APRA has delayed the commencement of new mortgage reporting standards, and watered down some requirements. On the other hand they are seeking to introduced the requirement for lenders to report on debt-to-income ratios for the first time, or at least looking at the cost benefit. Some would say, about time too, but many would not be able to comply, so do not hold your breath! Meantime, APRA says ad hoc requests will continue.

APRA received six submissions to their proposals to revise residential mortgage lending requirements. No submissions objected to the proposals, but some did raise concerns with timelines, data availability and specific definitions.

So APRA has revised the requirements.

Specifically, the start date has been delayed. APRA has deferred the first reporting period for the new reporting requirements to: for ADIs that currently report on ARF 320.8, the period ending 31 March 2018; and for ADIs that do not report on ARF 320.8, the period ending 30 September 2018.

APRA will accept data submitted for the first two reporting periods from these dates on a best endeavours basis. However, APRA expects ADIs will be able to provide accurate, reliable information from the first reporting period. All information provided on ARF 223.0 must be subject to processes and controls developed by the ADI for the internal review and authorisation of that information. These systems, processes and controls are to assure the completeness and reliability of the information provided.

The requirements to classify owner-occupied and investor loans based on security, and to report loans to household trusts has been removed.

Based on feedback, APRA believes the costs of reporting loans to household trusts outweighs the benefits, and has removed the concept.

APRA says it expects that a prudent ADI with material exposures to residential mortgage lending would invest in management information systems that allow for appropriate assessment of residential mortgage lending risk exposures.

They warn that as part of its supervisory monitoring, APRA requests information from ADIs regarding residential mortgage lending on an ad hoc basis. Four submissions to the consultation asked if these requests will continue. ARF 223.0 is designed to replace these data requests, and APRA intends to either significantly reduce or cease the regular requests for individual ADIs once reporting on ARF 223.0 commences. However, given the risks identified in the housing market, ad hoc requests will continue to be a necessary part of APRA’s prudential supervision from time to time.

On the upside (in terms of reporting), in March 2017, APRA noted heightened industry risks relating to residential mortgage lending, and the need to monitor residential mortgage lending more generally. APRA therefore proposes including additional data items to ARF 223.0 regarding:

borrower’s debt-to-income ratios;

additional information on increases in lending; and

lending to private unincorporated business.

These items are highlighted on the updated ARF 223.0. To improve the quality of regulation, the Australian Government requires all proposals to undergo a preliminary assessment to establish whether it is likely that there will be business compliance costs. In order to perform a comprehensive cost-benefit analysis, APRA welcomes information from interested parties.

Among a host of other issues, one the critical things that contributed to the housing crisis of 2008 was the fact that speculative borrowers had nearly no “skin in the game.” Anyone who decided they wanted a piece of the rapidly inflating housing bubble could go out and buy multiple houses with no money down or, in some cases, even do “cash out” purchases whereby banks would finance more than 100% of the purchase price leaving ‘buyers’ to pocket the excess.

Shockingly, such terrible underwriting standards was a really bad idea. Turns out that offering investors infinite returns on capital, given that they could purchase millions of dollar worth of assets without ponying up a single penny, causes wild speculation resulting in devastating asset bubbles.

But, in the wake of one of the worst asset bubbles in history, new legislation came along requiring traditional mortgage borrowers to put 20% down when purchasing a new home.

Ironically, the new owner of one of the worst mortgage lenders of the 2008 era, is now arguing that down payment requirements should be slashed in half. Speaking to CNBC, Bank of America CEO Brian Moynihan, the proud owner of Countrywide Financial, said that his mission is to reduce mortgage down payment requirements to 10% for traditional loans. Per CNBC:

“But, you know, I think at the end of the day is people forget that, at different points in your life and different points on what you’re doing in life requires you to think about housing differently as a place for you and your friends, as a place for you and maybe your significant other, and then ultimately, a place for family. That drives change. And so yes, it’s taken more time. And we talked a lot about this, you know, four or five years ago, that if you require a 20% down payment, it takes just a little more time to accumulate 20% than it would 3% or none, which is what the rules were for a short period of time.”

“So our goal, going back to regulatory reform, is should you move the down payment requirement from 20% to 10%? Wouldn’t introduce that much risk.”

“But would actually help a lot of mortgage to get done. And if you look at the statistics, the difference between 80 and 90 LTV –loan-to-value – isn’t much different as it is between 95 and 90. That’s when you start to see real differences in performance statistics. And so we don’t want to wish people into borrowing money that then they have trouble repaying.”

Of course, we’re certain that Moynihan’s sole purpose for wanting to lower down payments is to help those poor millennials living in mom’s basement and has nothing to do with the fact that’s he’s lost a ton of fee revenue to government-backed loans that only require a 3% down payment.

But, why not? Gradually destroying lending standards worked out really well last time around.

HSBC has announced a return to the Australian mortgage broking space after a 10-year absence, partnering with Aussie Home Loans.

