I discuss a Nucleus Wealth article authored by Tim Fuller, Head of Advice at Nucleus.

The allure of having complete control over your financial future is very compelling, and becomes even more so in turbulent market periods, like the one we have seen in 2020. So it is understandable that 2020’s volatile markets combined with the opaqueness of many large super funds could have left you wondering if you should be opening your own self managed super fund (SMSF).

A reprise of the current market moves, and a discussion about the underlying drivers, as well as the top 5 issues we get asked about. Plus a quick preview of a new intro…

0:00 Start 0:30 Market Moves 0:26 Nucleus Wealth Article On Capitalism 8:53 Markets 16:14 Drivers 17:33 Top 5 Topics 20:42 New Intro Candidate 21:06 Outro

A reprise of the current market moves, and a discussion about the underlying drivers, as well as the top 5 issues we get asked about. Plus a quick preview of a new intro…

0:00 Start 0:30 Market Moves 0:26 Nucleus Wealth Article On Capitalism 8:53 Markets 16:14 Drivers 17:33 Top 5 Topics 20:42 New Intro Candidate 21:06 Outro

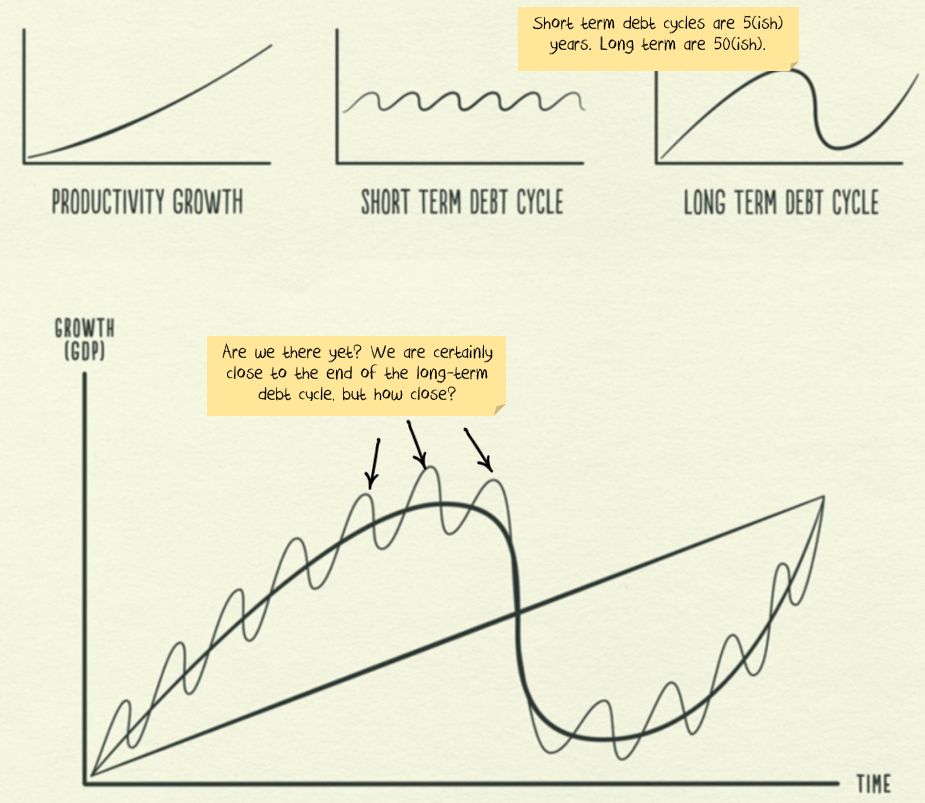

Ray Dalio has a series of explanatory videos that talk about debt cycles and in particular the contrast between a short debt cycle and a long debt cycle.

