Westpac has confirmed that the bank “detected mis-use” of the New Payments Platform’s PayID feature and “took additional preventative actions which did not include a system shutdown.” Via Computerworld.

Fairfax Media yesterday revealed details of the incident,

citing a confidential Westpac memo that said around 60,000 NPP PayID

lookups were made from seven compromised Westpac Live accounts. Around

98,000 “successfully resolved to a short name and this was displayed to

the fraudster,” the memo said, according to Fairfax.

“No customer bank account numbers were compromised as a result,” a spokesperson for the bank told Computerworld in a statement. “Westpac Group takes the protection of customer data and privacy extremely seriously.”

The NPP was launched in February 2018.

The platform enables real-time transfers between banks as well as a

number of other features including data-enriched transactions. As of

February this year, more than 75 financial institutions supported

system, with 52 million account holders able to make payments via the

NPP, according to NPP Australia, which maintains the platform.

PayID

is the platform’s addressing service. It allows payments to be directed

using an alternative identifier, such as an email address, ABN or phone

number, rather than using a BSB and account number.

“NPP Australia has firm regulations in place that require

participating financial institutions to monitor, detect and shut

down any attempts to harvest data from PayID,” an NPP Australia

spokesperson said. “NPP Australia is working closely with Westpac on

this matter.”

“No financial details or credentials are available

from the PayID database, and therefore none of these details have been

compromised,” the spokesperson said. “The only details obtained have

been the account name which was designed to be returned to a legitimate

enquiry.”

A PayID can’t be used to withdraw funds and “on its own cannot be used to create a false identity,” the spokesperson said.

“While

this incident was unacceptable, the information obtained would be

readily available in other public places,” the spokesperson said. “All

participating financial institutions are on notice and may apply

additional security controls if deemed necessary.”

“PayID was designed to provide more reassurance during the

payments process; it enables a payer to see the name associated with a

PayID to reduce the risk of a mistaken payments or scam,” the

spokesperson said.

Tony Richards, RBA Head of Payments Policy Department spoke at the Chicago Payments Symposium, Federal Reserve Bank of Chicago and described the progress on the new payments platform – NPP. 2 million PayID registrations have been achieved so far, and the volume of payments has already outpaced cheques in the system.

Initial NPP operations

After industry testing through much of 2017, the NPP became operational for industry ‘live proving’ in November 2017. It was launched for public use on 13 February this year. This involved around 50 institutions initially, with this number now having increased to around 65 institutions.

As with any completely new payment system, financial institutions have mostly taken a staged approach in their rollout strategies, gradually introducing services, channels and customer segments. In some cases this was to manage risk and allow them to fine-tune their systems and processes, while in other cases it has reflected different stages of readiness. The major banks have mainly focused initially on providing payment capabilities to consumers ahead of businesses, with the rollout to consumers now at a fairly advanced stage.

At this point, there are more than 50 million Australian bank accounts accessible via the NPP, with that number growing steadily. The number of PayID registrations has just reached 2 million – Australia has a population of 25 million. And monthly volumes and values of NPP transactions have been growing strongly.

One interesting statistic is that the number of payments occurring through the NPP has already surpassed the number of cheques that are being written by Australian households, businesses and government entities

An international comparison also offers another interesting metric. While each country is its own special case, it appears that the adoption of the NPP is proceeding at least as quickly as occurred for some other fast-payment systems

As long as the rollout of NPP to households has not been completed, advertising of Osko by BPAY has been limited, but I would expect that this will be picking up, and that financial institutions will also be doing more promotion of real-time payments to their customers. So I would expect the value and volume of NPP transactions to continue to grow strongly.

Some early lessons learned

While the NPP was launched less than eight months ago, I think one can make a number of observations that may be of interest to this audience regarding its design and build, as well as its operation to date.

The presence of a well-resourced project office (from KPMG as well as from APCA and then NPPA) that was independent of the participants was important in the design, build and test phases. This ensured high quality papers for meetings, brought skills that might not have been readily available from participants, and provided independent perspectives during debates about the design and build

Having three aggregators (or service providers) involved as participants was important in ensuring the broad reach (and public legitimacy) of the NPP. The majority of the institutions that were ready to go on Day 1 were small banks, credit unions and building societies using the services of aggregators.

While the build of the Basic Infrastructure and FSS in the centre were major projects, the internal builds for NPP participants were the most challenging tasks. The systems of large banks are inevitably extremely complex, and upgrading them to allow real-time posting and 24/7 operation has taken longer than expected for some. Banks have also placed significant focus on ensuring that their fraud detection systems can support real-time payments.

Ubiquity (or near-ubiquity) is important. It is hard for a new payment system or for individual participants to go out and market aggressively to customers until a critical mass of institutions and accounts are on board. However, balancing this point and the previous one is a challenge. Decisions to launch to the public can only occur once a critical mass of participants is ready, but a program cannot be expected to move at the pace of the slowest participant.

Real-time settlement is going well. The challenges raised by out-of-hours and weekend operations can be met by appropriate central bank liquidity arrangements. Banks can easily move the balances in their Exchange Settlement accounts between the FSS and the RBA’s main RTGS system during normal business hours. These balances are then all moved into the FSS overnight and on weekends. In addition the Reserve Bank introduced a new liquidity facility for open-dated repos, which are available to holders of Exchange Settlement accounts at no penalty relative to the Bank’s policy rate.

Five or six years ago, some banks may have questioned the case for moving to real-time payments, however no one is questioning that case now. Indeed, the early signs are that banks are looking to move their Direct Entry payments over to the fast rails sooner than was earlier expected. Similarly, the decision to move to the ISO 20022 message format and richer data will be an important one for future innovation.

It was important to have the Addressing Service ready to launch on Day 1. PayIDs get around the problems of end-users having to enter lots of numbers, give certainty about the recipient, help avoid ‘fat finger’ problems and mistaken payments, and can reduce fraud.

The involvement of the central bank – from the policy side, as well as in the delivery of settlement arrangements and as a banking service provider – has been important. I suspect that some industry participants may initially have had some concerns about having the Reserve Bank involved, but that they would recognise now that our involvement helped to get some key aspects of the design, build, and business rules right.

The fact that the Basic Infrastructure will be operated as an industry utility available to all, with commercial payment services to be provided by separate overlay services, was also helpful in getting agreement among participants in the design phase.

