Yesterday morning, several banks in Australia started rolling out a new payment system they’re calling NPP, or “New Payments Platform.”

Until now, sending a domestic funds transfer in Australia from one bank to another could take several days. It was slow and cumbersome.

With NPP, payments are nearly instantaneous.

And rather than funds transfers being restricted to the banks’ normal business hours, payments via NPP can be scheduled and sent 24/7.

You can also send money via NPP to mobile phones and email addresses. So it’s a pretty robust system.

Across the world in the United States, the domestic banking system has been working on something similar.

Domestic bank transfers in the Land of the Free typically transact through an electronic network known as ACH… another slow and cumbersome platform that often takes 2-5 days to transfer funds.

It’s pretty ridiculous that it takes more than a few minutes to transfer money. It’s 2018! It’s not like these guys have to load satchels full of cash onto horse-drawn wagons and cart them across the country.

(And even if they did, I suspect the money would reach its destination faster than with ACH…)

Starting late last year, though, US banks very slowly began to roll out something called the Real-time Payment system (RTP), which is similar to what Australian banks launched yesterday.

[That said, the banks themselves acknowledge that it could take several years to fully adopt RTP and integrate the new service with their existing online banking platforms.]

And beyond the US and Australia, there are other examples of banking systems around the world joining the 21st century and making major leaps forward in their payment system technologies.

It seems pretty clear they’re all playing catch-up with cryptocurrency.

The rapid rise of Bitcoin and other cryptocurrencies proved to the banking system that it’s possible to conduct real-time [or near-real-time] transactions, and not have to wait 2-5 days for a payment to clear.

Combined with other new technologies like Peer-to-Peer lending platforms, fundraising websites, etc., consumers are now able to perform nearly every financial transaction imaginable– deposits, loans, transfers, etc.– WITHOUT using a bank.

And it’s only getting better for consumers… which means it’s only getting worse for banks.

All of these threats from competing technologies have finally compelled the banks to innovate– literally for the FIRST TIME IN DECADES.

I’m serious.

When the CEO of the company launching RTP in the US announced the platform, he admitted that the “RTP system will be the first new payments system in the U.S. in more than 40 years.”

That’s utterly pathetic. The Internet has been around for 25 years. Even PayPal is nearly 20 years old.

Yet despite the enormous advances in technology over the past several decades, the last major innovation in bank payments was back when Saturday Night Fever was the #1 movie in America.

Banks have been sitting on their laurels for decades, enjoying their monopoly over our savings without the slightest incentive to improve.

Cryptocurrency has proven to be a major punch in the gut. The entire banking system keeled over in astonishment over Bitcoin’s rise, and they’ve been forced to come up with an answer.

And to be fair, the banks have reclaimed the advantage for now.

NPP, RTP, and all the other new protocols are faster and more efficient than most cryptocurrencies.

Bitcoin, for example, can only handle around 3-7 transactions per second. Ethereum Classic maxes at around 15 transactions per second. Litecoin isn’t much better.

By comparison, there were 25 BILLION funds transfers in 2016 using the ACH network in the US.

Based on the typical holiday schedule and the banks’ 8-hour working days, that’s an average “throughput” of roughly 3500 transactions per second.

So, now that banks have finally figured out how to conduct thousands of transactions per second in real-time, they clearly have superiority.

But that superiority is unlikely to last.

It takes banks decades to innovate. They have enormous bureaucratic hurdles to overcome. They have endless committees to appease, including the Federal Reserve’s “Faster Payments Task Force.”

And most importantly, given that most banks are still using absurdly antiquated software, any new systems they develop have to be carefully designed for backwards compatibility.

Cryptofinance and other financial technology companies have no such limitations.

As my colleague Tama mentioned in the podcast we released yesterday, the cryptocurrency space sort of exists in ‘dog years’.

Things move so quickly that one year in crypto is like 7 years for any other industry.

Right now there is almost a unified push across the crypto sector to solve the ‘scalability’ problem, i.e. to securely transact a near limitless number of transactions in real time.

Those solutions will almost undoubtedly come from technologies that you haven’t heard very much about yet.

Hashgraph and Radix, for example, are two such ventures working on extremely elegant payment solutions that break the mold of previous cryptos.

Rather than build upon standard cryptocurrency concepts like blockchain, Proof of Work, and Proof of Stake, both Hashgraph and Radix have created their own algorithms from scratch.

This is the bleeding edge of the bleeding edge of a massively disruptive sector that has existed for less than a decade.

And there are literally dozens of other companies and technologies aiming for similar heights.

Some of them will undoubtedly succeed. And still other ventures that won’t even be conceived for years will have yet more disruptive power in the future.

The banks don’t stand a chance. The future of finance absolutely belongs to crypto.

Will the future of digital money be cardless, as mobile devices pick up the slack? Well, perhaps not as Visa demonstrates a new Internet of Things (IoT) device which holds multiple payment cards and includes a digital display allowing for greater security, instant issuance and on-card alerts or coupons. Innovation, or the last gasp from “old” technology?