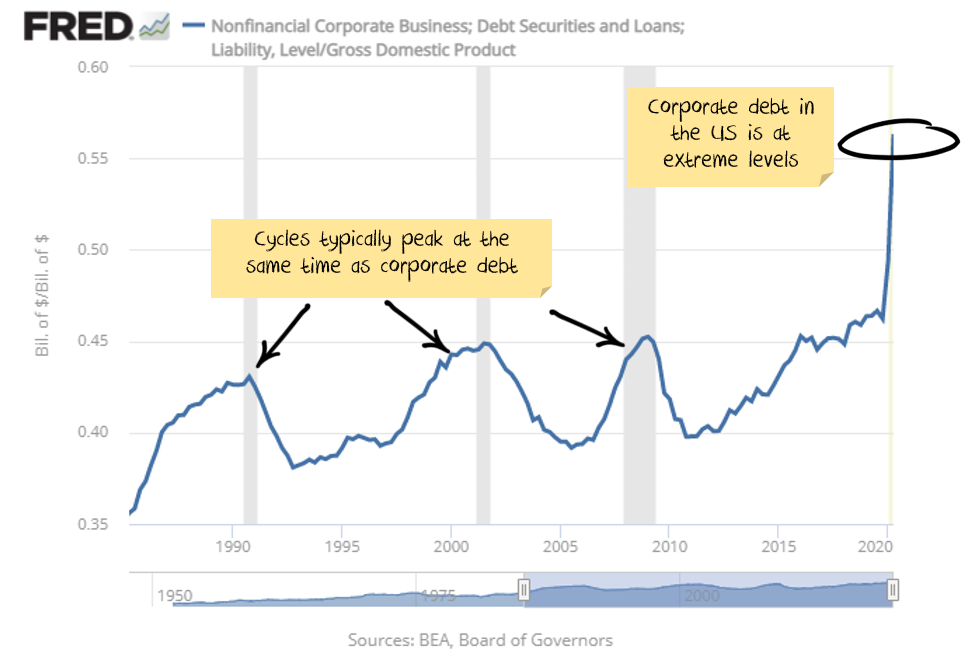

With record levels of corporate debt around most of the globe:

COVID-19 lockdowns suggested that this would be the end of the current short term debt cycle and potentially the end of the current long term debt cycle.

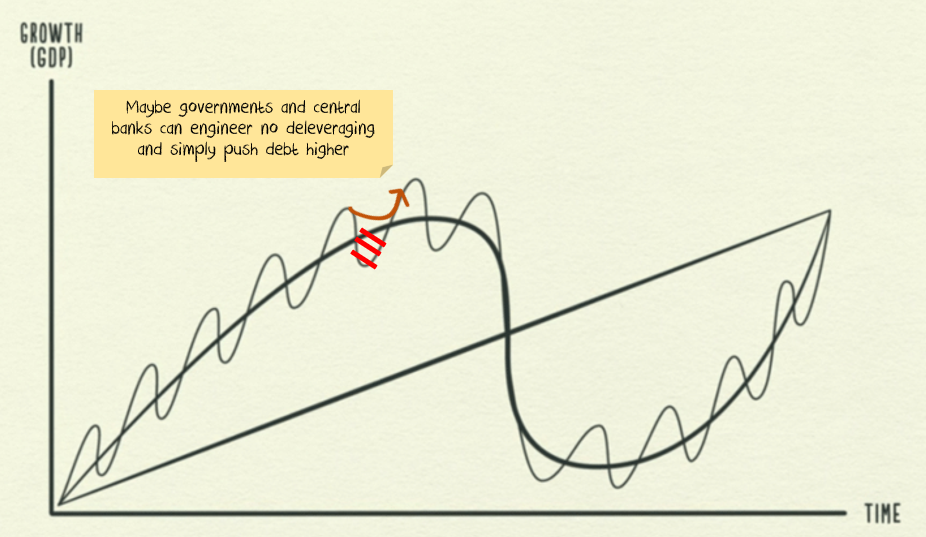

Governments and central banks to the rescue

Swift intervention by central banks and governments hit pause on the start of deleveraging. In effect they threw a lot of money at the economy, most ended up cushioning the blow for people who suffered from the shutdown. But a significant amount also ended up with people who didn’t suffer. Also, without travel, many more affluent people travelled less and consequently increased their saving and investment.

