Join us for a live discussion as I explore the latest from our surveys and models. Where are prices trending, and how are financial stress footprints trending.

You can ask a question live. The post code database will be online.

Go to the Walk The World Universe at https://walktheworld.com.au/

I talk financial stress with Steve from Canstar, as their survey reveals the size of the problem. And we discuss both the cause and potential mitigation strategies.

Steve Mickenbecker is in Canstar’s Group Executive Team, bringing more than 30 years of experience in the Australian financial services industry. As a financial commentator for Canstar, Steve enjoys sharing his expertise across topics such as home loans, superannuation, insurance, mortgages, banking, credit cards, investment, budgeting, money management and more. https://www.canstar.com.au/team-members/steve-mickenbecker/

Go to the Walk The World Universe at https://walktheworld.com.au/

We discuss the latest mortgage stress data to end February 2022. It is not pretty – and this was before the latest ructions in Europe!

Go to the Walk The World Universe at https://walktheworld.com.au/

Today’s post is brought to you by Ribbon Property Consultants.

If you are buying your home in Sydney’s contentious market, you do not need to stand alone. This is the time you need to have Edwin from Ribbon Property Consultants standing along side you.

Buying property, is both challenging and adversarial. The vendor has a professional on their side.

Emotions run high – price discovery and price transparency are hard to find – then there is the wasted time and financial investment you make.

Edwin understands your needs. So why not engage a licensed professional to stand alongside you. With RPC you know you have: experience, knowledge, and master negotiators, looking after your best interest.

Shoot Ribbon an email on info@ribbonproperty.com.au & use promo code: DFA-WTW/MARTIN to receive your 10% DISCOUNT OFFER.