Alice Del Vecchio, Head of Mortgages and Third Party Distribution, HSBC Australia said,“We’re excited to partner with Aussie. Aussie has a strong network of brokers and is a well regarded member of the broking industry.

“Our mortgage book has grown significantly over the past few years and now we’re ready to stretch it beyond the geography of our branch network with mortgage brokers. HSBC has a range of competitive products that we believe will be well-received by customers and brokers,” she added.

Chief Executive of Aussie, Mr James Symond said “Our link with the HSBC brand in Australia brings together two leading brands focused on delivering greater competition to the home loan market, backed by premium customer service.

“Our HSBC partnership will now provide Aussie’s customers with a greater choice of mortgage products, while giving our brokers access to consumers attracted to the strong HSBC offering, the majority of whom are high-net worth”, he added.”

RBA Governor Philip Lowe spoke at the Economic Society of Australia (QLD) Business Lunch. Of note is the data which shows one third of households with a mortgage have little or no interest rate buffer, and that the Reserve Bank does not have a target for the debt-to-income ratio or the ratio of nationwide housing prices to income.

This afternoon I would like to talk about household debt and housing prices.

This is a familiar topic and one that has attracted a lot of attention over recent times. It is understandable why this is so. The cost of housing and how we finance it matters to us all. We all need somewhere to live and for many people, their home is their largest single asset. Real estate is also the major form of collateral for bank lending. The levels of debt and housing prices also affect the resilience of our economy to future shocks. Beyond these economic effects, high levels of debt and housing prices have broader effects on the communities in which we live. The high cost of housing is a real issue for many Australians and can have serious side-effects. High levels of debt and high housing costs can also reinforce the existing distribution of wealth in our society, making social and geographic mobility more difficult. So it is understandable why Australians are so interested in these issues.

At the Reserve Bank, we too have been focused on these issues in the context of our monetary policy and financial stability responsibilities. Our work has been in three broad areas. First, understanding the aggregate trends and their causes. Second, understanding how debt is distributed across the community. And third, understanding how the level of debt and housing prices affect the way the economy operates and its resilience to future shocks.

This afternoon, I would like to make some observations in each of these three areas.

Aggregate Trends

This first chart provides a good summary of the aggregate picture (Graph 1). It shows the ratios of nationwide housing prices and household debt to household income. Housing prices and debt both rose a lot from the mid 1990s to the early 2000s. The ratios then moved sideways for the better part of a decade – in some years they were up and in others they were down. Then, in the past few years, these ratios have been rising again. Both are now at record highs.

Graph 1

Although the debt-to-income ratio has increased over recent times, the ratio of debt to the value of the housing stock has not risen. This reflects the large increase in housing prices and the growth in the number of homes. Over recent times, there has also been a substantial increase in the value of households’ financial assets, with the result that the ratio of household wealth to income is at a record high (Graph 2). So both the value of our assets and the value of our liabilities have increased relative to our incomes.

Graph 2

Turning now to why the ratios of housing prices and debt to income have risen over time. A central factor is that financial liberalisation and the lower nominal interest rates that came with the lower inflation of the 1990s increased people’s ability to borrow. These developments meant that Australians could take out larger and more flexible loans. By and large, we took advantage of this new ability, as we sought to buy the housing we desired.

We could, of course, have used the benefit of lower nominal interest rates in the 1990s and the increased ability to borrow for other purposes. But instead we chose to borrow more for housing and this pushed up the average price of housing given the constraints on the supply side. The supply of well-located housing and land in our cities has been constrained by a combination of zoning issues, geography and inadequate transport. Another related factor was that our population was growing at a reasonable pace. Adding to the picture, Australians consume more land per dwelling than is possible in many other countries, although this is changing, and many of us have chosen to live in a few large coastal cities. Increased ability to borrow, more demand and constrained supply meant higher prices.

So we saw marked increases in the ratios of housing prices and debt to household incomes up until the early 2000s. At the time, there was much discussion as to whether these higher ratios were sustainable. As things turned out, the higher ratios have been sustained for quite a while. This largely reflects the choices we have made as a society regarding where and how we live (and how much at least some of us are prepared to spend to do so), urban planning and transport, and the nature of our financial system. It is these choices that have underpinned the high level of housing prices. So the changes that we have seen in these ratios are largely structural.

Recently, the ratios of housing prices and debt to household income have been increasing again. Lower interest rates both in real and nominal terms – this time, largely reflecting global developments – have again played some role. But there have also been other important factors at work over recent times.

One of these is the slow growth in household income. During the 2000s, aggregate household income increased at an average rate of over 7 per cent (Graph 3). In contrast, over the past four years growth has averaged less than half of this, at about 3 per cent. Slower growth in incomes will push up the debt-to-income ratio unless growth in debt also slows. This partly explains what has happened over recent years.