Also, evictions and bankruptcies were made more difficult, and interest-rate holidays on loans given. The new rules prevented negative outcomes while encouraging positive ones. The stock market boomed.

Is capitalism finished?

We have been cautious on risk for months, avoiding the crisis at the start, but with minimal participation in the market recovery. And, to date, we have been wrong. We did identify the most likely reason to be wrong would be if governments would take ever more extreme steps to cancel capitalism. And that is what happened.

In many countries, “extend and pretend” has replaced the threat of bankruptcy. Someone who can’t pay their rent is not evicted but allowed to accrue debt. Don’t foreclose on those who can’t pay their interest. Instead, build up their interest payments into a larger debt burden.

The end game seems to be a cohort of zombie consumers and businesses. Weighed down by debt burdens too massive to ever pay off, but supported by interest rates low enough to keep them from defaulting.

US Treasury Secretary Mnuchin is letting several minor lending programs expire at the end of the year, to the loud complaints of many – including the US central bank. Many programs will likely be re-instated once Biden is in power. In other countries, there is very little consideration given to finishing similar programs.

It would seem we have a zombie future.

Can the debt cycle blast higher?

The question from here is whether a new debt boom can be launched without the old one ever having peaked.

Until recently, I thought the odds favoured the end of the cycle. I was wrong.

I’m still sceptical of a debt boom for businesses. Governments and central banks will try, but debt levels are already high and further interest rate reductions will be limited.

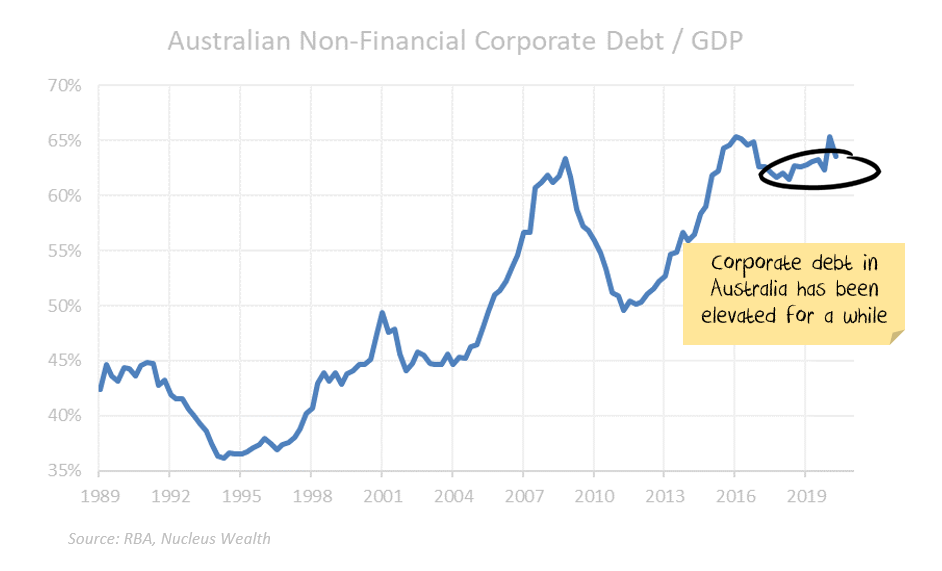

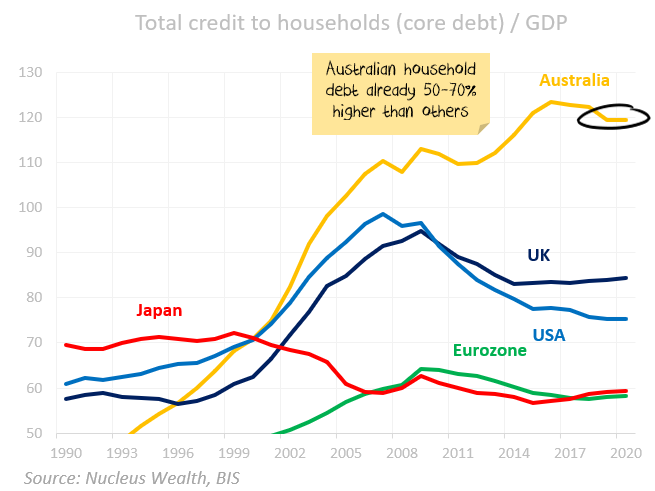

Another household debt boom is possible. Although Australia has already played this card:

