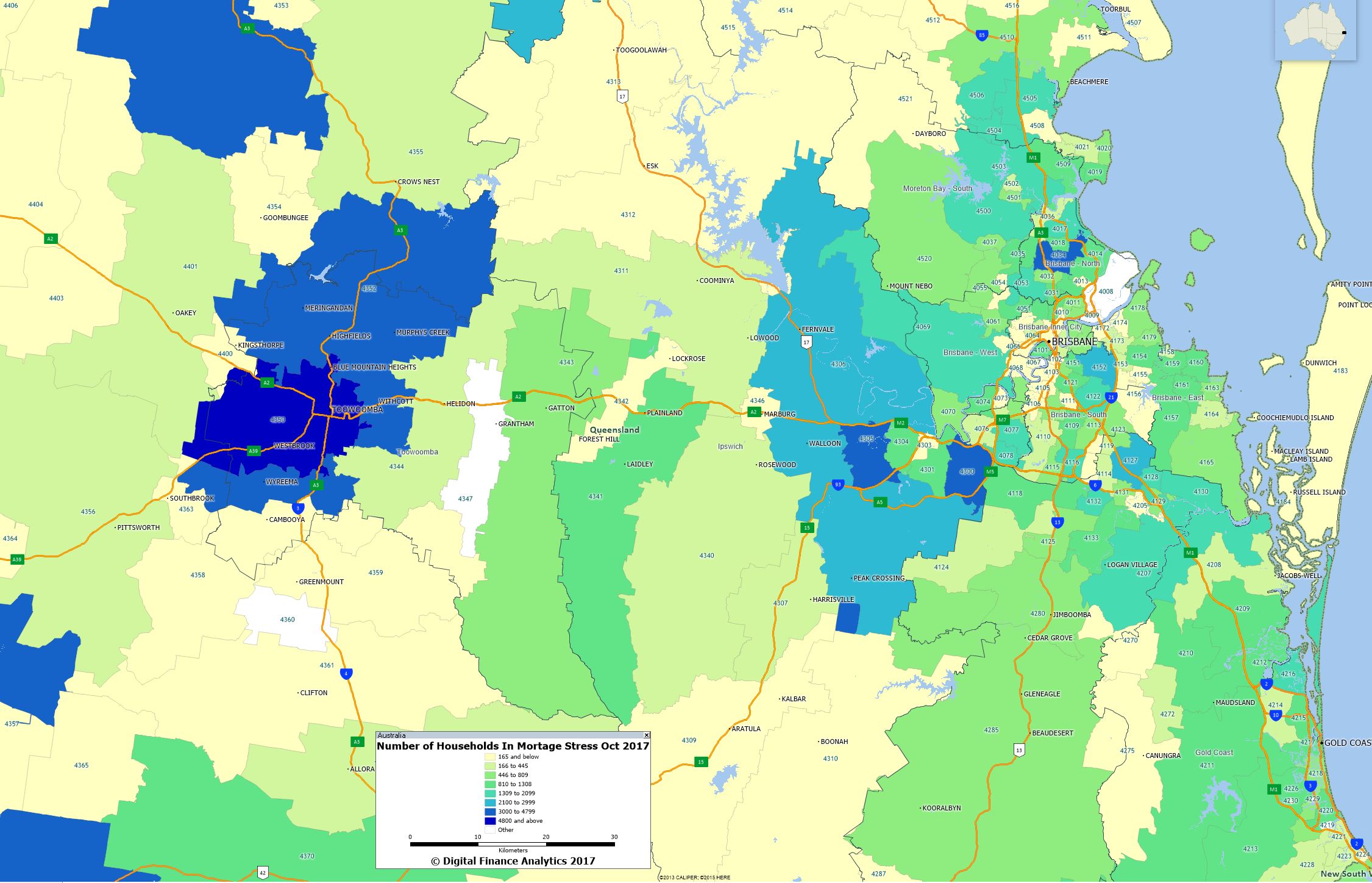

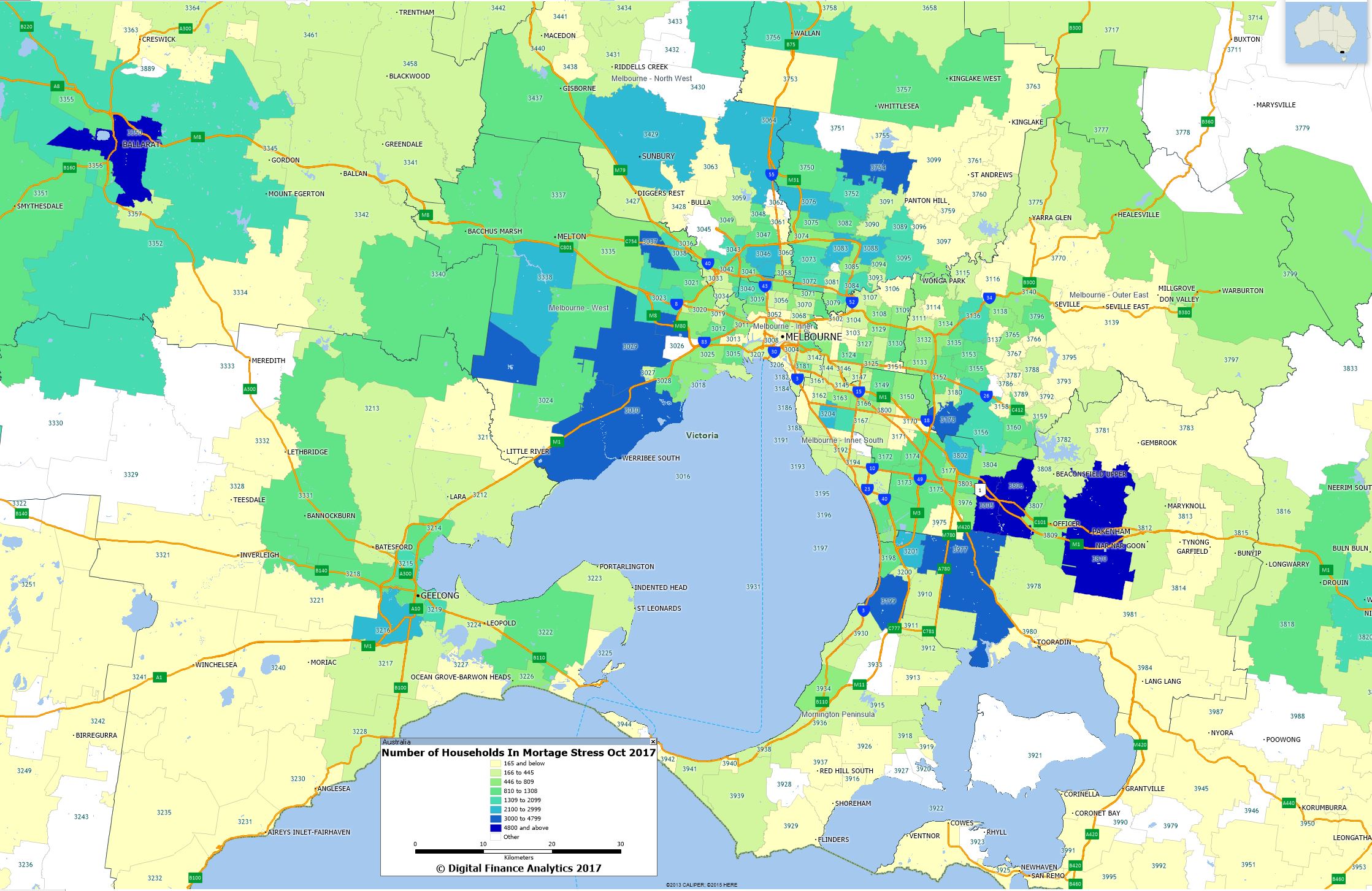

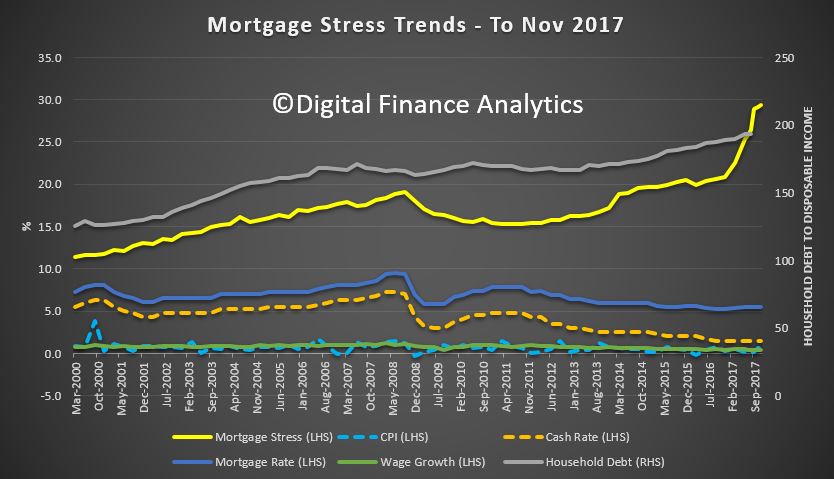

Digital Finance Analytics has released the November mortgage stress and default analysis update. Across Australia, more than 913,000 households are estimated to be now in mortgage stress (last month 910,000) and more than 21,000 of these in severe stress, the same as last month. Stress is sitting on a high plateau. This equates to 29.4% of households. We see continued default pressure building in Western Australia, as well as among more affluent household, beyond the traditional mortgage belts across the country. Stress eased a little in Queensland, thanks to better employment prospects.