LAS VEGAS–(BUSINESS WIRE)–Jan. 8, 2018– Visa and Dynamics today unveiled the Dynamics Wallet Card™, a connected payment card, at the 2018 Consumer Electronics Show (CES). The Visa-branded version of the Wallet Card is the same size and shape as a normal Visa credit or debit card, yet it incorporates multiple features and technologies not previously found in a single payment card. Features of the Wallet Card range from the capacity to access multiple cards – whether EMV-, contactless- or magnetic stripe-based – to a programmable on-card display that enables account information, such as alerts or coupons, to be sent to the cardholder via an embedded antenna.

“Innovation in the payments category is not limited to wearables, cars, security or mobile technology – there is still much that can be done to update the card-based experience, which continues to be the primary form factor used globally to complete digital payments transactions,” said Mark Nelsen, senior vice president of risk and authentication products, Visa. “Having collaborated with Dynamics since they launched their first product several years ago, we’re excited about the many unique benefits that the Visa Wallet Card can offer to both financial institutions and cardholders, alike.”

Wallet Card includes a cell phone chip and cell phone antenna so data can be transferred between Wallet Card and a consumer’s bank anywhere in the world and at any time of the day.

The device offers a number of cardholder benefits and cutting-edge technologies, including:

Multiple Cards in One: Cardholders can access their debit, credit, pre-paid, multicurrency, one-time use, or loyalty cards on a single card with the tap of a button. Account information is shown on the on-card display with the ability to toggle between cards or accounts.

Instant Issuance: As the first instant, digital card platform, financial institutions can distribute Visa Wallet Card anywhere and at any time – such as in their retail branches or at events, and consumers can activate it right away.

Greater Security: A bank can quickly delete a compromised card account number and replace it with a new account number, providing convenience and peace of mind for the cardholder.

Alerts and Messages: An on-card, 65,000-pixel display shows both account information and allows messages to be sent to the Visa Wallet Card at any time. For example, after every purchase, a message may be sent to notify the consumer of the purchase and their remaining balance if they used a pre-paid or debit card. Cardholders can also receive coupons directly on the display or be notified of a suspicious purchase and click on “Not Me” to report suspected fraud and request a new card number.

Self-Charging Battery: An organic chip ensures the payment card charges itself through normal operation and doesn’t require any work for the cardholder.

“Visa supported the initial launches of Dynamics first- and second-generation powered cards which brought new functionality to payment cards,” said Jeffrey Mullen, CEO of Dynamics Inc. “Today, we are pleased to again have Visa by our side as an integral partner and thought leader as we launch Wallet Card, our most innovative payment card to-date.”

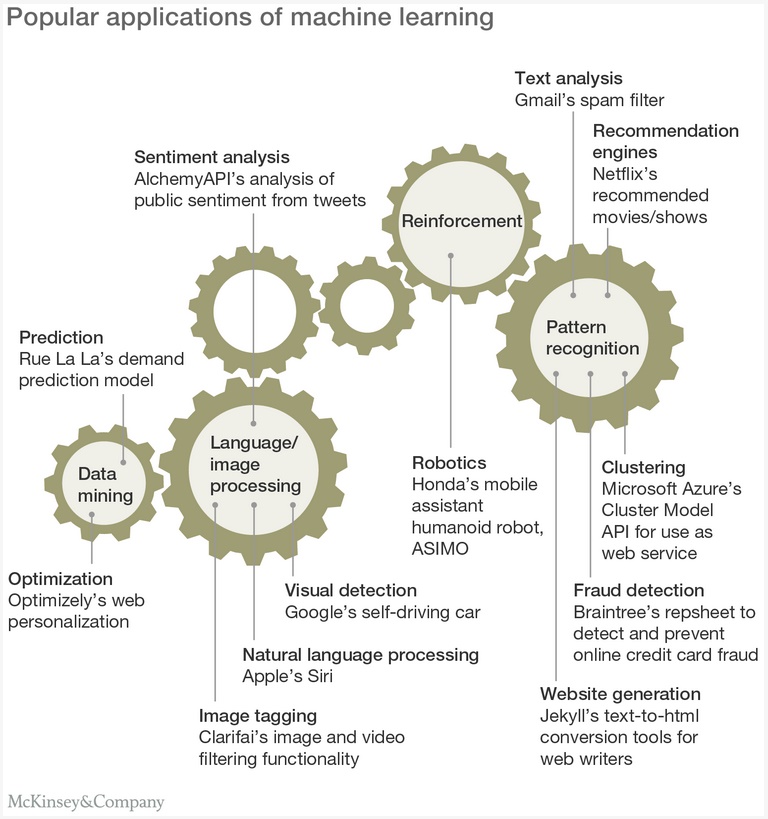

Good article from McKinsey on the revolution catalysed by the combination of machine learning and new payment systems as part of big data. The outline some of the opportunities to expand the use of machine learning in payments range from using Web-sourced data to more accurately predict borrower delinquency to using virtual assistants to improve customer service.

Machine learning is one of many tools in the advanced analytics toolbox, one with a long history in the worlds of academia and supercomputing. Recent developments, however, are opening the doors to its broad-scale applicability. Companies, institutions, and governments now capture vast amounts of data as consumer interactions and transactions increasingly go digital. At the same time, high-performance computing is becoming more affordable and widely accessible. Together, these factors are having a powerful impact on workforce automation. McKinsey Global Institute estimates that by 2030 47 percent of the US workforce will be automated.