With the initial build mostly complete, the industry has ambitious plans for additional NPP functionality. While some of this could potentially be delivered via overlay services, it is likely that there will be additional central functionality provided or arranged by NPPA – for example, possibly a central consent and mandate service that could be used to enable direct debits though the NPP. As NPPA increases its capabilities, it may also look to new means of providing functionality. On Friday it announced an API framework with three sample APIs.

From October this year, bank customers will be able to replace their clunky BSB and account number with an email address or mobile phone number, according to experts.

This ‘PayID’ will be a crucial part of Australia’s new payments system, which will allow almost instant bank transfers, 24 hours a day, 365 days a year.

The Reserve Bank, which operates the ageing system that clears payments between accounts, has been busily working for years with big players in the industry on the billion-dollar ‘New Payment Platform’ or ‘NPP’.

There’s plenty of complicated stuff happening behind the scenes, but one of the main things Australians should know is that, from October, they’ll be able to pick a PayID for each bank account they want to receive super-fast payments into.

NPP Australia CEO Adrian Lovney told The New Daily that the PayID concept will make account numbers easier to remember, and remove the risk of accidentally sending money to the wrong person.

“It makes payments more intuitive and simpler because users will be able to provide payers details which are easy to remember such as an email address or phone number,” Mr Lovney said.

“This offers greater peace of mind as people no longer have to rely on providing financial account information, such as a BSB and account number, to payers so they can receive payments.

“And services that use PayID may display a PayID name before you send a payment as an additional level of confirmation that you are sending money to the right person.”

So, if a family member wants to send you money or you’re splitting the bill at a restaurant with friends, you can simply tell them to type your PayID into their online banking and, in about 15 seconds, the money will be in your account.

The new system will be so fast and simple, it has been speculated that credit cards and cash will lose popularity.

It was built by the Society for Worldwide Interbank Financial Telecommunication (SWIFT), which also built Australia’s current payment system in 1998.

It will allow real-time processing for all ‘push’ payments (such as wages, welfare payments, bill payments or transfers to friends and family), but won’t speed up ‘pull’ payments made on debit and credit cards.

Payments expert Nathan Churchward, whose employer Cuscal is one of the 13 companies working on the new system, predicted that PayID could become as popular a brand name to Australians as Google and Uber.

He gave a real-world example: he recently bought $2500 worth of tickets for a group of friends and accidentally gave them all his wrong bank account number. Their payments bounced back and he was left wondering why no one was paying up.

“I work in banking. You’d think I’d be able to remember my account and BSB. But I can’t!” Mr Churchward told The New Daily.

“With PayID, if you get the mobile number wrong, it will ask you if you want to pay ‘Joe Bloggs’ and you’ll realise and won’t proceed.”

Businesses also won’t have to “splash” their bank details all over the internet, where fraudsters lurk, he said.

Cuscal’s hot tips on PayID

You can’t pick a random number. Banks will probably require a mobile phone number, email address, Australian Business Number (ABN) or Australian Company Number (ACN)

You can set multiple ‘PayIDs’ for the one bank account. For example, your mobile phone number and email could both be linked to the same transactions account

However, you can’t link the same PayID to multiple accounts

Every PayID will be changeable. So if you get a new phone number, you’ll be able to ask your bank to change your PayID to the new number

If you switch to a new bank, you’ll be to reuse an old PayID. But any direct debits you’ve set up won’t automatically transfer across

Some institutions may restrict PayIDs to specific account types. So you might be able to link to a debit card account, but not a mortgage offset or term deposit

Your institution may not offer PayID straight away in October

The Australian payments system is evolving, both in terms of some innovative new payment instruments that are on their way and the declining use of some of our older or legacy payment instruments. Tony Richards RBA Head of Payments Policy Department RBA, spoke at the Payments Innovation 2016 Conference on this evolution.

There is a lot happening in the payments industry at present, so my sense is that it would be premature to have a serious discussion about possibly phasing out cheques before the implementation of the New Payments Platform (NPP), which is scheduled to begin operations in late 2017. But if this conference was to revisit this issue in early 2018 with the NPP up and running, it should find significant new payments functionality in place. This will include the ability for end-users to make real-time transfers with immediate availability of funds, to make such transfers on a 24/7 basis, to attach data or documents with payments or payment requests, and to send funds without knowing the recipient’s BSB and account number. These are all aspects that match or exceed particular attributes of cheques.

In addition, by early 2018 another two years will have passed and there will no doubt have been a significant further decline – based on current trends, a further 30 per cent or so – in cheque usage.

By that point, more organisations and individuals will have further reduced their cheque usage. The Bank has recently been doing some liaison with payment system end-users in our Payments Consultation Group and has heard some impressive accounts about how some of the major Commonwealth government departments and some large corporates have largely moved away from the use of cheques. Cheque usage in the superannuation industry has also fallen very significantly as part of the SuperStream reforms.

A shift away from the use of bank cheques is also underway in property settlements. On average, there are around 40 000 property transactions in Australia each month, plus a significant number of refinancings, with most of these requiring at least a couple of cheques for settlement. However, starting in late 2014 and after much preparatory work, electronic conveyancing and settlement is now feasible. This is being arranged by Property Exchange Australia Ltd (an initiative that includes several state governments and a number of financial institutions), with interbank settlement occurring in RITS, the Reserve Bank’s real-time gross settlement system. Volumes have risen steadily and by late 2015 the number of property batches settled in RITS – each batch typically corresponds to a single transaction or refinancing – had reached nearly 4 000 per month. This trend is expected to continue.

In addition, the Bank’s Consumer Use Survey indicates that usage of cheques is falling rapidly for households of all ages. Our survey from late 2013 confirmed that older households continue to use cheques more than younger ones. However, older households are also reducing their use of cheques significantly. And with more and more older households now using the internet, their use of cheques is likely to continue falling. Indeed, I’m sure we all have a story about an older family member or friend who has recently bought or received a tablet or notebook and discovered the benefits of being online.

Graph 8

Graph 9

We will get a further reading on households’ use of cheques and other payment instruments in the Bank’s next Consumer Use Survey, which – if we follow the timetable of recent surveys – will be published in the first half of next year based on data collected late this year.

More broadly, as the industry starts to think about options for the cheque system, it will be important to make sure that those parts of the community that still use cheques are fully consulted so that we can be sure that their payment needs are met by other instruments. This is likely to involve consultations with organisations representing older age groups, the non-profit sector and those in rural Australia.

Cash

Discussions about the declining use of cheques sometimes also touch upon the declining use of cash.