Graph 3

A second factor is that some of our cities have become major global cities. Reflecting this, in some markets there has been strong demand by overseas investors.

A third factor has been stronger population growth. Population growth picked up during the mining investment boom and, although it subsequently slowed, it is still around ½ percentage point faster than it was before the boom (Graph 4). For some time the rate of home-building did not respond to the faster population growth; indeed, the response took the better part of a decade. The rate of home-building has now responded and we are currently adding to the housing stock at a rate not seen for more than two decades. Over time, this will make a difference.

Graph 4

It is Melbourne and Sydney where population growth has been the fastest over recent times. Not surprisingly, it is these two cities where the price gains have been largest, and these price gains have helped induce more supply. Indeed, Victoria and New South Wales account for all of the recent upward movement in the national housing price-to-income ratio (Graph 5). In the other states, the ratio of housing prices to income is below previous peaks. So there is not a single story across the country. This is despite us having a common monetary policy for the country as a whole. Factors other than the level of interest rates are clearly at work.

Graph 5

In summary then, the supply-demand dynamics have been pushing aggregate housing prices in our largest cities higher relative to our incomes. With interest rates as low as they have been, and prices rising, many people have found it attractive to borrow money to invest in an asset whose price is increasing. The result has been strong growth in borrowing by investors, with investors accounting for 30 to 40 per cent of new loans.

This borrowing is not the underlying cause of the higher housing prices. But the borrowing has added to the upward pressure on prices caused by the underlying supply-demand dynamics. It has acted as a financial amplifier in some cities, adding to the already upward pressure on prices. The borrowing by investors is also obviously contributing to the rise in the aggregate debt-to-income ratio. Just like in the early 2000s, there is again a discussion as to whether these increases will continue and whether they are sustainable.

The Distribution of Debt

I would now like to turn to the distribution of housing debt across households. This is important, as it is not the ‘average’ household that gets into trouble. At the Reserve Bank we have devoted considerable resources to understanding this distribution. One important source of household-level information is the survey of Household Income and Labour Dynamics in Australia (HILDA).

If we look across the income distribution, it is clear that the rise in the debt-to-income ratio has been most pronounced for higher-income households (Graph 6). This is different from what occurred in the United States in the run-up to the subprime crisis, when many lower-income households borrowed a lot of money.

Graph 6

It is also possible to look at how the debt-to-income ratio has changed across the age distribution. This ratio has risen for households of all ages, except the very youngest, who tend to have low levels of debt (Graph 7). Borrowers of all ages have taken out larger mortgages relative to their incomes and they are taking longer to pay them off. Older households are also more likely than before to have an investment property with a mortgage and it has become more common to have a mortgage at the time of retirement.

Graph 7

We also look at the share of households with a debt-to-income ratio above specific thresholds. In 2002, around 12 per cent of households had debt that was over three times their income (Graph 8). By 2014, this figure had increased to 20 per cent of households. There has also been an increase, although not as pronounced, in the share of households with even higher debt-to-income ratios.

Graph 8

Another dataset that provides insight into distributional issues is one maintained by the Reserve Bank on loans that have been securitised. This indicates that around two-thirds of housing borrowers are at least one month ahead of their scheduled repayments and half of borrowers are six months or more ahead (Graph 9). This is good news. But a substantial number of borrowers have only small buffers if things go wrong.

Graph 9

At the overall level, though, nationwide indicators of household financial stress remain contained. This is not surprising with many borrowers materially ahead on their mortgage repayments, interest rates being low and the unemployment rate being broadly steady over recent years. At the same time, though, the household-level data show that there has been a fairly broad-based increase in indebtedness across the population and the number of highly indebted households has increased.

Impact on Economy and Policy Considerations

I would now like to turn to the third element of our work: the implications of all this for the way the economy operates and its resilience.

It is now commonplace to say that housing prices and debt levels matter because of financial stability. What people typically have in mind is that a severe correction in property prices when balance sheets are highly leveraged could make for instability in the banking system, damaging the economy. So the traditional financial stability concern is that the banks get in trouble and this causes trouble for the overall economy.

This is not what lies behind the Reserve Bank’s recent focus on household debt and housing prices in Australia. The Australian banks are resilient and they are soundly capitalised. A significant correction in the property market would, no doubt, affect their profitability. But the stress tests that have been done under APRA’s eye confirm that the banks are resilient to large movements in the price of residential property.

Instead, the issue we have focused on is the possibility of future sharp cuts in household spending because of stretched balance sheets. Given the high levels of debt and housing prices, relative to incomes, it is likely that some households respond to a future shock to income or housing prices by deciding that they have borrowed too much. This could prompt a sharp contraction in their spending, as they try to get their balance sheets back into better shape. An otherwise manageable downturn could be turned into something more serious. So the financial stability question is: to what extent does the higher level of household debt make us less resilient to future shocks?