Payments providers are already familiar with machine learning, primarily as it pertains to credit card transaction monitoring, where learning algorithms play important roles in near real-time authorization of transactions. Given today’s rapid growth of data capture and affordable high-performance computing, McKinsey sees many near- and long-term opportunities to expand the use of machine learning in payments. These include everything from using Web-sourced data to more accurately predict borrower delinquency to using virtual assistants to improve customer service performance.

Machine learning: Major opportunities in payments

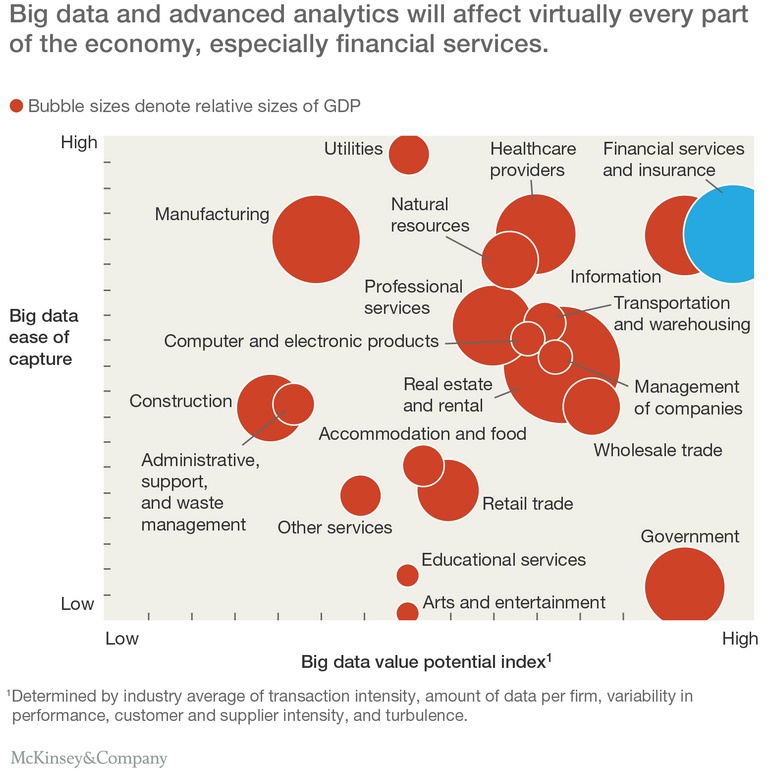

Rapid growth in the availability of big data and advanced analytics, including machine learning, will have a significant impact on virtually every part of the economy, including financial services (exhibit). Machine learning can be especially effective in cases involving large dynamic data sets, such as those that track consumer behavior. When behaviors change, it can detect subtle shifts in the underlying data, and then revise algorithms accordingly. Machine learning can even identify data anomalies and treat them as directed, thereby significantly improving predictability. These unique capabilities make it relevant for a broad range of payments applications.

What is machine learning?

Machine learning is the area of computer science that uses large-scale data analytics to create dynamic, predictive computer models. Powerful computers are programmed to analyze massive data sets in an attempt to identify certain patterns, and then use those patterns to create predictive algorithms (exhibit). Machine learning programs can also be designed to dynamically update predictive models whenever changes occur in the underlying data sources. Because machine learning can extract information from exceptionally large data sets, recognize both anomalies and patterns within them, and adjust to changes in the source data, its predictive power is superior to that of classical methods.

Machine learning has already established a strong foothold in credit cards, particularly in fraud management. PayPal’s Braintree Auth payments tool, for example, uses PayPal’s consumer transaction data in conjunction with software developer Kount’s fraud detection capabilities to authorize high volumes of transactions and verifications in near real-time. Each credit card transaction or verification is analyzed in milliseconds using hundreds of fraud detection tests.

There are several other areas in the payments value chain where machine learning is adding significant value:

Product sales: Machine learning can be a powerful tool for developing deeper insights about customers and sales prospects because it can draw upon a wider variety of internal and external data than marketers have traditionally used. It can more accurately cluster customers and prospects into segments according to their profiles and probable needs. This deeper insight can reveal new opportunities for cross-selling and up-selling among both customers and prospects. McKinsey finds that with machine learning payments providers can increase revenue from existing customers by 10 to 15 percent.

Customer retention: Companies typically monitor and forecast customer churn based on changes in account status; when churn rates rise they take steps to address the problem. Now, through machine learning, they can identify those customers they are at risk of losing and act quickly to retain valuable customers. For example, 47Lining, an Amazon Web Services partner, uses a combination of site behavior, demographics, and media-sentiment measures to predict customer churn with 71 percent accuracy. Companies using machine learning to address customer churn have achieved reductions of as much as 25 percent.

Collections: Collection practices and debt restructuring work best when closely aligned with borrowers’ changing circumstances and propensity to pay. Machine learning can help companies build robust dynamic models that are better able to segment delinquent borrowers, and even identify self-cure customers (that is, customers that proactively take action to improve their standing). This enables them to better tailor their collection strategies and improve their on-time payment rates. TrueAccord’s HeartBeat, for instance, is a machine learning tool that helps lenders customize personal interactions in real time, based on its ability to detect why a customer’s payments are late. Companies using machine learning have been able to reduce their bad debt provision by 35 to 40 percent.