Because transactions involving cash typically do not involve a financial institution, data for the use of cash are actually quite limited. However, one good source of data on the use of cash by individuals is the Bank’s Consumer Use Study. Our most recent study, in late 2013, showed that cash remained the most important payment method for low-value transactions (around 70 per cent of payments under $20). However, it confirmed that the use of cash had declined significantly, with the proportion of all transactions involving cash falling from 70 per cent in the 2007 survey to 47 per cent in 2013.

More recent data on the transactions use of cash are not available, though the ongoing fall in cash withdrawals from ATMs and at the point of sale suggest that it has continued. In addition, the continuing strong growth of contactless transactions and the growing acceptance of cards for low-value transactions are also suggestive of a further decline in the use of cash.

Graph 10

Graph 11

However, that is where the parallels with cheque usage end. While the use of cash in transactions has been declining, the demand to hold cash has continued to grow. This is the case for low denomination banknotes as well as high denomination ones. Indeed, in recent years there has been a modest increase in the rate of growth of banknotes on issue, to an annual rate of around 7 per cent over the past couple of years. More broadly, over the longer term, growth in banknote holdings has been largely in line with nominal growth in the overall economy.

Graph 12

Graph 13

The growing demand for holdings of cash suggest that it continues to have an important role as a store of value and there is some evidence – from demand for larger denomination notes – that this increased following the global financial crisis. So, despite the decline in use in transactions, cash is likely to remain an important part of both the payments system and the economy more broadly for the foreseeable future. In particular, significant parts of the population appear to remain more comfortable with cash than with other payment methods in terms of ease of use for transactions or transfers, as a backup when electronic payment methods may not be available, or as an aide for household budgeting.

Given the important ongoing role of cash in the payments system, the Bank is currently undertaking a major project to upgrade the existing stock of notes. Counterfeiting rates of the current series of banknotes remain low by international standards but have been rising and there are some signs that the counterfeiters are getting a bit better with new and cheaper scanning, printing and image manipulation technology. Accordingly, the program for the next generation of banknotes includes major security upgrades that should ensure that Australia’s banknotes remain some of the world’s most secure. The first release of the new banknotes will occur in September this year, with the release of the new five dollar note.

Australia is not alone in continuing to invest to ensure that the public can continue to have confidence in its banknotes. The United States has also done so recently, and Sweden – which is often cited as being furthest along the path to a cashless or less-cash society – is also in midst of introducing a new series of notes.

Digital currencies and distributed ledgers

As the use of cash and cheques continues to fall, the Bank will – subject to there not being any overriding concerns about risk – be agnostic as to what payment methods replace the legacy systems, consistent with its mandate to promote competition and efficiency.

In the short run, it is likely that we will see further growth in the existing electronic payment methods, including payment cards in their various form factors. In the medium term, it is likely that we will see growth in new payment methods and systems, including those that will be enabled by the NPP.

Let me stress that the Bank has not reached a stage where it is actively considering this, but in the more distant future it is even possible that we may we see a digital version of the Australian dollar. As the Bank has noted in the past, it seems improbable that privately-established virtual currencies like Bitcoin, with its significant price volatility, could ever displace well-established, low-inflation national currencies in terms of usage within individual economies. Bitcoin has, however, served to stimulate interest in the potential offered by distributed ledgers, extending to the possibility of central-bank-issued digital currencies. A plausible model would be that issuance would be by the central bank, with distribution and transaction verification by authorised entities (which might or might not include existing financial institutions). The digital currency would presumably circulate in parallel (and at par) with banknotes and other existing forms of the national currency.

A few countries have explicitly discussed the possibility of digital versions of their existing currency. Both the Bank of England and Bank of Canada have indicated that they are undertaking research in this area. And a recent announcement from the People’s Bank of China indicated that it has plans for digital currency issuance, though few specifics were provided.

The Bank will be interested to see what proves to be possible and what proves to be problematic, as countries consider going down the path of digital currency issuance. Given the various cybersecurity and cryptography risks involved, my personal expectation is that full-scale issuance of digital currency in any country, as opposed to limited trials, is still some time away. And I think it remains to be seen if there is real demand for a digital equivalent of cash and what it might offer end-users relative to what will be offered by the various forms of real-time payments that are being developed in many countries through projects like the NPP.

I should also touch briefly on another potential application of blockchain or distributed ledger technologies, namely in the settlement of equity market transactions. As the overseer of clearing and settlement facilities licensed to operate in Australia, the Bank obviously has a keen interest in the plans of the ASX Group to explore the use of distributed ledgers. Along with the Australian Securities and Investments Commission and other relevant public sector organisations, we will be working closely with ASX as it considers whether a distributed ledger solution might be the best way to replace its existing CHESS infrastructure.

Review of Card Payments Regulation

I will conclude with a few comments on the ongoing Review of Card Payments Regulation.

The Bank issued a consultation paper containing some draft changes to standards in late 2015. It has received substantive submissions from 43 different stakeholders, with a number of parties providing both a public submission and additional confidential information. 33 non-confidential submissions have been published on the Bank’s website.

The submissions indicate that most end-users of the payments system are broadly supportive of the Bank’s reforms over the past decade or more. Some submissions have indeed suggested that the Bank could have gone further in its proposed regulatory changes. Financial institutions and payment schemes have expressed a range of views. For the most part they have recognised the policy concerns that the Bank is responding to. In some cases there is a fair bit of common ground in areas where they have made suggestions for changes to the draft standards, but in others there are conflicting positions that correspond to the different business models of the entities that have responded to consultation.

The Payments System Board discussed the Review at its meeting last Friday, focusing on issues that stakeholders have highlighted in submissions. As we always do when regulatory changes are proposed, Bank staff will be meeting with a wide range of stakeholders to discuss submissions. Indeed, we have already had a significant number of meetings, sometimes multiple meetings with particular firms as they were preparing their submissions.

Some of the issues to be explored in consultation meetings include: the treatment of commercial cards and domestic transactions on foreign-issued cards in the interchange benchmarks; the proposed shift to more frequent compliance to ensure that average interchange rates remain consistent with benchmarks; and the calculation of permissible surcharges for merchants (such as travel agents or ticketing agencies) that are subject to significant chargeback risk when they accept credit or debit cards.

One other issue that I would like to flag ahead of our consultation meetings relates to the proposed reforms to surcharging arrangements. The Bank’s proposed new surcharging standard has been drafted to be consistent with amendments to the Competition and Consumer Act 2010 which were passed by the House of Representatives on 3 February and by the Senate yesterday.