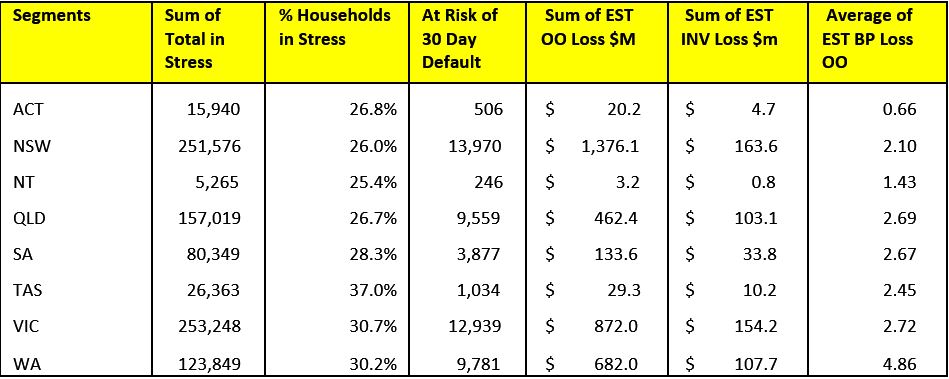

We estimate that more than 52,000 households risk 30-day default in the next 12 months, similar to last month. We expect bank portfolio losses to be around 2.8 basis points, though with losses in WA rising to 4.9 basis points.