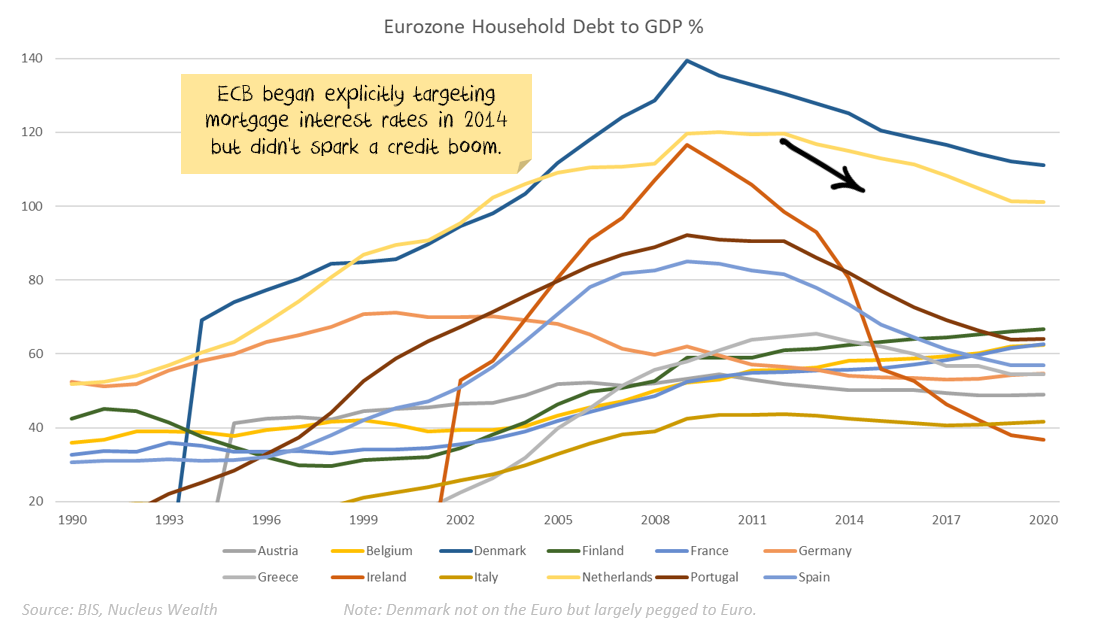

The other difficulty is that despite the European Central Bank’s best efforts, household debt has been declining across much of the Eurozone.

The most likely outcome now appears to be continued increases in government debt, but limited increases in corporate debt. Household debt is an open question.

Are we reduced to watching governments and central banks?

Mostly. It seems clear that policymakers have decided on zombification. Limit bankruptcies. Increase debt. Never raise interest rates again.

It doesn’t make for a healthy economy. But it limits short term pain which appears to be the current goal of every politician.

The economic plan is to try to get a debt-funded consumer boom going so that bankruptcy protection and consumer support can be removed.

Policy mistakes are what matters from here. The goal? Prevent a business cycle from occurring.

Indications that a normal business cycle is occurring will be a sign to sell. Too much support and markets will grind higher.

Damien Klassen is Head of Investments at Nucleus Wealth.

An edited edition of the live Q&A as I discuss the challenges of investing in the current climate with Damien Klassen, Head of Investments and Tim Fuller, Head of Advice, at Nucleus Wealth. https://walktheworld.com.au/

Original version with live chat here:https://youtu.be/IV-Ev2Sriqw

Go to the Walk The World Universe at https://walktheworld.com.au/

Digital Finance Analytics (DFA) Blog

DFA Live Q&A HD Replay: Investing In An Uncertain World [Podcast]

Join us for a live discussion on investing in the current environment. I will be joined by Damin Klassen and Tim Fuller from Nucleus Wealth. You can ask as question live via the YouTube Chat.