The proposed framework envisages that merchants will retain the right to surcharge for expensive payment methods. However, the permitted surcharge will be defined more narrowly as covering only the merchant service fee and other fees paid to the merchant’s bank or other payments service provider. Acquirers would be required to provide merchants with easy-to-understand information on their cost of acceptance for each payment method, with debit/prepaid and credit cards separately identified. The draft standard would require that merchants would receive an annual statement on their payment costs which they could use in setting any surcharge for the following year. The information in these statements should allow the Australian Competition and Consumer Commission (ACCC) to easily investigate whether a merchant is surcharging excessively.

The objectives of the proposed changes to the regulation of surcharging received widespread support in submissions. However, a number of financial institutions have argued that it would be difficult to provide statements to merchants on their average acceptance costs for each payment system. Some have said that their billing process draws on multiple systems within their organisations (and sometimes from third parties), so that it is not straightforward to provide the average cost information proposed by the Bank. Some have indicated that they do not currently provide annual statements to merchants, so this would be a significant change. Accordingly, a number have suggested that they would prefer a significant implementation delay before they are required to provide merchants with the desired transparency of payment costs. Bank staff will be testing these points in our consultation meetings with acquirers. In doing so, we will be looking to see what might be done to ensure that the standards can take effect as soon as possible, in order to meet community expectations about the elimination of instances of excessive surcharging.

More broadly, the Board also discussed a possible timeline for concluding the Review. The Bank’s expectation is that a final decision on any regulatory changes should be possible at the May meeting. It is too soon to give much guidance on the date when any changes to the Bank’s standards might take effect, but the Board recognises that an implementation period will be necessary for the industry.

According to the Galaxy research commissioned by MasterCard, Australians of all ages continue to embrace contactless payments, with 66% preferring to use tap and go for small transactions under a $100 instead of entering their PIN, and 64% favoring it as a payment method over cash. The study was conducted online during October 2015 using a sample of 1,005 Australians aged between 18-64 years old, who have a credit or debit card.

Results from the survey showed that speed and convenience continue to generate increased adoption of the technology by Aussies (77%), and safety benefits available through contactless cards are also contributing to its growing popularity over cash; the majority of Australians (82%) believe they are more likely to be reimbursed for unauthorised contactless payments made with a stolen credit or debit card than they are likely to get stolen cash back.

First introduced into Australia in 2007, contactless payments have been one of the fastest-adopted payment technologies globally, and despite recent reports, MasterCard data in addition to industry data, reveals no increase in fraud specifically relating to contactless payments. Australian Card Data* has found that fraud relating to contactless payments makes up less than 2% of all total card fraud. This is despite huge growth in the category, where contactless MasterCard transactions have grown 148% based on card data compiled by MasterCard and Visa showing that number of Contactless MasterCard transactions grew 148% between July 2013 and 2014.

MasterCard SVP and Country Manager, Andrew Cartwright said “This research indicates not only a shift in the preferred methods in which consumers like to pay, but also suggests that they are beginning to understand and trust the safety benefits associated with paying by card. As contactless payments continue to rise, cash is increasingly become unnecessary real estate in wallets.

“I’ll take a card any day of the week – it is safer than cash. With a card I’m protected against unauthorised purchases, whereas, if my wallet is stolen, the cash is as good as gone”, said Cartwright.

Shoppers in West Australia have the highest preference for contactless payments in the country (72%), followed by shoppers in NSW (67%), VIC and TAS (66%).

Tony Richards, Head of Payments Policy, RBA, spoke at the APCA Australian Payments 2015 Conference today. He gave an update on current payment initiatives in Australia, including NPP, payments coordination, and the interchange regime. He also mentioned the outcomes from the FSI.

The first is the initiatives that came out of the 2012 conclusions of the Reserve Bank’s Strategic Review of Innovation in the Payments System. The background to the Review was a growing amount of evidence that the services provided to end-users of the Australian payments system were falling behind the services available to end-users in some other countries.

The most prominent outcome of the Review was that the Bank asked the payments industry to consider ways of filling the gaps in the payments system that had been identified in the Review. As you know, the industry – coordinated by APCA – proposed a project, which has been developed over the past three years, to build some new industry infrastructure which will be called the New Payments Platform (NPP). The NPP will deliver real-time, data-rich payments to end-users on a 24/7 basis. It will also be a platform for all sorts of other innovative services, many of which we cannot yet imagine.

The Bank has been heavily involved in this project. It is one of the 12 financial institutions that have agreed to fund the build of the NPP and to connect to it when it goes live. The Bank is also developing a new service, the Fast Settlement Service (FSS), which will provide real-time settlement of NPP transactions. My colleagues in Payments Settlements Department are making good progress on the FSS.

Paul Lahiff, the Chair of NPP Australia Ltd, will be speaking to you in more detail about the status of the NPP, but I can tell you that the Payments System Board (the Board), having encouraged this project, has been taking a close interest in it and has been pleased by the excellent collaboration in the industry.

Another initiative coming out of the Strategic Review of Innovation was that the Bank called for the establishment of an enhanced industry coordination body. The intention was that this should take a more strategic view than existing industry governance bodies and have membership from a wider range of institutions than had traditionally been the case for APCA. It was also to have high-level representation, with individuals who are more able to commit their organisations to courses of action agreed by the group.

The rationale for this focus on industry governance was that the identified gaps in the services offered to end-users partly reflected difficulties in getting the industry to work together to develop the cooperative elements of payment systems. The development of common rules, standards, communications networks and other infrastructure sometimes requires collaborative innovation, where institutions have to work together. There was a concern that this had previously proved difficult in Australia.

I’m happy to say that there has been good progress here. The Australian Payments Council held its first meeting in late 2014 and – as you will have heard in the first session today – has recently been consulting on an Australian Payments Plan, seeking views on long-term trends, systemic challenges and desirable characteristics for the payments system.

The first meeting between the Board and the Council occurred in August. The Board is looking forward to seeing the progress that the Council makes on its payments plan. The Council may be a useful vehicle for the payments industry, including the Bank, to think about some of our legacy payment systems, in particular the future of the cheque system.

Fraud, digital identity and cyber security are other areas where there could be real benefits to industry collaboration. Of course, they are not just issues for the payments system. Cyber security and digital identity were referred to in the Government’s response to the Financial System Inquiry (FSI) Report and are issues that touch the entire financial system and, indeed, the broader economy.

The second issue I would like to cover is the Bank’s ongoing Review of Card Payments Regulation.