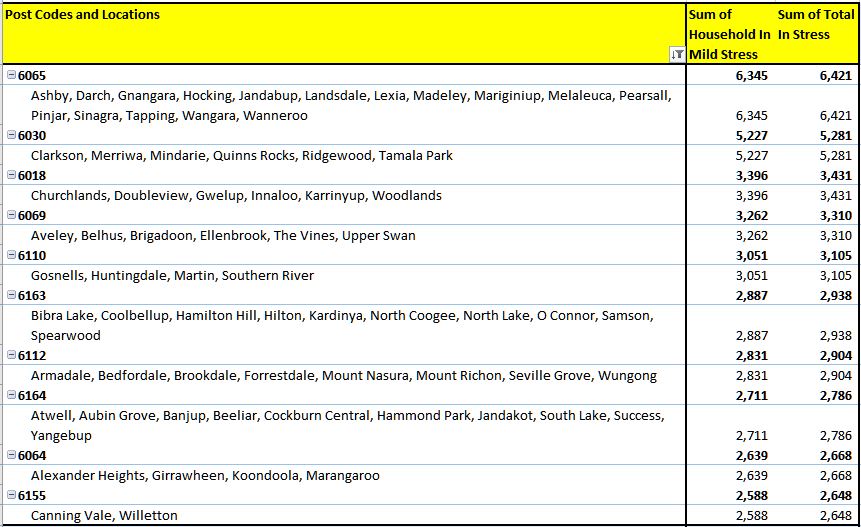

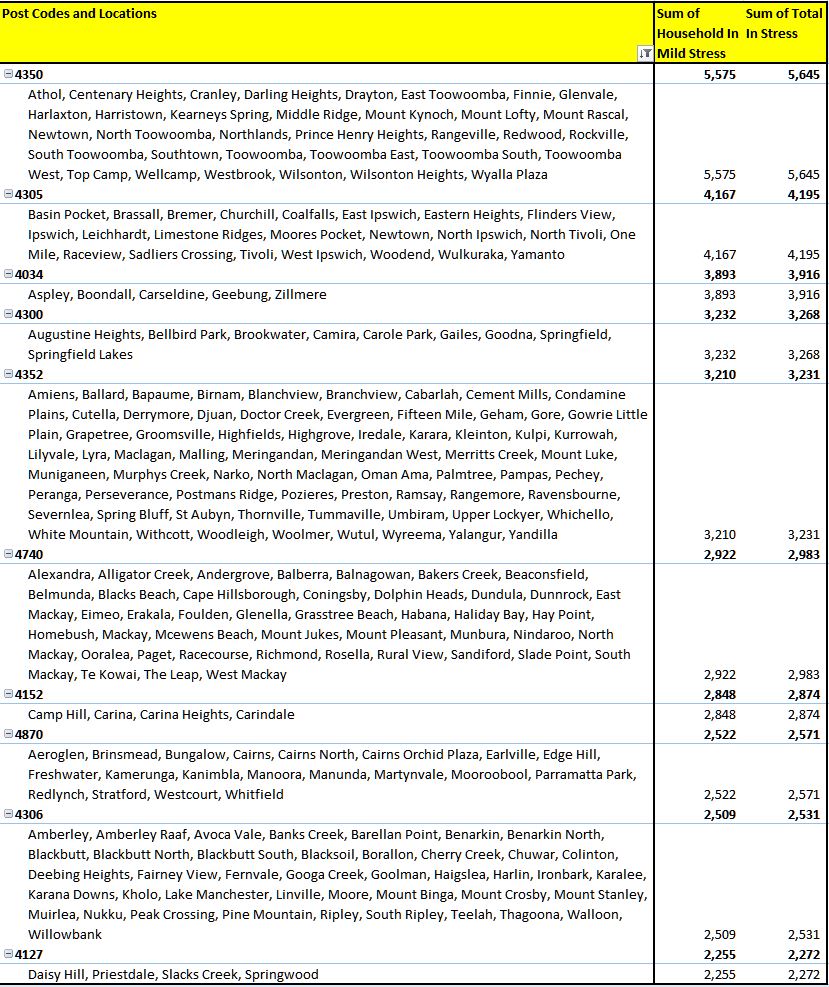

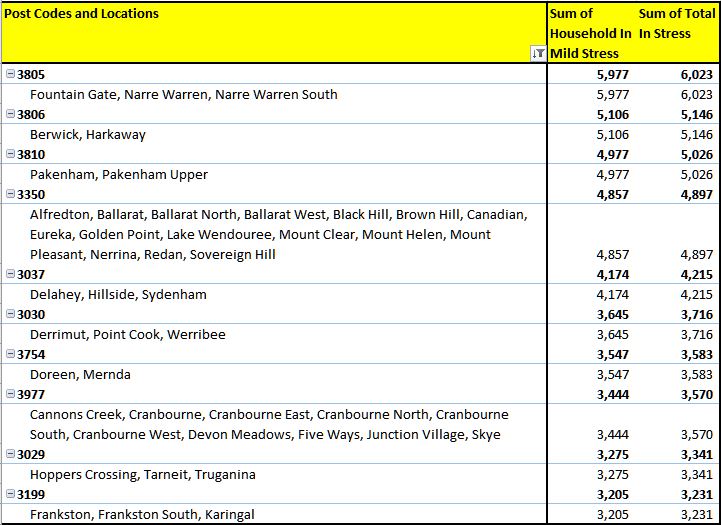

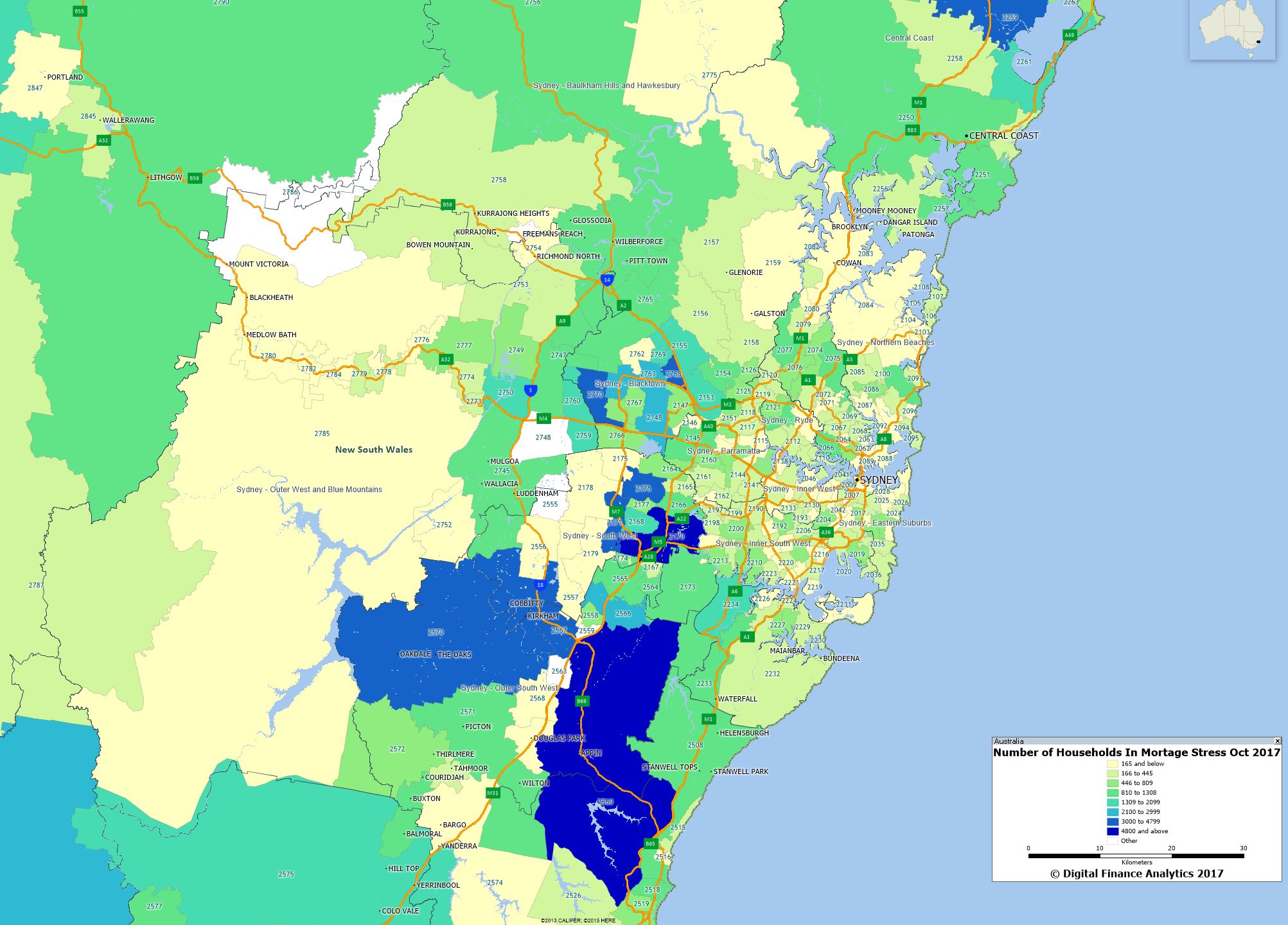

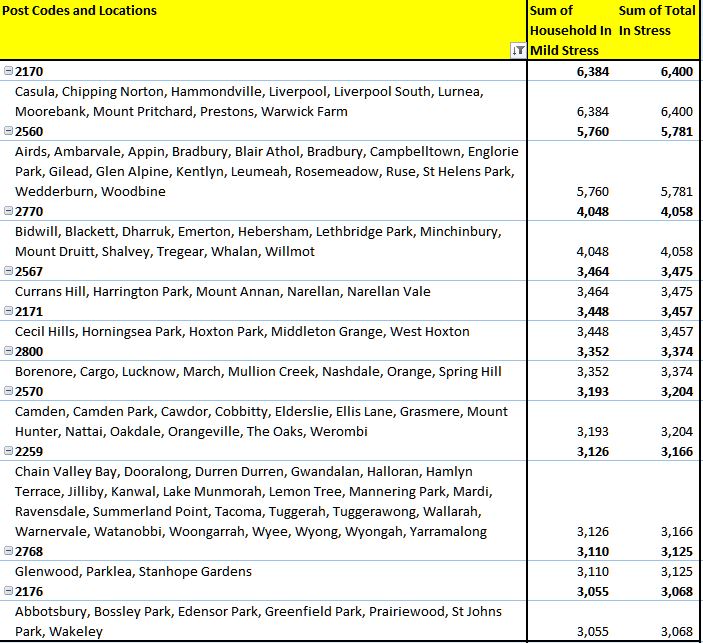

We discuss the findings from our analysis and count down the top 10 post codes, to identify the most highly stressed post code currently in the country.

We discuss the findings from our analysis and count down the top 10 post codes, to identify the most highly stressed post code currently in the country.

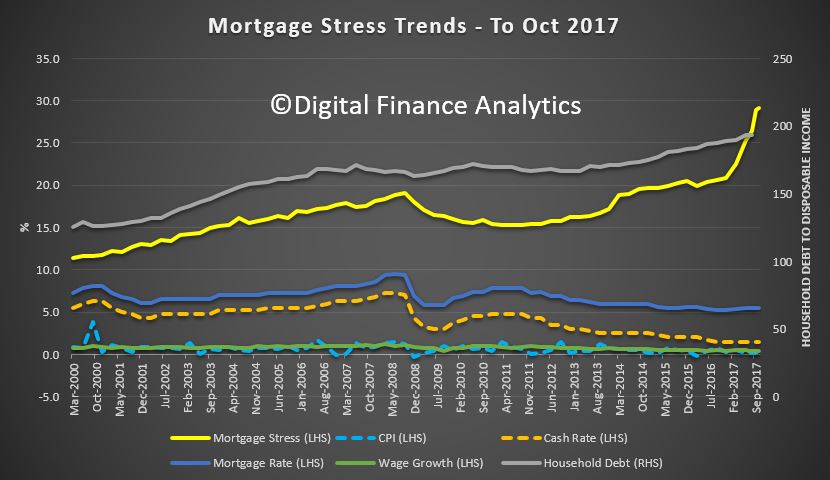

As continued pressure from low wage growth and rising costs bites, those with larger mortgages are having more difficulty balancing the family budget. As a result, risks in the system continue to rise, and while recent strengthening of lending standards will help protect new borrowers, there are many households currently holding loans which would not now be approved. These stressed households are less likely to spend at the shops, which will act as a further drag anchor on future growth, one reason why retail spending is muted. The number of households impacted are economically significant, especially as household debt continues to climb to new record levels. Mortgage lending is still growing at three times income. This is not sustainable. The latest household debt to income ratio is now at a record 193.7.[1]

Our analysis uses the DFA core market model which combines information from our 52,000 household surveys, public data from the RBA, ABS and APRA; and private data from lenders and aggregators. The data is current to end November 2017. We analyse household cash flow based on real incomes, outgoings and mortgage repayments, rather than using an arbitrary 30% of income.

Households are defined as “stressed” when net income (or cash flow) does not cover ongoing costs. Households in mild stress have little leeway in their cash flows, whereas those in severe stress are unable to meet repayments from current income. In both cases, households manage this deficit by cutting back on spending, putting more on credit cards and seeking to refinance, restructure or sell their home. Those in severe stress are more likely to be seeking hardship assistance and are often forced to sell.

The forces which are lifting mortgage stress levels remain largely the same. In cash flow terms, we see households having to cope with rising living costs whilst real incomes continue to fall and underemployment remains high. Households have larger mortgages, thanks to the strong rise in home prices, especially in the main eastern state centres. While mortgage rates remain quite low for owner occupied borrowers, those with interest only loans or investment loans have seen significant rises. We expect some upward pressure on real mortgage rates in the next year as international funding pressures mount, a potential for local rate rises and margin pressure on the banks. We revised our expectation of potential interest rate rises, given the stronger data on the global economy and the recently announced Finance Sector Royal Commission.