Answering this question with precision is difficult. History does not provide a particularly good guide, given that housing prices and debt relative to income are at levels that we have not seen before, and the distribution of debt across the population is changing.

Given this, one of the research priorities at the Reserve Bank has been to use individual household data to understand better how the level of indebtedness affects household spending. The results indicate that the higher is indebtedness, the greater is the sensitivity of spending to shocks to income. This is regardless of whether we measure indebtedness by the debt-to-income ratio or the share of income spent on servicing the debt. If this result were to translate to the aggregate level, it would mean that higher levels of debt increase the sensitivity of future consumer spending to certain shocks.

The higher debt levels also appear to have affected how higher housing prices influence household spending. For some years, households used the increasing equity in their homes to finance extra spending. Today, the reaction seems different. This is evident in the estimates of housing equity injection (Graph 10). In earlier periods of rising housing prices, the household sector was withdrawing equity from their housing to finance spending. Today, households are much less inclined to do this. Many of us feel that we have enough debt and don’t want to increase consumption using borrowed money. Many also worry about the impact of higher housing prices on the future cost of housing for their children. As I have spoken about previously, higher housing prices are a two-edged sword. They deliver capital gains for the current owners, but increase the cost of future housing services, including for our children.

Graph 10

This change in attitude is also affecting how spending responds to lower interest rates. With less appetite to incur more debt for current consumption, this part of the monetary transmission mechanism looks to be weaker than it once was. There is, however, likely to be an asymmetry here. When the interest rate cycle turns and rates begin to rise, the higher debt levels are likely to make spending more responsive to interest rates than was the case in the past. This is something that we will need to take into account.

In terms of resilience, my overall assessment is that the recent increase in household debt relative to our incomes has made the economy less resilient to future shocks. Given this assessment, the Reserve Bank has strongly supported the prudential measures undertaken by APRA. Double-digit growth in debt owed by investors at a time of weak income growth cannot be strengthening the resilience of our economy. Nor can a high concentration of interest-only loans.

I want to point out that APRA’s measures are not targeted at high housing prices. The international evidence is that these types of measures cannot sustainably address pressures on housing prices originating from the underlying supply-demand balance. But they can provide some breathing space while the underlying issues are addressed. In doing so, they can help lessen the financial amplification of the cycle that I spoke about before. Reducing this amplification while a better balance is established between supply and demand in the housing market can help with the resilience of our economy.

There are some reasons to expect that a better balance between supply and demand will be established over time.

One is the increased rate of home-building. As we are seeing here in Brisbane and some parts of Melbourne, increased supply does affect prices. This increase in supply is also affecting rents, which are increasing very slowly in most markets.

A second reason is the increased investment in some cities, including in Sydney, on transport. Over time, this will increase the supply of well-located residential land, and this will help as well.

And a third reason is that at some point, interest rates in Australia will increase. To be clear, this is not a signal about the near-term outlook for interest rates in Australia but rather a reminder that over time we could expect interest rates to rise, not least because of global developments. Over recent years, the low interest rates in Australia have helped the economy adjust to the winding down of the mining investment boom. They have helped support employment and demand through a significant adjustment in the Australian economy. We should not, though, expect interest rates always to be this low.

It remains to be seen how the various influences on housing prices play out. Other policies, including tax and zoning policies, also have an effect. But increased supply and better transport could be expected to help address the ongoing rises in housing prices relative to incomes. These changes and some normalisation of interest rates over time might also reduce the incentive to borrow to invest in an asset whose price is rising strongly. To the extent that, over time, a better balance is established, we will be better off not incurring too much debt, and having housing prices go too high, while this is occurring.

I want to make it clear that the Reserve Bank does not have a target for the debt-to-income ratio or the ratio of nationwide housing prices to income.

As I spoke about earlier, there are good reasons why these ratios move over time. My judgement, though, is that, in the current environment, the resilience of our economy would be enhanced by an extended period in which housing prices and debt outstanding increased no faster than our incomes. Again, this is not a target or a policy objective of the Reserve Bank, but rather a general observation about how we build resilience.

Many of you will be aware that these issues have figured in the deliberations of the Reserve Bank Board for some time. This is entirely consistent with our flexible medium-term inflation targeting framework. With a medium-term target, it is appropriate that we pay attention to the resilience of our economy to future shocks. In the current environment of low income growth, faster growth in household debt is unlikely to help that resilience.

We have also been watching the labour market closely. The unemployment rate has moved up a little over recent months and wage growth remains subdued. Encouragingly, employment growth has been a bit stronger of late and the forward-looking indicators suggest ongoing growth in employment. We will want to see a continuation of these trends if the overall growth in the economy is to pick up as we expect. Stronger growth in incomes would of course also help people deal with the high levels of debt and housing prices. Overall, our latest forecast is for economic growth to pick up gradually and average around 3 per cent or so over the next few years.