In its March 2014 submission to the FSI, the Bank indicated that it would be reviewing some aspects of the regulatory framework for card payments. The Final Report of the FSI, which was released in December 2014, endorsed the broad nature of the Bank’s reforms over the past decade or more but noted a few areas where the Inquiry believed the existing framework could be improved. The Bank released an Issues Paper in March 2015, inviting submissions on a broad range of issues in card payments regulation, including those raised in the FSI Report. I will touch on four of these issues.

The first is the growing lack of transparency of payment costs to many merchants. While interchange fees on credit and debit cards are currently subject to benchmarks that must be observed every three years, there has been a tendency for the two large international four-party schemes to promote new, high-interchange, high-rewards cards. At the same time, they have introduced lower interchange rates for ‘strategic’ or other preferred merchants. These merchants get the same low interchange rate – for credit cards, as low as 20 basis points – on all their transactions, even if a super-premium, high-rewards card is presented. But smaller merchants and others who do not benefit from strategic rates pay interchange rates of up to 200 basis points on their transactions. Furthermore, when presented with a card, such merchants may have no way of knowing if it is a card with a 30 basis point interchange rate or a 200 basis point rate. So the issues that we have raised are the growing lack of transparency of payment costs for many merchants and the growing wedge in average payment costs between preferred and nonpreferred merchants.

Second, the Bank is consulting on whether it would be desirable to lower the interchange benchmarks or to make other changes to the system, such as to have more frequent compliance. One issue here is that the behaviour of schemes and issuers under the current three-yearly compliance system is seeing average interchange rates rising significantly above the benchmark in between compliance dates.

The third issue is whether it would be desirable to extend the coverage of the regulatory framework for interchange payments. This is especially relevant in the case of companion cards – in particular, bank-issued American Express cards, which have issuer fees and other payments that are equivalent in many respects to interchange payments.

The final major issue for the Review is concerns over excessive surcharging in some industries. There is a balance to be struck here between ensuring that merchants have the right to surcharge for expensive payment methods, including some cards, and ensuring that they do not surcharge excessively. Excessive surcharging is not a widespread problem, but I think we can all point to a few cases where there are genuine concerns. The Board is keen to take action here.

The Board discussed the Review in its August meeting and will be discussing it again at its November meeting. In preparation for discussions about possible changes in the regulatory framework, the Board has recently taken a decision to designate five payment systems: the American Express companion card system, the Debit MasterCard system and the eftpos, MasterCard and Visa prepaid card systems. Designation does not impose regulation nor does it commit the Bank to a regulatory course of action; rather it is the first of a number of steps the Bank must take to exercise any of its regulatory powers.

Any proposals to apply regulation to designated systems through standards or access regimes are subject to requirements for detailed consultation. Designation of these five systems will allow a more holistic consideration of the issues – including issues such as the regulatory treatment of companion cards and prepaid cards – as the Bank continues with review of the regulatory framework and considers the case for changes to the framework.

As you know, there has been a lot of discussion of the issues that the Review is focusing on. Banks, payment schemes, consumer organisations and merchants have been able to express views in four different contexts: the original FSI call for submissions, submissions on the FSI’s interim report, the Government’s call for comments on the FSI Final Report, and responses to the Bank’s Issues Paper. And in turn, the industry will have seen the Bank’s views in at least three different vehicles: the Bank’s two submissions to the FSI in 2014 and its Issues Paper from March this year.

We have received over 40 submissions in response to the Issues Paper, with all non-confidential submissions published on our website. The Bank also hosted an industry roundtable in June and has held around 40 meetings with stakeholders.

Overall, there appear to be some areas where there is common ground across most stakeholders. For example, there is fairly wide acceptance that the widening of the international schemes’ interchange fee schedules has created issues in terms of the rising cost of card payments to nonpreferred merchants and the declining transparency of the cost of card payments to them. There is also general agreement that it would be good to deal with instances of excessive surcharging.

However, there are other areas where there are real differences in the views expressed by different stakeholders. These include issues such as whether companion card arrangements should be subject to regulation and whether there might be a case for a reduction in the interchange fee benchmarks.

It will be up to the Board to weigh up the arguments on some of these contentious issues, balancing the interests of consumers, businesses, financial institutions and card schemes. As always, its consideration will be based on its mandate to promote competition and efficiency in the payments system. And let me stress again that if the Board decides to propose changes to the regulatory framework, the Bank will, as usual, undertake a thorough consultation process on any draft standards.

Finally, as you will know, the Government released its response to the FSI yesterday. Its response referred to the Bank’s review and noted that it was looking forward to the Board completing its work on the issues of interchange fees and surcharging. The Government also indicated that it will ban excessive surcharging and give the ACCC enforcement power in this area. I would expect that once the Board has provided greater clarity on what constitutes excessive surcharging, we will work closely with Treasury and the ACCC on legislation. I expect that we will end up with a framework where the Board has decided on a narrower definition of costs of acceptance and allowable surcharges and where the Bank will be able to count on help from the ACCC in the enforcement of the new framework.

In December 2014, a group of Australian financial institutions announced that funding had been secured for the next phase of the New Payments Platform (NPP), which will provide the capability for Australian consumers and businesses to make and receive payments in near to real time. The NPP is one example of a fast retail payment system, a number of which have been implemented in other countries in recent years.

Advances in technology – in particular improved telecommunications, faster processing speeds and wide penetration of internet connectivity – mean that real-time payments can be extended to the high-volume, low-value payments used by consumers and businesses (‘retail payments’). Systems implemented in a number of countries allow businesses and consumers to make and receive payments in near to real time, with close-to-immediate funds availability to the recipient. Fast retail payment systems can benefit end users of payments systems, and also payment providers themselves – for example, by replacing the use of relatively costly cheque payments with real-time transfers using a payment application on a mobile device.