Treasury pricing: In commercial payments, companies can capture 10 to 15 percent more revenue through optimized treasury pricing. In the near term, advanced analytics can identify quick-win opportunities to reduce price leakage (such as discounts exceeding authorized limits) and billing errors. Over the long term, clustering techniques built on machine learning can significantly improve customer segmentation and lead to more appropriate pricing models.

Customer care: Over time, McKinsey expects to see a gradual increase in the automation of many customer services. This is an area in which the cognitive intelligence capabilities of machine learning are particularly well suited. Among the benefits are: lower servicing costs, enhanced agent performance, more efficient capacity management, improved digital customer experience, reduced risk, and elimination of waiting times. A variety of relevant applications are already available, including virtual assistants that use natural language processing, deep insight tools like IBM’s Watson, and cognitive engines that can do things presently handled by humans, such as IPSoft’s Amelia, which can understand and interact with people (see sidebar, “Cognitive agents”).

Machine learning in the card collection environment

Cognitive agents

Cognitive agents like IPSoft’s Amelia combine natural language and deep insight technologies to complete tasks typically handled by humans. Using a three-step process, they help companies intelligently automate a variety of tasks:

Understand: Cognitive agents can rapidly absorb and comprehend a diverse range of data sets, from complex manuals to call logs and flow charts.

Learn: Cognitive agents absorb data from the customer language they process, and can refer the customer to a live agent language they process, and can refer the customer to a live agent when uncertain about how to react. They also learn from cases they refer to agents, further improving effectiveness as they continue to record interactions and data.

Resolve: Finally, cognitive agents can directly resolve customer inquiries received through online chat, mobile, and voice channels. Alternatively, when connected to a backend system they can support live agents in resolving customer issues.

Service automation tools can help payments providers increase customer satisfaction, enhance financial performance, and improve compliance.

In card issuing, machine learning is already having a valuable impact. This is especially true in collections, where McKinsey has seen 10 to 15 percent improvements in recovery rates and 30 to 40 percent increases in collections efficiency. To minimize delinquencies, issuers can use individual-account pattern recognition technologies, and develop contact guidelines and strategies for accounts that are already delinquent. Following an account delinquency, issuers allow a brief time window (usually 90 days) before they write off the receivables and turn collection over to third-party providers. This brief period is an ideal time for issuers to apply collection strategies that draw heavily on the capabilities of machine learning.

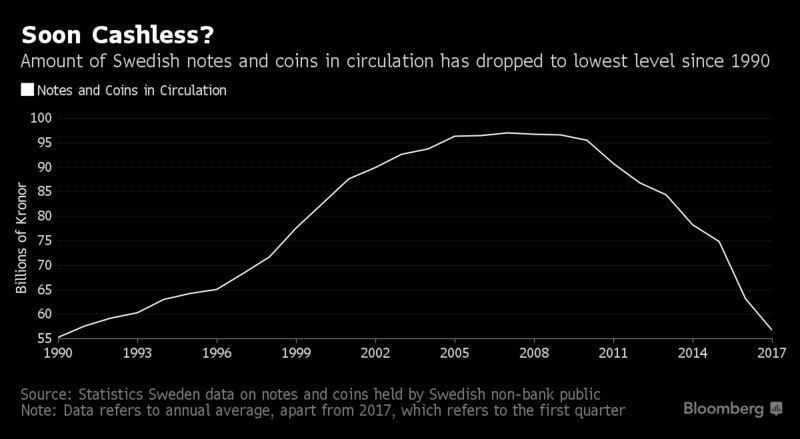

In the most cashless society on the planet, even God now accepts digital payments.

A growing number of Swedish parishes have started taking donations via mobile apps. Uppsala’s 13th-century cathedral also accepts credit cards.

The churches’ drive to keep up with the times is the latest sign of Sweden’s rapid shift to a world without notes and coins. Most of the country’s bank branches have stopped handling cash; some shops and museums now only accept plastic; and even Stockholm’s homeless have started accepting cards as payment for their magazine. Go to a flea market, and the seller is more likely to ask to be paid via Sweden’s popular Swish app than with cash.

“Fifteen years ago I would withdraw my entire salary and put it in my wallet, so I knew how much I had left, but these days I never really carry cash,” said Lasse Svard, the acting vicar at the parish of Jarna-Vardinge, about 50 kilometers (31 miles) south of Stockholm.