To conclude, I hope these remarks help provide some insight into the Reserve Bank’s thinking about housing prices and household debt. As household balance sheets have changed, so too has the way that the economy works. Both from an individual and an economy-wide perspective, we need to pay attention to how the higher level of debt affects our resilience to future shocks.

Suncorp has announced an exclusive new offer for first home buyers to “help them realise their property ownership dreams”.

Suncorp’s Home Package Plus Special Offer for First Home Buyers allows customers to choose from a Standard Variable rate or a 5 Year Fixed rate of 3.99% p.a. on new lending of $150,000 or more.

The initial Home Package Plus annual fee will be waived and most customers will also be eligible for savings on their Lenders Mortgage Insurance (LMI) , as well as building and contents insurance.

Suncorp EGM Stores and Specialty Banking, Lynne Sutherland, said buying a home is one of the biggest financial commitments customers make and it’s becoming increasingly difficult for those looking to enter the market for the first time.

“Housing affordability is creating a barrier for young people wanting to purchase their first home,” Sutherland said.

“The average age of home owners across the country has increased by 10 years, and while we know property ownership isn’t for everyone, it’s still a goal for many Australians.

“Our Home Package Plus Special Offer for First Home Buyers gives customers choice by providing the same low rate on a Standard Variable or 5 Year Fixed loan, while also offering a range of discounts on some of the additional fees and products that go with home ownership.

“Where the customer is borrowing more than 80% of the property’s value, we will contribute $1,000 towards their mortgage insurance premium.

“Eligible customers will also be offered 20% off the first year’s premium for Suncorp issued building and contents insurance, as well as savings on Suncorp Home Loan Protect for new policies issued.

“This offer is especially timely for first home buyers in Queensland, with the Government’s First Home Owner’s $20,000 grant only available until 30 June 2017.

“Entering the property market can be daunting, but these savings could be the difference for many of our customers in realising home ownership.”

More data and end-to-end systems are pushing us ever closer to the paperless mortgage and point-of-sale approvals but predicting the future of technology is a risky business.

From the millennium bug to Google Glass, we’ve seen plenty of ‘game changers’ which were no such thing. Rather than take an impossibly broad view of the future, we asked our industry leaders to explain what brokers should expect over the next few years, starting with the paperless mortgage.

Glenn Lees, CEO of Connective, says the entirely paperless mortgage is “closer than ever … I think what’s driving it now is lenders understand what a competitive advantage it can be”. The barriers are simply “institutional inertia”, he says, with lenders’ risk and compliance teams “understandably nervous” about changing the application process.

NextGen.Net sales director Tony Carn is less optimistic; he believes the paperless mortgage will take some time to come about due to the current focus on credit risk. However, he says the technology is there, and mortgages are already becoming increasingly electronic thanks to e-conveyancing platform PEXA and increasing use of electronic verification by lenders.

At AFG, CIO Jaime Vogel believes that “we will end up with a significant number of applications being digital end-to-end”. The process will be similar to the gradual take-up of ApplyOnline. “As lenders understand the benefits of that innovation it’ll progressively change and we’ll find the vast majority will be digital end-to-end,” Vogel says. “We feel the technology would be relatively easily implemented in the broker process.”

Verifying with video at HashChing

Identifying borrowers, under the Know Your Customer (KYC) guidelines, has long been a time-consuming part of the application process. It was a particular problem for online marketplace HashChing, CEO Mandeep Sodhi recalls. “The broker was seeing ‘the consumer is in Cairns, but I’ve got this great deal and I’m in Sydney’.” For brokers there was an additional problem: having to visit a bank or Australia Post outlet to get identified was causing many customers to walk away from a deal.

HashChing’s virtual online identification (VOI) technology uses a video call to compare the borrower to a photo on their Australian passport or driver’s licence, giving the broker a percentage of how much they match. It also does a behind-the-scenes DBS check and tells the broker the borrower’s current location, and the video is stored for seven years in case of an enquiry from ASIC. The system is currently being trialled by 150 brokers, saving them eight hours on average, with a full rollout scheduled for 1 March.

There’s no legal barrier to video identification; the challenge is persuading lenders to accept it. While HashChing has an exclusive partnership with the South African developer of the software, E4, it is encouraging lenders to work with E4 to use VOI technology. Combined with online document collection, VOI can free brokers from the tyranny of distance, Sodhi believes. “With this technology the broker can be anywhere in Australia and the consumer can be anywhere in Australia … the geographic barrier is gone.”

Using data

In March 2016 Siobhan Hayden, then-CEO of the MFAA, predicted the next evolution in mortgage broking would be driven by data scraping. Data scraping is extracting data from documents, web pages and storage vaults, which can then be put to use in a number of ways: automatically filling in forms, reducing the need to ask borrowers for documentation, and more informed decisions by lenders.