Fast retail payments can be thought of as payments that are available for use by the recipient a short time after the payment has been initiated by the sender – within minutes, or indeed seconds. This contrasts with many established retail payment systems that rely on batch processing where funds are made available on the next business day, or even several days later – particularly in the case of cheques. There are three steps within the payment process relevant for achieving fast payments – clearing, posting and settlement. First, following the initiation of a payment by the customer (payer), the exchange of payment instructions and the calculation of payment obligations between financial institutions (referred to collectively as ‘clearing’) need to be performed in real time. Many retail payment systems have tended to clear payments infrequently in batches, making timely receipt of funds by the payee impossible. Second, the recipient’s financial institution must act on the payment instructions it receives in the clearing process to make funds available to the recipient (‘posting’) in near to real time. Finally, the payer’s financial institution needs to ‘settle’ the funds owing to the receiver’s financial institution for the payment. This typically occurs by transferring funds between accounts held by financial institutions at the central bank (Exchange Settlement Accounts in Australia’s case). Clearing and posting need to occur quickly for a system to be, in effect, a ‘fast’ system. However, settlement between financial institutions need not be completed before funds are made available to the recipient customer. There is therefore freedom for settlement to occur in a number of ways and indeed the fast retail payment systems implemented to date have taken varying approaches. While there have been significant developments in recent years, the concept of fast retail payments is not new. For example, Japan’s Zengin Data Telecommunication System (Zengin System) was established in 1973. The development of fast payment systems has generally occurred in one of two ways: through the extension of existing infrastructures (such as high-value systems or real-time ATM infrastructure) to accommodate high-volume, fast retail payments, or through new purpose-built infrastructure. In most cases, new specialised infrastructure has been adopted for retail payments, but there are examples of hybrid systems processing both high-value and retail payments. For example, Japan’s Zengin System clears both high-value and low-value funds transfers in near to real time, but settlement arrangements vary with transaction size. Switzerland’s Swiss Interbank Clearing (SIC) provides for near to real time clearing and settlement of high-value payments and some retail funds transfers. A range of other countries have introduced fast retail payment systems either as hybrid systems or as dedicated low-value systems since 2000. Australia’s NPP system will rely on newly developed clearing infrastructure, with settlement occurring in real time through a new component of the Reserve Bank’s high-value settlement system, the Reserve Bank Information and Transfer System (RITS).

The use of mobile phones as an access channel for fast payment services is a focus for a number of fast payment systems, including in the United Kingdom, Sweden and Singapore. This dovetails particularly well with some services for easier addressing of payments. For instance, the Paym service recently introduced in the United Kingdom enables mobile phone numbers to be used as payment addresses for person-to-person payments (Payments Council 2014). Users register their mobile phone number and link it to their bank account number. They can then send and receive real-time payments to other registered users using their mobile phone numbers through their bank’s internet portal.

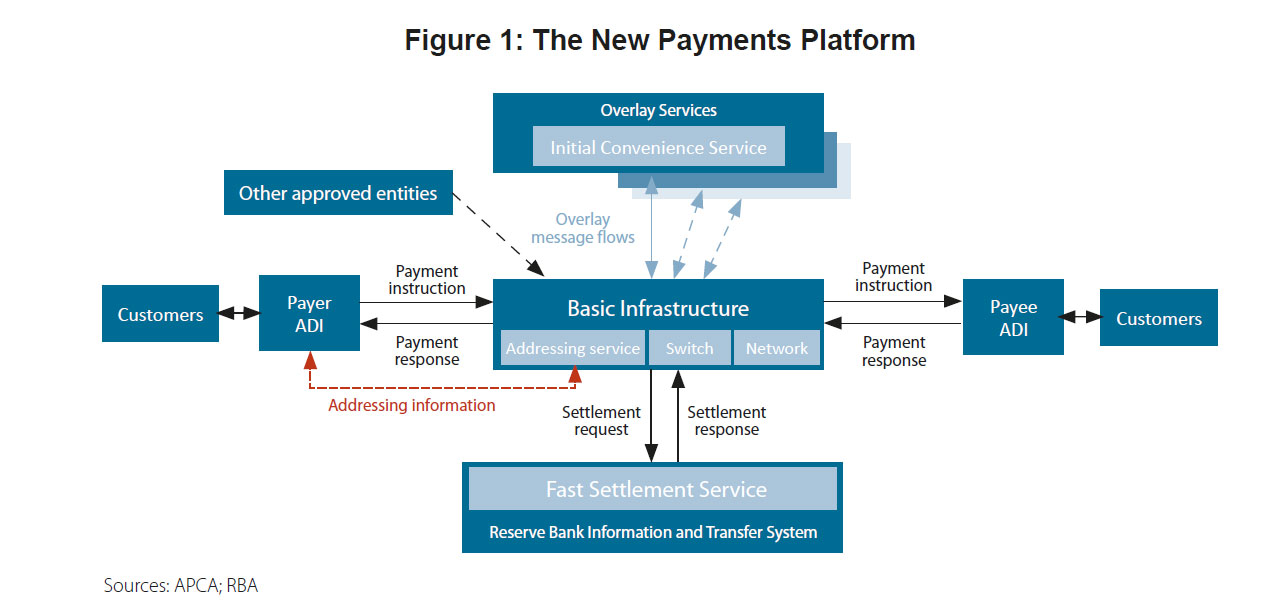

The broad approach to providing infrastructure that would support fast retail payments in Australia was established by the industry Real-Time Payments Committee (RTPC) and published in February 2013 (APCA 2013). The RTPC proposed the establishment of a mutual collaborative clearing utility to provide the payments infrastructure to which authorised deposit-taking institutions would be connected for real-time clearing of payments. This utility, known as the Basic Infrastructure (BI), will not be commercial in nature and will provide a platform through which a variety of payment services can be offered. While financial institutions will be able to offer basic payment services to their customers using only the BI, the model proposed by the RTPC anticipates that a variety of ‘overlay services’ will be able to use the BI to offer commercially oriented services, for instance through a commercial scheme. Participation by financial institutions in any particular commercial overlay would be voluntary. This model was chosen with the view that it would provide the greatest scope for innovation and competition between financial institutions and payment providers in the services that can be offered to end users. The RTPC also proposed that an agreed overlay service, referred to as the ‘Initial Convenience Service’ (ICS), would be built at the same time as the BI, to help establish a compelling proposition for use of the NPP from the outset. While the ICS will be the first overlay to give payments system users access to fast retail payments, it is intended to be the first of a number of overlay services that could be developed over time. The BI and the ICS comprise two of the three main components of the NPP. In addition, the Reserve Bank is developing a Fast Settlement Service (FSS) that will provide line-by-line real-time settlement of transactions processed through the NPP. This model will enable real-time clearing and settlement for retail payments, with the recipient’s financial institution able to provide fast access to funds without incurring interbank settlement risk. The interaction of these three components – BI, ICS and FSS – is illustrated below (Figure 1). Consistent with the approach taken in recently developed fast retail payment systems, the NPP will operate 24 hours a day, 7 days a week and will incorporate ISO 20022 messaging standards to facilitate the inclusion of richer remittance information with transactions. The NPP model also includes an addressing solution, enabling users to receive payments without having to supply BSB and account numbers to the payer. This combination – of real-time capability, 24/7 operations, richer messaging functionality and easier addressing – addresses the key gaps in the payments system identified by the Strategic Review. The capacity for new overlay services to utilise the system should also be a vehicle for innovation and competition.