Vanishing Act

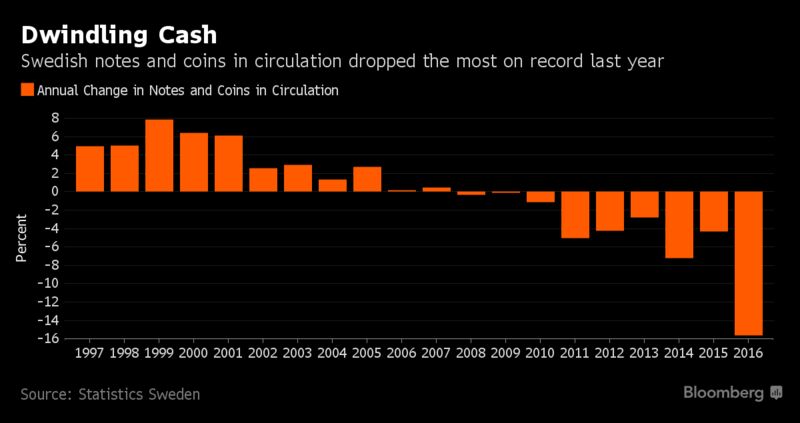

Swedes’ aversion to cash is increasingly showing up in money supply data. According to Statistics Sweden, notes and coins in public circulation dropped to an average of 56.8 billion kronor ($6.4 billion) in the first quarter of this year. That was the lowest level since 1990 and more than 40 percent below its 2007 peak with the pace of the decline accelerating to its fastest ever in 2016.

According to the central bank, which is also studying whether to launch its own digital currency, the main reason for the disappearing act is technical innovation.

Riksbank Deputy Governor Cecilia Skingsley notes that Swedes were early adopters of both personal computers and mobile phones (remember those Ericsson phones?), and that the country’s banks were quick to create sector-wide structures such as debit cards, credit cards and Swish, which has 5.5 million users and is owned by the country’s largest banks. Swedes also seem to trust those systems, she said in a recent interview in Stockholm.

Innovation Drive

“A drive for innovation has been created in Sweden to come up with cost-effective and user-friendly alternatives to cash,” Skingsley said. Cash is likely to “more or less disappear” as a means of payment in the private sector, she said.

But a cashless society is not without its challenges or critics.

Many pensioners are struggling to make payments in an online world, while privacy campaigners lament the fact that the state is acquiring greater control over what its citizens do. There are also concerns about the vulnerability of a cashless society in the event of an attack or major blackouts.

It seems that for now, the benefits — including lower business costs, more control over tax revenue and greater safety from criminals — outweigh the drawbacks.

Policy Impact

In fact, Swedes have become so averse to cash that they’ve even been shunning it during the current regime of negative interest rates.

“The fact that people chose to hold so little cash in their wallets despite getting zero interest on their bank accounts emphasizes the strength of this trend even more,” Robert Bergqvist, chief economist at SEB AB, said by phone.

So far, the development has had little impact on monetary policy. But if cash were to disappear entirely, it would give extra powers to the central bank.

“Negative interest rates would be more powerful as there wouldn’t be any way to escape their impact,” Bergqvist said. “In a sense it would give the Riksbank more room for maneuver.”

Niklas Arvidsson, a researcher in industrial economics and management at KTH, says that the widespread and growing embrace of the mobile payment system, Swish, is helping hasten the day when Sweden replaces cash altogether.

“Cash is still an important means of payment in many countries’ markets, but that no longer applies here in Sweden,” Arvidsson says. “Our use of cash is small, and it’s decreasing rapidly.”

In a country where bank cards are routinely used for even the smallest purchases, there are less than 80 billion Swedish crowns in circulation (about EUR8 billion), a sharp decline from just six years ago, when the total in circulation was SEK106 billion.

“And out of that amount, only somewhere between 40 and 60 percent is actually in regular circulation,” he says. The rest is socked away in people’s homes and bank deposit boxes, or can be found circulating in the underground economy.

The result of collaboration between major Swedish and Danish banks, Swish is a direct payment app that is used for transactions between individuals, in real time. The service’s direct collaboration with Bankgiro and Sweden’s national bank, Riksbanken, is a critical factor in its success.

But if Swish starts to be used on a larger scale and grows to include retail transactions and e-commerce, Arvidsson says it is likely the country’s entire payment system infrastructure will have to be revamped.

That may not be as prohibitive an idea as it sounds. Arvidsson says Swish is already revolutionizing the banking system, which itself is no stranger to bold digital projects.

With digital giro systems, early electronic payment services and other advances in online financial services, Swedish banks have been early adopters of advanced IT systems, he says.

“Combined with a strong IT sector, this has led to more competitive financial services in Sweden. The success also depends on the Swedish consumer tradition of welcoming electronic payment services.”

Besides simplicity and lower costs, digital payments also add transparency to the nation’s payment system. Several banks in Sweden already have 100 percent digitalized branches that will simply not accept cash.

“At the offices which do handle banknotes and coins, the customer must explain where the cash comes from, according to the regulations aimed at money laundering and terrorist financing,” he says. Bank staff are required to file police reports in response to suspicious cash transactions.

In spite its popularity, Sweden will still have to ensure that all people are able to participate in the new payment system, Arvidsson says. The transformation would present serious challenges for those who are unfamiliar with computers and mobile phones — mainly older people living in rural areas.

Other segments of the population likely to feel the impact are the homeless and undocumented immigrants. In a society without notes and coins, they will be even more at the mercy of government systems to survive.

Whether cashless societies spread beyond Sweden is another question. “Swish is a brilliant idea, but to introduce it internationally is a challenge, not least because it takes a long time to change other countries’ banking systems from scratch. But it is not impossible that a Swish-based banking revolution can also occur abroad,” Arvidsson says.