Data is already changing the mortgage application process. Electronic mortgages through Bank Australia and conditional approvals via the CommBank Property app are available to customers of these banks, as the banks already have the relevant data. Data scraping across institutions is in its early stages, warns AFG’s Vogel. “There’s certainly not enough data available to make a complete and proper assessment, but we’re trying to make the best of the data which is available to use.”

Other professions are further ahead in data scraping. Next.Gen.Net’s Carn points out that accountants can already access information on their clients held by the ATO; giving brokers the same access would be a “very simple technology solution, but there [needs to be] a risk appetite to allow that to happen”.

At Rubik Group a current project is looking at using wealth management to provide solutions for property investors. “One of the top unmet needs is around investment property,” head of product Emily Chen says. “It’s almost personal financial management: how do I budget? How do I know when I’m ready to buy that next property?”

Already some banks offer digital ‘dashboards’ that show customers the funds available in their current, savings and super accounts. Chen suggests that property could be added to this mix, bringing in external data on property values on fixed loan terms, creating “a total wealth view for the customer”.

What’s holding back data scraping – and by consequence paperless mortgages – is concerns around security. Computer hacking has become international news, and 71% of Australians are concerned about having their information stolen, according to Veda’s 2016 Cybercrime and Fraud Report, with older Australians more concerned.

“A lot of brokers are not aware of how much is invested in secure data processing,” argues Carn. However, he warns that vulnerabilities remain: “We’re operating in a market that’s heavily regulated, and everyone’s aware of data security, yet we still see a lot of emailing of personal customer information, which I think is quite horrifying.”

Vogel believes younger borrowers are more accepting of their data being used. “If there is value for the customer and the opportunity to get a reduced interest rate then I’d certainly expect that a high percentage of customers would be willing to provide that information.” That is conditional, however, on those customers trusting that brokers can keep their data secure, which is why AFG is investing heavily in data security.

Australian house price growth will slow to 7 per cent in 2017 before it collapses to between zero and 3 per cent in 2018, predicts UBS.

In a new housing outlook report, UBS said it is “calling the top” for Australian residential housing activity despite a surprise rebound in February approvals to 228,000.

While the “historical trigger” for a housing downturn is missing (namely, RBA interest rate hikes), mortgage rates are rising and home buyer sentiment is at a near record low, said UBS.

“Hence, we are ‘calling the top’, but stick to our forecasts for commencements to ‘correct but not collapse’ to 200,000 in 2017 and 180,000 in 2018,” said the report.

House prices are rising four times faster than incomes, noted UBS, which is unsustainable and suggests that growth has peaked.

“We see a moderation to [approximately] 7 per cent in 2017 and 0-3 per cent in 2018, amid record supply and poor affordability, with the new buyer mortgage repayment share of income spiking to a decade high,” said UBS.

The report also pointed to the March 2017 Rider Levett Bucknall residential crane count, which has more than tripled since 2013 to a record 548, but is now flat year-on-year.

Housing affordability has gone from “bad to even worse”, said UBS, with the house price to income ratio soaring to a record 6.5.

“With record low rates, repayments haven’t yet reached historical tipping points where prices fell, but would if mortgage rates rose by only [approximately] 100 basis points,” said the report.

The gross rental yield for two-bedroom unit has fallen to a record-low of less than 4 per cent, said UBS, which is now below mortgage rates of 4.25-4.50 per cent.

UBS also pointed to Australia’s household debt to GDP ratio of 123 per cent, which is one of the highest in the world.

Although dwelling valuations in Australia are 5-15% above historical averages, the risk of a catastrophic collapse in the housing market is low, argues Merlon Capital Partners, a Sydney-based boutique fund manager.

In its latest paper, entitled Some Thoughts on Australian House Prices, Merlon acknowledged that the nation is currently at a cyclical high point, with “house prices, housing finance activity and building approvals … all at historically elevated levels.” At the same time, interest rates are at record lows and have begun to hike, particularly for investors.

“We think the housing market is 5-15% overvalued relative to ‘mid-cycle’ levels. Contrary to recent commentary, we do not find this over-valuation to be concentrated in the Sydney market,” said Hamish Carlisle, analyst at Merlon Capital Partners.

Carlisle doesn’t find the modest system-wide overvaluation to be particularly surprising at the current point in the economic cycle, and notes that the nation is a long way off from what are considered to be “mid-cycle” interest rates. “Rising interest rates – as we are currently experiencing – are likely to be a precursor to a turn in the cycle so it is likely we will enter into a phase of more subdued house price inflation.”

Favourable tax treatment of housing, coupled with historically low interest rates and favourable fundamentals (i.e. income and rental growth), mean that it’s highly unlikely that house prices will retrace to “mid-cycle” levels in the foreseeable future.

Carlisle further asserts that regulator concerns about house prices are “overblown”. Growing regulatory restrictions, which force banks to ration lending, particularly to property investors, are probably unnecessary and will achieve little other than improving the short-term profitability of banks via higher interest rates for borrowers.

