NAB says two new innovative Good Money community finance stores will respond to the increasing need for access to fair and affordable financial services for Queenslanders on low incomes.

The Queensland Government is supporting the Good Money stores which will be in Cairns and on the Gold Coast. The stores are a three-way partnership involving financial inclusion organisation, Good Shepherd Microfinance, the National Australia Bank (NAB) and the Queensland Government.

Adam Mooney, Chief Executive Officer of Good Shepherd Microfinance said that he was excited to see the expansion of Good Money to a third state – building on the existing three stores in Victoria and one in South Australia.

“Good Money provides access to the award-winning No Interest Loan Scheme (NILS) which provides small loans upto $1,200 for essential goods and services such as fridges, washing machines or car repairs,” said Mr Mooney.

“We’ve been experiencing increasing enquiries from Queenslanders for our services and these two new stores will strengthen the footprint of NILS across the state, complementing the work of the Queensland NILS network which has a presence in around 115 locations.

“The financial conversations our microfinance workers have with clients positively builds confidence and focuses on the best options available. More than 90 per cent of clients feel they’re better able to budget after speaking with Good Money, and 50 per cent of clients who had previously used high cost payday loans said they’d avoid them in the future.

“The Queensland Government is showing national leadership in investing in financial inclusion to build community and family resilience. This is a wonderful new initiative as part of the Queensland Government’s commitment to its Financial Inclusion Action Plan, announced on Thursday this week,” he said.

NAB, a key partner in the development of the Good Money model first introduced in 2012, has committed $130 million in loan capital to microfinance programs nationally.

Michaela Healey, Group Executive – Governance and Reputation at NAB said the bank had a long history of contributing skills, expertise and resources to improving financial inclusion in Australia.

“NAB is committed to financial inclusion – but we realise we can do so much more when we work together with others. Good Money is a great example of what can be achieved when a bank, government and community organisation make a long-term commitment and come to the table with an open mind and a willingness to work together,” said Ms Healey.

“Over the past 11 years NAB has provided more than 138,000 products to help more than 421,000 low-income Australians access appropriate and affordable financial services. The extension of Good Money stores into Queensland is an exciting development that will make the stores’ vital products and services readily accessible to Queenslanders for the first time,” she said.

Communities Minister Shannon Fentiman said battling financial distress can take a heavy toll on health and relationships.

“Quite often people seek solutions that land them even deeper in debt,” she said.

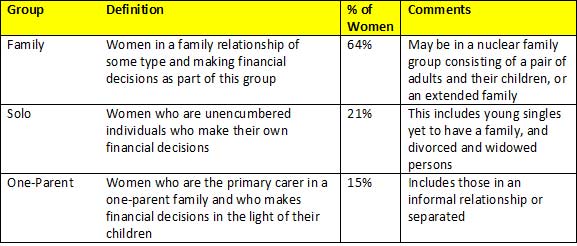

“These stores will provide real alternatives to unscrupulous payday lender and rent-to-buy schemes to make sure people don’t spiral into debt – especially women, who are the fastest growing demographic accessing payday loans,” said Minister Fentiman.

The Good Money stores will offer the following services:

- No Interest Loan Scheme (NILS) – Loans of between $300 – $1,200 for essential goods and services such as fridges, washing machines or education expenses

- StepUP Loans – Low interest loans of between $800 – $3,000 with no fees and affordable repayment periods

- AddsUP – A matched savings plan of up to $500 offered to people who have successfully repaid a NILS or StepUP loan

- Affordable insurance – Simple car and contents insurance with flexible payment options

- Referrals to other services – Such as financial counselling which provides information and support to assist people in financial difficulty

It is envisaged that the stores will open for business in 2017.

Good Shepherd Microfinance’s national NILS program is also offered through local community organisations in 115 sites across Queensland.