on market.

Macquarie intends to purchase approximately $A390 million of shares on-market to satisfy the requirements of the Macquarie Group Employee Retained Equity Plan (MEREP) for FY15. The buying period for the MEREP will commence on 18 May 2015 and is expected to be completed by 10 July 20159. No discount will apply for the 2H15 Dividend Reinvestment Plan (DRP) and the shares required under the DRP are to be acquired on market.

Outlook

While the impact of future market conditions makes forecasting difficult, it is currently expected that the combined net profit contribution1 from operating groups for the year ending 31 March 2016 (FY16) will be broadly in line with FY15. The FY16 tax rate is currently expected to be broadly in line with 2H15, and down on FY15. Accordingly, the FY16 result for the Group is currently expected to be slightly up on FY15. The Group’s short term outlook remains subject to a range of challenges including: market conditions; the impact of foreign exchange; the cost of our continued conservative approach to funding and capital; and potential regulatory changes and tax uncertainties.

Regulatory update

In August 2014, APRA issued its final rules for Conglomerates with the implementation timing dependent on the outcomes of the Financial System Inquiry. Macquarie continues to work through the application of these rules with APRA and the Group’s current assessment remains that Macquarie has sufficient capital to meet the minimum APRA capital requirements for Conglomerates. Based on finalised Bank for International Settlements (BIS) leverage ratio requirements released in January 2014, the Bank Group is well in excess of the currently proposed Basel III three per cent minimum, with an estimated 6.0 per cent leverage ratio as at 31 March 2015. The leverage ratio applies to the Bank Group only. APRA published draft standards relating to the leverage ratio in September 2014 and is currently undertaking industry consultation regarding its final form.

Liquidity Coverage Ratio (LCR) requirements, which also only apply to the Bank Group, came into effect on 1 January 2015. As at 31 March 2015, the Bank Group’s LCR exceeded 120 per cent. Macquarie has been compliant with the LCR at all times since the ratio became a minimum requirement, with the average LCR for the first quarter of 2015 also exceeding 120 per cent. APRA has recently indicated its intention to deal with the level of capital held against mortgages, perhaps narrowing the mortgage risk weight differential between internal ratings-based (IRB) and standardised approach banks. While it remains unclear if, and to what extent, the gap will be narrowed, if the current APRA standardised approach were to be used instead of Macquarie’s IRB mortgage risk weights, the expected impact on the Bank Group’s Common Equity Tier 1 capital would be less than $A250 million.

Operating group performance

Macquarie Asset Management delivered a net profit contribution1 of $A1,450 million, up 38 per cent on the prior year. The result was driven by strong performance fee income and growth in annuity base fee income from higher assets and equity under management. AUM increased 14 per cent on the prior year to $A484.0 billion. Macquarie Infrastructure and Real Assets (MIRA) raised $A8.3 billion in new equity commitments during the year, invested equity of $A6.2 billion in portfolio assets across the globe and divested assets of over $A2.5 billion. Macquarie Investment Management (MIM) continued its strong investment performance, launched several new products across the fixed income, equities and alternatives asset classes, reached capacity in a number of strategies and continued to expand its global distribution network. Macquarie Specialised Investment Solutions continued to grow the Macquarie Infrastructure Debt Investment Solutions (MIDIS) business reaching second close on the UK Inflation-linked Infrastructure Debt Fund to bring total third party investor commitments to the MIDIS platform to over $A3.3 billion.