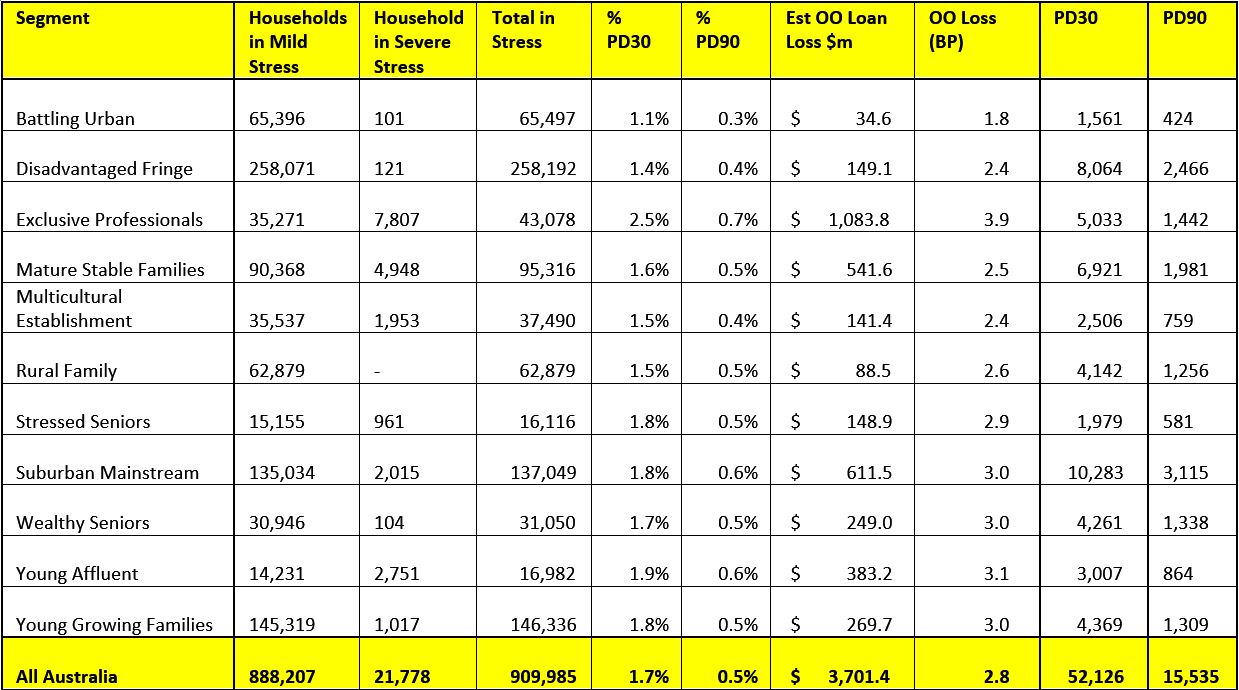

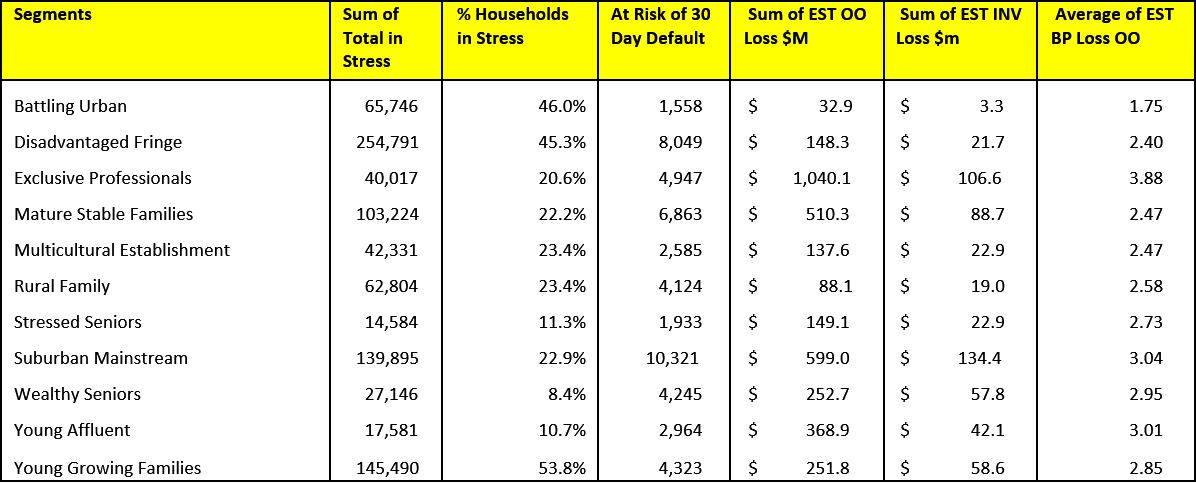

Probability of default extends our mortgage stress analysis by overlaying economic indicators such as employment, future wage growth and cpi changes. We have also extended our Core Market Model to examine the potential of portfolio risk of loss in basis point and value terms. Losses are likely to be higher among more affluent households.