Tony Richards, Head of Payments Policy, RBA, spoke at the APCA Australian Payments 2015 Conference today. He gave an update on current payment initiatives in Australia, including NPP, payments coordination, and the interchange regime. He also mentioned the outcomes from the FSI.

The first is the initiatives that came out of the 2012 conclusions of the Reserve Bank’s Strategic Review of Innovation in the Payments System. The background to the Review was a growing amount of evidence that the services provided to end-users of the Australian payments system were falling behind the services available to end-users in some other countries.

The most prominent outcome of the Review was that the Bank asked the payments industry to consider ways of filling the gaps in the payments system that had been identified in the Review. As you know, the industry – coordinated by APCA – proposed a project, which has been developed over the past three years, to build some new industry infrastructure which will be called the New Payments Platform (NPP). The NPP will deliver real-time, data-rich payments to end-users on a 24/7 basis. It will also be a platform for all sorts of other innovative services, many of which we cannot yet imagine.

The Bank has been heavily involved in this project. It is one of the 12 financial institutions that have agreed to fund the build of the NPP and to connect to it when it goes live. The Bank is also developing a new service, the Fast Settlement Service (FSS), which will provide real-time settlement of NPP transactions. My colleagues in Payments Settlements Department are making good progress on the FSS.

Paul Lahiff, the Chair of NPP Australia Ltd, will be speaking to you in more detail about the status of the NPP, but I can tell you that the Payments System Board (the Board), having encouraged this project, has been taking a close interest in it and has been pleased by the excellent collaboration in the industry.

Another initiative coming out of the Strategic Review of Innovation was that the Bank called for the establishment of an enhanced industry coordination body. The intention was that this should take a more strategic view than existing industry governance bodies and have membership from a wider range of institutions than had traditionally been the case for APCA. It was also to have high-level representation, with individuals who are more able to commit their organisations to courses of action agreed by the group.

The rationale for this focus on industry governance was that the identified gaps in the services offered to end-users partly reflected difficulties in getting the industry to work together to develop the cooperative elements of payment systems. The development of common rules, standards, communications networks and other infrastructure sometimes requires collaborative innovation, where institutions have to work together. There was a concern that this had previously proved difficult in Australia.

I’m happy to say that there has been good progress here. The Australian Payments Council held its first meeting in late 2014 and – as you will have heard in the first session today – has recently been consulting on an Australian Payments Plan, seeking views on long-term trends, systemic challenges and desirable characteristics for the payments system.

The first meeting between the Board and the Council occurred in August. The Board is looking forward to seeing the progress that the Council makes on its payments plan. The Council may be a useful vehicle for the payments industry, including the Bank, to think about some of our legacy payment systems, in particular the future of the cheque system.

Fraud, digital identity and cyber security are other areas where there could be real benefits to industry collaboration. Of course, they are not just issues for the payments system. Cyber security and digital identity were referred to in the Government’s response to the Financial System Inquiry (FSI) Report and are issues that touch the entire financial system and, indeed, the broader economy.

The second issue I would like to cover is the Bank’s ongoing Review of Card Payments Regulation.

In its March 2014 submission to the FSI, the Bank indicated that it would be reviewing some aspects of the regulatory framework for card payments. The Final Report of the FSI, which was released in December 2014, endorsed the broad nature of the Bank’s reforms over the past decade or more but noted a few areas where the Inquiry believed the existing framework could be improved. The Bank released an Issues Paper in March 2015, inviting submissions on a broad range of issues in card payments regulation, including those raised in the FSI Report. I will touch on four of these issues.

The first is the growing lack of transparency of payment costs to many merchants. While interchange fees on credit and debit cards are currently subject to benchmarks that must be observed every three years, there has been a tendency for the two large international four-party schemes to promote new, high-interchange, high-rewards cards. At the same time, they have introduced lower interchange rates for ‘strategic’ or other preferred merchants. These merchants get the same low interchange rate – for credit cards, as low as 20 basis points – on all their transactions, even if a super-premium, high-rewards card is presented. But smaller merchants and others who do not benefit from strategic rates pay interchange rates of up to 200 basis points on their transactions. Furthermore, when presented with a card, such merchants may have no way of knowing if it is a card with a 30 basis point interchange rate or a 200 basis point rate. So the issues that we have raised are the growing lack of transparency of payment costs for many merchants and the growing wedge in average payment costs between preferred and nonpreferred merchants.

Second, the Bank is consulting on whether it would be desirable to lower the interchange benchmarks or to make other changes to the system, such as to have more frequent compliance. One issue here is that the behaviour of schemes and issuers under the current three-yearly compliance system is seeing average interchange rates rising significantly above the benchmark in between compliance dates.

The third issue is whether it would be desirable to extend the coverage of the regulatory framework for interchange payments. This is especially relevant in the case of companion cards – in particular, bank-issued American Express cards, which have issuer fees and other payments that are equivalent in many respects to interchange payments.

The final major issue for the Review is concerns over excessive surcharging in some industries. There is a balance to be struck here between ensuring that merchants have the right to surcharge for expensive payment methods, including some cards, and ensuring that they do not surcharge excessively. Excessive surcharging is not a widespread problem, but I think we can all point to a few cases where there are genuine concerns. The Board is keen to take action here.