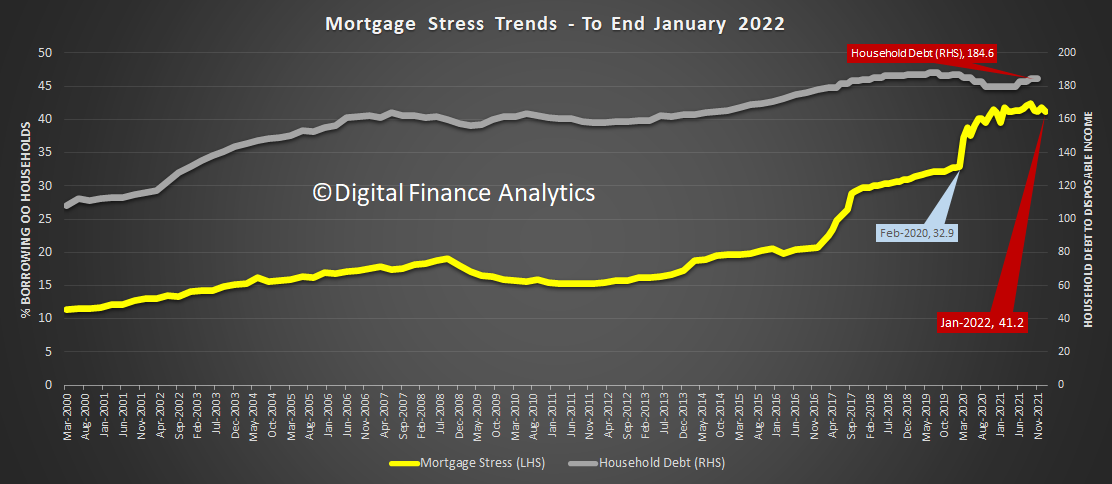

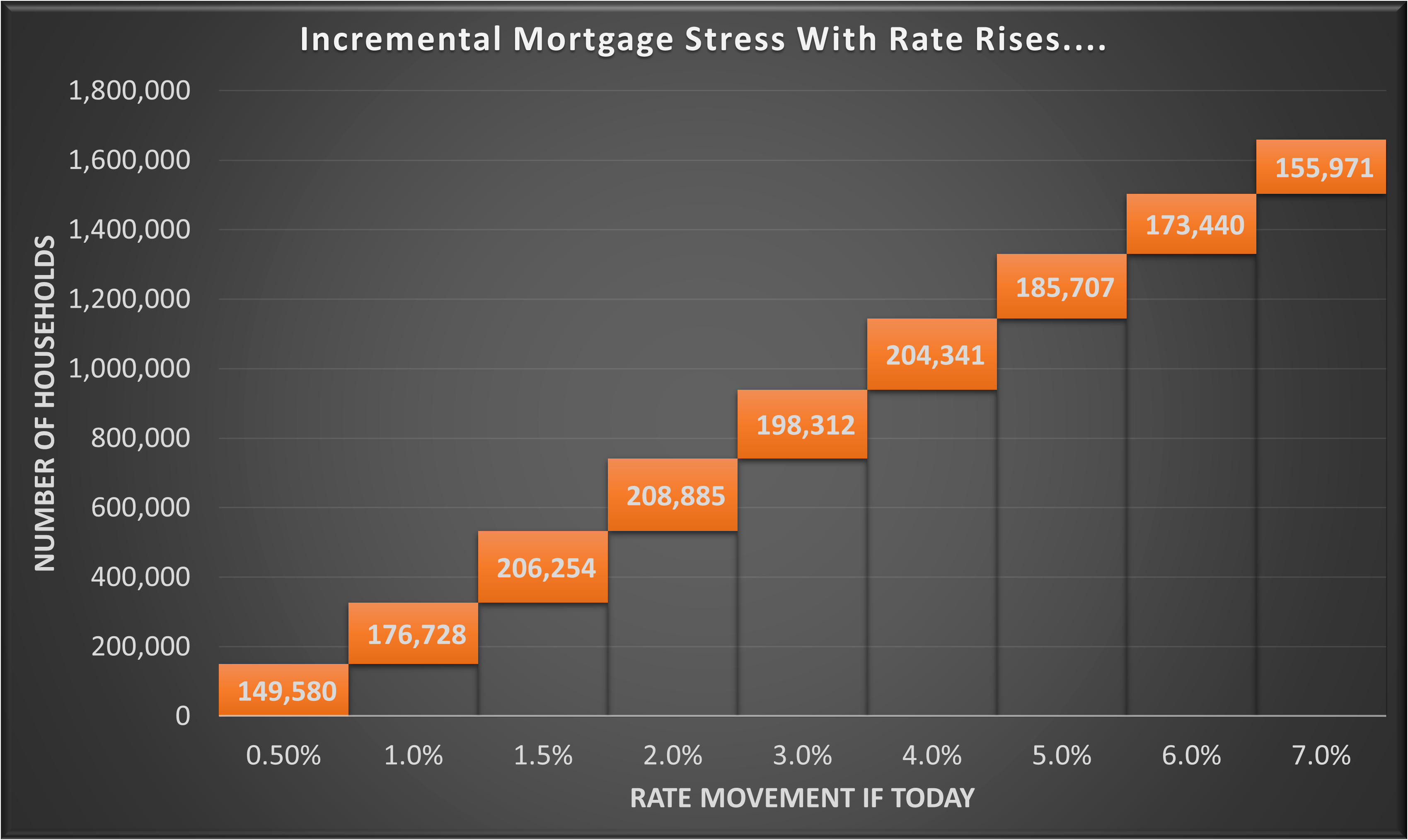

A deep dive of our mortgage stress analysis to end of January 2022, plus some rate sensitivity analysis and mapping. Where are the hot spots? How many households are under pressure?

Rate Sensitivity

Go to the Walk The World Universe at https://walktheworld.com.au/

This is material drawn from several recent shows on this and other channels, explaining mortgage and household stress and what is happening in the current environment – with data to December 2021 and beyond.

Go to the Walk The World Universe at https://walktheworld.com.au/

This is a succinct summary of our latest mortgage stress analysis, based on our surveys. We also add some additional comments about how to address stress at a household level.

Go to the Walk The World Universe at https://walktheworld.com.au/ The original live stream is here:

This is an edited version of our latest live Q&A as I discuss the latest from our surveys and models, as we look at the latest mortgage stress and scenarios. You can ask a question live – down to a specific post code.

Original live show here: https://youtu.be/CCIym9IPamk with chat replay.

Go to the Walk The World Universe at https://walktheworld.com.au/

Digital Finance Analytics (DFA) Blog

DFA Live Q&A: HD Replay Household Stress And Scenarios [Podcast]

We discuss the September 2021 DFA Household survey results. Many households remain in a difficult position, as cash-flows remain negative thanks to crushed incomes, rising costs and bigger mortgages (despite the lower available interest rates). We examine data at a state, segment and post code level, as well as geo-mapping which highlights the patchwork nature of the problem. Stress lurks in strange places, including some more “affluent” places!

Go to the Walk The World Universe at https://walktheworld.com.au/

Blog")