Corporate and Asset Finance delivered a net profit contribution1 of $A1,112 million, up 35 per cent on the prior year, including gains on several asset sales. CAF’s asset and loan portfolio increased 13 per cent during the year to $A28.7 billion. The corporate and real estate lending portfolio increased by 24 per cent to $A11.2 billion. There were $A4.7 billion of portfolio additions, comprising $A3.1 billion in new primary financings and $A1.6 billion of loans acquired in the secondary market. CAF’s asset finance portfolio of $A17.5 billion was up six per cent on the prior year due to the impact of the depreciation of the Australian dollar. The aircraft leasing business signed an agreement to acquire an operating lease portfolio of 90 aircraft valued at approximately $US4.0 billion, with acquisition and delivery to be completed during FY16. Throughout the year CAF also saw the continued expansion in the motor vehicle and equipment finance channels, as well as growth in the energy asset portfolio of smart meters in the UK and solar energy assets in Australia. CAF continued its securitisation activities, with $A4.0 billion of motor vehicle and equipment leases and loans securitised during FY15.

Banking and Financial Services delivered a net profit contribution1 of $A285 million, up 10 per cent on the prior year. BFS’ Australian mortgage portfolio grew by 44 per cent to $A24.5 billion, including $A2.5 billion in residential mortgage portfolios acquired during the year. This portfolio represents 1.7 per cent of the Australian mortgage market. Macquarie platform assets under administration increased by 19 per cent during the year to $A48.0 billion, while Macquarie Life inforce risk premiums increased by 17 per cent to $A223 million. Average business banking deposits increased 19 per cent over the year, with the business banking loan portfolio at $A5.2 billion as at 31 March 2015, up 27 per cent from $A4.1 billion in the prior year. Total retail deposits were up 12 per cent to $A37.3 billion. During the year BFS continued to invest in its technology to improve client experience, support growth and simplify, streamline and centralise its product and transactional functions.

Macquarie Securities Group delivered a net profit contribution1 of $A64 million, down from $A107 million in the prior year. Brokerage income remained relatively flat whilst equity capital markets activity increased on the prior year largely driven by initial public offering (IPO) activity in Australia. Certain markets experienced favourable conditions, which benefited the derivatives and trading divisions, however operating expenses (excluding brokerage, commission and trading-related expenses) were up 11 per cent on the prior year, resulting largely from investment in platforms and processes driven by regulatory compliance requirements, as well as restructuring costs from the exit of Structured Products. Macquarie was ranked No.1 in Australia for IPOs and No.2 for Australian equity and equity related deals in calendar year 2014. MSG continued to build on its expertise as one of the largest derivative warrant issuers in the Asia-Pacific region, holding No.1 market share for listed warrants in Singapore and Malaysia, No.3 in Thailand and No.7 in Hong Kong.

Macquarie Capital delivered a net profit contribution1 of $A430 million, up 54 per cent on the prior year. The business advised on 470 transactions worth $A141 billion and was ranked No.1 for announced and completed merger and acquisitions (M&A) deals in Australia in calendar year 2014. During the year, Macquarie Capital advised Freeport LNG on its landmark $US11.0 billion equity and debt raising to project finance its LNG export facility in Texas; was Joint Lead Manager on the $A5.7 billion IPO of Medibank Private, the largest Australian IPO in calendar year 2014 and the second largest Australian IPO ever; advised Emperador on its acquisition of Whyte & Mackay from United Spirits for £430 million; and was sole Sponsor and exclusive Financial Adviser to IHS Lothian for the project finance facilities of £185 million to the Royal Hospital for Sick Children public private partnership project in Edinburgh.

Commodities and Financial Markets delivered a net profit contribution1 of $A835 million, up 15 per cent on the prior year. The improved result reflected a general improvement in market conditions compared to the prior year. The Energy Markets business was a significant contributor to CFM’s overall result with revenues generated across the global energy platform, particularly in Global Oil and North American Gas. The Metals, Mining and Agriculture business had an overall improved result on the prior year, primarily driven by continued growth in the base metals platform across financing, physical execution and hedging activities, however further provisions for impairment were taken on underperforming resources investments and loans. Volatility and volumes improved in foreign exchange, interest rates and futures markets in the second half. US credit markets were mixed, however debt capital markets volumes and fees increased as M&A activity increased. The securitisation and origination businesses experienced continued growth and increased transaction flows, particularly in the UK and Europe.