Gill North, Joint DFA Principal and Professorial Research Fellow in the law school at Deakin University, said “the numbers of households in mortgage and financial stress in Australia are at record levels and the consequential risks and likely adverse impacts are difficult to overstate. When external events and or the personal circumstances of these highly indebted households deteriorate, the number of people who cannot afford to rent or purchase a home is likely to increase exponentially, leaving many more households without adequate accommodation. In extreme instances, other households may lose the residential property they presently live in due to rental defaults or a forced sale or foreclosure.”

Gill North, Joint DFA Principal and Professorial Research Fellow in the law school at Deakin University, said “the numbers of households in mortgage and financial stress in Australia are at record levels and the consequential risks and likely adverse impacts are difficult to overstate. When external events and or the personal circumstances of these highly indebted households deteriorate, the number of people who cannot afford to rent or purchase a home is likely to increase exponentially, leaving many more households without adequate accommodation. In extreme instances, other households may lose the residential property they presently live in due to rental defaults or a forced sale or foreclosure.”

While there have been numerous inquiries into housing affordability and homelessness in Australia, the issues involved are complex, and real progress has been limited (at best). For policy options to make any meaningful difference to the nature and scale of housing affordability and homelessness, policy makers and others need to acknowledge the sheer magnitude of the problem, and respond accordingly.

One of the options that policy makers have considered to address affordable housing issues and to provide housing for the most vulnerable sections of the community is the use of social impact investment. Gill North was part of a team that reviewed the potential for impact investment models to provide housing for the vulnerable and reported to the Australian Housing and Urban Research Institute (AHURI). The report on “Supporting Vulnerable Households To Achieve Their Housing Goals: The Role Of Impact Investment” is available from https://ssrn.com/author=905894. The report authors acknowledge and thank AHURI for the funding that allowed this important research”.