The Board discussed the Review in its August meeting and will be discussing it again at its November meeting. In preparation for discussions about possible changes in the regulatory framework, the Board has recently taken a decision to designate five payment systems: the American Express companion card system, the Debit MasterCard system and the eftpos, MasterCard and Visa prepaid card systems. Designation does not impose regulation nor does it commit the Bank to a regulatory course of action; rather it is the first of a number of steps the Bank must take to exercise any of its regulatory powers.

Any proposals to apply regulation to designated systems through standards or access regimes are subject to requirements for detailed consultation. Designation of these five systems will allow a more holistic consideration of the issues – including issues such as the regulatory treatment of companion cards and prepaid cards – as the Bank continues with review of the regulatory framework and considers the case for changes to the framework.

As you know, there has been a lot of discussion of the issues that the Review is focusing on. Banks, payment schemes, consumer organisations and merchants have been able to express views in four different contexts: the original FSI call for submissions, submissions on the FSI’s interim report, the Government’s call for comments on the FSI Final Report, and responses to the Bank’s Issues Paper. And in turn, the industry will have seen the Bank’s views in at least three different vehicles: the Bank’s two submissions to the FSI in 2014 and its Issues Paper from March this year.

We have received over 40 submissions in response to the Issues Paper, with all non-confidential submissions published on our website. The Bank also hosted an industry roundtable in June and has held around 40 meetings with stakeholders.

Overall, there appear to be some areas where there is common ground across most stakeholders. For example, there is fairly wide acceptance that the widening of the international schemes’ interchange fee schedules has created issues in terms of the rising cost of card payments to nonpreferred merchants and the declining transparency of the cost of card payments to them. There is also general agreement that it would be good to deal with instances of excessive surcharging.

However, there are other areas where there are real differences in the views expressed by different stakeholders. These include issues such as whether companion card arrangements should be subject to regulation and whether there might be a case for a reduction in the interchange fee benchmarks.

It will be up to the Board to weigh up the arguments on some of these contentious issues, balancing the interests of consumers, businesses, financial institutions and card schemes. As always, its consideration will be based on its mandate to promote competition and efficiency in the payments system. And let me stress again that if the Board decides to propose changes to the regulatory framework, the Bank will, as usual, undertake a thorough consultation process on any draft standards.

Finally, as you will know, the Government released its response to the FSI yesterday. Its response referred to the Bank’s review and noted that it was looking forward to the Board completing its work on the issues of interchange fees and surcharging. The Government also indicated that it will ban excessive surcharging and give the ACCC enforcement power in this area. I would expect that once the Board has provided greater clarity on what constitutes excessive surcharging, we will work closely with Treasury and the ACCC on legislation. I expect that we will end up with a framework where the Board has decided on a narrower definition of costs of acceptance and allowable surcharges and where the Bank will be able to count on help from the ACCC in the enforcement of the new framework.

Customers using their Android phone for ‘tap and pay’ purchases are most likely to be buying their groceries or a takeaway meal, spending an average of $27 per transaction, according to new data to be released by CUA at a national conference in Melbourne. By way of background, CUA originally was formed as a credit union in Queensland in the 1940s with just 180 members. Since then, through the amalgamation of more than 160 credit unions, they have become Australia’s “largest customer-owned financial institution”, with more than 400,000 customers, over 900 employees and $9 billion in assets under management.

In July last year, customer-owned financial institution CUA became the first banking provider in the Asia-Pacific to roll out a free mobile app using HCE technology, which allowed customers to ‘tap and pay’ with any compatible Android phone. The mobile app – CUA redi2PAY – was developed by CUA’s payments provider Cuscal and works on any NFC-enabled Android phone running on KitKat 4.4 or later.

CUA Head of Customer Insights Chris Malcolm and Cuscal Head of EFT, Acquiring and Digital Colin Sultana will share insights into how customers are using their ‘mobile wallets’ as part of a case study on the redi2PAY implementation at the Australian Cards and Payments Summit taking place at the Melbourne Convention & Exhibition Centre today.

Mr Malcolm said groceries were the top retail category for redi2PAY transactions, followed by fast food, petrol stations, restaurants/ dining and alcohol purchases.

“Interestingly, the top five retail categories for redi2PAY mobile payments are the exact same retail categories where CUA customers make the highest number of Visa PayWave purchases using their debit card,” he said.

“It appears that CUA’s early adopters of mobile payments technology are literally swapping their debit card for their mobile phone, using it for the same kind of purchases as they would have made with a traditional plastic card.”

Customers using redi2PAY are also using it more frequently – the number of customers using redi2PAY more than 35 times per month was around three times higher in March than it was six months earlier in October. The number of customers using mobile payments semi-regularly (5 to 14 times per month) is up 63 per cent for the same period.

The data also shows:

Customers spend an average of $27 per transaction when using CUA redi2PAY – the same as the average amount for Visa PayWave purchases.

The number of redi2PAY transactions spikes towards the end of the week (Thursday to Saturday). Saturday has the highest number of redi2PAY transactions, while Sunday has the least. Visa PayWave transactions also peak on Saturday, while Monday has the lowest number of payments.

