Mortgage Choice released its full-year results, reporting a $2.1-billion hit to its mortgage volumes. Via The Adviser.

Mortgage Choice has published its results for the 2019 financial year (FY19), recording a 40 per cent decline in its cash net profit after tax, from $23.4 million in FY18 to $14 million.

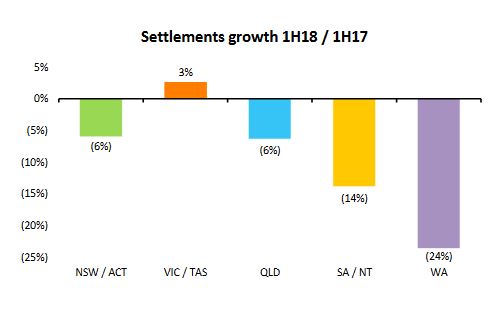

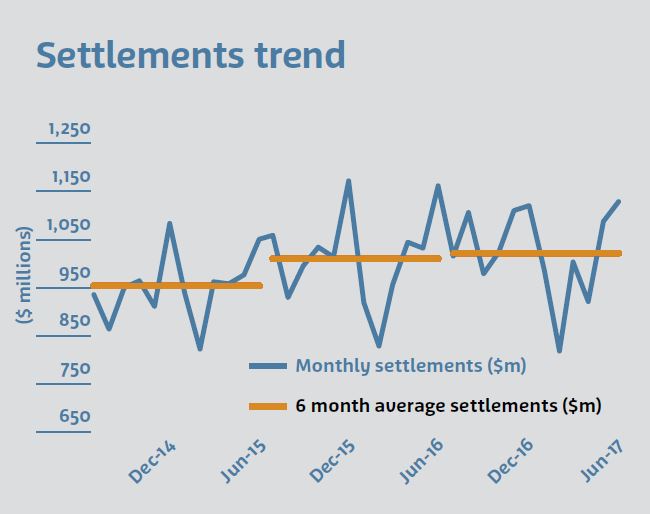

The decline was driven by an 18 per cent ($2.1 billion) fall in its home loan settlement volumes, down from $11.5 billion to $9.4 billion.

The brokerage’s loan book also contracted, slipping by approximately $300 million from $54.6 billion to $54.3 billion.

Mortgage Choice CEO Susan Mitchell attributed the fall in home loan volumes to subdued market activity in response to weaker housing market conditions and increased scrutiny on mortgage applications.

“Settlements for the year were lower than we expected, given a tightening of credit and lending processes for residential mortgages and a continued softening of the housing market in the wake of the [banking] royal commission, especially in the second half,” Ms Mitchell said.

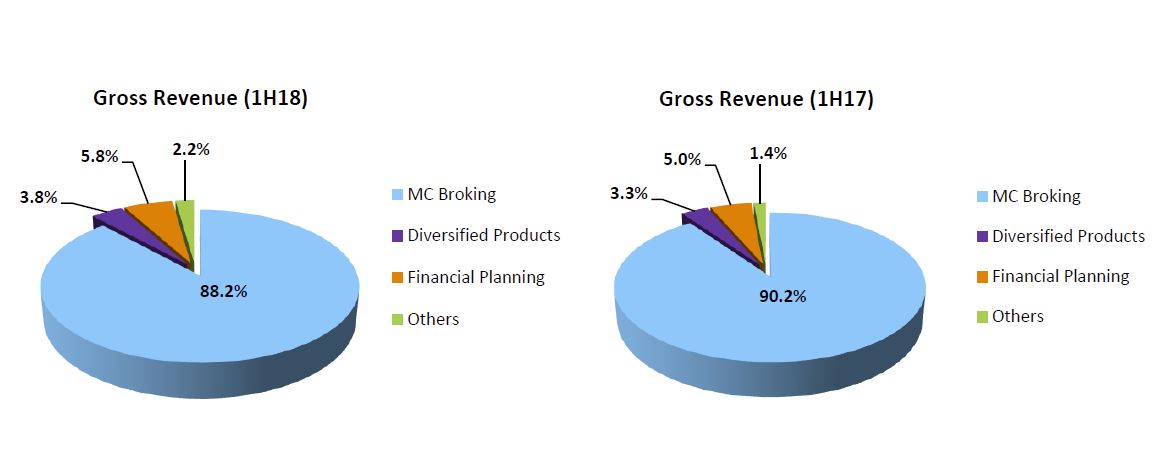

As a result of the fall in mortgage settlements, the total value of commissions received by Mortgage Choice fell by 6 per cent ($11.2 million), from $168.5 million to $157.7 million.