“As with all our investing, we work on the basis that, over time, interest rates will revert back to long term levels as will aggregate housing valuation metrics. Against this, we think aggregate rents and household incomes will continue to grow which will cushion the overall impact on dwelling prices and that the exposure of the household sector to higher interest rates means that the time frame over which interest rates will rise could be quite protracted. As such, we think the risk of a catastrophic collapse in the housing market is low,” he said.

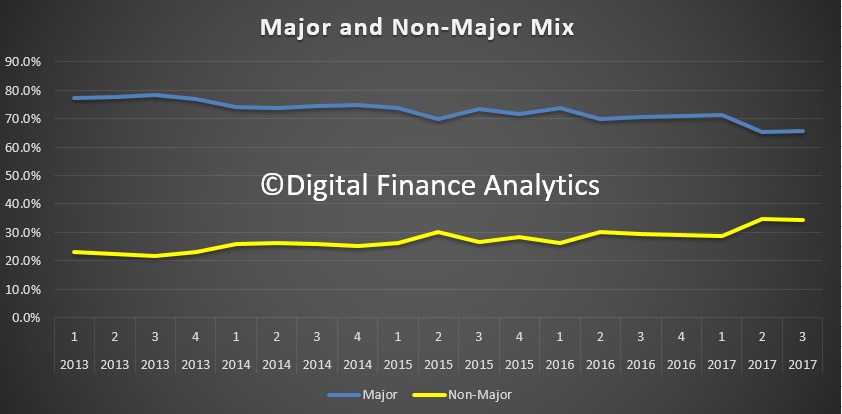

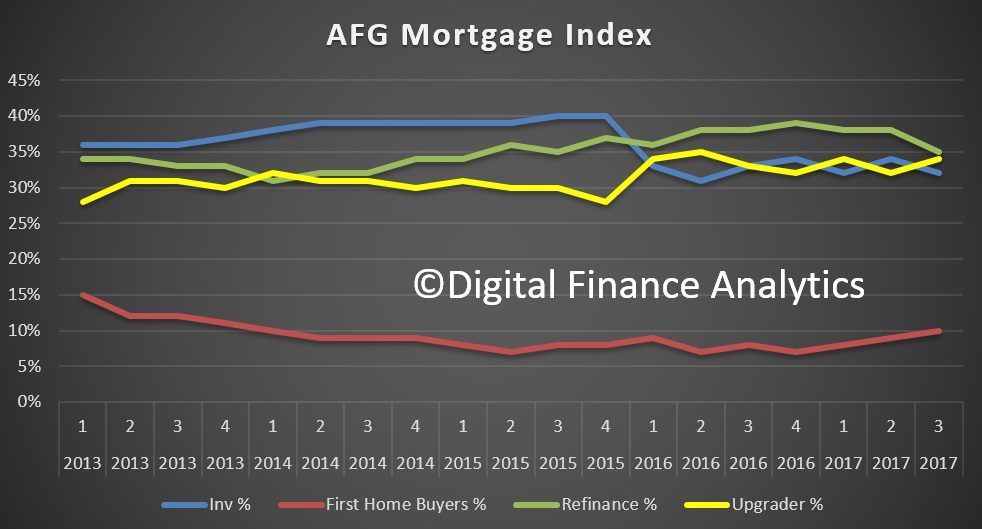

AFG has released their mortgage index today including Q3 2017. The overall volume of lodgements fell again, though volumes are still higher than last year at this time.

This data provides additional insights into the market, with the caveat, it reflects transactions via the AFG channel only.

The mix between majors and non-majors remained similar to last quarter, when the non-majors share grew a little.

The volumes of first time buyers rose a little, whilst refinanced transactions fell a little.

The national First Home Owner Grant (FHOG) scheme funded by the states and territories has largely been hailed a success as it seeks to ease the hefty upfront costs for new entrants to the market. The effectiveness of the scheme however has been questioned of late and it appears this may have encouraged governments to act. “The Victorian state government has recently announced a number of changes to the scheme in that state and New South Wales is currently examining their options to help counter rising house prices in those states,” said AFG Interim CEO David Bailey.

AFG data shows positive signs amongst the FHB market with lodgments lifting back up to 10% for the first time since the first quarter of 2014.

“First home buyer numbers have been in the single digits for some time. It is good to see state governments looking to support those trying to get a foot on the property ladder. Time will tell if the proposed changes to the scheme go far enough to assist those looking to buy their first home in our two most populous states.”

APRA-imposed lender policy changes have had an impact on both the investor market and refinancers as many lenders lift interest rates for borrowers.

“Lenders have been told by the regulator to rein in their exposure to the investor market and APRA continues to monitor growth in lending to investors,” said Mr Bailey. “As a result many lenders have embarked upon a series of rate increases and a tightening of credit policy for investors to comply with APRA’s guidelines.

“This activity has seen investor loans drop from 34% to 32% across the quarter.”