Most mobile payments occur between 12pm and 8pm, with a spike from 1-2pm. The trend is similar for Visa PayWave payments.

The number of redi2PAY transactions each month has increased by more than 16 per cent since September 2014.

December 2014 recorded the highest value of redi2PAY transactions for a single month, coinciding with the lead up to Christmas.

CUA and Cuscal have already been recognised in Australia and Asia as pioneers in mobile payments. A leading financial research company in Asia, IDC, recently named CUA redi2PAY as one of the top 25 mobile innovations in financial services for 2014-15.

“There is huge potential for this technology to fundamentally change how people pay for purchases,” Mr Malcolm said.

“People tend to take their smart phones everywhere they go and now, the need to also carry cash and cards in your wallets is becoming a thing of the past.”

He said approximately eight times more CUA customers now have a compatible Android phone which could be used for redi2PAY, compared to a relatively small group of customers who had the required technology when redi2PAY was launched 10 months ago.

“We’re seeing increased take-up of this HCE technology across the banking sector, as others follow our lead. The use of ‘mobile wallets’ will only continue to grow as customers become more familiar with the technology and its security features, and upgrade their Android devices to the latest models.”

TOP 10 RETAIL CATEGORIES – redi2PAY vs Visa PayWave

After many decades, it’s still interesting to watch Apple continue to push the envelope around its primary business model.

Apple Watch is a prime example, as it plunges the brand deeply into the fashion world as well as the personal tech sphere that it already dominates. Intriguing new wrinkles include the just-uncovered fact that a loophole in security would hypothetically allow a thief to use someone else’s Apple Watch to make Apple Pay payments with the owner’s credit card data, according to PhoneArena.com.

While the Apple Watch launch may have somewhat overshadowed the company’s Apple Pay platform, the latter’s list of participating vendors keeps expanding—including its newest addition, Cole Haan.

“The Cole Haan enthusiast is on the go and online at all times,” said David Maddocks, chief marketing officer at Cole Haan, in a press release. “The mobile wallet in our popular mobile application made perfect sense for the Cole Haan customer who wants to stay stylish at the touch of a button.”

Las Vegas is getting in on the Apple action as well. Apple Pay is now making its way to The Cosmopolitan hotel and casino there, where consumers will be able to use it at the front desk, restaurants and bars. According to Digital Trends, however, it can’t be used to buy chips for gambling—yet.

All of that may be table stakes, though, compared with Apple’s biggest target for Apple Pay: China.

China is Apple’s second-biggest market by revenues and snaps up more iPhones now than the US, according to CNBC. “We very much want to get Apple Pay in China,” CEO Tim Cook told a Chinese news agency.

The company reportedly is in talks with Alibaba about bringing Apple Pay to China using Alibaba’s Alipay to process transactions. Apple has been eying the China market for some time, according to Zack’s.com, but regulatory hurdles have made it difficult for the company to enter the market.

As with smartphones, Samsung looms as a formidable competitor in mobile-pay systems after its acquisition earlier this year of Massachusetts-based startup LoopPay, according to Recode.net. The price, it was reported, was $250 million.

Will that be enough for Samsung to arm wrestle with Apple Pay as its smartphones have done with iPhones? The answer likely will come quickly.

Optus today announced a proof of concept (POC) that uses wearable technology to enable mobile payments on Apple and Android handsets via the Cash by Optus app. Cash by Optus is a contactless payment app, powered by Visa payWave, which allows customers to use a compatible smartphone to pay for goods and services instead of using cash or plastic debit and credit cards.

This next evolution of Cash by Optus enables contactless payments across multiple platforms. It uses wearable technology – a connected watch or a wristband – linked to an Android or Apple handset. Payments can be made using only the wearable without the linked phone nearby. When in close range, the connected watch and linked smartphone sync up via Bluetooth to update the account balance on the connected watch and transaction details on the linked phone.

Optus was the first Australian telco to launch a mobile payments app late last year, on Android, but wearable is designed to work on both Apple and Android smartphones. Launched in collaboration with Visa and Heritage Bank, Cash by Optus uses Near Field Communication (NFC) and Visa payWave technology that can replace cash purchases below $100.

Cash by Optus works just like a Visa Prepaid debit card. Customers can load up to $500 at any one time and make contactless purchases under $100 at any of the hundreds of thousands of retailers that accept Visa payWave. To get access to Cash by Optus, customers need an Optus mobile service on a monthly plan, a compatible Android smartphone, a NFC enabled SIM and the Cash by Optus app. Cash by Optus is now available for over 110 compatible Android devices across 10 different vendors – an increase from 25 compatible devices at launch last year. The app uses Visa payWave technology, which features the international EMV chip standard, and provides some of the most widely adopted cryptographic security.

Cash by Optus speeds up the transaction process and makes payments even more convenient compared to fumbling with cash and heavy change. Australians are leading the world in their usage of contactless payments with over 75 million Visa payWave transactions in January 2015. In fact, more than half (60%) of face-to-face Visa transactions in Australia are made using Visa payWave. Cash by Optus will continue to evolve as compatibility with platforms, devices and systems grows. Future applications of Cash by Optus could extend to the prepaid mobile market and to other sectors including public transport.

What is machine learning?

What is machine learning?