What are the forces pulling the market higher, versus lower, and which will likely win out?

Investment markets have a host of both positive and negative factors fighting for supremacy. The real question is whether central banks and governments will engineer a continued suspension of capitalism. I was sceptical six months ago. I’m less sceptical now that capitalism will return anytime soon. On balance, however, there is still plenty of room for caution.

Short-term government policies to suspend capitalism (increased hurdle for bankruptcies, mortgage holidays, eviction moratoriums, banks not recognising bad debts, etc.) have morphed into medium-term policies. And, it is hard to see any government ready to exit. There is a quiet extension to each policy that lapses.

We took advantage of pre-election weakness to increase our risk exposure a little. But given the rise in markets since the election, the positive factors have mostly been reflected already. And, the positive factors tend to be short-term, the negative aspects tend to be medium-term.

Key positive factors for share prices

Government stimulus: Global governments continue to add stimulus. The US has some question marks, and the stimulus won’t be as large as if Biden won Senate majority. But it would seem additional stimulus is highly likely.

Low probability of US tax hikes: Subject to the Georgia senate run-offs, it looks unlikely the US Senate will pass Biden’s company tax rate increases. If passed, these would have reduced US earnings by around 10%.

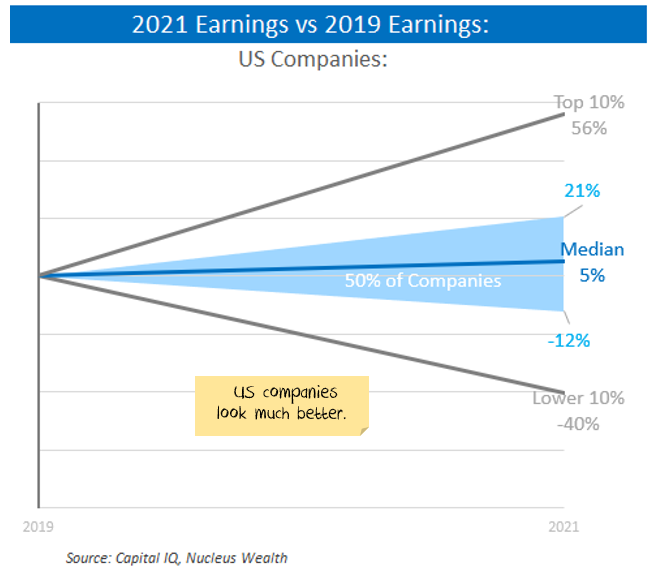

Earnings very good: 3rd quarter earnings were much better than expected. Analyst forecasts haven’t changed much, but that is better than usual! Typically, later year forecasts are far too optimistic and get revised down as they get closer. Forecast growth is 24% for 2021 and then 15% for 2022.

Inequality to remain high: No changes to taxes in the US = economic inequality likely to remain high. In Australia, there are tax cuts for the rich, reduced support for the poor. Travel limitations depressing spending for the rich. Plus stimulus tends to be relatively indiscriminate; some ends up in the right hands, some in the hands of those that don’t need it. Net effect: the rich have more money to put into investment markets.

Other positive factors for share prices

Bankruptcies, evictions limited: in many countries bankruptcies are down 30%+, driven by a mix of stimulus and rule changes. Businesses feel richer if they haven’t had to write down bad debts. Not fixing the problem, just delaying the pain.

Mortgage repayment holidays: as above.

Wage growth very low: helpful to company profits.

Productivity: forced change/digitisation often results in better outcomes. Having to fire staff usually results in the least productive going first, increasing overall company productivity.

Low oil prices: keeping transport costs down.

Vaccine hope: successful trials give hope to an end of the virus.

Policy certainty: President Biden is far less likely than Trump to be unpredictable.

Key negative factors for share prices

COVID in the Northern Hemisphere: It is ripping through populations. Importantly, hospitals are reaching capacity, which means lockdowns have begun again in Europe and seem highly likely in the US.

