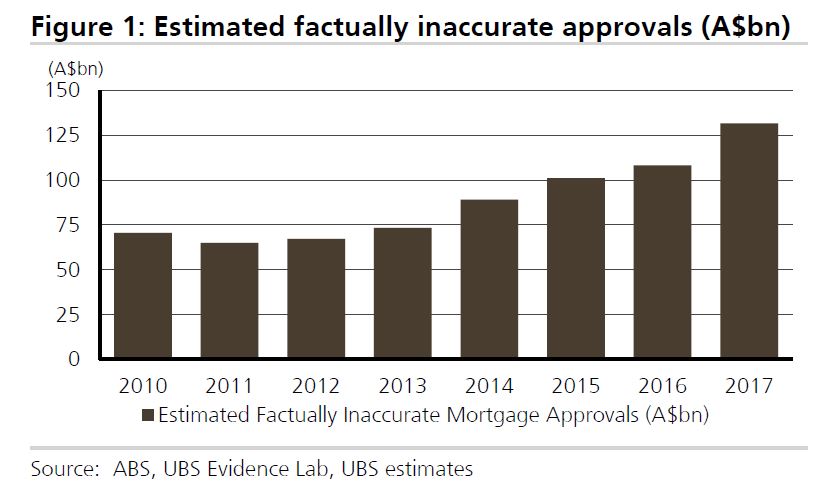

The MFAA and FBAA have harshly criticised a UBS report which claimed 1/3 of mortgage applications were not entirely accurate (which they term ‘liar loans’).

The report, which also claimed broker channel loans were more likely to contain inaccurate information, was branded ‘reckless’ by the FBAA because it was “based on implied presumptions.”

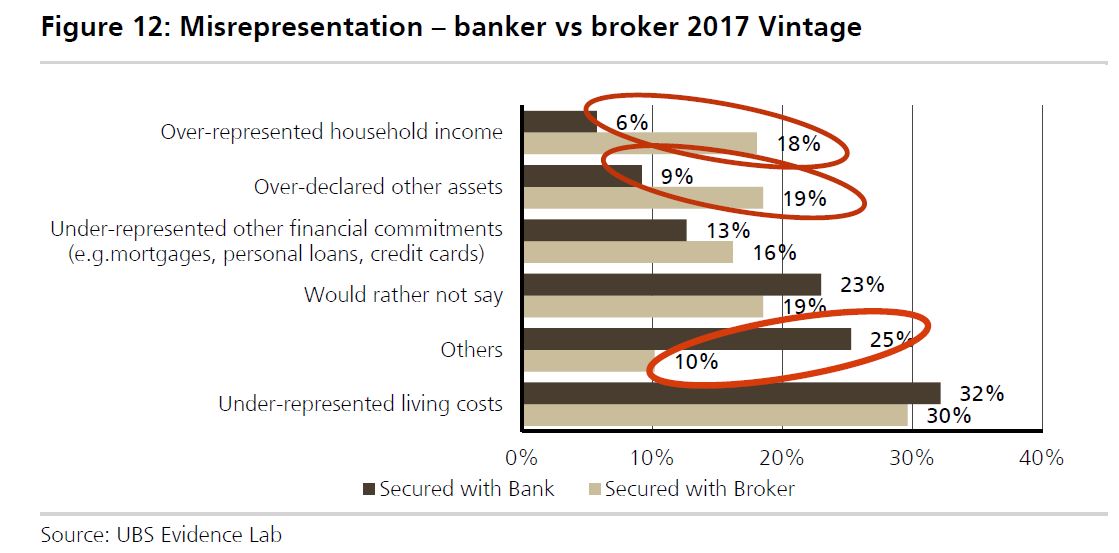

MFAA CEO Mike Felton questioned the validity of UBS’ results, stating that “we particularly question their comparison of misrepresentation in the ‘Banker vs broker’ channels given that the actual data shows us that default rates experienced on loans originated through the respective channels are quite similar once controlled for demographic differences.”

Felton also pointed to the low numbers of brokers being deregistered by ASIC, the high market share of brokers and ASIC’s Review of Mortgage Remuneration to counter UBS’ claims. He also notes that “whilst the broker is an intermediary in the process with a significant role, final responsibility for approving or declining a loan has to lie with the lender.”

eChoice’s general manager of aggregation Blake Buchanan argued that UBS’ report demonstrated a lack of understanding of the sector: “the level of scrutiny for broker introduced business is greater than their retail counterparts and with advancements in technology, information sharing and better regulation the event of misrepresentation is more discoverable than ever before.”

Lenders also criticised UBS. Major bank ANZ, which was singled out by UBS for an alleged high proportion of incorrect loans, told MPA: “a survey of 907 people covering all of the major banks is an extremely limited sample given ANZ has more than one million home loans.”

Methodology and sample size

UBS results come from an online survey of 907 individuals who had taken out mortgages in the last 12 months.

Peter White, executive director of the FBAA, has asked to see UBS’ questions (of which there were 70) and asked whether participants were paid to take part, arguing that “UBS must prove there is no steering of answers or influences to produce outcomes which are not factual or fair or commercially sound.”

ANZ and brokers have questioned whether UBS’ sample size could adequately support the bank’s claims. UBS does not disclose what proportion of its respondents used brokers, but assuming 50%, that meant 65 respondents claimed “the broker suggested I misrepresent” on their mortgage application. Just 9 individuals claimed bankers had suggested they misrepresent.

In comparison, ASIC’s Review of Mortgage Broker Remuneration analysed 1.4m home loans worth $5.5bn, collecting 157 data points for each, in addition to surveying 3000 consumers on their opinion of brokers.

The MFAA told MPA it will continue to benchmark against ASIC’s data rather than consumer surveys.

UBS involvement in Australia and fines

FBAA boss White also criticised UBS’ knowledge of mortgage broking: “this is not their data and not data from a bank/lender, so the question must be asked as to the accuracy and integrity of the research, which is fundamentally divorced of market broker and lender marketplace data.”

According to APRA’s monthly banking statistics, UBS have $0 lent out in mortgages in Australia although they are involved in over $2bn of lending to Australian corporations.

UBS themselves disclose they are linked to the major banks through the provision of investment banking services. However, the bank is not a member of the Australian Bankers Association or the Australian Finance Industry Association, and so not involved in the Combined Industry Forum on broker remuneration.

The bank has been fined for misconduct several times in recent years, albeit for services not clearly connected with their recent report, and in many cases outside Australia.

In 2015 UBS was fined US$545m by the UK regulator for rigging inter-bank exchange rates, US$15m in 2016 by the US regulator for failing to properly instruct financial advisors on the products they were selling and 2 million Swiss Franks in 2017 for releasing price-sensitive information too late. UBS’ most recent brush with ASIC was a $280,000 fine in June this year for incorrect disclosures related to trading and an electronic trading system.

What is the industry doing to respond?

With UBS’ report covered extensively by Australia’s financial and mainstream press, the industry has come under pressure to protect broking’s reputation.

The MFAA and FBAA have made public statements against the report, although it is not clear whether they will engage directly with UBS.

ANZ told MPA that: “We have processes in place designed to ensure our home loans continue to be assessed conservatively. This includes applying an interest rate floor of 7.25% and using the higher of either the customer-stated expenses or a benchmark based on independent data provided by the Melbourne Institute.”

ANZ added that UBS’ report “reinforces the need for the introduction of Comprehensive Credit Reporting which ANZ strongly supports.”