Those looking to refinance have also been impacted, with that segment of the market dropping from 38% to 35% last quarter – its lowest level since the third quarter of 2015.

In overall lodgment numbers, AFG has reported a lift of 8% on Quarter 3 last year driven primarily by increasing activity of upgraders. “With a significant amount of changes being made to the appetites and pricing of lenders, help from a mortgage broker can be vital for consumers trying to navigate the dynamic market that is home lending,” said Mr Bailey.

“A result that should please the regulators is a drop in the loan to value ratio (LVR) in all states apart from South Australia where a marginal increase of 0.4% was evident. The national LVR is now down to 68.6%, the lowest level since the first quarter of 2013,” he concluded.

Evidence has emerged suggesting alternative lenders are offering commercial loans to non-residents for the purchase of residential property.

Loan documents obtained by Australian Broker through an anonymous source show commercial finance firm Prime Capital approving ‘working capital’ for the purchase of an inner city apartment in Brisbane.

The 12-month business loan for $315,000 was approved on 23 March for a property estimated to be worth $575,000. Despite this being a commercial loan, the borrower’s Australian Company Number (ACN) was only registered a day later.

Conditions for the loan include a “lower” interest rate of 10.95% per annum with a “higher” rate of 2% per month applying in the event of default.

Additional fees include a 2.2% establishment fee, a monthly loan management fee of 0.2%, a default fee of $635 per hour for time spent dealing with the default, and a 2.2% termination fee.

Avoiding the squeeze

This is an example of how alternative financiers may bypass tighter regulations on foreign lending as well as the guidelines in the National Consumer Credit Protection (NCCP) Act, the source said.

“Since last year, there has been a lot of tightening up on non-resident lending so basically these non-resident investors can’t borrow anymore. A lot of private lenders have come out and now basically ask buyers to change the purchase contract into a business.”

This involves creating an ACN or Australian Business Number (ABN) with the lender then providing ‘working capital’ to that business.

“This actually makes sense in a commercial deal because it’s working capital for you to purchase property. However, this is literally playing around with words. In the end, you’re still purchasing a residential unit for investment purposes.”

Risk at all costs

The excessive fees offered in the leaked loan contract were one concern, our source said, especially since they could be further increased in the event of default.

One condition of default in Prime Capital’s approved loan is using funds for a purpose other than working capital. However, whether this condition is met by purchasing residential property is a grey area, the source said.

“It depends on the angle that you take. From the company’s perspective, they are buying a property which can be deemed as working capital but from a transactional perspective, it’s borrowing to buy a residential unit.”

This means there is a risk that the borrowers in these schemes could eventually have their properties seized, he said.

“Obviously, the company has the right to take the property away from the borrower but they may not because they’ll lose business in the future. It may or may not be the case that they want to take the property – it’s a matter of what makes more money.”

Client confirmation

Prime Capital told Australian Broker of the challenges in the early application stages to confirm all details provided.

“We can confirm approvals are conditional, including being subject to items like valuation and any required clarification around use of funds/commercial purpose. It is a condition of our funding lines that our lawyers (Dentons and Kemp Strang) review all files before settlement to ensure compliance with our lending guidelines and all regulatory requirements,” they said in an emailed statement.

Regulated or unregulated?

If an unregulated commercial loan is written which should have fallen within the regulated residential mortgage space, there can be quite hefty fines as well as sanctions by the Australian Securities & Investments Commission (ASIC), Elise Ivory, partner at law firm Dentons, told Australian Broker.

“If they have an ACL and they’ve treated a loan as unregulated when they shouldn’t have, that could have implications for their licence.”

There are also implications for the borrower if it is determined they had defrauded the lender, Ivory said.

Determining whether a borrower is guilty of fraud is a difficult question that depends on a range of factors including who structured the loan, whether the lender or broker made recommendations or whether the borrower was acting alone.

Proper usage of funds

To ensure that funds are used for the purpose originally stated, lenders should note exactly where the loan proceeds are going on settlement, she said.

“Look at the cheques that are being drawn, look at the transfers that are being made – actually look at how the funds are being dispersed. That’s probably the best way to see what’s going on.”

A red flag for working capital being used to purchase residential property would be a cheque for the entire loan amount going to a third party the lender has never heard of, Ivory said.

“They would need to check why that party is being paid, who they are, what they have to do with the transaction. We normally recommend that any funds dispersed in excess of $10,000 must be investigated in terms of why that cheque is being paid to whomever it’s being paid to.”

“Lenders certainly can’t close their eyes to what the loan is actually being used for and pretend that just because they were told it was working capital for a company that this is exactly what is being done with it.”

Beware the newborn firm

Another big red flag is that if the company has only just been established prior to the loan, Ivory said, adding that further questions should be asked at this point.

“Why has the company just been set up? Has it been trading before? What is it going to be doing? If it was set up last week and suddenly it needs a large amount of money, the lender should understand what that money’s being used for.”