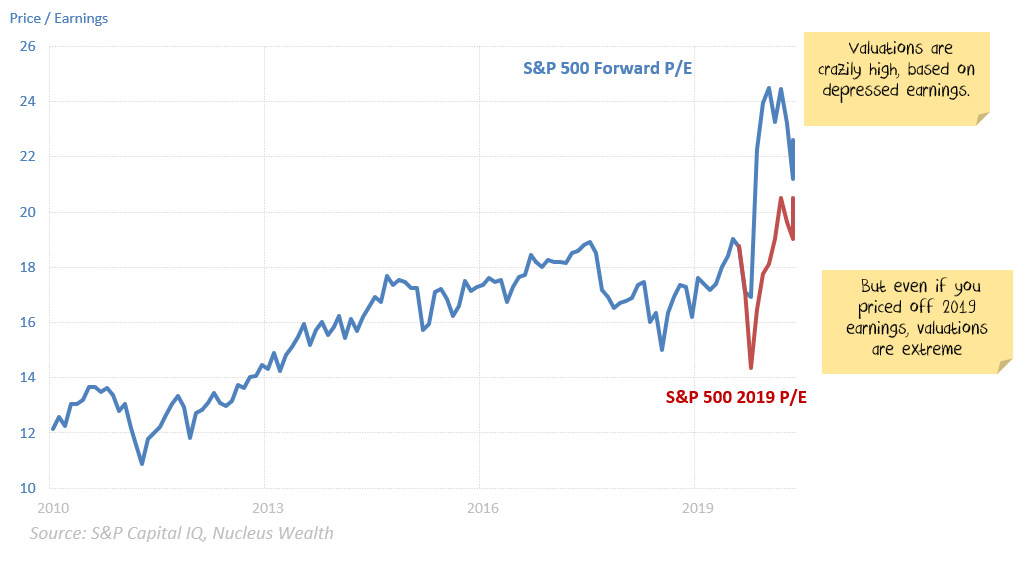

Valuation: Share market valuations are extraordinarily high.

Latent bankruptcies: Changing the rules so that companies and individuals who are otherwise bankrupt are allowed to increase their debt does not fix the problem. It also runs the risk that the bad actors not paying their bills start to pull down the good actors.

Low genuine credit growth: credit growth has been poor; banks are still tightening lending standards. But the credit growth also includes mortgage holidays. And companies borrowing to survive rather than to make productive investments. Which means genuine credit growth is lower than the already weak headline numbers. Economic growth has been tied at the hip to credit growth for the last decade. It is difficult to see what will replace easy money as the only thing holding economic growth up.

Other negative factors for share prices

Short term gap in US economic conditions: There may not be stimulus until Biden takes power. If so, there are three months with limited government support while the virus sets new records. This might be enough to tip the economy into a funk and result in more job losses.

Inequality longer-term effects: the short term effect of increased inequality increases savings and investment and (probably) increases stock market valuations. The longer-term impact is depressed demand and profits. And more political upheaval.

Structural change: leading to weak demand, higher unemployment. There are industries like travel and tourism which will have to deal with lower sales and employment. The means job losses continue as former employees have to give up on finding a job and retrain for a new industry.

Net effect

It bears repeating: the positive factors for investment markets tend to be short-term, the negative ones medium-term. Will there be “clear air” for a few months before the consequences begin? Maybe. The stock market has had a lot thrown at it and is still holding up.

On the flip side, the risks are not symmetrical. The upside appears more limited than the downside.

Damien Klassen is Head of Investments at Nucleus Wealth.

I caught up with Damien Klassen Head of Investments, at Nucleus Wealth to discuss their investment strategy in the current uncertain climate – ahead of some important announcements coming later in the week.

Finally some of the commentators are seeing though the Government spin to the underlying ideology, and are highlighting the weaknesses and risks in the massive proposed spending. And it’s not so much the quantum, as the direction of fire…

This is the edited edition of our latest live stream with Damien Klassen.

Join us for a live Q&A as I discuss the current market environment with Damien Klassen from Nucleus Wealth. We will also discuss their property calculator, which I think is one of the best out there.

Blog")