By the Numbers

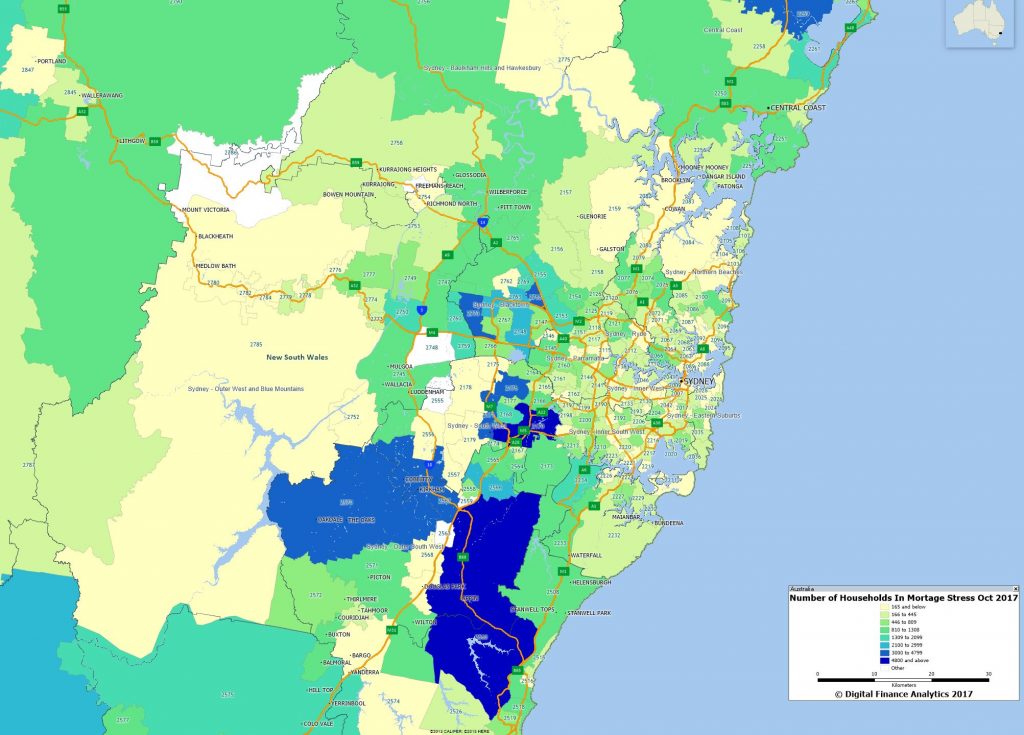

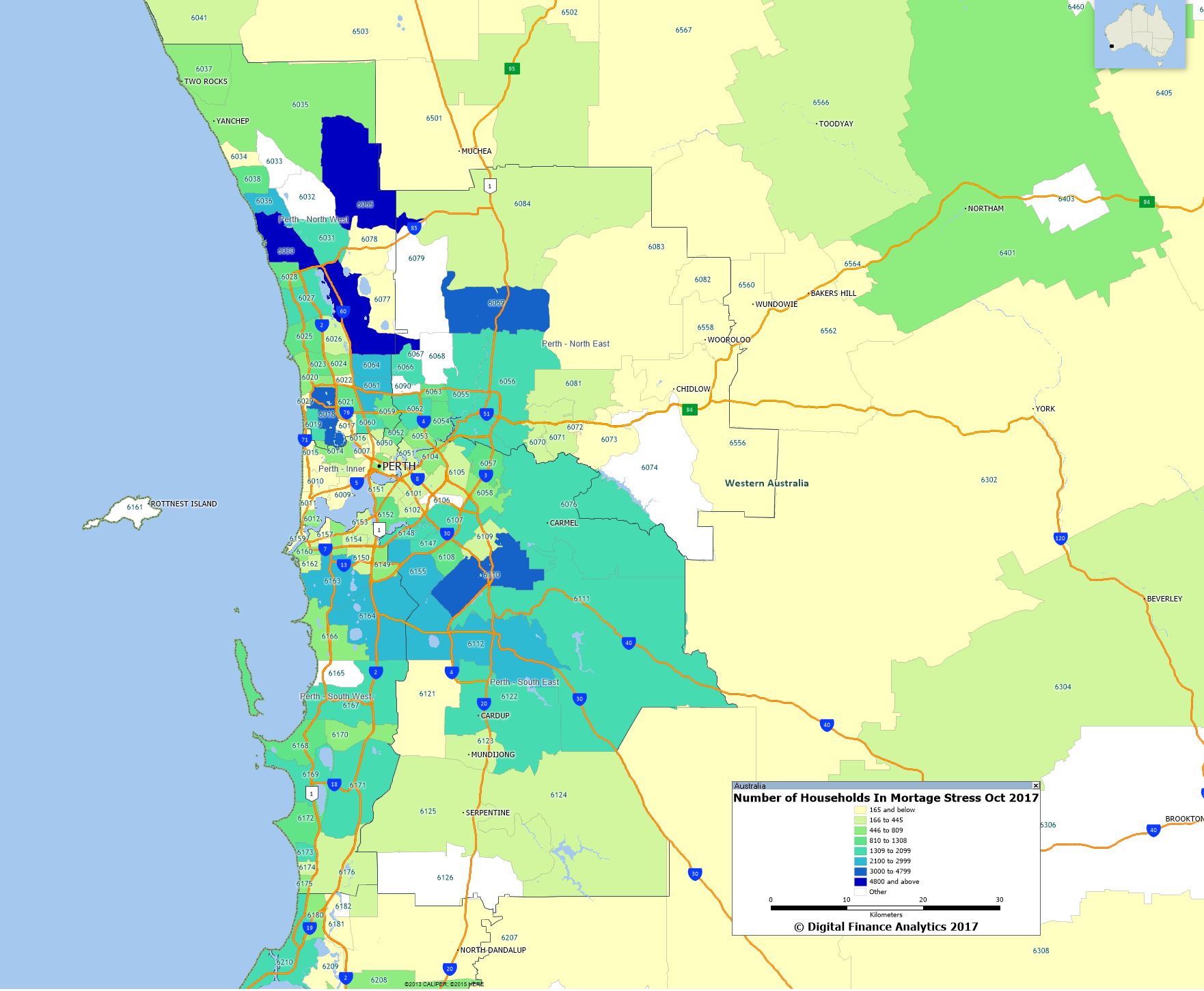

Regional analysis shows that NSW has 251,576 households in stress (242,399 last month), VIC 253,248 (250,259 last month), QLD 157,019 (162,726 last month) and WA 123,849 (121,393 last month). The probability of default rose, with around 9,800 in WA, around 9,600 in QLD, 13,000 in VIC and 13,900 in NSW.

The largest financial losses relating to bank write-offs reside in NSW ($1.3 billion from Owner Occupied borrowers) and VIC ($870 million from Owner Occupied Borrowers, which equates to 2.1 and 2.7 basis points respectively. Losses are likely to be highest in WA at 4.9 basis points, which equates to $682 million from Owner Occupied borrowers and $108 million from Property Investors over the next 12 months.

The largest financial losses relating to bank write-offs reside in NSW ($1.3 billion from Owner Occupied borrowers) and VIC ($870 million from Owner Occupied Borrowers, which equates to 2.1 and 2.7 basis points respectively. Losses are likely to be highest in WA at 4.9 basis points, which equates to $682 million from Owner Occupied borrowers and $108 million from Property Investors over the next 12 months.

You can request our media release. Note this will NOT automatically send you our research updates, for that register here.

[contact-form to=’mnorth@digitalfinanceanalytics.com’ subject=’Request The Nov 2017 Stress Release’][contact-field label=’Name’ type=’name’ required=’1’/][contact-field label=’Email’ type=’email’ required=’1’/][contact-field label=’Email Me The Nov 2017 Media Release’ type=’radio’ required=’1′ options=’Yes Please’/][contact-field label=”Comment If You Like” type=”textarea”/][/contact-form]

Note that the detailed results from our surveys and analysis are made available to our paying clients.

[1] RBA E2 Household Finances – Selected Ratios June 2017