The FSI Interim report, released earlier in the week, includes a section on how technology may disrupt payments, a critical domain in financial services.

The report says ” Advances in technology have reduced traditional barriers to market entry in payments, such as the need to construct a dedicated network. New entrants can leverage high levels of internet connectivity, penetration of smart devices and pre-existing networks to connect users to payments services more easily and cheaply than incumbents. The payment hub, being developed by eftpos Payments Australia Limited, and the New Payments Platform (NPP), an industry project being developed as a result of the Reserve Bank of Australia’s (RBA’s) strategic innovation review, may further reduce barriers to entry and drive competition. Incumbents in the Australian payments industry are facing competitive challenges from new market entrants, such as PayPal, POLi, PayMate and Stripe. Closed-loop pre-paid systems operated by companies outside the financial sector, such as Apple, Skype and Starbucks, are holding growing amounts of customers’ funds. Apple has also recently signalled its interest in mobile payments more broadly and recently developed fingerprint biometric authentication for its phones. Advances in cryptography and computer processing power have facilitated the development of virtual or crypto-currencies.

Today we look at the potential convergence of new payment mechanism, overlaid on smart devices, and in the context of customer centric thinking. Consider this, the ubiquitous smart mobile device is essentially a mobile wallet plus a payment instrument, a centre of interaction and potentially can provide secure identification.

You walk down a high street and receive a personalised messages from a retailer, based on your profile, as you pass. The offer is triggered by your proximity to the store. It is a deep discount on that item you were goggling last night, available for just 10 minutes. You decide to accept the offer, pay direct from your phone using your secure wallet, and the deal is done. Rather than collect it, you choose to have it delivered to your home, later in the day. No human interaction, simply a combination of technologies to fundamentally change the customer experience.

Consider the disruptive impact of this, on the retail trade, the payments system, and human behaviour.

Is this far fetched? Not at all. For example, Apple has been working on iBeacon, which is “a new technology that extends Location Services in iOS. Your iOS device can alert apps when you approach or leave a location with an iBeacon. In addition to monitoring location, an app can estimate your proximity to an iBeacon (for example, a display or checkout counter in a retail store). Instead of using latitude and longitude to define the location, iBeacon uses a Bluetooth low energy signal, which iOS devices detect”. It is still early, but Apple has been testing it since December last year in its US retail stores. In the UK, Virgin Atlantic is also conducting trial of iBeacon at Heathrow airport, so that passengers heading towards the security checkpoint will find their phone automatically pulling up their mobile boarding pass ready for inspection. Paypay is experimenting with its own version of beacon – “hands Free shopping – the future in here”, they say.

In May, St. George revealed that is trialling iBeacon at three Sydney branches. When a customer walks into the bank, the iBeacon senses the person’s entrance and sends a welcome message and personalised information directly to the iPhone or iPad, according to Computerworld. George Frazis, CEO of St. George Banking Group, said in a statement the launch of the new technology forms part of an increased focus on delivering an innovative and customer-centric in-branch experience. “The future of business will be in the ability to anticipate customer’s needs, understand what matters to them and act on that knowledge to surprise and delight them,” he said. “Our investment in iBeacon will help us to achieve that — and it has the potential to dramatically change the service experience in Australian banking.”

The question is, what is the right regulatory settings to, on one hand allow innovations like this to flourish, whilst on the other hand, ensure that adequate protections are in place. That is the question posed, but not yet answered in the FSI interim report.

“Some submissions argue that firms performing similar functions should be regulated in the same way. This position is often made by large incumbent players concerned about the capacity of new players to operate around the edge of the regulatory perimeter. Failure to apply equivalent regulation may result in an uneven playing field and regulatory arbitrage. It may also incentivise those within the current regulatory perimeter to lower their own standards of compliance to compete. However, applying the full weight of prudential or conduct regulation to small players and new start-ups, regardless of the materiality of the risk they represent, may stifle valuable innovation unnecessarily.”

What is clear to me, based on our survey of households and their use of mobile devices, there is potentially a revolution round the corner, which will disrupt traditional payment mechanisms, retail behaviour and customer expectations. Actually many people are ahead of many of the incumbents, and are expecting to do ever more with their ubiquitous mobile devices. The real power is wedding the multiple technologies contained in the device, to create a seamless consumer experience, with smart analytics and segment data. The marketeers dream of one to one targetting is here. Unless people to select to opt out – if they can find the right tab. That may not be easy.

Following on from yesterdays discussion about current consumer payment trends, today we will look at the current status of the New Payments Platform. “The proposed centralised infrastructure and real-time nature of the system, combined with the flexibility of payment messaging, ability to carry additional remittance information and the easy addressing capability, will mean that payments can be better integrated with many other aspects of our lives. Businesses should be able to achieve substantial efficiency gains and there will be significant improvements to the timeliness, accessibility and usability of the payments system for consumers” according to Tony Richards, the Head of Payments Policy Department at the Reserve Bank. in his recent speech The Way We Pay: Now and in the Future.

A bit of history first. The current payment infrastructure in Australia is complex, quite old and will not provide the flexibility demanded by new devices and systems. It is supported by a complex web of networks and bilateral charging arrangements, which makes it difficult for new players to enter the payments market, and so protects the current incumbents. In May 2010 the RBA announced a review of the Australian payments systems and how innovation may be improved. It took a medium-term perspective, looking at trends and developments overseas in payment systems and at possible gaps in the Australian payments system that might need to be filled over a time horizon of five to ten years. In June 2012, the conclusions from the review were published. The headline findings reflected the potential gaps in the payments system identified during the course of the Strategic Review.

In the Review, the Payments System Board (PSB) identified a number of gaps in the services currently provided by the payments system. Among these were:

the ability for individuals to make electronic payments with real-time funds availability to the recipient

the ability to make and receive such payments outside of normal banking hours

the ability to address payments in a relatively simple way, such as to an individual’s mobile phone number or email address rather than to their BSB and account number

and, most relevant for businesses, the ability to send anything more than a minimal amount of information with an electronic payment.