However, the total value of commissions paid by Mortgage Choice to its broker network increased by 6 per cent from $108.8 million to $115.5 million, reflecting changes to the brokerage’s remuneration model, which also weighed on its underlying financial performance.

The total value of Mortgage Choice’s net core commissions fell by 29 per cent, from $59.7 million to $42.2 million.

The withdrawal of its white-label partnership with Macquarie Bank and increased IT expenditure also reduced its pre-tax earnings by approximately $700,000 and $600,000, respectively.

The revenue losses were partly offset by an above-target reduction in operating expenses of 17 per cent ($6 million).

Speaking to the media following the release of the financial results, Ms Mitchell said she expects settlement volumes to increase in the coming financial year, improving the brokerage’s financial position.

Ms Mitchell stated that the brokerage has experienced a rise in mortgage applications in response to the Reserve Bank of Australia’s (RBA) back-to-back cuts to the cash rate and the Australian Prudential Regulation Authority’s (APRA) new lending guidance.

“We have seen our loan applications rise significantly since June 30. I think everyone has seen that,” she said.

“The feedback I’ve gotten from the banks is that they are as busy as they’ve ever been.

“There’s a lot of activity, and I think we still need to see that activity come through into settlement results, which will obviously take another few months.”

Franchise numbers drop

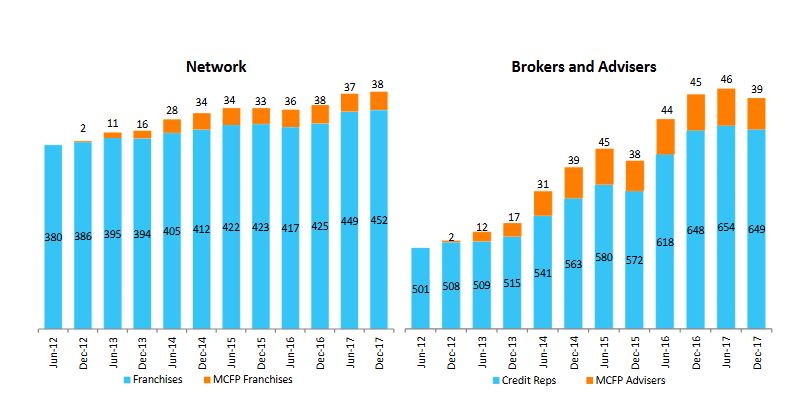

Mortgage Choice has also reported a 13 per cent decline in its franchise network, down from 449 as at the close of FY18 to 381.

The number of brokers operating under the Mortgage Choice brand also slipped, down 9 per cent from 619 to 562 over the same period.

However, the brokerage described the reduction as a “one-off” adjustment that came in response to its new franchise remuneration model, which resulted in 29 franchise mergers and 26 buybacks, with a further 11 franchises listed as “inactive”.

During FY19, Mortgage Choice recruited seven new franchisees but hopes to expand its network over the coming financial year with a renewed focus on recruitment as a means of mitigating risks associated with market volatility.

“We believe that our focus on recruitment will help us weather what’s coming, should there be some uncertainty in settlements going forward,” Ms Mitchell told The Adviser.

The brokerage CEO also told The Adviser that Mortgage Choice’s new franchise remuneration structure – which increased the average commission payout rate from 65 per cent to 74 per cent – would help drive investment from franchisees and lift settlement volumes.

“We believe our remuneration model has put money in the pockets of our franchisees that will allow them to invest in our businesses in the form of broker marketing and administrative functions as well as adding loan writers to their businesses,” she said.

According to Ms Mitchell, the new model has received positive feedback from franchisees, who she said are ready to capitalise on recent market developments, making particular reference to the outcome of the federal election, which signalled the defeat of the Labor opposition’s proposed ban on trailing commissions and property tax reforms.

“Our remuneration model and our IT platform changes were very well received by our network over the past year and our network is ready to get back to work now that we’ve had the result of the federal election back in May,” she said.

‘Devil’s in the detail’

Ms Mitchell was also asked whether she expects the banking royal commission’s proposed best interests duty for brokers to resemble obligations in the financial advice industry.

The Mortgage Choice CEO said she would reserve judgement into a draft bill but expressed support for a “principles-based” duty.

“They haven’t released draft legislation and, of course, for something like this, the devil is always in the detail,” she said.

“I suspect it will be principles-based – the financial planning best interests duty is actually enshrined in law very specifically – and I’m hoping that the broker’s best interests duty will be more principles-based.”

She concluded: “I would expect it to be very much in line [with what] brokers do today but with more documentation and more definition as to why a broker has chosen a particular product and how it meets the requirements of a borrower.”

The best interests duty is due for consultation, with legislation to be introduced before the end of the year ahead of expected implementation in July 2020