A key objective was the establishment of a system that would provide real-time retail payments, with real-time funds availability, by the end of 2016. The review recognised that this type of system has been a focus of innovation in a number of other countries. Finally, the bank stated that they believed that a real-time retail payment system would best be delivered by the establishment of a real-time payments hub, rather than a web of bilateral links. It is also prepared to consider helping to facilitate these payments by providing a system for real-time interbank settlement via the Reserve Bank’s RITS system, which currently provides real-time settlement for high-value transactions.

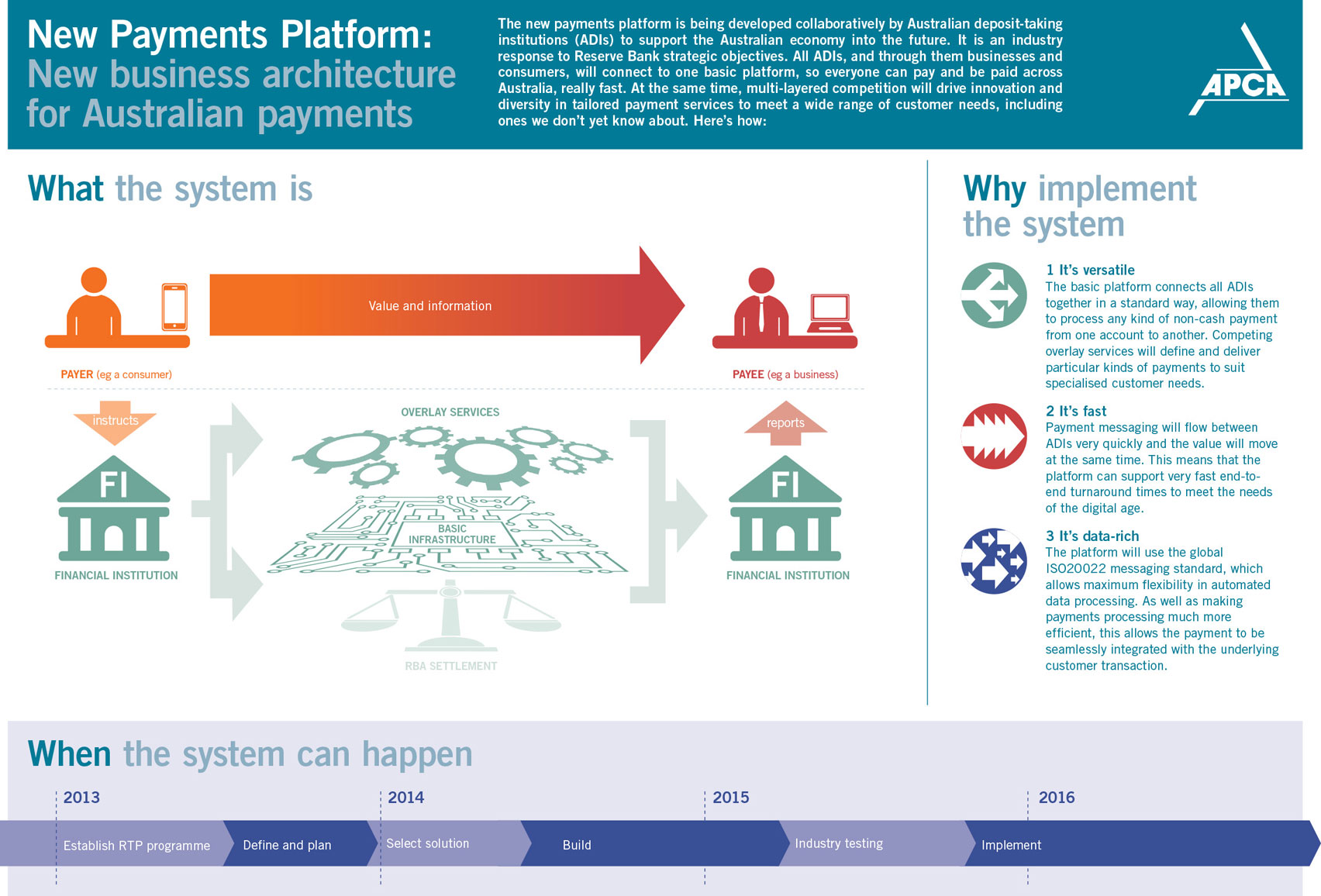

So the New Payment Platform (NPP) was born. An industry steering committee is overseeing development of the NPP. The New Payments Platform Steering Committee first met on 20 June 2013. It comprises senior representatives from the Australian banking and mutual sector, an alternative payments provider and the APCA CEO. An independent Chair, Paul Lahiff, was appointed in September 2013. The Steering Committee appointed KPMG as program manager to the project to ensure a well-resourced, highly collaborative industry program.

According to The Australian Payments Clearing Association CEO, Chris Hamilton, these 17 of its 87 members have agreed so far to fund the network, although the costs are not currently known. Lahiff is quoted as saying that NPP will provide “the basic “rail-tracks” on which “overlays” or payments services would be built. “It is minimalist in what it needs to do. It will be constructed as a utility that will be industry owned,” he said. “That allows networking, switching, addressing and settlement. As long as you have an interface to the basic infrastructure, it allows everybody to compete on how they use it most effectively.”

A new utility entity, owned by the payments industry will be created. Tenders were issued earlier in 2014, and responses are being considered at the moment. About 80 people are working on the project. Once the enabling infrastructure in launched, there is the prospect of additional value-added services “overlay services” being offered. Here is the schematic which APCA draws:

There are a number of issues worth reflecting on.

The banks have considerable investments in the current bilateral systems and processes. Will they need to write off these investments if they migrate to a new platform?

Whilst the establishment of a centralised payment switch is relatively simple (its been done elsewhere), the real challenge is to retrofit the current bank’s systems and processes into the new world. It is well known that some banks have problematic infrastructure, and as a result any migration will be complex and expensive. Banks with batch processing will have issues fitting into a real-time 24/7 world, and may need to create “shadow” real-time proxies such are used for internet banking.

What will the revenue model which will underpin the new infrastructure be?

Will the current 17 members put barriers in the way which means that the new payments infrastructure will be inaccessible by new players and innovators? Will new competitors be locked out?

The intention will be to migrate from sort code and account numbers to a single number used for receiving payments. So should this infrastructure also be considered an a mechanism to establish account number portability. A number of recent submissions to the Federal Government’s financial system inquiry have proposed this.

The NPP has the potential to liberate payments and offer innovation to consumers and businesses. It is essential to evolve payments into a more innovative and open environment, we will see if NPP fits the bill.